Finance

UK Debt Advice & Financial Inclusion: The 2026 Picture

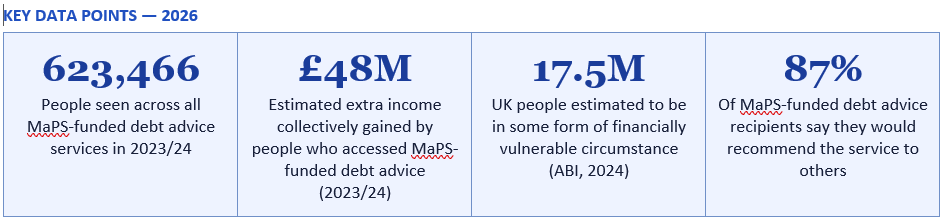

623,466 people accessed MaPS-funded debt advice in 2023/24. Those who did collectively gained an estimated £48 million in extra income. Seventeen and a half million UK people are in some form of financially vulnerable circumstance. The UK government published its first comprehensive Financial Inclusion Strategy in November 2025. This is the definitive guide to where the UK stands on debt advice, financial inclusion, and the policy agenda for long-term resilience — and what it means for individuals who need support right now.

The UK's cost of living crisis has not resolved itself. UK consumer prices are approximately 25% higher than they were in early 2020. Energy bills, rents, mortgage payments, and food costs have all risen faster than wages for most of the period since 2021. And the consequence — for millions of households — is a debt burden that has become unmanageable without professional guidance.

The data is unambiguous. The Money and Pensions Service (MaPS) MoneyView 2026 survey, conducted with 12,647 nationally representative UK adults between August and October 2025, provides the most comprehensive picture available of UK financial wellbeing and the need for debt advice, broken down to local authority and parliamentary constituency level. MaPS measures the 'need for debt advice' using questions drawn from the Debt Need Survey, identifying not only people already in problem debt but also those 'at risk' — at a tipping point who need to seek help before their situation worsens.

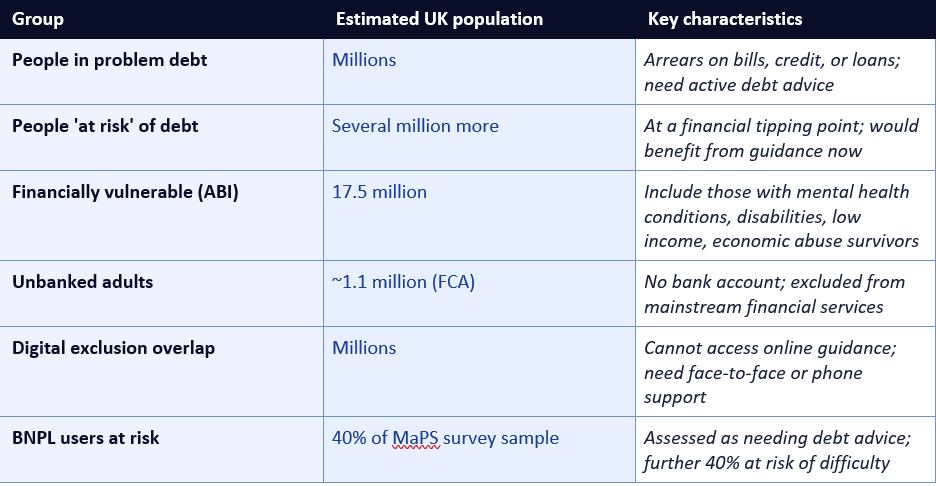

The Association of British Insurers (ABI) estimates that at least 17.5 million people in the UK are in some form of financially vulnerable circumstance — a figure that encompasses those in problem debt, those at risk of falling into it, those with mental health conditions that affect their financial decision-making, those experiencing or recovering from economic abuse, and those excluded from mainstream financial products altogether. These 17.5 million people are the population that the UK's evolving system of debt advice, financial guidance, and financial inclusion policy is designed to serve.

The urgency of the policy context was underlined in November 2025 when the UK government published its first comprehensive Financial Inclusion Strategy — a document five years in the making that represents the most systematic official attempt yet to address the structural causes of financial exclusion in the UK. Understanding what this strategy commits to, and what it means in practice for the people it is designed to help, is the central purpose of this article.

