Professional & Career Development

ACCA 15 Questions & Answers: SBL, SBR and AFM Papers

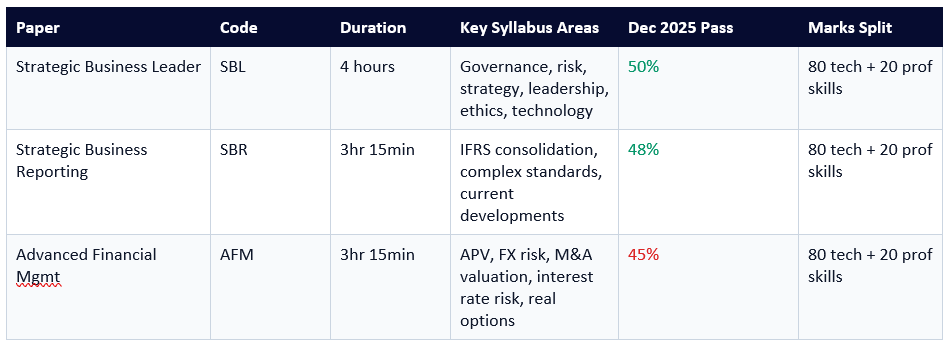

Strategic Business Leader (SBL), Strategic Business Reporting (SBR), and Advanced Financial Management (AFM) represent three of the most intellectually demanding papers in the ACCA qualification. SBL is a four-hour integrated case study that tests leadership, governance, risk, and strategy simultaneously — requiring candidates to think and write like a senior adviser to a board. SBR demands mastery of complex IFRS standards applied to multi-entity reporting scenarios. AFM requires fluency in advanced financial modelling, risk management, and strategic financial decisions. Together, they prepare candidates for the most senior levels of the accountancy and finance profession. This guide delivers 15 questions — five per paper — drawn directly from the syllabus areas and scenario types that recent exam sittings have tested, each paired with a concise, structured model answer built from official examiner reports, ACCA guidance, and current syllabus materials.

SBL and SBR are the two compulsory Strategic Professional papers — every ACCA candidate must pass both. AFM is one of four optional papers (alongside APM, ATX, and AAA) from which candidates choose two. Together, these three papers span the full breadth of strategic financial leadership: integrating governance, ethics, strategy, and leadership (SBL); mastering complex IFRS financial reporting (SBR); and applying advanced financial modelling and risk management (AFM).

Strategic Business Leader is the only four-hour ACCA examination. It is a unique integrated case study in which ALL tasks relate to a single organisation described through pre-seen materials published weeks before the exam and unseen exhibits revealed on the day. Every task requires the candidate to apply knowledge directly to the scenario — models, frameworks, and technical knowledge earn zero marks if they are not applied to the specific context. ACCA awards 20 out of 100 marks for professional skills: communication, commercial acumen, analysis and evaluation, and professional scepticism and judgement.

Strategic Business Reporting builds directly on the Financial Reporting paper and tests the full scope of IFRS in complex, multi-entity scenarios. From September 2025, IFRS 18 (Presentation and Disclosure in Financial Statements) replaced IAS 1 and is now examinable — introducing new income statement categories, management-defined performance measures, and revised disclosure requirements. The SBR pass rate has ranged between 48% and 50% in recent sittings, consistent with the long-run average of 46–52% since the paper launched in 2018.

Advanced Financial Management covers investment appraisal (APV, real options), risk management (FX, interest rate, commodity risk), business valuation, mergers and acquisitions, and treasury management in multinational corporations. The AFM March/June 2025 Examiner's Report noted strong candidate performance in calculations but significant underperformance in discussion-based questions requiring commercial awareness and professional scepticism — a consistent pattern across recent sittings.

Sources: ACCA Global official pass rates · Eduyush ACCA Subjects 2026 · Learnsignal SBR Pass Rate History (March 2026) · Quintedge ACCA Pass Rates 2026.

Political factors: include government policy stability, trade regulations, taxation regimes, public spending priorities, and geopolitical risk. For example, a company expanding into an emerging market must evaluate political risk (expropriation, sanctions, regulatory reversal) and how that affects the risk profile of the investment decision being brought to the board.

Economic factors: include GDP growth, inflation, interest rates, consumer confidence, and unemployment. For a consumer goods company, rising interest rates reduce disposable income and increase borrowing costs — implications that must be connected to the company's strategic response: pricing, product mix, or cost structure.

Social factors: include demographic shifts, changing consumer attitudes, workforce changes, and cultural values. A business with an ageing workforce must plan for skills transfer, succession, and talent pipeline development at board level.

Technological factors: cover digital transformation, automation, AI, cybersecurity risk, and platform disruption. The SBL examiner consistently rewards candidates who connect technology trends directly to competitive positioning — not just a list of technologies.

Environmental factors: cover climate change, carbon obligations, ESG investor expectations, and resource scarcity. Post-2025, sustainability and climate-related financial disclosures (aligned with IFRS S1 and S2) are increasingly tested in SBL scenarios.

Legal factors: cover employment law, data protection (GDPR), intellectual property, contract law, and sector-specific regulations.

► SBL Examiner insight (June 2024 Report, GlobalAPC): Candidates who wrote generic PESTEL essays without referencing the scenario's specific exhibits consistently scored below passing. Credit is awarded exclusively for applying each factor to the organisation's strategic context using evidence from the pre-seen and unseen materials.

► Risk oversight — the board does not manage risk directly, but ensures that effective risk management frameworks are in place, that risks are identified and monitored, and that risk appetite is clearly defined and communicated.

► Internal controls oversight — the board is responsible for the design and effectiveness of internal control systems, including financial controls, compliance, and IT governance.

► Accountability and transparency — boards must ensure financial reporting is accurate, disclosures are complete, and stakeholders receive timely, relevant information.

► The UK Corporate Governance Code (and equivalents in other jurisdictions) recommends at least 50% of the board (excluding the chair) should be independent NEDs for premium-listed companies.

► Key board committees — Audit, Remuneration, Nomination — must be chaired by independent NEDs to ensure independence of decision-making on matters where executive interests could conflict.

► SBL exam scenarios frequently test governance failures: a CEO who also chairs the board, remuneration packages not aligned with performance, or audit committees lacking financial expertise.

► They fail to capture value creation from intangible assets — brand reputation, human capital, supply chain relationships, innovation pipelines — that often represent the majority of a company's market value in knowledge-intensive industries.

► They provide limited transparency on environmental and social impacts that increasingly influence stakeholder confidence, regulatory risk, and long-term business sustainability.

► Forward-looking information: how the organisation intends to create value in the short, medium, and long term.

► The Integrated Thinking Principle: IR is not just a reporting framework — it requires the organisation to embed integrated thinking into governance and decision-making, breaking down silos between financial, operational, HR, and sustainability functions.

► SBL candidates must be able to advise the board on what sustainability information to disclose, why it matters to investors and other stakeholders, and how it connects to the organisation's integrated value creation narrative.

► High power, low interest (KEEP SATISFIED): meet their needs proactively to prevent them becoming blockers. Regulators typically sit here — they have the power to prevent the strategy but low day-to-day interest unless something triggers their attention.

► Low power, high interest (KEEP INFORMED): regular, clear communication. Local communities or NGOs watching an environmental project have high interest but limited ability to block decisions.

► Low power, low interest (MONITOR): minimal effort — periodic updates only.

► Assess whether stakeholder concerns represent genuine strategic risks (e.g., reputational damage from community opposition, regulatory intervention triggered by media coverage) that require the board to modify its approach.

► Recommend specific engagement strategies — not generic 'communicate with stakeholders' — but specific: investor briefings, community consultations, employee engagement sessions, or regulatory pre-submission meetings.

