The Simple 3 ETF Portfolio Strategy: Build $1 Million for Income or $2 Million for Growth

Table of Contents

- Introduction: Why Simplicity Wins

- Three Timeless Investment Rules

- Understanding ETFs: The Foundation

- The Three ETFs Explained

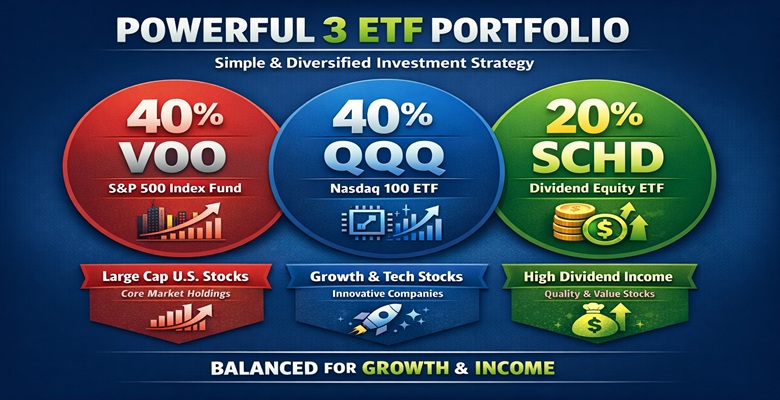

- VOO: The Foundation

- QQQ: The Growth Engine

- SCHD: The Income Stabilizer

- ETF Comparison Table

- Two Portfolio Strategies: Income vs. Growth

- 30-Year Projection Breakdown

- FAQs

Introduction: Why Simplicity Wins

If you had to start over with nothing—no portfolio, no savings, just zero—what would you do? The answer isn't chasing hot stocks or trying to outsmart the market. The answer is simplicity.

Most investors don't struggle because they choose the wrong investments. They struggle because they overcomplicate decisions that don't need to be complex. The real challenge isn't finding more options—it's knowing what actually matters long-term.

This guide walks you through a simple three ETF portfolio that can be structured for income or growth using the same investments. One version builds a portfolio close to $1 million that pays over $2,000 per month in dividends. The other grows to $2 million by focusing purely on growth. Same ETFs, different emphasis.

Three Timeless Investment Rules

Before discussing specific ETFs, understand these fundamental rules that apply regardless of your income, experience level, or market conditions.

Rule 1: Time Decides Emphasis

Not investment opinions, not headlines, not last year's winners. When you have time ahead of you, lean toward growth. Your contributions are small relative to the time they have to compound.

Rule 2: Capital Must Exist Before Income Matters

This trips up many investors. Income feels productive because it's visible—cash hitting your account feels like progress. But mathematically, income drawn too early slows compounding. A portfolio paying you before it's large enough is doing a later-stage job too soon.

Rule 3: Volatility Isn't the Enemy

Volatility only becomes dangerous when it changes behavior. If you're adding money consistently, price swings work in your favor. You buy more shares when prices are lower and fewer when prices are higher. The real risk isn't fluctuation—it's panic, stopping contributions, and locking in losses.

Understanding ETFs: The Foundation

An ETF (Exchange-Traded Fund) is simply a structure—a way to own a large group of companies all at once, automatically, at very low cost. You're not picking winners. You're buying systems that evolve on their own.

Companies that stop performing fall out. Companies that grow become a bigger part of the portfolio. This automatic adjustment is a massive advantage over trying to manage everything yourself.

When you apply these rules using ETFs, investing becomes about staying invested long enough for compounding to work. The goal isn't to be right this year—it's to still be invested 10, 20, or 30 years from now.

The Three ETFs Explained

VOO: The Foundation

VOO tracks the S&P 500, meaning it owns the 500 largest publicly traded companies in the United States, weighted by size. When companies grow, they become a bigger part of the index. When they shrink, they eventually get replaced. You don't predict winners—the index does that work.

This sounds boring, but boring is exactly why it works. The S&P 500 has survived wars, recessions, inflation spikes, tech bubbles, and financial crises. Entire industries have come and gone, yet the index keeps moving forward because it constantly renews itself.

VOO Key Statistics:

- Average annual share price appreciation: 12.47%

- Current dividend yield: 1.12%

- Dividend growth rate: 6.17%

- Expense ratio: 0.03%

For every $10,000 invested, you pay about $3 per year in fees. Compare that to actively managed funds charging 1% or more, and the difference compounds into hundreds of thousands over a lifetime.

VOO works as the base for both investor types. For growth investors, it provides broad market exposure. For income investors, it represents ownership in profitable businesses generating real earnings.

QQQ: The Growth Engine

QQQ tracks the NASDAQ 100—the 100 largest non-financial companies on the NASDAQ exchange. This tilts the portfolio toward technology, innovation, and scale. These businesses reinvest aggressively into software, data centers, automation, and new products.

The key concept is return on capital. Companies that consistently reinvest profits at high rates compound faster. Even a few percentage points of higher annual returns sustained for years creates life-changing differences.