The services we fund are making a real difference. Not only do people access vital debt advice — they come away with greater financial resilience, more income, and significantly less worry. But there remains more to do to ensure provision meets demand.

— MONEY AND PENSIONS SERVICE (MAPS), DEBT ADVICE IMPACT REPORT, 2025

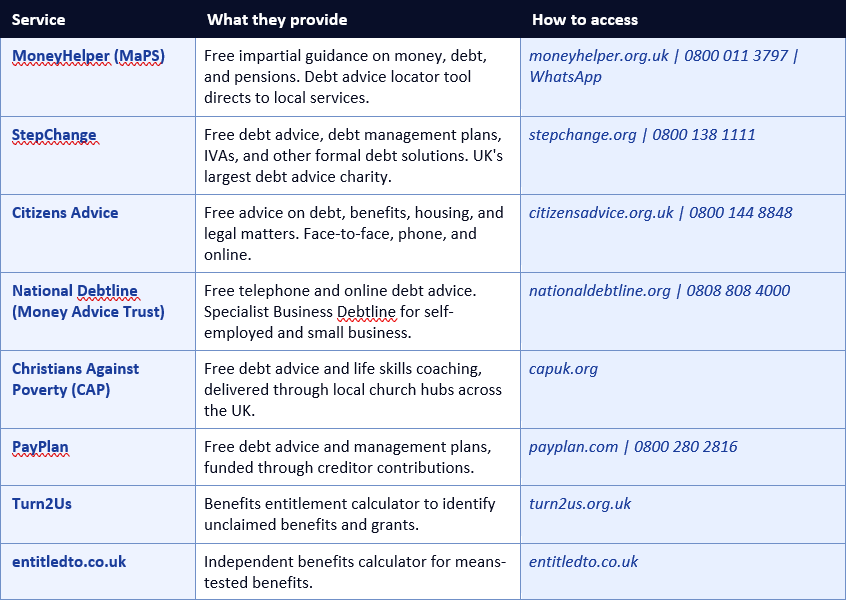

MaPS delivers this purpose through MoneyHelper — its public-facing guidance service, accessible online at moneyhelper.org.uk, by phone on 0800 011 3797, and via WhatsApp, email, and live chat. MoneyHelper provides a comprehensive range of tools, calculators, and expert articles covering budgeting, debt, savings, mortgages, insurance, pension planning, and benefits entitlement. For people in problem debt, MoneyHelper's debt advice locator tool directs users to the appropriate free debt advice service in their area.

An important distinction is that MaPS does not provide debt advice directly. Instead, it commissions and funds a network of debt advice providers — including StepChange, Citizens Advice, National Debtline (run by the Money Advice Trust), Christians Against Poverty, and local money advice services — who deliver face-to-face, telephone, and online debt advice to people in problem debt. MaPS coordinates the UK Strategy for Financial Wellbeing, working with partners across government, the financial services industry, the advice sector, and civil society to improve financial outcomes for the UK population.

MoneyHelper also houses the Pensions Helpline, which provides impartial guidance to people approaching retirement decisions, and coordinates the Pensions Dashboards Programme — the long-running initiative to create a single digital view of all a person's pension savings across different providers. The breadth of MaPS and MoneyHelper's remit reflects the recognition that financial vulnerability is rarely limited to a single domain: households struggling with debt are often also under-saving for retirement, claiming fewer benefits than they are entitled to, and carrying inadequate or no insurance protection.

MaPS's MoneyView data provides local authority and parliamentary constituency level estimates of the 'need for debt advice' — a measure that encompasses both people in active problem debt (arrears, missed payments, debt at unmanageable levels relative to income) and those 'at risk' who are approaching a tipping point. This granular geographic data reveals stark regional variation that national averages conceal: need for debt advice is significantly higher in deprived urban areas, in coastal and former industrial communities, and in areas with high concentrations of private rented accommodation.