► SBL Examiner's Report (June 2024): Task 2a asked about CSR's impact on specific stakeholders. Many candidates wrote broad essays on CSR theory rather than analysing how CSR affected the specific stakeholders in the scenario. This approach — theory without application — consistently fails to achieve the required marks.

► Change: implement the new processes, structures, systems, or behaviours. The change must be managed as a structured programme with clear milestones, resource allocation, and accountability.

► Refreeze: embed the changes in culture, processes, and performance management so they become the new norm. Without refreezing, organisations revert to old behaviours after the initial change energy dissipates.

► The board's specific responsibilities in Kotter's model: creating urgency (step 1), building the guiding coalition by appointing the right change leadership team (step 2), and institutionalising change by updating governance structures and performance metrics (step 8).

► Structural change without cultural change consistently fails — the board must identify which cultural elements support the new strategy and which create resistance.

► The SBL examiner rewards answers that recommend specific actions to address identified cultural barriers — not just the observation that culture must change.

► Step 2 — Identify the performance obligations (POs): a PO is a distinct good or service — capable of being distinct (customer can benefit from it independently) AND distinct in the context of the contract (not highly integrated with other items). In multi-element contracts, each separately distinct item is a separate PO.

► Step 3 — Determine the transaction price: includes fixed consideration, variable consideration (constrained to the extent probable of no significant reversal — a key judgement area), non-cash consideration, and consideration payable to the customer.

► Step 4 — Allocate the transaction price to POs: allocate based on standalone selling prices (SSP). If SSP is not directly observable, estimate using the expected cost plus margin method, adjusted market assessment approach, or residual approach.

► Step 5 — Recognise revenue when (or as) each PO is satisfied: either at a point in time (customer obtains control) or over time (if criteria in IFRS 15.35 are met — e.g., customer simultaneously receives and consumes benefits, or the asset has no alternative use and the entity has a right to payment for work performed to date).

► Licences: licences of IP recognised at a point in time (right to use) vs. over time (right to access) depending on whether the underlying IP is expected to change.

► Contract modifications: treat as a new contract if adding distinct goods/services at standalone price; otherwise, adjust existing contract cumulatively or prospectively depending on whether remaining POs are distinct.

► Derecognise the non-controlling interest (NCI) at its carrying amount.

► Recognise the fair value of any consideration received.

► Recognise the fair value of any retained interest at the date control is lost.

► Reclassify to profit or loss any amounts previously recognised in OCI (e.g., foreign currency translation reserves, revaluation surplus if a policy election is not permitted) — this reclassification is often missed by candidates.

► Recognise any resulting gain or loss in profit or loss.

► This remeasurement to fair value is a deemed disposal and deemed reacquisition — a critical concept that SBR candidates frequently omit.

Part-year consolidation:

► If the disposal occurs mid-year, include the subsidiary's results in the consolidated income statement only up to the date control was lost — time-apportion income and expenses to the disposal date.

► SBR Examiner consistent feedback: errors in the gain on disposal calculation (particularly forgetting to include goodwill and reclassify OCI) and failure to time-apportion results are the most common sources of mark loss in disposal questions.

► ROU asset = lease liability + initial direct costs + prepaid lease payments − lease incentives received + estimated costs to restore the asset.

► ROU asset: depreciated on a straight-line basis (typically over the shorter of the lease term and the asset's useful life); tested for impairment under IAS 36.

► All other modifications: remeasure the lease liability at a revised discount rate (using the remaining term and revised payments) and adjust the ROU asset accordingly.

► If the transfer is NOT a sale (seller-lessee retains the risks and rewards): do NOT derecognise the asset. Recognise a financial liability equal to the proceeds received. This is a secured borrowing, not a sale.

► The correct identification of whether a sale has occurred (applying IFRS 15 transfer of control criteria) is the critical first step — errors here cascade through the entire subsequent accounting.

► Calculate the carrying amount of the CGU: all assets allocated to the CGU including the goodwill allocated to it.

► Calculate the recoverable amount: higher of FVLCD and VIU. VIU = present value of future pre-tax cash flows expected from the CGU, discounted at a pre-tax rate reflecting current market assessments of the time value of money and the risks specific to the asset.

► Impairment loss = Carrying amount − Recoverable amount (if carrying amount exceeds recoverable amount).

► Then, reduce other assets in the CGU pro-rata on the basis of their carrying amounts — but no individual asset is reduced below the higher of its FVLCD, its VIU, or zero.

► Goodwill impairment CANNOT be reversed — once recognised, it is permanent.

► Fair Value through Other Comprehensive Income (FVOCI): held for collecting contractual cash flows AND selling; SPPI test passes. Gains and losses recognised in OCI and recycled to P&L on derecognition. Also: equity instruments designated at FVOCI (irrevocable election — gains/losses NEVER recycled to P&L).

► Fair Value through Profit or Loss (FVTPL): all other financial assets, or assets designated at FVTPL (to eliminate accounting mismatch). Changes in fair value recognised in P&L each period.

► Three-stage model for financial assets at amortised cost and FVOCI:

► Stage 1 (no significant increase in credit risk since initial recognition): recognise 12-month ECL (expected losses from default events possible within 12 months). Effective interest calculated on gross carrying amount.

► Stage 2 (significant increase in credit risk): recognise lifetime ECL. Effective interest still on gross carrying amount.

► Stage 3 (credit-impaired — objective evidence of impairment): recognise lifetime ECL. Effective interest calculated on net carrying amount (i.e., carrying amount after deducting the allowance).

► Simplified approach for trade receivables, contract assets, and lease receivables: lifetime ECL always applied (no staging required) — entities may use a provision matrix based on historical loss rates adjusted for forward-looking factors.

► Common SBR exam error: applying the IAS 39 incurred loss approach instead of ECL; and failing to move assets between stages as credit quality changes.

► PV of tax shield: if permanent debt is used, PV of tax shield = Tax rate × Amount of debt (Modigliani-Miller). If debt is temporary or reduces, calculate the PV of annual tax savings: D × Kd × t, discounted at Kd (cost of debt) if the tax shield has the same risk as the debt.

► Other financing side effects: issue costs of new debt or equity (deduct), subsidised loan benefits (add), issue costs on retained earnings (nil).

► The project involves a heavily leveraged transaction where debt is repaid over the project life — WACC changes as the debt-to-equity ratio changes, making a single WACC unreliable.

► Cross-border investments or projects with subsidised financing where financing terms are non-standard.

► The project involves issue costs, debt capacity changes, or other specific financing effects that are difficult to incorporate into a single WACC.

► AFM March/June 2025 Examiner's Report (ACCA official): Kampai Co question required candidates to calculate APV, ungear the beta using Modigliani-Miller, calculate the ungeared Ke using CAPM, compute the base-case NPV, and add PV of tax shield. Candidates who confused APV steps with WACC steps, or discounted tax shield at the wrong rate, lost significant marks.

► Matching: matching interest-bearing assets and liabilities in the same currency and term structure so changes in rates affect both sides equally.

► Netting: within a group, offsetting floating rate borrowings against floating rate deposits to reduce the net exposure.

► Benefit: liquid, transparent, exchange-margin system eliminates counterparty risk. Limitation: standardised contracts (quarterly expiry dates, fixed notional amounts) create basis risk and an imperfect hedge.

► Best used when: the company wants downside protection but is unwilling to forgo an upside benefit; uncertainty about whether the transaction will proceed (options can be abandoned if transaction does not materialise).

► Best used for: medium-to-long term, high-value exposures; converting existing floating rate debt to a fixed rate (or vice versa) without refinancing.

