Professional & Career Development

Trades Workers and Debt: Why Even Skilled Labor Owes

Table of Contents

- The Debt-Free Promise That Wasn’t

- Trade School Debt vs. College Debt: The Real Numbers

- The Hidden Debt Layer 1: For-Profit Trade Schools and Predatory Loans

- The Hidden Debt Layer 2: Tools, Equipment, and the First-Year Tax

- The Hidden Debt Layer 3: Licensing, Certification, and Continuing Education Fees

- The Hidden Debt Layer 4: Starting Your Own Business

- Who Is Most at Risk: The Default Rate Problem

- The Bright Side: Where Trades Financing Really Does Work

- How to Enter the Trades Without Drowning in Debt

- Conclusion: Trades Are Still a Smart Financial Path — With Eyes Open

- Frequently Asked Questions

- External References

The Debt-Free Promise That Wasn’t

The pitch has been consistent, and it is not wrong exactly: skip the four-year degree, go into a skilled trade, earn a good living, and avoid the student debt burden that has put a generation of college graduates behind financially before they’ve had their first real job. Electricians, plumbers, HVAC technicians, and welders can earn $60,000 to $100,000 or more. The average trade school credential costs a fraction of a bachelor’s degree. The skilled trades shortage is real, and the hiring market is strong.All of that is true. And yet something is also left out of that story. Across the country, tradespeople are carrying debt — sometimes significant debt — that accumulated not because they chose the wrong path, but because the path came with costs that the pitch did not fully prepare them for. Trade school tuition at the wrong institution. Tools they had to buy before they could work. Licensing exams and continuing education fees. Equipment loans to start a business. Vehicle debt for the work truck that the job requires.

This article is not an argument against the trades. The financial case for skilled trades careers remains strong, particularly compared to degree paths in lower-earning fields. But the specific ways tradespeople wind up in debt are worth understanding clearly, because some of them are avoidable and some are simply the cost of entry that more people should know about before they sign the paperwork.

The Federal Reserve finding: 30% of borrowers whose highest education is some college, a technical certificate, or an associate degree are behind on their student loan payments, compared to 11% of borrowers with a bachelor’s degree. — Federal Reserve Survey of Household Economics and Decisionmaking, 2024

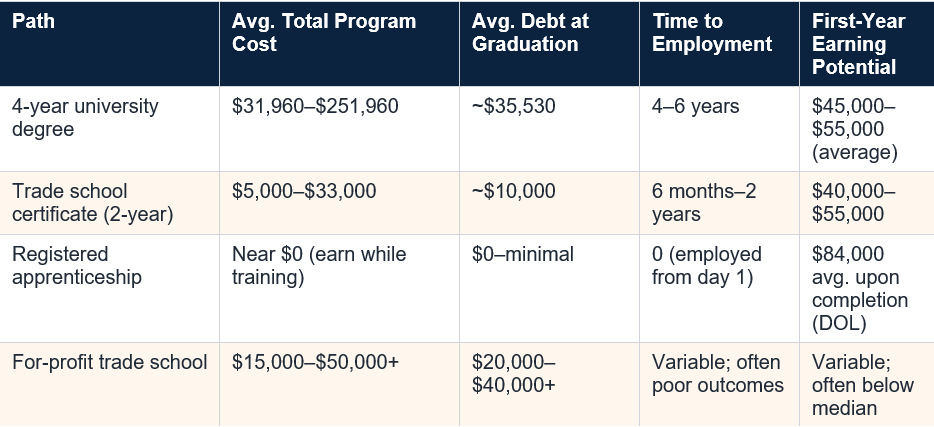

Trade School Debt vs. College Debt: The Real Numbers

The comparison between trade school and college debt is usually presented as a straightforward win for the trades, and on average, it is. The average trade school credential runs well under $20,000 in total program cost, while the average four-year university degree costs $31,960 to $251,960 depending on institution type, and leaves graduates with roughly $35,530 in student loan debt nationally.For a trade worker who completes a two-year credential at a community college, earns a Pell Grant covering much of the tuition, and enters an apprenticeship program earning wages from day one, the debt comparison strongly favours the trades path. The average trade school graduate carries approximately $10,000 in debt, enters the workforce in under two years, and begins earning $40,000 to $55,000 in the first year.