The ABI's 2024 assessment that 17.5 million UK people are in some form of financially vulnerable circumstance is the most comprehensive estimate of the population requiring support. This group is not homogeneous: it includes those in crisis (active problem debt, imminent financial collapse), those in chronic vulnerability (persistent low income, inadequate emergency savings, reliance on high-cost credit), and those in circumstantial vulnerability (triggered by a life event such as job loss, relationship breakdown, bereavement, or health deterioration). The FCA's Consumer Duty, introduced in 2023, explicitly requires regulated financial firms to identify and serve all three groups with appropriate care.

In 2023/24, organisations funded by MaPS reported seeing 623,466 people across all debt advice services. Those people collectively gained an estimated £48 million in extra income — a figure that includes unclaimed benefits identified and activated, income maximisation through debt solutions that freed up cash flow, and improved financial management reducing unnecessary expenditure. Put differently, for every pound invested in MaPS-funded debt advice, the return in extra income generated for service users substantially exceeds the cost of provision.

The qualitative outcomes are equally compelling. Eighty-seven per cent of people who received MaPS-funded debt advice said they would recommend the service to someone in a similar situation — an exceptionally high net promoter score for any public service. Sixty-five per cent report worrying less about their debts or financial difficulties after receiving advice. These outcomes reflect the fundamental value of professional debt advice: not simply the technical resolution of debt arrangements, but the restoration of agency, hope, and financial confidence to people who often arrive at advice services feeling overwhelmed, ashamed, and unable to see a way forward.

The Money Advice Trust's parliamentary evidence submission, provided to the HM Treasury committee examining the Financial Inclusion Strategy, noted that Business Debtline — the only dedicated free debt advice service for self-employed people and small business owners in Great Britain — sees 90% of clients with debts that reduce or stabilise following advice. The provision of specialist small business debt advice is particularly important given the overlap between personal and business finances for many sole traders and micro-enterprises.

The strategy acknowledges that financial exclusion is cumulative: affordability pressure, service and product design barriers, and risk-based pricing reinforce one another, pushing households from instability into product-level exclusion and reducing their ability to recover. Key commitments in the strategy include: regulating Buy Now Pay Later (BNPL) products (new rules in force from July 2026), reforming the approach to opening bank accounts for people without standard ID (targeting homeless people and economic abuse survivors), creating a Credit Union Transformation Fund to support credit unions in upgrading technology, expanding the No Interest Loan Scheme, improving contents insurance access for social housing tenants, and addressing coerced debt in the credit files of domestic abuse survivors.

The Hogan Lovells analysis of the strategy, published in November 2025, noted that 'financial inclusion remains a particular area of focus for both the FCA and the government' and highlighted the FCA's planned 2026 focus on capability-by-design at key customer moments, plain-language financial explainers, and shared evaluation frameworks so that successful financial inclusion models can scale across the sector.

The strategy has received broadly positive but critically engaged responses from the advice sector. The Money Advice Trust's parliamentary evidence welcomed the strategy's direction but noted that 'the strategy, unfortunately, lacks detail on a longer-term plan to ensure funding for debt advice is adequate to meet the need.' Citizens Advice and StepChange have similarly called for the strategy to be supported by enforceable minimum standards rather than voluntary commitments, and for lived experience of financial exclusion to be embedded in implementation.

In April 2026, the FCA and the Information Commissioner's Office (ICO) issued a joint statement setting out their expectations of firms for delivering good outcomes for retail consumers in vulnerable circumstances, in line with Consumer Duty, while maintaining compliance with data protection law. This joint statement reflects the practical complexity of serving vulnerable customers: firms need their customers' personal data to identify and support vulnerability, but that data must be handled in accordance with strict privacy requirements. The joint statement provides practical guidance on how firms can navigate this balance.

The consumer protection implications of the Consumer Duty are particularly relevant for BNPL products (now being brought into FCA regulation), high-cost credit products, insurance (where the poverty premium disproportionately affects lower-income consumers), and pension drawdown decisions (where poor choices can have irreversible long-term consequences). The FCA's 2026 supervisory work is expected to focus particularly on mortgage lenders' treatment of customers in payment difficulties — a group that will grow if interest rates remain elevated and fixed-rate terms continue to expire.