► Limitation: over-the-counter (OTC) — creates counterparty credit risk; difficult to exit before maturity without cost.

► Pe = exercise price (for real options: the present value of the investment cost).

► r = continuous risk-free interest rate.

► t = time to expiry of the option (in years).

► s = standard deviation of returns on the underlying asset (for real options: a proxy for project risk, often given in the question).

► d1 = [ln(Pa/Pe) + (r + s²/2)t] ÷ (s√t). d2 = d1 − s√t. N(d1), N(d2) = cumulative normal distribution probabilities for d1 and d2.

► Option to abandon: the value of the right to sell or shut down the project early and recover salvage value if performance is poor.

► Option to delay: the value of waiting before committing to an investment — valuable when the project's NPV is currently close to zero and more information will arrive.

► AFM Examiner's insight (Learnsignal, April 2025): Candidates performing well on real options questions correctly identify which real option type is present in the scenario (expand, abandon, or delay) BEFORE setting up the B-S formula, and explicitly interpret the final option value in the context of the board's investment decision.

► Revenue synergies: cross-selling opportunities, access to the target's customer base, product range extension, geographic market entry.

► Financial synergies: improved borrowing capacity (combined entity has stronger credit rating), tax benefits (utilising the target's tax losses), and lower WACC through optimal capital structure.

► Dividend Valuation Model (Gordon's Growth Model): P = D₁ ÷ (Ke − g). Suitable for dividend-paying targets with stable growth.

► Free Cash Flow to Equity (FCFE): discount projected FCFEs at the cost of equity. Appropriate when dividends are not a reliable guide to value.

► Asset-based valuation (net asset value): relevant for asset-intensive businesses or as a floor valuation. Adjusted NAV uses FV of assets.

► The bid premium paid is subject to market reaction — AFM candidates must evaluate whether the market will view the acquisition as value-creating or value-destructive.

► Money market hedge: replicate the forward rate by borrowing/lending in the foreign currency. Useful when forward markets are illiquid or when the company has natural foreign currency borrowing capacity.

► Currency futures: exchange-traded standardised contracts. Provides transparency and eliminates counterparty risk but creates basis risk and requires daily margin calls.

► Currency options: pay a premium for the right to deal at a fixed rate while retaining the benefit if rates move favourably. Most appropriate when cash flows are uncertain or when the company wants to benefit from favourable movements.

► The AFM examiner expects candidates to calculate the outcome under at least two hedging methods and then recommend which is preferable — with reasoning linked to the company's risk tolerance, cost, and certainty of the underlying transaction.

► Managed by: matching debt denomination with the currency of foreign assets (natural hedge), or using currency swaps to denominate borrowings in the foreign currency.

► AFM Examiner's Report (March/June 2025): Candidates performed well on forward market hedge calculations but frequently failed to address translation and economic risk adequately — missing marks available for the more strategic, discussion-based parts of FX questions.

For SBL, prioritise reading the latest pre-seen material thoroughly before practising — the scenarios change for every exam window. For SBR, ensure you work through at least one full past consolidation question under exam conditions before your sitting; errors in group accounts are compounding and time-consuming to correct. For AFM, balance calculation practice with essay technique — the examiner's reports from 2024 and 2025 consistently show that many candidates who pass the numerical parts of a question fail to earn the discussion marks that could have taken them comfortably above 50.

Pass rates across these three papers cluster between 45% and 53% in recent sittings — meaning that roughly half of all candidates who sit these exams do not pass on their first attempt. The candidates who do pass consistently share one characteristic: they answer the question actually set, not the question they prepared for. They apply knowledge to the scenario with specific evidence from the exhibits, and they communicate their analysis in the structured, professional format that the examiner's mark scheme rewards. These 15 questions and model answers are designed to help you build exactly those habits.

ACCA Global — Strategic Business Reporting (SBR) Pass Rates and Resources (Official) https://www.accaglobal.com/in/en/student/exam-support-resources/professional-exams-study-resources/strategic-business-reporting.html

ACCA Global — Advanced Financial Management (AFM) Pass Rates (Official) https://www.accaglobal.com/my/en/student/exam-support-resources/professional-exams-study-resources/p4.html

ACCA Global — AFM March/June 2025 Examiner's Report (Official PDF — Kampai Co, Sohbet Co, GCR Co) https://www.accaglobal.com/content/dam/acca/global/PDF-students/acca/p4/examinersreports/MJ25%20AFM%20examiner's%20report.pdf

The Accountant Online — ACCA March 2025 Exam Pass Rates (April 2025) https://www.theaccountant-online.com/news/acca-march-2025-pass-rates/

Eduyush — ACCA Subjects and Syllabus 2026: All 13 Papers, Pass Rates and Study Order (April 2026) https://eduyush.com/en-us/blogs/acca/acca-subjects

TABLE OF CONTENTS

- Understanding SBL, SBR, and AFM in the ACCA Qualification

- Paper 1: Strategic Business Leader (SBL) — 5 Questions

- Paper 2: Strategic Business Reporting (SBR) — 5 Questions

- Paper 3: Advanced Financial Management (AFM) — 5 Questions

- How to Use These Questions in Your Exam Preparation

- Conclusion

- Frequently Asked Questions

- References

Understanding SBL, SBR, and AFM in the ACCA Qualification

SBL and SBR are the two compulsory Strategic Professional papers — every ACCA candidate must pass both. AFM is one of four optional papers (alongside APM, ATX, and AAA) from which candidates choose two. Together, these three papers span the full breadth of strategic financial leadership: integrating governance, ethics, strategy, and leadership (SBL); mastering complex IFRS financial reporting (SBR); and applying advanced financial modelling and risk management (AFM).Strategic Business Leader is the only four-hour ACCA examination. It is a unique integrated case study in which ALL tasks relate to a single organisation described through pre-seen materials published weeks before the exam and unseen exhibits revealed on the day. Every task requires the candidate to apply knowledge directly to the scenario — models, frameworks, and technical knowledge earn zero marks if they are not applied to the specific context. ACCA awards 20 out of 100 marks for professional skills: communication, commercial acumen, analysis and evaluation, and professional scepticism and judgement.

Strategic Business Reporting builds directly on the Financial Reporting paper and tests the full scope of IFRS in complex, multi-entity scenarios. From September 2025, IFRS 18 (Presentation and Disclosure in Financial Statements) replaced IAS 1 and is now examinable — introducing new income statement categories, management-defined performance measures, and revised disclosure requirements. The SBR pass rate has ranged between 48% and 50% in recent sittings, consistent with the long-run average of 46–52% since the paper launched in 2018.

Advanced Financial Management covers investment appraisal (APV, real options), risk management (FX, interest rate, commodity risk), business valuation, mergers and acquisitions, and treasury management in multinational corporations. The AFM March/June 2025 Examiner's Report noted strong candidate performance in calculations but significant underperformance in discussion-based questions requiring commercial awareness and professional scepticism — a consistent pattern across recent sittings.

Sources: ACCA Global official pass rates · Eduyush ACCA Subjects 2026 · Learnsignal SBR Pass Rate History (March 2026) · Quintedge ACCA Pass Rates 2026.

RECOMMENDED STUDY HOURS — First-Time Candidates

- SBL: 200–250 hours — the four-hour case study format requires intensive scenario practice. Read and re-read the pre-seen; develop the habit of answering the ACTUAL question set, not the question you wish had been set.

- SBR: 150–200 hours — master the core IFRS standards (IFRS 3, IFRS 10, IFRS 15, IFRS 16, IAS 36, IFRS 9, and IFRS 18 from Sep 2025). Group accounts appear in virtually every sitting and errors cascade through entire questions.