The problem is that the “average $10,000” figure masks enormous variation. Trade school costs range from near zero at a community college with Pell Grant coverage to $50,000 or more at for-profit vocational schools that market aggressively to students who do not understand the difference. The average is pulled down by the most financially efficient paths. The worst outcomes — heavy debt, poor job placement, low wages — are concentrated in specific types of institutions.

The Hidden Debt Layer 1: For-Profit Trade Schools and Predatory Loans

The most significant source of unexpected debt among trade workers is one that the industry’s boosters rarely discuss: the for-profit vocational school sector. For-profit trade and career schools range from high-quality, well-managed institutions with strong job placement to genuinely predatory operators that charge four-year tuition for two-year credentials, have low accreditation standards, and leave graduates with debt and credentials that employers do not recognise.The collapse of ITT Technical Institute in 2016 — which left 35,000 students with debt and no degree — was the highest-profile example of this dynamic. The Department of Education ultimately discharged $1.1 billion to 115,000 borrowers who had attended ITT. But the underlying pressures that created ITT have not disappeared. For-profit career schools still enrol hundreds of thousands of students annually, still market heavily in communities with limited access to traditional higher education, and still produce graduates with debt loads that the credential’s earning potential cannot support.

The cosmetology school sector is one of the most studied examples. Cosmetology programs often cost $10,000 to $20,000, graduate students into a field where median wages are approximately $30,000 to $35,000, and have some of the highest student loan default rates in the vocational education sector. Students who borrowed $15,000 to $20,000 to become licensed cosmetologists and are earning $28,000 in their first year are not failing because they made a bad choice individually — they are in a structural position where the debt-to-earnings ratio was never sustainable.

The accreditation test: Before enrolling at any trade or vocational school, verify accreditation status and whether the school participates in the federal Title IV financial aid program. Federal student loans are only available through accredited schools. If a school requires only private loans to fund its programs, that is a significant warning sign about the institution’s quality and legitimacy.

The Hidden Debt Layer 2: Tools, Equipment, and the First-Year Tax

Even a tradesperson who financed their education wisely — community college, Pell Grant, minimal debt — faces a substantial and often underestimated financial challenge in the first year of actual work: the tools requirement.In most skilled trades, workers are expected to arrive at a job site with their own hand tools and, in many cases, power tools. The professional toolset expected of a licensed electrician, plumber, or HVAC technician is not a $200 kit from a hardware store. A professional-grade electrician’s tool kit can run $500 to $2,000. A plumber’s tool inventory, including pipe wrenches, drain equipment, and testing gear, can easily reach $1,000 to $3,000. Add a reliable work vehicle — which most tradespeople working independently will need — and the initial capital required to work runs $5,000 to $30,000 or more.

These costs are often financed. A new tradesperson leaving a two-year program with $10,000 in student loan debt may add another $8,000 to $15,000 in vehicle financing and tool loans before they write their first invoice. The monthly payment burden on a $25,000 total debt package at standard consumer interest rates is $400 to $600 per month — manageable on a $55,000 salary, but not comfortable, and not the “debt-free trades” story that was advertised.

The tool cost reality: A complete professional tool kit for a licensed electrician starting their first job can run $1,500 to $3,000. A used work truck costs $15,000 to $30,000. A plumber adding a drain camera and hydro-jetting machine to handle commercial work is looking at $5,000 to $15,000 in equipment. These are startup costs most trades pathways do not discuss during recruitment.

The Hidden Debt Layer 3: Licensing, Certification, and Continuing Education Fees

The skilled trades require licensing, and licensing requires ongoing investment of time and money that is almost never mentioned in the initial discussion of trades costs. Most states require electricians, plumbers, HVAC technicians, and other tradespeople to pass licensing exams, renew their licenses every two to five years, complete continuing education credits, and sometimes hold multiple certifications for different types of work.Licensing exam fees typically run $50 to $300 per attempt. Prep courses, which most candidates use, add $200 to $600. License renewal every two to three years costs $100 to $300 in most states. Continuing education credits, often required for renewal, cost another $100 to $500 per cycle depending on the state and the field. An EPA 608 certification for HVAC work costs $20 to $80 to sit. A master plumber license in many states requires years of journeyman experience followed by a more expensive exam and additional fees.

