Retirement

Americans Losing Retirement Confidence: 2026 Survey Finds

Table of Contents

- A Confidence Crisis in Slow Motion

- What the 2026 EBRI Survey Actually Found

- Why Workers Are More Worried Than Retirees

- The Social Security Time Bomb: What the Numbers Say

- The Debt Problem Nobody’s Talking About Enough

- Healthcare Costs: The Retirement Budget Destroyer

- The Retirement Age Gap: What Workers Expect vs. What Happens

- The ‘Stool’ Is Missing a Leg: The Pension Collapse

- What the Numbers Look Like for Average Savers

- What You Can Do: Practical Steps for Every Stage

- Conclusion: Anxiety Is Rational — And Actionable

- Frequently Asked Questions

- External References

A Confidence Crisis in Slow Motion

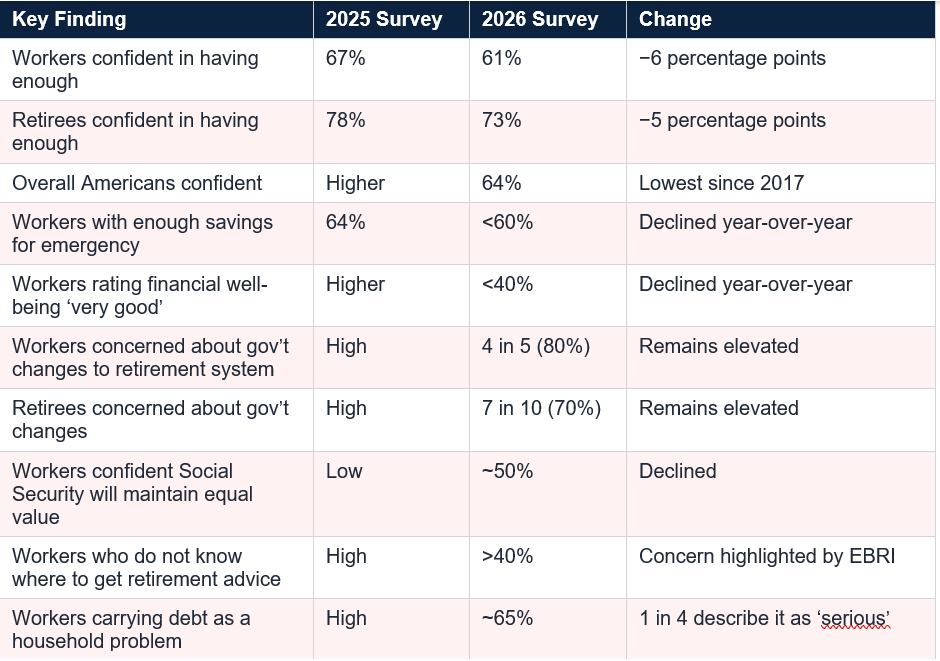

Retirement is supposed to be the destination. The reward at the end of a working life. The point at which the decades of payroll deductions, 401(k) contributions, and compound interest calculations finally add up to something that resembles security. For the better part of a generation, most Americans maintained at least a baseline confidence that this destination existed and was reachable.That confidence is eroding. Not in a single dramatic collapse, but in the slow, grinding way that anxiety tends to work: a percentage point here, a policy change there, a Social Security trustees’ report that moves the depletion date one more year closer, a Medicare premium that consumes most of the annual cost-of-living adjustment. The 2026 Retirement Confidence Survey from the Employee Benefit Research Institute and Greenwald Research captured the result of this gradual erosion in its 36th annual measurement of American retirement sentiment: only 64 percent of Americans say they feel confident they have enough money to live comfortably throughout retirement, the lowest figure since 2017.

This article examines what the survey found, why confidence is declining, the structural forces making retirement harder to plan, and the concrete steps that people at every stage — from their 30s to their 60s — can take to address the gaps before the retirement date becomes a deadline.

Disclaimer: This article is for general informational and educational purposes only. It is not financial, investment, or retirement planning advice. Social Security and Medicare rules change frequently. Consult a qualified financial adviser or retirement planner for guidance specific to your situation.

What the 2026 EBRI Survey Actually Found

The 2026 Retirement Confidence Survey, conducted online from 2 to 28 January 2026 among 2,544 Americans aged 25 and older, is the longest-running survey of retirement confidence in the United States. Its 36th iteration found a clear and statistically significant deterioration across virtually every dimension of retirement readiness and confidence it measures.