- AFM: 160–200 hours — balance calculation practice with discussion technique. The March/June 2025 examiner noted candidates performed well in calculations but significantly underperformed in discussion-based parts requiring commercial awareness and scepticism.

Paper 1: Strategic Business Leader (SBL) — 5 Questions

SBL is entirely case-study based. The pre-seen material is published approximately six weeks before the exam. The unseen exhibits add new information on exam day. Every task refers to the specific organisation — abstract or generic answers score very little. The examiner consistently rewards candidates who use evidence from exhibits to support every analytical point they make.Q1 SBL How should a board apply the PESTEL framework strategically in an SBL scenario, and why does generic description fail to earn marks?

✦ PERFECT ANSWER

PESTEL is a macro-environmental analysis tool covering Political, Economic, Social, Technological, Environmental, and Legal factors. At SBL level, its purpose is NOT to list external factors — it is to evaluate which factors create the most significant strategic threats or opportunities for the specific organisation in the scenario, and to connect those factors to board-level strategic decisions.Political factors: include government policy stability, trade regulations, taxation regimes, public spending priorities, and geopolitical risk. For example, a company expanding into an emerging market must evaluate political risk (expropriation, sanctions, regulatory reversal) and how that affects the risk profile of the investment decision being brought to the board.

Economic factors: include GDP growth, inflation, interest rates, consumer confidence, and unemployment. For a consumer goods company, rising interest rates reduce disposable income and increase borrowing costs — implications that must be connected to the company's strategic response: pricing, product mix, or cost structure.

Social factors: include demographic shifts, changing consumer attitudes, workforce changes, and cultural values. A business with an ageing workforce must plan for skills transfer, succession, and talent pipeline development at board level.

Technological factors: cover digital transformation, automation, AI, cybersecurity risk, and platform disruption. The SBL examiner consistently rewards candidates who connect technology trends directly to competitive positioning — not just a list of technologies.

Environmental factors: cover climate change, carbon obligations, ESG investor expectations, and resource scarcity. Post-2025, sustainability and climate-related financial disclosures (aligned with IFRS S1 and S2) are increasingly tested in SBL scenarios.

Legal factors: cover employment law, data protection (GDPR), intellectual property, contract law, and sector-specific regulations.

► SBL Examiner insight (June 2024 Report, GlobalAPC): Candidates who wrote generic PESTEL essays without referencing the scenario's specific exhibits consistently scored below passing. Credit is awarded exclusively for applying each factor to the organisation's strategic context using evidence from the pre-seen and unseen materials.

Q2 SBL Explain the concept of corporate governance and why effective governance structures are critical in the SBL context.

✦ PERFECT ANSWER

Corporate governance is the system by which organisations are directed and controlled — defining the relationships between the board, management, shareholders, and other stakeholders. At SBL level, governance is examined through the lens of the board's responsibility to oversee strategy, manage risk, ensure accountability, and uphold ethical standards.The board's governance responsibilities:

► Setting and monitoring organisational strategy — ensuring the strategic direction serves the long-term interests of all stakeholders, not just short-term shareholder returns.► Risk oversight — the board does not manage risk directly, but ensures that effective risk management frameworks are in place, that risks are identified and monitored, and that risk appetite is clearly defined and communicated.

► Internal controls oversight — the board is responsible for the design and effectiveness of internal control systems, including financial controls, compliance, and IT governance.

► Accountability and transparency — boards must ensure financial reporting is accurate, disclosures are complete, and stakeholders receive timely, relevant information.

Board composition and independence:

► A unitary board (used in the UK) combines executive and non-executive directors. Non-executive directors (NEDs) provide independent challenge, scrutiny of management decisions, and connection to external stakeholder perspectives.► The UK Corporate Governance Code (and equivalents in other jurisdictions) recommends at least 50% of the board (excluding the chair) should be independent NEDs for premium-listed companies.

► Key board committees — Audit, Remuneration, Nomination — must be chaired by independent NEDs to ensure independence of decision-making on matters where executive interests could conflict.

Agency theory in governance:

► Agency theory identifies the conflict of interest between principals (shareholders) and agents (management). Governance mechanisms — remuneration linked to long-term performance, independent audit, shareholder voting rights — exist to align management behaviour with shareholder interests.► SBL exam scenarios frequently test governance failures: a CEO who also chairs the board, remuneration packages not aligned with performance, or audit committees lacking financial expertise.

Q3 SBL What is integrated reporting and how does it differ from traditional financial reporting for the purposes of SBL?

✦ PERFECT ANSWER

Integrated reporting (IR) is a framework developed by the IIRC (now part of IFRS Foundation) that presents a holistic picture of how an organisation creates value over time — encompassing financial AND non-financial capital. The International IR Framework defines six capitals: Financial, Manufactured, Intellectual, Human, Social and Relationship, and Natural.Why traditional financial reporting is insufficient for strategic decision-making:

► Traditional financial statements are backward-looking, reporting on historical financial performance using monetary measures only.► They fail to capture value creation from intangible assets — brand reputation, human capital, supply chain relationships, innovation pipelines — that often represent the majority of a company's market value in knowledge-intensive industries.

► They provide limited transparency on environmental and social impacts that increasingly influence stakeholder confidence, regulatory risk, and long-term business sustainability.

What integrated reporting provides:

► A connected narrative linking the organisation's strategic objectives, its business model, its operating environment (including the six capitals), the material risks and opportunities it faces, and its performance against strategic targets — all in a single concise report.► Forward-looking information: how the organisation intends to create value in the short, medium, and long term.

► The Integrated Thinking Principle: IR is not just a reporting framework — it requires the organisation to embed integrated thinking into governance and decision-making, breaking down silos between financial, operational, HR, and sustainability functions.

IFRS S1 and S2 in the SBL context:

► IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures), effective for periods beginning 1 January 2024, are increasingly tested in SBL scenarios where boards must decide on sustainability disclosure strategy.► SBL candidates must be able to advise the board on what sustainability information to disclose, why it matters to investors and other stakeholders, and how it connects to the organisation's integrated value creation narrative.

Q4 SBL How should an organisation conduct and apply a stakeholder analysis in an SBL board-level scenario?

✦ PERFECT ANSWER

Stakeholder analysis at SBL level requires candidates to identify ALL groups affected by a strategic decision, assess their POWER and INTEREST in the outcome, and recommend specific board-level responses to manage each stakeholder group effectively.Mendelow's Power-Interest Matrix:

► High power, high interest (KEY PLAYERS): manage closely and continuously. These stakeholders can both block strategic initiatives and actively enable them — they require direct engagement, consultation, and ongoing communication. For a listed company considering a major acquisition, institutional investors and the acquiree's board fall into this quadrant.► High power, low interest (KEEP SATISFIED): meet their needs proactively to prevent them becoming blockers. Regulators typically sit here — they have the power to prevent the strategy but low day-to-day interest unless something triggers their attention.

► Low power, high interest (KEEP INFORMED): regular, clear communication. Local communities or NGOs watching an environmental project have high interest but limited ability to block decisions.

► Low power, low interest (MONITOR): minimal effort — periodic updates only.

Connecting stakeholder analysis to board decisions:

► Identify which stakeholders are MOST affected by the proposed strategic change and what their likely reaction will be.► Assess whether stakeholder concerns represent genuine strategic risks (e.g., reputational damage from community opposition, regulatory intervention triggered by media coverage) that require the board to modify its approach.

► Recommend specific engagement strategies — not generic 'communicate with stakeholders' — but specific: investor briefings, community consultations, employee engagement sessions, or regulatory pre-submission meetings.