The Help to Save scheme, designed to support low-income workers in building savings, illustrates the scale of the engagement gap: 575,200 accounts have been opened since the scheme's launch, against an eligible population of approximately 3 million — a take-up rate of only around 20%. Among those eligible but not enrolled, 58% report lack of awareness as the primary reason. This data point is simultaneously a success story (the scheme works for those who use it) and an indictment of financial engagement (four in five eligible people have not accessed a valuable government-backed savings incentive that could significantly improve their financial resilience).

The pension literacy gap is more acute among specific groups. Women face a structural disadvantage: career breaks, part-time working, and the gender pay gap all reduce pension accumulation, and MaPS's MoneyHelper website has been updated to include specific content on why the gender pension gap exists and how to address it. Gen X — aged 44 to 59, approaching retirement with less time to course-correct — has been identified by both the Aegon Financial Priorities Survey and the MaPS data as the generation most at risk from inadequate pension provision. The Pensions Dashboards Programme — which will allow anyone to see all their pension savings in one place — is a critical infrastructure project for improving pension engagement, though its rollout has been subject to significant delays.

The MaPS survey finding that four in ten BNPL users were assessed as needing debt advice, with a similar proportion at risk of falling into financial difficulty, is one of the most alarming statistics in the financial inclusion landscape. BNPL products are psychologically different from traditional credit in ways that make their debt risks easy to underestimate: each individual transaction is small, the interest is zero (initially), and the product is embedded seamlessly in the checkout process. But the accumulation of multiple BNPL obligations across several providers — each with separate payment schedules, late fees, and credit reporting implications — can create a debt trap that is difficult to exit.

The Financial Inclusion Strategy's commitment to bringing BNPL into FCA regulation — with new rules coming into force in July 2026 — is a welcome development that will require affordability checks, clear information about missed payment consequences, and access to redress for consumers who experience problems. The Government Debt Management Strategy 2026 to 2030 also notes the importance of ensuring BNPL regulation is coherent with the broader consumer credit framework. For consumers currently using BNPL, the key practical steps are to treat each BNPL obligation as debt (because it is), to track all active BNPL balances alongside traditional debt, and to seek advice from MoneyHelper or StepChange if multiple BNPL obligations are becoming difficult to manage.

The UK's new Financial Inclusion Strategy, MaPS's MoneyView data, the FCA's Consumer Duty, and the Government Debt Management Strategy 2026 to 2030 together represent the most coherent official policy framework for financial inclusion that the UK has had. But policy frameworks are only as effective as their implementation — and the advice sector is right to push for enforceable standards, adequate long-term funding, and genuine lived-experience co-production of solutions. For the 17.5 million people in financially vulnerable circumstances, the quality of that implementation is not an abstract question. It is the difference between a debt spiral that takes years to recover from and a supported path to financial stability that restores agency, reduces anxiety, and builds the foundations of long-term resilience.

MaPS — Debt Advice Impact Report 2023/24: Key Findings https://maps.org.uk/en/media-centre/press-releases/2025/debt-advice-funded-by-maps-helps-boost-income

MaPS — Financial Lives of UK People with Debts (January 2026) https://maps.org.uk/en/media-centre/financial-wellbeing-blog/2026/the-financial-lives-of-uk-people-with-debts-in-2024

GOV.UK — UK Financial Inclusion Strategy (HM Treasury, November 2025) https://www.gov.uk/government/publications/financial-inclusion-strategy/financial-inclusion-strategy

Hogan Lovells — Financial Inclusion: UK Government's Strategy 2025 Analysis https://www.hoganlovells.com/en/publications/financial-inclusion-uk-governments-strategy-looks-to-embed-accessibility

Money Advice Trust — Parliamentary Evidence on Financial Inclusion Strategy https://committees.parliament.uk/writtenevidence/161537/pdf/

Shelter England — Debt Matters Round-Up April 2026 https://england.shelter.org.uk/professional_resources/debt_advice/resources_for_debt_advisers/debt_matters_round_up_april_2026

MaPS — UK Strategy for Financial Wellbeing NI Progress Report Summer 2025 https://maps.org.uk/content/dam/maps-corporate/en/our-work/uk-strategy-for-financial-wellbeing/UKSFW%20NI%20progress%20report%20Summer%202025.pdf

MoneyHelper — Free Debt Advice Locator https://www.moneyhelper.org.uk/en/money-troubles/dealing-with-debt/debt-advice-locator

Turn2Us — Benefits Entitlement Calculator https://www.turn2us.org.uk

TABLE OF CONTENTS

- Setting the Scene: Why Debt Advice Has Never Mattered More

- What Is MaPS and What Does MoneyHelper Do?