Craig Copeland, EBRI director of wealth benefits research: "Americans are contending with a mix of immediate financial pressures and long-term uncertainty. Many workers are struggling with debt, inflation and rising housing and health care costs, while retirees are increasingly worried about the future of Social Security and Medicare."

Why Workers Are More Worried Than Retirees

One of the persistent patterns in the EBRI survey is that workers consistently report lower confidence than retirees — 61 percent versus 73 percent in 2026. This gap is not simply about having more money. It reflects a structural difference in the certainties available to each group.Retirees know what their Social Security payment is. They know their Medicare coverage. They have resolved the uncertainty about when they will retire, what their expenses will be, and how their investment portfolio behaves. Workers, by contrast, are facing a future where all of these variables remain open. They are asking whether Social Security will still exist in its current form when they reach 65 or 67, whether healthcare inflation will continue outpacing their savings growth, whether their 401(k) balance will be adequate, and whether they will even be able to retire when they plan to.

The survey captures an important and underappreciated finding: nearly 39 percent of workers expect to retire at age 70 or older, or not at all. Yet only 10 percent of actual retirees say this was the case for them. The gap between what workers expect to do (work longer) and what retirees actually experienced (retire earlier than planned, median age 62) is one of the most dangerous financial planning mismatches in the survey. Workers who are counting on working until 70 to close their savings gap are making an assumption that the labour market, their health, and family circumstances may not allow them to keep.

The retirement age mismatch: Workers’ median expected retirement age is 65. The actual median retirement age among current retirees is 62. Nearly half of retirees say they retired earlier than planned. The assumption of extra working years to compensate for savings gaps is one of the most common and most dangerous planning errors in American retirement preparation.

The Social Security Time Bomb: What the Numbers Say

No single factor is driving retirement anxiety more consistently than uncertainty about Social Security. The EBRI survey found that 4 in 5 workers (80 percent) and 7 in 10 retirees (70 percent) are concerned about government changes to the US retirement system. Only about half of workers and 6 in 10 retirees expressed confidence that Social Security will continue to provide benefits of equal value in the future.Those concerns are grounded in documented financial reality, not media-generated fear. The Congressional Budget Office’s February 2026 projections updated the Social Security Old-Age and Survivors Insurance trust fund depletion date to fiscal year 2032 — approximately one year earlier than the 2025 estimate. If Congress takes no action before that date, an automatic benefit cut of approximately 28 percent would take effect in 2033, the first full year after depletion.

The 2.8 percent cost-of-living adjustment for 2026 added approximately $56 per month to the average retirement benefit, raising it to $2,071. But the Medicare Part B premium rose simultaneously by $17.90 per month to $202.90, consuming roughly 32 percent of the COLA increase. The effective net gain for many retirees was $38 per month. Against continued food, energy, and housing inflation, this represents continued real purchasing power erosion. AARP has reported that Social Security benefits have lost 20 percent of their purchasing power since 2010.

Several legislative proposals circulating in Congress in 2026 would make additional changes: shifting to Chained CPI for COLA calculations (which would reduce lifetime benefits by 3 to 4 percent over a 20-year retirement), raising the full retirement age to 69, and means-testing benefits for higher earners. Any combination of these changes could reduce annual Social Security income for average retirees by $2,400 to $4,800, according to CBO projections.

The Debt Problem Nobody’s Talking About Enough

Buried in the EBRI survey findings is a debt picture that deserves more attention than it typically receives in retirement coverage. Nearly two-thirds of workers reported that debt is a household problem, and one in four described it as a serious problem. Close to one-third of workers carry more than $25,000 in non-mortgage debt. The EBRI survey found that these obligations are limiting workers’ ability to save or maintain financial security heading toward retirement.Credit card debt is the most common form. But the debt picture for workers in their 40s and 50s increasingly includes student loan debt — either their own from degrees completed later in life or, increasingly, Parent PLUS loans taken for their children’s education — car loans, and in some cases medical debt. Each of these obligations competes directly with retirement savings for the same dollars.

The retirement savings mathematics of debt are stark. A worker aged 50 contributing $500 per month to a 401(k) earning 7 percent annually will accumulate approximately $64,000 by age 65. The same worker spending $500 per month servicing high-interest credit card debt instead has $0 in savings growth from that money and pays additional interest costs on top. The opportunity cost of carrying significant debt into the peak savings years (ages 50 to 65) is among the most underappreciated obstacles to retirement security in the United States.