► SBL Examiner's Report (June 2024): Task 2a asked about CSR's impact on specific stakeholders. Many candidates wrote broad essays on CSR theory rather than analysing how CSR affected the specific stakeholders in the scenario. This approach — theory without application — consistently fails to achieve the required marks.

Q5 SBL Explain change management frameworks and how a board should lead strategic change effectively according to SBL principles.

✦ PERFECT ANSWER

Strategic change management is one of the highest-value topic areas in SBL, regularly appearing in both pre-seen scenarios and unseen case materials. The board's role in change is not merely to authorise a change programme — it is to lead, communicate, govern, and sustain the transformation.Lewin's Three-Stage Model (Unfreeze — Change — Refreeze):

► Unfreeze: create awareness of the need for change by communicating the burning platform — why the current state is unsustainable. This requires the board to be transparent about performance data, competitive threats, or regulatory obligations that make the status quo untenable.► Change: implement the new processes, structures, systems, or behaviours. The change must be managed as a structured programme with clear milestones, resource allocation, and accountability.

► Refreeze: embed the changes in culture, processes, and performance management so they become the new norm. Without refreezing, organisations revert to old behaviours after the initial change energy dissipates.

Kotter's Eight-Step Change Model (for complex transformational change):

► (1) Create urgency; (2) Build a guiding coalition; (3) Form a strategic vision; (4) Enlist a volunteer army; (5) Enable action by removing barriers; (6) Generate short-term wins; (7) Sustain acceleration; (8) Institute change.► The board's specific responsibilities in Kotter's model: creating urgency (step 1), building the guiding coalition by appointing the right change leadership team (step 2), and institutionalising change by updating governance structures and performance metrics (step 8).

Cultural change — Johnson's Cultural Web:

► To sustain strategic change, the board must understand and deliberately reshape the cultural web: the Paradigm (shared assumptions), Stories (organisation's history and heroes), Routines and Rituals, Organisational Structure, Control Systems, and Symbols.► Structural change without cultural change consistently fails — the board must identify which cultural elements support the new strategy and which create resistance.

► The SBL examiner rewards answers that recommend specific actions to address identified cultural barriers — not just the observation that culture must change.

Paper 2: Strategic Business Reporting (SBR) — 5 Questions

SBR Section A is a compulsory case study question worth 50 marks. Section B contains two 25-mark questions, both compulsory. From September 2025, IFRS 18 is examinable — replacing IAS 1 and introducing significant changes to income statement presentation. The SBR pass rate has been 48–50% in recent sittings, with consolidated statements and complex IFRS standards the dominant content area in every exam.Q6 SBR How does IFRS 15 (Revenue from Contracts with Customers) apply to complex multi-element contracts in an SBR exam scenario?

✦ PERFECT ANSWER

IFRS 15 establishes a single five-step model for recognising revenue across all industries. At SBR level, the focus is on the application of these five steps to complex scenarios: bundled products and services, variable consideration, significant financing components, licences, and contract modifications.The five-step model:

► Step 1 — Identify the contract(s) with a customer: the contract must be approved by both parties, create enforceable rights and obligations, have commercial substance, and make collection of consideration probable.► Step 2 — Identify the performance obligations (POs): a PO is a distinct good or service — capable of being distinct (customer can benefit from it independently) AND distinct in the context of the contract (not highly integrated with other items). In multi-element contracts, each separately distinct item is a separate PO.

► Step 3 — Determine the transaction price: includes fixed consideration, variable consideration (constrained to the extent probable of no significant reversal — a key judgement area), non-cash consideration, and consideration payable to the customer.

► Step 4 — Allocate the transaction price to POs: allocate based on standalone selling prices (SSP). If SSP is not directly observable, estimate using the expected cost plus margin method, adjusted market assessment approach, or residual approach.

► Step 5 — Recognise revenue when (or as) each PO is satisfied: either at a point in time (customer obtains control) or over time (if criteria in IFRS 15.35 are met — e.g., customer simultaneously receives and consumes benefits, or the asset has no alternative use and the entity has a right to payment for work performed to date).

Common SBR exam issues under IFRS 15:

► Warranties: assurance-type warranties are not a separate PO; service-type warranties (providing a service beyond fixing defects) ARE a separate PO.► Licences: licences of IP recognised at a point in time (right to use) vs. over time (right to access) depending on whether the underlying IP is expected to change.

► Contract modifications: treat as a new contract if adding distinct goods/services at standalone price; otherwise, adjust existing contract cumulatively or prospectively depending on whether remaining POs are distinct.

Q7 SBR Explain the accounting treatment for group consolidation when a parent loses control of a subsidiary during the reporting period under IFRS 10.

✦ PERFECT ANSWER

The disposal of a subsidiary — resulting in loss of control — is one of the most technically demanding SBR topics and appears frequently in Section A consolidation scenarios. IFRS 10 and IFRS 3 govern the accounting when control is lost.Accounting on the date control is lost:

► Derecognise ALL assets (including goodwill) and liabilities of the subsidiary at their carrying amounts.► Derecognise the non-controlling interest (NCI) at its carrying amount.

► Recognise the fair value of any consideration received.

► Recognise the fair value of any retained interest at the date control is lost.

► Reclassify to profit or loss any amounts previously recognised in OCI (e.g., foreign currency translation reserves, revaluation surplus if a policy election is not permitted) — this reclassification is often missed by candidates.

► Recognise any resulting gain or loss in profit or loss.

Formula for the gain or loss on disposal:

► Gain / Loss = (Fair value of consideration received + Fair value of retained interest + Carrying amount of NCI) − Carrying amount of net assets of subsidiary (including goodwill allocated to that subsidiary)If a retained interest remains (e.g., associate or investment):

► The retained interest is remeasured to fair value at the date of disposal — this fair value becomes the new cost for subsequent accounting under IAS 28 (associate) or IFRS 9 (financial instrument).► This remeasurement to fair value is a deemed disposal and deemed reacquisition — a critical concept that SBR candidates frequently omit.

Part-year consolidation:

► If the disposal occurs mid-year, include the subsidiary's results in the consolidated income statement only up to the date control was lost — time-apportion income and expenses to the disposal date.

► SBR Examiner consistent feedback: errors in the gain on disposal calculation (particularly forgetting to include goodwill and reclassify OCI) and failure to time-apportion results are the most common sources of mark loss in disposal questions.

Q8 SBR What are the key accounting requirements under IFRS 16 (Leases) for lessees and how are sale and leaseback transactions treated?

✦ PERFECT ANSWER

IFRS 16, effective from 1 January 2019, fundamentally changed lessee accounting by requiring almost all leases to be recognised on the balance sheet as a right-of-use (ROU) asset and a lease liability. At SBR level, the most technically demanding aspects are variable lease payments, lease modifications, and sale and leaseback transactions.Initial recognition for lessees:

► Lease liability = present value of future lease payments (including fixed payments net of lease incentives; variable payments based on an index or rate; exercise price of a purchase option if reasonably certain; and penalties for early termination if the lessee is reasonably certain not to exercise a termination option).► ROU asset = lease liability + initial direct costs + prepaid lease payments − lease incentives received + estimated costs to restore the asset.

Subsequent measurement:

► Lease liability: unwound using the effective interest method (interest charged to P&L at the discount rate); reduced by lease payments made.► ROU asset: depreciated on a straight-line basis (typically over the shorter of the lease term and the asset's useful life); tested for impairment under IAS 36.

Lease modifications:

► If the modification grants a RIGHT TO USE an additional asset that is NOT already captured in the original lease, and the consideration equals the standalone price of the additional right — treat as a new, separate lease.► All other modifications: remeasure the lease liability at a revised discount rate (using the remaining term and revised payments) and adjust the ROU asset accordingly.