- The Scale of the Problem: Who Needs Debt Advice in the UK?

- What MaPS-Funded Debt Advice Actually Achieves

- The UK Financial Inclusion Strategy: Published November 2025

- The Five Cross-Cutting Themes of Financial Inclusion

- The FCA's Consumer Duty and Vulnerable Customers

- The Pension Literacy Gap: A Crisis in Slow Motion

- BNPL, Buy Now Pay Later, and the New Debt Frontier

- Barriers to Accessing Debt Advice — and How to Overcome Them

- Help Available Right Now: A Practical Directory

- How to Move from Financial Vulnerability to Financial Resilience

- Conclusion

- Frequently Asked Questions

- References

Setting the Scene: Why Debt Advice Has Never Mattered More

The UK's cost of living crisis has not resolved itself. UK consumer prices are approximately 25% higher than they were in early 2020. Energy bills, rents, mortgage payments, and food costs have all risen faster than wages for most of the period since 2021. And the consequence — for millions of households — is a debt burden that has become unmanageable without professional guidance.The data is unambiguous. The Money and Pensions Service (MaPS) MoneyView 2026 survey, conducted with 12,647 nationally representative UK adults between August and October 2025, provides the most comprehensive picture available of UK financial wellbeing and the need for debt advice, broken down to local authority and parliamentary constituency level. MaPS measures the 'need for debt advice' using questions drawn from the Debt Need Survey, identifying not only people already in problem debt but also those 'at risk' — at a tipping point who need to seek help before their situation worsens.

The Association of British Insurers (ABI) estimates that at least 17.5 million people in the UK are in some form of financially vulnerable circumstance — a figure that encompasses those in problem debt, those at risk of falling into it, those with mental health conditions that affect their financial decision-making, those experiencing or recovering from economic abuse, and those excluded from mainstream financial products altogether. These 17.5 million people are the population that the UK's evolving system of debt advice, financial guidance, and financial inclusion policy is designed to serve.

The urgency of the policy context was underlined in November 2025 when the UK government published its first comprehensive Financial Inclusion Strategy — a document five years in the making that represents the most systematic official attempt yet to address the structural causes of financial exclusion in the UK. Understanding what this strategy commits to, and what it means in practice for the people it is designed to help, is the central purpose of this article.

The services we fund are making a real difference. Not only do people access vital debt advice — they come away with greater financial resilience, more income, and significantly less worry. But there remains more to do to ensure provision meets demand.

— MONEY AND PENSIONS SERVICE (MAPS), DEBT ADVICE IMPACT REPORT, 2025

What Is MaPS and What Does MoneyHelper Do?

The Money and Pensions Service (MaPS) is an arm's-length body of the UK government, sponsored by the Department for Work and Pensions and funded by levies on the financial services industry and pension schemes. Its core purpose is to help everyone in the UK make the most of their money and pensions by providing free, impartial guidance across three domains: money, debt, and pensions.MaPS delivers this purpose through MoneyHelper — its public-facing guidance service, accessible online at moneyhelper.org.uk, by phone on 0800 011 3797, and via WhatsApp, email, and live chat. MoneyHelper provides a comprehensive range of tools, calculators, and expert articles covering budgeting, debt, savings, mortgages, insurance, pension planning, and benefits entitlement. For people in problem debt, MoneyHelper's debt advice locator tool directs users to the appropriate free debt advice service in their area.