Healthcare Costs: The Retirement Budget Destroyer

Nearly 60 percent of workers told the EBRI survey that medical expenses are hindering their retirement savings. Forty percent of retirees reported higher-than-expected healthcare costs in retirement. These findings align with broader data on American healthcare inflation, which has consistently outpaced overall CPI and directly erodes the real value of both retirement savings and Social Security COLAs.The standard financial planning assumption — that retirees should plan to replace 70 to 85 percent of their pre-retirement income — increasingly understates the healthcare cost burden. A 65-year-old couple retiring today will spend an estimated $315,000 (Fidelity estimate, 2025) on healthcare costs over the course of their retirement, excluding long-term care. Long-term care, which is not covered by Medicare, adds another potential six-figure liability for couples where one or both partners require nursing home or assisted living care.

The Medicare Part B premium increase in 2026 illustrates the compounding nature of the problem: a 9.7 percent single-year jump in premiums, taken directly from Social Security checks for most recipients, effectively cancelled out most of the COLA increase. Workers who are counting on Social Security to provide a floor of retirement income need to build their retirement plan around the assumption that healthcare will claim an increasing share of that benefit over time.

The Retirement Age Gap: What Workers Expect vs. What Happens

One of the survey’s most practically important findings is the persistent and widening gap between when workers expect to retire and when retirement actually happens. Workers’ median expected retirement age remained 65 in the 2026 survey. But the median actual retirement age among current retirees is 62, and nearly half say they retired earlier than planned.The reasons for unplanned early retirement are predominantly involuntary: health deterioration, family caregiving responsibilities, job loss or layoff, and workplace changes that made continued employment difficult. These are not marginal scenarios. They are the actual retirement experience of nearly half of all American retirees.

The financial consequence of retiring three years earlier than planned — from 65 to 62 — is significant along multiple dimensions simultaneously. Three fewer years of savings contributions. Three years of earlier drawdown from retirement accounts. Three years of Social Security benefits claimed at a reduced level (claiming at 62 vs. 65 reduces Social Security benefits by approximately 25 percent for life). And, for workers who were counting on employer health insurance through age 65, a coverage gap before Medicare eligibility that can cost $5,000 to $20,000 or more per year in the open market.

The ‘Stool’ Is Missing a Leg: The Pension Collapse

David Demming, founder of Demming Financial Services Corp., told Marketplace.org that the old pension model — where retirees received a fixed income until death regardless of how long they lived — is a thing of the past. “Today,” he said, “less than 10% of people have pensions unless you’re working for the government.”The traditional “three-legged stool” of retirement income — Social Security, pension, and personal savings — has effectively become a two-legged stool for most American workers, with the defined benefit pension leg replaced by the participant-directed defined contribution (401(k)) model. The difference is not merely structural. A defined benefit pension provides guaranteed lifetime income that cannot be outlived. A 401(k) provides a balance that can be depleted.

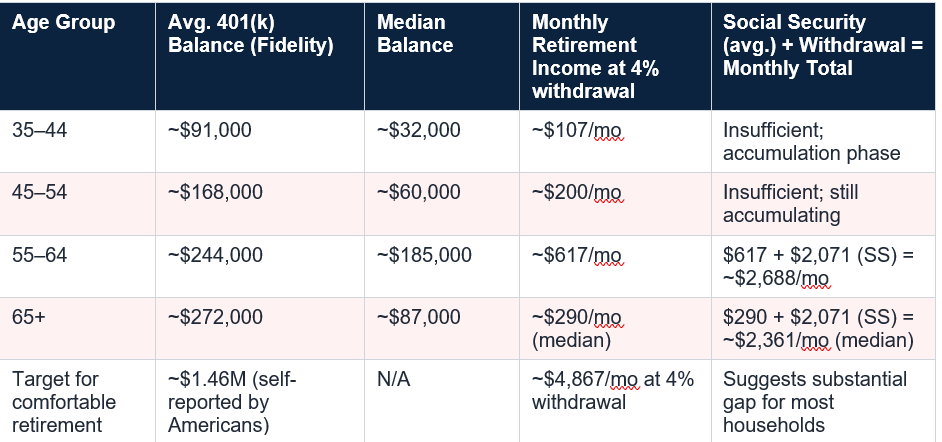

The median retirement account balance for individuals aged 55 to 64 is approximately $185,000, according to the Federal Reserve’s Survey of Consumer Finances. At a standard 4 percent withdrawal rate, $185,000 generates $7,400 per year in income — approximately $617 per month. Combined with the average Social Security benefit of $2,071 per month, a median-balanced household has approximately $2,688 per month in retirement income, or about $32,250 per year. For reference, the average annual household spending for a couple aged 65 to 74 is approximately $57,000, according to Bureau of Labor Statistics consumer expenditure data. The gap is real and significant for many households.