Sale and leaseback under IFRS 16:

► If the transfer of the asset IS a sale under IFRS 15: recognise only the proportion of the gain relating to the rights transferred (i.e., gain is restricted to the portion not retained through the leaseback). Recognise the ROU asset and lease liability for the rights retained.► If the transfer is NOT a sale (seller-lessee retains the risks and rewards): do NOT derecognise the asset. Recognise a financial liability equal to the proceeds received. This is a secured borrowing, not a sale.

► The correct identification of whether a sale has occurred (applying IFRS 15 transfer of control criteria) is the critical first step — errors here cascade through the entire subsequent accounting.

Q9 SBR How should an entity account for impairment of goodwill and other assets under IAS 36, and what are the common SBR exam pitfalls?

✦ PERFECT ANSWER

IAS 36 (Impairment of Assets) requires assets to be carried at no more than their recoverable amount — the higher of (a) Fair Value Less Costs of Disposal (FVLCD) and (b) Value in Use (VIU). Goodwill must be tested for impairment annually (or more frequently when indicators exist) by allocating it to Cash Generating Units (CGUs).The impairment test process:

► Identify the CGU: the smallest identifiable group of assets that generates independent cash inflows from continuing use. Goodwill cannot be tested in isolation — it must be allocated to CGUs.► Calculate the carrying amount of the CGU: all assets allocated to the CGU including the goodwill allocated to it.

► Calculate the recoverable amount: higher of FVLCD and VIU. VIU = present value of future pre-tax cash flows expected from the CGU, discounted at a pre-tax rate reflecting current market assessments of the time value of money and the risks specific to the asset.

► Impairment loss = Carrying amount − Recoverable amount (if carrying amount exceeds recoverable amount).

Allocation of impairment loss within a CGU:

► First, reduce goodwill allocated to the CGU to zero.► Then, reduce other assets in the CGU pro-rata on the basis of their carrying amounts — but no individual asset is reduced below the higher of its FVLCD, its VIU, or zero.

Corporate assets:

► Corporate assets (e.g., the group's head office, shared IT infrastructure) cannot generate independent cash flows. They must be allocated to CGUs or groups of CGUs and tested as part of those groups.Reversal of impairment losses:

► Reversals are permitted for assets other than goodwill (IAS 36.114) — recognised in profit or loss, restoring the asset's carrying amount up to what its depreciated historical cost would have been.► Goodwill impairment CANNOT be reversed — once recognised, it is permanent.

IFRS 18 (effective 1 January 2027; examinable from Sep 2025):

► The new income statement categories under IFRS 18 require impairment losses on goodwill to be presented in the 'investing' category — not in operating profit. This is a recent syllabus development that SBR candidates must reflect in their presentation answers.Q10 SBR How does IFRS 9 classify and measure financial instruments, and what is the expected credit loss (ECL) model for impairment?

✦ PERFECT ANSWER

IFRS 9 replaced IAS 39 and fundamentally reformed the classification, measurement, and impairment of financial assets. At SBR level, classification and ECL impairment are the most frequently examined aspects.Classification of financial assets — three categories:

► Amortised Cost: held for collecting contractual cash flows; cash flows are solely payments of principal and interest (SPPI test passes). Measured at amortised cost using the effective interest method. Typical examples: trade receivables, bonds held to maturity.► Fair Value through Other Comprehensive Income (FVOCI): held for collecting contractual cash flows AND selling; SPPI test passes. Gains and losses recognised in OCI and recycled to P&L on derecognition. Also: equity instruments designated at FVOCI (irrevocable election — gains/losses NEVER recycled to P&L).

► Fair Value through Profit or Loss (FVTPL): all other financial assets, or assets designated at FVTPL (to eliminate accounting mismatch). Changes in fair value recognised in P&L each period.

The Expected Credit Loss (ECL) model — impairment under IFRS 9:

► IFRS 9 replaced the IAS 39 incurred loss model (recognise impairment only when objective evidence of loss event exists) with a forward-looking expected loss model — recognising probable future losses before they crystallise.► Three-stage model for financial assets at amortised cost and FVOCI:

► Stage 1 (no significant increase in credit risk since initial recognition): recognise 12-month ECL (expected losses from default events possible within 12 months). Effective interest calculated on gross carrying amount.

► Stage 2 (significant increase in credit risk): recognise lifetime ECL. Effective interest still on gross carrying amount.

► Stage 3 (credit-impaired — objective evidence of impairment): recognise lifetime ECL. Effective interest calculated on net carrying amount (i.e., carrying amount after deducting the allowance).

► Simplified approach for trade receivables, contract assets, and lease receivables: lifetime ECL always applied (no staging required) — entities may use a provision matrix based on historical loss rates adjusted for forward-looking factors.

► Common SBR exam error: applying the IAS 39 incurred loss approach instead of ECL; and failing to move assets between stages as credit quality changes.

Paper 3: Advanced Financial Management (AFM) — 5 Questions

AFM Section A is a compulsory 50-mark question — typically a report combining multiple syllabus areas. Section B contains two compulsory 25-mark questions. The March/June 2025 examiner (Kampai Co, Sohbet Co, GCR Co) specifically highlighted that AFM rewards those who move beyond calculations to deliver commercially aware, strategically relevant recommendations, and exercise appropriate professional scepticism when evaluating management's assumptions.Q11 AFM How is Adjusted Present Value (APV) used in investment appraisal and when is it preferred over WACC-based NPV?

✦ PERFECT ANSWER

Adjusted Present Value (APV) is an investment appraisal technique that separates the value of a project into two components: (1) the base-case NPV assuming all-equity financing, and (2) the present value of financing side effects (most importantly the tax shield from debt). APV was developed by Stewart Myers and is particularly valuable when the financing structure of a project changes the appropriate discount rate significantly.The APV formula: APV = Base-case NPV + PV of financing side effects:

► Base-case NPV: discount the project's free cash flows using the ungeared cost of equity (Ke_u) — as if the project were entirely equity-financed. This isolates the value of the project's operating cash flows from the capital structure.► PV of tax shield: if permanent debt is used, PV of tax shield = Tax rate × Amount of debt (Modigliani-Miller). If debt is temporary or reduces, calculate the PV of annual tax savings: D × Kd × t, discounted at Kd (cost of debt) if the tax shield has the same risk as the debt.

► Other financing side effects: issue costs of new debt or equity (deduct), subsidised loan benefits (add), issue costs on retained earnings (nil).

When APV is superior to WACC-based NPV:

► The project has a DIFFERENT capital structure from the company as a whole — for example, a project financed with a specific loan where the gearing changes significantly.► The project involves a heavily leveraged transaction where debt is repaid over the project life — WACC changes as the debt-to-equity ratio changes, making a single WACC unreliable.

► Cross-border investments or projects with subsidised financing where financing terms are non-standard.

► The project involves issue costs, debt capacity changes, or other specific financing effects that are difficult to incorporate into a single WACC.

► AFM March/June 2025 Examiner's Report (ACCA official): Kampai Co question required candidates to calculate APV, ungear the beta using Modigliani-Miller, calculate the ungeared Ke using CAPM, compute the base-case NPV, and add PV of tax shield. Candidates who confused APV steps with WACC steps, or discounted tax shield at the wrong rate, lost significant marks.

Q12 AFM Explain the interest rate risk management techniques available to a corporate treasurer and when each is most appropriate.

✦ PERFECT ANSWER

Interest rate risk arises when a company's borrowings or deposits are subject to floating interest rates, exposing it to adverse rate movements. At AFM level, the corporate treasurer must evaluate the full range of hedging instruments and recommend the most appropriate for the specific scenario.Internal techniques (no external counterparty required):

► Smoothing: maintaining a mix of fixed and floating rate debt to reduce overall sensitivity to rate changes. Simple but provides incomplete protection.► Matching: matching interest-bearing assets and liabilities in the same currency and term structure so changes in rates affect both sides equally.