Over the course of a 30-year trades career, these ongoing licensing and certification costs are meaningful but manageable. In the first two to three years, when earnings are at the lower end of the range and debt from training and tools has not yet been paid down, they add pressure to an already tight budget. A newer tradesperson who needs to pay a license renewal fee and complete continuing education in the same month as a tool loan payment and a student loan payment is not in a crisis, but they are experiencing the hidden overhead of a profession that marketing tends to describe simply as “high-paying and debt-free.”

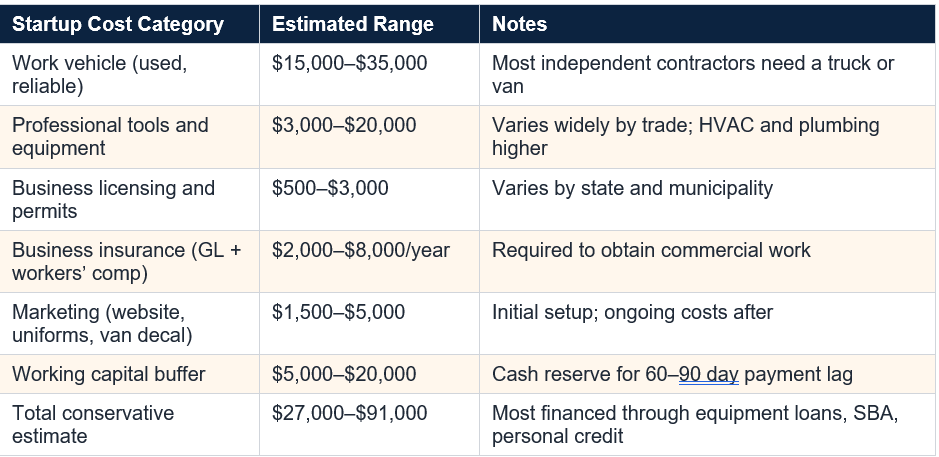

The Hidden Debt Layer 4: Starting Your Own Business

Many tradespeople’s long-term financial goal is to move from employed journeyman to self-employed contractor — to own the business rather than work for one. This transition is one of the most powerful wealth-building moves available in the trades, and many electricians, plumbers, and HVAC technicians do successfully build six-figure businesses within ten years of credentialing.But the transition from employee to owner requires capital, and that capital is typically borrowed. A new trades business needs: a work vehicle (or fleet), professional-grade equipment for the specific type of work, business licensing and insurance (general liability, workers’ compensation if hiring employees), marketing costs, and working capital to cover expenses while waiting on customer payments. Conservative startup costs for a solo licensed plumber or electrician going independent run $20,000 to $60,000. A small HVAC firm with one helper and service van can require $50,000 to $100,000 in initial capital.

Most of this capital is financed. SBA loans, equipment financing, business lines of credit, and personal guarantees on commercial loans are the standard mechanisms. A tradesperson who transitions to independent contracting at age 30, carrying $10,000 in remaining student loan debt, $15,000 in vehicle debt, and $40,000 in business startup debt, is carrying $65,000 in total debt obligations. That number is still manageable against a successful plumbing business generating $150,000 in annual revenue — but it is a long way from the “no debt in the trades” narrative.

Who Is Most at Risk: The Default Rate Problem

The 30 percent behind-on-payments figure from the Federal Reserve deserves careful interpretation. Not every person in that statistic is a tradesperson who made a poor financial decision. The category includes students who enrolled in short certificate programs, students who dropped out before completing, students who attended unaccredited schools that left them with debt and no credential, and students who borrowed for programs in very low-wage fields.The default rate is not evenly distributed across all trade pathways. Electricians, plumbers, and HVAC technicians — trades with strong wages, clear credential pathways, and genuine labour market demand — have very different default profiles than cosmetology, culinary arts, or general business certificate graduates. The common thread among the highest-default programmes is not “trade” versus “college” but “low wages relative to debt load.”

The specific risk factors for trades debt problems include: attending a for-profit school with high tuition and poor job placement; entering a trade with limited local demand; taking on equipment or business debt before establishing a stable employment base; and entering fields where licensing requirements change or where wages have not kept pace with cost growth. None of these risks are hidden — they are predictable and largely avoidable with good information before enrollment.