What the Numbers Look Like for Average Savers

The $1.46 million figure Americans report they believe they need to retire comfortably (cited in ADVISOR Magazine coverage of the 2026 survey period) versus median balances in the $87,000 to $185,000 range for pre-retirees represents a gap of approximately $1 million to $1.3 million for the median household. This gap is not theoretical — it is the retirement savings shortfall that underlies the 36 percentage points of Americans who told the EBRI they do not feel confident about their retirement.

What You Can Do: Practical Steps for Every Stage

In Your 30s and 40s: Build the Habit and Close the Gap

- Maximise employer 401(k) match before any other savings decision. An employer match is an immediate 50 to 100 percent return on that dollar. Not capturing it is leaving guaranteed money on the table.

- Prioritise high-interest debt elimination. Every dollar paid off on 20 percent APR credit card debt is equivalent to earning 20 percent guaranteed. No investment reliably beats that risk-adjusted return.

- Open and fund a Roth IRA if eligible. Roth accounts grow tax-free and withdrawals in retirement are not counted as taxable income, which becomes valuable if Social Security means-testing becomes law.

- Run a retirement projection at least annually. Free tools from Fidelity, Vanguard, and the Social Security Administration’s website allow you to see your projected monthly retirement income and identify your savings gap while there is still time to close it.

In Your 50s: The Decade That Defines the Outcome

- Take advantage of 401(k) catch-up contributions. In 2026, workers aged 50 and older can contribute an additional $7,500 above the standard $23,500 limit, for a total of $31,000 annually. Workers aged 60 to 63 get an enhanced catch-up of $11,250 above the standard limit under SECURE 2.0 rules.

- Plan explicitly for the early-retirement scenario. If half of people retire earlier than planned, build a plan that works if retirement happens at 62, not 65. If it still works at 62, retiring at 65 or later becomes a bonus.

- Do not count on working until 70 to make the numbers work. Build the plan without that assumption. If you work until 70, great. If you do not, you will not face a crisis.

- Approaching and In Retirement: Protecting What You’ve Built

- Optimise Social Security timing. Delaying Social Security from 62 to 70 increases the monthly benefit by approximately 77 percent. For a person in good health, delaying to 70 is often the highest-return risk-free decision available. Each year of delay adds 8 percent to the annual benefit.

- Plan for healthcare inflation, not just general inflation. A dedicated healthcare savings account (HSA, if eligible) allows pre-tax contributions for medical expenses and provides a hedge against healthcare cost inflation specifically.

- Consider a guaranteed income product. The EBRI survey found that more than 4 in 5 workers expressed interest in purchasing a guaranteed monthly income product with retirement savings. Annuities have real structural advantages for longevity risk — the risk of outliving your savings. Evaluate them with a fee-only financial adviser who is not paid commissions on their sale.

- Use the Social Security Administration’s my Social Security portal to check your earnings record and benefit estimate. Errors in the earnings record are more common than most people realise and can reduce your benefit permanently if not corrected.

Conclusion

The anxiety documented in the 2026 EBRI Retirement Confidence Survey is not irrational. The median American household approaching retirement does face a real savings gap. Social Security’s funding trajectory is genuinely concerning without congressional action. Healthcare inflation is genuinely eroding purchasing power. Debt is genuinely competing with savings for the same dollars. These are not misperceptions to be corrected with more optimistic messaging. They are accurate assessments of real structural challenges.But anxiety is only useful if it motivates action, and there is more action available at every stage of the retirement planning journey than many people realise. Catch-up contribution limits are generous for those in their 50s and 60s. Social Security optimisation through delayed claiming can add tens of thousands of dollars in lifetime benefits. Debt elimination in the pre-retirement decade has compounded benefits that rival investment returns. And the simple act of running a retirement projection — which more than 40 percent of workers have not done, according to consistent survey findings — is the most immediate and highest-leverage step available.