► Netting: within a group, offsetting floating rate borrowings against floating rate deposits to reduce the net exposure.

External derivatives — Interest Rate Futures:

► Standardised exchange-traded contracts (e.g., Short Sterling futures). The treasurer sells futures today (if borrowing — to protect against rising rates) and buys back when the borrowing rate is fixed.► Benefit: liquid, transparent, exchange-margin system eliminates counterparty risk. Limitation: standardised contracts (quarterly expiry dates, fixed notional amounts) create basis risk and an imperfect hedge.

Interest Rate Options (IRGs — Interest Rate Guarantees):

► Give the right but not the obligation to deal at a maximum (cap) or minimum (floor) rate. The treasurer pays a premium but retains the benefit if rates move favourably.► Best used when: the company wants downside protection but is unwilling to forgo an upside benefit; uncertainty about whether the transaction will proceed (options can be abandoned if transaction does not materialise).

Interest Rate Swaps (IRS):

► A bilateral agreement to exchange fixed-rate interest payments for floating-rate payments on a notional principal. Typically arranged via a bank.► Best used for: medium-to-long term, high-value exposures; converting existing floating rate debt to a fixed rate (or vice versa) without refinancing.

► Limitation: over-the-counter (OTC) — creates counterparty credit risk; difficult to exit before maturity without cost.

Caps, Floors, and Collars:

► A cap sets a maximum interest rate — the seller pays the difference when the reference rate exceeds the cap rate. A floor sets a minimum. A collar combines a cap and floor, reducing the net premium cost at the expense of limiting the benefit from favourable rate movements.Q13 AFM What is the Black-Scholes Option Pricing Model and how is it applied to value real options in capital investment decisions?

✦ PERFECT ANSWER

The Black-Scholes model (B-S) provides a mathematical formula for pricing European call options — options that can only be exercised at expiry. In AFM, it is used both to value traded financial options and, critically, to quantify the option value embedded in strategic capital investment decisions (real options).The Black-Scholes formula: C = Pa·N(d1) − Pe·e^(-rt)·N(d2):

► Pa = current price of the underlying asset (for real options: the present value of the future cash flows from the investment).► Pe = exercise price (for real options: the present value of the investment cost).

► r = continuous risk-free interest rate.

► t = time to expiry of the option (in years).

► s = standard deviation of returns on the underlying asset (for real options: a proxy for project risk, often given in the question).

► d1 = [ln(Pa/Pe) + (r + s²/2)t] ÷ (s√t). d2 = d1 − s√t. N(d1), N(d2) = cumulative normal distribution probabilities for d1 and d2.

Types of real options valued using B-S in AFM:

► Option to expand: the value of the right to invest additional capital if the initial project is successful — particularly relevant for staged investments.► Option to abandon: the value of the right to sell or shut down the project early and recover salvage value if performance is poor.

► Option to delay: the value of waiting before committing to an investment — valuable when the project's NPV is currently close to zero and more information will arrive.

Why real options analysis improves NPV analysis:

► Traditional discounted cash flow NPV assumes a single course of action committed at time zero. Real options analysis recognises that managers can respond dynamically to new information — expand successful projects, abandon failures, delay uncertain commitments — generating additional value that DCF ignores.► AFM Examiner's insight (Learnsignal, April 2025): Candidates performing well on real options questions correctly identify which real option type is present in the scenario (expand, abandon, or delay) BEFORE setting up the B-S formula, and explicitly interpret the final option value in the context of the board's investment decision.

Q14 AFM How does the AFM examiner expect candidates to evaluate a proposed merger or acquisition — covering synergies, valuation, and post-merger integration?

✦ PERFECT ANSWER

Mergers and acquisitions (M&A) is one of the highest-weighted topics in AFM, regularly appearing in Section A. The AFM examiner expects candidates to move well beyond NPV calculations — analysing strategic rationale, identifying synergy sources, applying multiple valuation approaches, assessing the bid structure, and evaluating post-merger integration risks.Strategic rationale — why acquire?:

► Cost synergies: eliminate duplicated functions (back-office, distribution, management layers), achieve purchasing economies, and rationalise production capacity.► Revenue synergies: cross-selling opportunities, access to the target's customer base, product range extension, geographic market entry.

► Financial synergies: improved borrowing capacity (combined entity has stronger credit rating), tax benefits (utilising the target's tax losses), and lower WACC through optimal capital structure.

Business valuation methods for M&A:

► Price Earnings (P/E) approach: apply acquirer's (or sector) P/E ratio to the target's earnings. Simple but sensitive to the choice of P/E multiple and definition of earnings.► Dividend Valuation Model (Gordon's Growth Model): P = D₁ ÷ (Ke − g). Suitable for dividend-paying targets with stable growth.

► Free Cash Flow to Equity (FCFE): discount projected FCFEs at the cost of equity. Appropriate when dividends are not a reliable guide to value.

► Asset-based valuation (net asset value): relevant for asset-intensive businesses or as a floor valuation. Adjusted NAV uses FV of assets.

The maximum price to pay: the MBO/merger premium calculation:

► Maximum price = value of combined entity post-synergy − value of acquirer standalone. Any premium above this destroys acquirer shareholder value.► The bid premium paid is subject to market reaction — AFM candidates must evaluate whether the market will view the acquisition as value-creating or value-destructive.

AFM March/June 2025 Examiner's Report (Sohbet Co question):

► The examiner noted that candidates who only calculated NPV without evaluating the strategic rationale, synergy risks, and financing implications scored significantly below passing. Integration risk, management distraction, and cultural incompatibility are M&A risks that earn marks for discussion — but only when linked to the specific scenario facts.Q15 AFM Explain how a multinational company should manage foreign exchange (FX) transaction risk, translation risk, and economic risk.

✦ PERFECT ANSWER

Foreign exchange risk is the most consistently examined topic in AFM Section B. The AFM examiner expects candidates to distinguish clearly between the three types of FX risk and apply the full range of hedging tools — including forward contracts, futures, options, and money market hedges — with appropriate evaluation of each.Transaction risk: the risk that the SETTLEMENT VALUE of a known future foreign currency cash flow changes due to exchange rate movements:

► Forward market hedge: lock in a fixed exchange rate today for the future transaction. Simple, certain outcome, widely used for large commercial transactions. Limitation: no upside if rates move favourably.► Money market hedge: replicate the forward rate by borrowing/lending in the foreign currency. Useful when forward markets are illiquid or when the company has natural foreign currency borrowing capacity.

► Currency futures: exchange-traded standardised contracts. Provides transparency and eliminates counterparty risk but creates basis risk and requires daily margin calls.

► Currency options: pay a premium for the right to deal at a fixed rate while retaining the benefit if rates move favourably. Most appropriate when cash flows are uncertain or when the company wants to benefit from favourable movements.

► The AFM examiner expects candidates to calculate the outcome under at least two hedging methods and then recommend which is preferable — with reasoning linked to the company's risk tolerance, cost, and certainty of the underlying transaction.

Translation risk: the risk that reported consolidated financial statements are adversely affected by movements in exchange rates when converting foreign subsidiary balances:

► Not a cash flow risk — assets and liabilities do not change because of exchange rate translation. However, it affects reported net assets and earnings per share, which can influence credit ratings and investor perceptions.► Managed by: matching debt denomination with the currency of foreign assets (natural hedge), or using currency swaps to denominate borrowings in the foreign currency.