The Bright Side: Where Trades Financing Really Does Work

The antidote to all of the above is the path that the data consistently rewards: the registered apprenticeship. Apprenticeship programs, run through the Department of Labor and managed by unions, industry associations, and individual employers, offer the rarest financial structure in American education: training that pays you while you learn.Apprentices typically start at around 50 percent of a journeyworker’s rate, with graduated raises built into the program as skills develop. Upon completion, registered apprenticeship graduates earn an average starting salary of $84,000, according to a March 2025 Department of Labor fact sheet. They finish with a nationally recognised credential, an employer already in place, and no debt. A January 2025 DOL study confirmed that registered apprenticeships significantly expand access to living wages across the country, particularly for workers without four-year degrees.

Congress recently passed legislation extending Pell Grant eligibility to shorter-term credential programs starting July 1, 2026, allowing students to use up to $4,310 per year for programs as short as eight weeks in fields including skilled trades. For students who do need to attend a school programme rather than an apprenticeship, this expansion means more grant money available and less loan dependency.

Additionally, many trades employers offer employer tuition assistance — up to $5,250 per year tax-free under IRS rules — yet only 2 to 5 percent of eligible employees actually use it, largely because they do not know the benefit exists. A tradesperson whose employer offers this benefit and who uses it for continuing education or additional certifications is accessing free money that compounds over a career.

How to Enter the Trades Without Drowning in Debt

Prioritise Apprenticeships Over Trade School When Possible

The clearest financial advice is to enter through the apprenticeship system if at all possible. Visit Apprenticeship.gov to find registered programmes in your area and trade of interest. Union apprenticeships and non-union registered apprenticeships both offer earn-while-you-learn structures that eliminate the debt problem entirely. Competition for apprenticeship slots is real, but the financial advantage of the zero-debt, paid-training model is substantial.Choose Accredited Community Colleges Over For-Profit Vocational Schools

If you need a school programme, community colleges and technical colleges offer similar or superior credential quality at dramatically lower costs than for-profit trade schools. Pell Grants cover a significant portion of community college costs for eligible students. Always verify accreditation status and ask directly about job placement rates, median starting salary of graduates, and default rates on federal student loans before enrolling anywhere.Plan the Tool and Vehicle Costs Before Day One

Budget the first-year working costs explicitly before you start. Ask experienced workers in your target trade what a complete professional tool kit costs and whether employers provide any tools. Research used work vehicle options before you need one. Building a $5,000 to $10,000 tool-and-vehicle fund during training — even while working part-time — can eliminate the financing burden that turns a $10,000 student loan into a $30,000 total debt package.Use Employer Tuition Assistance for Continuing Education

- Ask your employer whether they offer tuition assistance before paying out of pocket for license renewal courses.

- Check whether your union offers educational benefits — many union apprenticeship programmes include continuing education as part of membership.

- Research state-level workforce development programmes, which in many states provide grants for trades workers seeking additional credentials.

Conclusion

The trades remain one of the most financially sound career choices available to anyone entering the workforce in 2026. The labour shortage is real. The wages are strong and rising. The job security is excellent. And the total lifetime debt burden, for someone who navigates the training pathway wisely, is genuinely far lower than the equivalent college graduate carrying $35,000 in student loans into an entry-level office job.But the narrative that trades work is uniformly debt-free is not accurate, and it is not doing people who are choosing this path any favours. Trade school at the wrong institution can generate $30,000 to $40,000 in debt with poor job placement. Tool and vehicle costs can add $15,000 to $30,000 in financed expenses in the first year. Licensing and continuing education create ongoing overhead. And the transition to business ownership — the goal most independent tradespeople are working toward — typically requires $30,000 to $90,000 in borrowed startup capital.

None of these costs make the trades the wrong choice. They make the trades a choice that deserves the same clear-eyed financial planning as any other major career decision. The tradesperson who enters through an apprenticeship, chooses their employer carefully, saves for their tool kit, and understands the licensing overhead is on a financial trajectory that rivals or exceeds most white-collar careers. The one who borrows $40,000 at a for-profit cosmetology school for a $30,000-a-year job is in a structural trap that has nothing to do with trades being a poor path — and everything to do with a system that was designed to capture their federal loan eligibility. Know the difference. The distinction is the whole story.

Frequently Asked Questions

Do trade school graduates actually carry debt?