The 2026 survey’s most actionable finding may be this: workers with access to a workplace retirement plan are more than twice as likely to be confident about retirement as those without one — 70 percent versus 32 percent. Participation in the retirement system that exists, whatever its imperfections, remains the single most reliable predictor of retirement confidence. The gap between what Americans worry about and what they need to do is knowable. And it is closable, for most people, with the right information and enough lead time.

Frequently Asked Questions

What did the 2026 EBRI Retirement Confidence Survey find?

The 36th annual Retirement Confidence Survey, conducted by the Employee Benefit Research Institute and Greenwald Research among 2,544 Americans in January 2026, found that only 64% of Americans feel confident about having enough money to live comfortably in retirement — the lowest level since 2017. Workers’ confidence fell six percentage points to 61%, while retirees’ confidence fell five percentage points to 73%. The survey found growing anxiety about Social Security, Medicare, healthcare costs, debt, and housing expenses.How much do Americans need to retire comfortably?

Americans self-report needing approximately $1.46 million to retire comfortably. Many financial planners recommend targeting retirement savings equal to 10 to 12 times your final annual salary, which for a household earning $75,000 would be $750,000 to $900,000. The 4% withdrawal rule suggests that $1 million generates $40,000 per year in income. Combined with the average Social Security benefit of $2,071 per month ($24,852 annually), a $1 million 401(k) would generate approximately $65,000 per year in retirement income before taxes.Will Social Security run out?

Social Security’s OASI trust fund is projected to be depleted in fiscal year 2032, according to the Congressional Budget Office’s February 2026 projections — approximately one year earlier than the 2025 estimate. If Congress takes no action before depletion, benefits would be automatically cut by approximately 28% starting in 2033. This does not mean Social Security disappears: ongoing payroll tax revenues would still fund approximately 72% of promised benefits. However, a 28% cut would be significant for households depending heavily on Social Security income.What is the average Social Security retirement benefit in 2026?

The average monthly retirement benefit is $2,071 in 2026, following a 2.8% COLA increase. The maximum benefit for someone retiring at full retirement age in 2026 is $4,018 per month. However, the Medicare Part B premium rose to $202.90 in 2026, effectively consuming about $17.90 of the $56 monthly COLA increase for most recipients. Social Security replaces approximately 40% of the average worker’s pre-retirement income, leaving a significant income gap to be filled by personal savings.What are 401(k) contribution limits for 2026?

The standard 401(k) contribution limit for 2026 is $23,500. Workers aged 50 and older can make catch-up contributions of an additional $7,500, for a total of $31,000 annually. Under SECURE 2.0 rules effective from 2025, workers aged 60 to 63 can make an enhanced catch-up of $11,250 above the standard limit, for a maximum contribution of $34,750. These limits apply to 403(b) plans as well.When should I claim Social Security benefits?

Claiming Social Security at the earliest eligible age of 62 permanently reduces your monthly benefit by approximately 25 to 30% compared with claiming at full retirement age (67 for those born in 1960 or later). Delaying beyond full retirement age increases the benefit by 8% for each year of delay, up to age 70. Claiming at 70 versus 62 can result in a benefit that is approximately 77% higher per month. The break-even point for delayed claiming (the age at which total lifetime benefits from delayed claiming exceed early claiming) is typically in the late 70s, making delay financially advantageous for people in good health.External References and Further Reading

EBRI — 2026 Retirement Confidence Survey Press Release (April 21, 2026), InvestmentNews — Retirement Confidence Slips as Americans Grapple with Rising Costs and Policy Fears (April 2026), Marketplace.org — Americans Are Losing Confidence in Retirement Savings (April 22, 2026), Money.com — Retirement Confidence Is Slipping for Older Americans (February 23, 2026), 401k Specialist — Retirement Confidence Falls as Social Security Concerns Mount (April 2026), Kiplinger — Six Changes to Social Security in 2026, Due.com — The Social Security Change in 2026 That Could Cost Retirees $4,800 a Year (April 2026), AARP — 9 Ways Your Retirement Planning Will Change in 2026, Social Security Administration — 2026 COLA Information, Rethinking65 — Americans’ Confidence About Retirement Falters (April 2026)

0 Comments Comments