Economic (operating) risk: the long-term impact of exchange rate movements on a company's competitive position and future cash flows:

► The most significant but hardest-to-hedge FX risk. Structural responses include: diversifying production locations, sourcing inputs locally in foreign markets, diversifying the revenue base across multiple currencies, and building pricing flexibility into contracts.► AFM Examiner's Report (March/June 2025): Candidates performed well on forward market hedge calculations but frequently failed to address translation and economic risk adequately — missing marks available for the more strategic, discussion-based parts of FX questions.

How to Use These Questions in Your Exam Preparation

Each of the 15 questions in this guide maps directly onto the content areas most consistently examined across recent SBL, SBR, and AFM sittings. Treat each model answer as a framework for how a strong exam answer is structured — not a script to memorise. For best results: cover the answer, attempt the question under timed conditions (allocate 1.95 minutes per mark as a guide), then compare your response to the model. Identify specifically what you omitted — was it a technical point, a piece of scenario application, or a professional skills element such as a specific recommendation or a sceptical observation about an assumption?For SBL, prioritise reading the latest pre-seen material thoroughly before practising — the scenarios change for every exam window. For SBR, ensure you work through at least one full past consolidation question under exam conditions before your sitting; errors in group accounts are compounding and time-consuming to correct. For AFM, balance calculation practice with essay technique — the examiner's reports from 2024 and 2025 consistently show that many candidates who pass the numerical parts of a question fail to earn the discussion marks that could have taken them comfortably above 50.

CONCLUSION

Strategic Business Leader, Strategic Business Reporting, and Advanced Financial Management together represent the apex of the ACCA qualification's technical and professional demands. SBL requires candidates to function as a senior adviser to a board — integrating governance, risk, strategy, leadership, and ethics in a single cohesive response. SBR demands professional judgement in applying some of the world's most complex financial reporting standards to multi-entity scenarios. AFM requires both quantitative precision and strategic commercial awareness in advising on the most complex financial decisions a senior executive or adviser will face. The 15 questions in this guide address the topics that recent exam sittings have most consistently tested: PESTEL and stakeholder analysis in SBL; IFRS 15, IFRS 16, IAS 36, and IFRS 9 in SBR; and APV, interest rate risk, real options, M&A, and FX management in AFM.Pass rates across these three papers cluster between 45% and 53% in recent sittings — meaning that roughly half of all candidates who sit these exams do not pass on their first attempt. The candidates who do pass consistently share one characteristic: they answer the question actually set, not the question they prepared for. They apply knowledge to the scenario with specific evidence from the exhibits, and they communicate their analysis in the structured, professional format that the examiner's mark scheme rewards. These 15 questions and model answers are designed to help you build exactly those habits.

Frequently Asked Questions

What are the pass rates for SBL, SBR, and AFM in recent sittings?

Based on the most recent published data: SBL recorded a 53% pass rate in March 2025 and 50% in December 2025 (The Accountant Online, April 2025; Eduyush, April 2026). SBR recorded 50% in March 2025 and 48% in December 2025 — consistent with its long-run average of 46–52% since 2018 (ACCA Global official data; Learnsignal SBR pass rate analysis, March 2026). AFM recorded 45% in March 2025 and December 2025 (ACCA Global official data; Eduyush 2026). All three papers require a minimum score of 50 out of 100 to pass. ACCA emphasises that pass rate differences reflect candidate preparedness and the nature of each paper, not differences in marking standards.Is SBL harder than SBR and AFM?

SBL is structurally different from SBR and AFM, making direct comparison difficult. It is a four-hour case study — the longest ACCA exam — requiring integrated application across governance, risk, strategy, and leadership simultaneously. SBR and AFM are both 3 hours 15 minutes. SBL's pass rate of 50–53% is typically the highest of the three, suggesting that its integrated format rewards well-prepared candidates who invest in scenario practice. SBR and AFM each have specific technical areas that candidates find challenging: group consolidation (SBR) and discussion-based financial analysis (AFM) are consistently cited in examiner reports as areas where mark loss is concentrated. For most candidates, AFM requires the greatest combination of quantitative skill and strategic communication.How many marks are available for professional skills in each paper?

All three papers award 20 out of 100 marks for professional skills. In SBL, these 20 marks are distributed across all tasks and assess: communication (up to 5 marks — appropriate format, structure, and professional language), commercial acumen (up to 5 marks — linking analysis to commercial realities), analysis and evaluation (up to 5 marks — critical thinking, not just description), and professional scepticism and judgement (up to 5 marks — questioning assumptions, exercising professional judgement). SBR and AFM both include professional skills marks within their Section A and Section B questions, distributed similarly. Candidates who answer in complete, formatted professional responses (using headings, sub-headings, and clear recommendations) consistently earn more professional skills marks than those who write in unstructured note form.What IFRS standards are most frequently tested in SBR?

Based on examiner reports and syllabus guidance from September 2025 onwards: IFRS 18 (Presentation and Disclosure — new examinable standard from September 2025, replacing IAS 1) covers income statement categories, management-defined performance measures, and disaggregation requirements. IFRS 15 (Revenue from Contracts with Customers) — performance obligations, variable consideration, licences, warranties. IFRS 16 (Leases) — sale and leaseback, lease modifications, initial recognition. IAS 36 (Impairment) — goodwill allocation to CGUs, corporate assets, annual impairment testing. IFRS 9 (Financial Instruments) — ECL model, three-stage classification, trade receivable provisioning. IFRS 3 (Business Combinations) and IFRS 10 (Consolidation) — goodwill calculation, NCI measurement, disposal with loss of control. Group consolidation scenarios appear in virtually every SBR Section A question across recent sittings.Which AFM topics carry the most marks in recent exam sittings?

Based on the AFM March/June 2025 Examiner's Report (ACCA official, Kampai Co, Sohbet Co, GCR Co questions) and the ACCA Global AFM page: investment appraisal (APV, real options, DCF with complex inputs) and foreign exchange risk management (transaction hedging using forwards, futures, options, and money market hedges) are the most consistently high-value areas. Section A regularly integrates multiple topics — for example, combining a business valuation, synergy analysis, and FX risk assessment in a single 50-mark question. Section B questions have recently covered interest rate risk (swaps, caps, options), M&A financial evaluation, and performance analysis (financial ratios from both company and investor perspectives). The examiner consistently rewards candidates who address both the computational AND the discussion/evaluation dimensions of each requirement.References

ACCA Global — Strategic Business Leader (SBL) Syllabus and Study Guide 2025–2026 (Official) https://www.accaglobal.com/content/dam/acca/global/PDF-students/acca/SBL/SBL%20S25-J26%20syllabus%20and%20study%20guide.pdfACCA Global — Strategic Business Reporting (SBR) Pass Rates and Resources (Official) https://www.accaglobal.com/in/en/student/exam-support-resources/professional-exams-study-resources/strategic-business-reporting.html

ACCA Global — Advanced Financial Management (AFM) Pass Rates (Official) https://www.accaglobal.com/my/en/student/exam-support-resources/professional-exams-study-resources/p4.html

ACCA Global — AFM March/June 2025 Examiner's Report (Official PDF — Kampai Co, Sohbet Co, GCR Co) https://www.accaglobal.com/content/dam/acca/global/PDF-students/acca/p4/examinersreports/MJ25%20AFM%20examiner's%20report.pdf

The Accountant Online — ACCA March 2025 Exam Pass Rates (April 2025) https://www.theaccountant-online.com/news/acca-march-2025-pass-rates/

Eduyush — ACCA Subjects and Syllabus 2026: All 13 Papers, Pass Rates and Study Order (April 2026) https://eduyush.com/en-us/blogs/acca/acca-subjects

0 Comments Comments