Yes. The average trade school graduate carries approximately $10,000 in debt at graduation, according to Trade Colleges Directory’s analysis. However, that average masks wide variation. Graduates of community college programmes with Pell Grant coverage may carry very little debt. Graduates of for-profit trade schools can carry $20,000 to $40,000 or more. The 30 percent behind-on-payments rate cited by the Federal Reserve for associate degree and certificate holders reflects the worst outcomes in the sector, concentrated in for-profit and low-wage fields.Why is the default rate so high for trade and vocational school graduates?

The 30 percent behind-on-payments rate for certificate and associate degree holders reflects several overlapping problems: students at for-profit schools with poor job placement, students who dropped out without completing credentials, and students who entered very low-wage fields (cosmetology, culinary arts) with debt loads their earnings cannot support. Tradespeople in strong-wage fields like electrical, plumbing, and HVAC have significantly better repayment outcomes than this aggregate figure suggests.What does it actually cost to start working as a tradesperson?

Beyond education costs, plan for professional tool costs ($1,000 to $3,000+ depending on trade), a reliable work vehicle if working independently ($15,000 to $35,000 used), and licensing and certification fees ($200 to $1,000 in the first year). The total first-year working costs beyond education, if financed, can add $15,000 to $40,000 in debt to whatever was borrowed for training.What is a registered apprenticeship and why is it the best financial option?

A registered apprenticeship is a DOL-approved earn-while-you-learn programme run by unions, employers, or industry associations. Apprentices are employees from day one, earning approximately 50 percent of a journeyworker’s rate with graduated raises as skills develop. Upon completion, registered apprentices earn an average starting salary of $84,000 (DOL, March 2025 fact sheet). They finish with a nationally recognised credential, a job already in place, and zero debt.What are for-profit trade schools and why are they risky?

For-profit trade and vocational schools are privately owned institutions that often charge much higher tuition than community colleges for comparable credentials, spend heavily on recruiting, and have variable job placement records. The collapse of ITT Technical Institute, which left hundreds of thousands of students with debt and no usable credential, is the most dramatic example. Before enrolling at any for-profit school, verify accreditation, check the school’s Gainful Employment disclosure showing typical debt and earnings for graduates, and compare costs with community college alternatives.Are there loan forgiveness options for trade school debt?

Yes. Federal loan forgiveness programmes do not require a four-year degree. Public Service Loan Forgiveness (PSLF) is available to anyone working in qualifying public service employment — including electricians, HVAC technicians, or plumbers working for government agencies or non-profits — after 120 qualifying payments. Income-Driven Repayment (IDR) plans can also reduce monthly payments, with remaining balances forgiven after 20 to 25 years. Certain healthcare trades may qualify for National Health Service Corps loan repayment of up to $55,000. Trade school borrowers who attended schools that closed may qualify for Closed School Discharge.How much does it cost to start an independent trades business?

Conservatively, $27,000 to $91,000, including a work vehicle, professional tools and equipment, business licensing, liability insurance, initial marketing, and a working capital buffer. Most of this is financed through equipment loans, SBA loans, or personal credit. The monthly debt service on a $50,000 startup financing package is significant and should be planned against realistic revenue projections before making the leap to independent contracting.What is the Pell Grant expansion for trades students in 2026?

Congress passed legislation extending Pell Grant eligibility to shorter-term credential programmes starting July 1, 2026. Students will be able to use up to $4,310 per year for programmes as short as eight weeks covering tuition, books, transportation, and housing at eligible schools specifically designed for career-focused certificate programmes in skilled trades, healthcare, and IT. Students considering trade school programmes shorter than the previous minimum eligibility period should check whether their school qualifies after July 2026.External References and Further Reading

Trade Colleges Directory — Trade School Debt Comparison: Which Trades Get You Working Fastest (March 2026), Trade Colleges Directory — How to Finance Your Trade School Education: A Complete Guide (March 2026), Federal Reserve — Survey of Household Economics and Decisionmaking: Higher Education and Student Loans (2024), Credible — Trade School Loans for Career Training in 2025, LendEDU — Top Student Loans for Trade Schools and Career Programs (2026), The College Investor — Trade School Loan Forgiveness Programs, MetaIntro — University or Trade School in 2026: A Data-Driven Comparison, Apprenticeship.gov — Find a Registered Apprenticeship Program, Federal Student Aid — FAFSA and Aid for Vocational Schools, Bureau of Labor Statistics — Occupational Outlook Handbook: Construction Trades

0 Comments Comments