QQQ Key Statistics:

- Average annual share price appreciation: 18.45%

- Current dividend yield: 0.51%

- Dividend growth rate: 6.66%

- Expense ratio: 0.20%

Higher return potential comes with higher volatility. QQQ falls harder during downturns—it has experienced drawdowns of 30%, 40%, and more during major market events. But if you're contributing regularly and not forced to sell, lower prices mean your contributions buy more shares.

Volatility is the price paid for higher expected growth. When growth is your objective, that price is rational. However, growth shouldn't be the entire plan forever. What feels tolerable at $50,000 feels very different at $1 million.

SCHD: The Income Stabilizer

SCHD focuses on high-quality companies with strong cash flow and a history of paying and growing dividends. These are established, profitable businesses like Coca-Cola, PepsiCo, Texas Instruments, Cisco, and Verizon—focused on consistency and returning capital to shareholders rather than aggressive expansion.

The mistake many make is treating dividends as the goal from day one. When a portfolio is small, cash flow isn't meaningful enough to change outcomes, but the cost to compounding is real. Every dollar paid out can't compound internally at higher rates.

But as portfolios grow and contributions become smaller relative to portfolio size, cash flow matters more. Dividends reduce the need to sell shares during downturns, making volatility easier to handle.

SCHD Key Statistics:

- Average annual share price appreciation: 7.82%

- Current dividend yield: 3.77%

- Dividend growth rate: 10.61%

- Expense ratio: 0.06%

SCHD doesn't chase the highest yield—it focuses on balance sheets, payout ratios, and sustainability. Reinvested dividends buy more shares, which generate more dividends, creating a powerful feedback loop.

ETF Comparison Table

| Metric | VOO | QQQ | SCHD |

|---|---|---|---|

| Tracks | S&P 500 | NASDAQ 100 | Dividend Growth |

| Share Price Growth | 12.47% | 18.45% | 7.82% |

| Dividend Yield | 1.12% | 0.51% | 3.77% |

| Dividend Growth | 6.17% | 6.66% | 10.61% |

| Expense Ratio | 0.03% | 0.20% | 0.06% |

| Best For | Foundation | Growth | Income/Stability |

Two Portfolio Strategies: Income vs. Growth

The same three ETFs can serve different purposes depending on allocation. Nothing about the strategy changes—only the weights.

Income-Focused Portfolio

| ETF | Allocation |

|---|---|

| VOO | 20% |

| QQQ | 10% |

| SCHD | 70% |

- Portfolio dividend yield: 2.91%

- Dividend growth rate: 9.61%

- Share price appreciation: 9.81%

Growth-Focused Portfolio

| ETF | Allocation |

|---|---|

| VOO | 20% |

| QQQ | 70% |

| SCHD | 10% |

- Portfolio dividend yield: 0.92%

- Dividend growth rate: 8.91%

- Share price appreciation: 16.19%

30-Year Projection Breakdown

Assumptions: $10 per day ($3,650/year), dividends reinvested, starting from zero.

| Timeline | Income Portfolio | Growth Portfolio |

|---|---|---|

| Year 1 | $3,650 | $3,650 |

| Year 10 | $66,195 | $80,884 |

| Year 20 | $283,496 | $452,350 |

| Year 30 | $992,646 | $2,133,710 |

| Monthly Dividends (Year 30) | $2,010 | $157 |

The income portfolio generates $24,123 annually in dividends by year 30. The growth portfolio's value comes almost entirely from capital appreciation—$2,003,351 from price growth versus just $20,859 from dividends.

Conclusion

Building wealth doesn't require complexity. Three ETFs—VOO, QQQ, and SCHD—cover everything that matters long-term. The same system serves both growth and income investors. The only variable is emphasis, which shifts as your portfolio grows and priorities change.

Start with $10 per day. Stay consistent. Let compounding do its work.

FAQs

What is the best 3 ETF portfolio for beginners?

A combination of VOO (S&P 500 foundation), QQQ (growth exposure), and SCHD (dividend income) provides broad diversification, growth potential, and income stability—suitable for any investor starting out.

Should I focus on growth or income ETFs?

This depends on your time horizon. Younger investors with decades ahead should emphasize growth (more QQQ). Those approaching retirement or seeking cash flow should emphasize income (more SCHD).

How much should I invest daily to reach $1 million?

Investing $10 per day ($3,650 annually) in an income-focused portfolio can reach approximately $992,646 after 30 years with dividends reinvested.

Is QQQ too risky for long-term investing?

QQQ experiences higher volatility but has historically delivered superior long-term returns. Risk becomes problematic only if volatility causes you to sell at the wrong time or stop contributing.

When should I shift from growth to income?

Consider shifting emphasis as your portfolio grows and your need for stability increases. There's no fixed age—watch for when drawdowns become emotionally difficult or when you need cash flow.

Can I use this strategy in tax-advantaged accounts?

Yes. This strategy works in 401(k)s, IRAs, and taxable accounts. Tax-advantaged accounts benefit most because dividends compound without annual tax drag.

0 Comments Comments