An important distinction is that MaPS does not provide debt advice directly. Instead, it commissions and funds a network of debt advice providers — including StepChange, Citizens Advice, National Debtline (run by the Money Advice Trust), Christians Against Poverty, and local money advice services — who deliver face-to-face, telephone, and online debt advice to people in problem debt. MaPS coordinates the UK Strategy for Financial Wellbeing, working with partners across government, the financial services industry, the advice sector, and civil society to improve financial outcomes for the UK population.

MoneyHelper also houses the Pensions Helpline, which provides impartial guidance to people approaching retirement decisions, and coordinates the Pensions Dashboards Programme — the long-running initiative to create a single digital view of all a person's pension savings across different providers. The breadth of MaPS and MoneyHelper's remit reflects the recognition that financial vulnerability is rarely limited to a single domain: households struggling with debt are often also under-saving for retirement, claiming fewer benefits than they are entitled to, and carrying inadequate or no insurance protection.

The Scale of the Problem: Who Needs Debt Advice in the UK?

Understanding the scale of need for debt advice in the UK requires looking beyond the headline figures to the distribution of that need across geography, demographics, and the spectrum of severity.MaPS's MoneyView data provides local authority and parliamentary constituency level estimates of the 'need for debt advice' — a measure that encompasses both people in active problem debt (arrears, missed payments, debt at unmanageable levels relative to income) and those 'at risk' who are approaching a tipping point. This granular geographic data reveals stark regional variation that national averages conceal: need for debt advice is significantly higher in deprived urban areas, in coastal and former industrial communities, and in areas with high concentrations of private rented accommodation.

The ABI's 2024 assessment that 17.5 million UK people are in some form of financially vulnerable circumstance is the most comprehensive estimate of the population requiring support. This group is not homogeneous: it includes those in crisis (active problem debt, imminent financial collapse), those in chronic vulnerability (persistent low income, inadequate emergency savings, reliance on high-cost credit), and those in circumstantial vulnerability (triggered by a life event such as job loss, relationship breakdown, bereavement, or health deterioration). The FCA's Consumer Duty, introduced in 2023, explicitly requires regulated financial firms to identify and serve all three groups with appropriate care.

What MaPS-Funded Debt Advice Actually Achieves

The case for investing in free debt advice is not theoretical — MaPS publishes an annual impact report on the debt advice services it funds, providing one of the most comprehensive evaluations of debt advice effectiveness available anywhere in the world. The 2023/24 impact report, published in 2025, documents both the scale of reach and the quality of outcomes.In 2023/24, organisations funded by MaPS reported seeing 623,466 people across all debt advice services. Those people collectively gained an estimated £48 million in extra income — a figure that includes unclaimed benefits identified and activated, income maximisation through debt solutions that freed up cash flow, and improved financial management reducing unnecessary expenditure. Put differently, for every pound invested in MaPS-funded debt advice, the return in extra income generated for service users substantially exceeds the cost of provision.

The qualitative outcomes are equally compelling. Eighty-seven per cent of people who received MaPS-funded debt advice said they would recommend the service to someone in a similar situation — an exceptionally high net promoter score for any public service. Sixty-five per cent report worrying less about their debts or financial difficulties after receiving advice. These outcomes reflect the fundamental value of professional debt advice: not simply the technical resolution of debt arrangements, but the restoration of agency, hope, and financial confidence to people who often arrive at advice services feeling overwhelmed, ashamed, and unable to see a way forward.

The Money Advice Trust's parliamentary evidence submission, provided to the HM Treasury committee examining the Financial Inclusion Strategy, noted that Business Debtline — the only dedicated free debt advice service for self-employed people and small business owners in Great Britain — sees 90% of clients with debts that reduce or stabilise following advice. The provision of specialist small business debt advice is particularly important given the overlap between personal and business finances for many sole traders and micro-enterprises.

The UK Financial Inclusion Strategy: Published November 2025

On 5 November 2025, HM Treasury published the UK's first comprehensive Financial Inclusion Strategy — a document that represents the most systematic official framework for addressing financial exclusion since the establishment of MaPS itself. The strategy defines financial inclusion as the ability to participate in the economy, manage finances effectively, and plan for the future — framing it as a matter of economic participation rather than simply product access.The strategy acknowledges that financial exclusion is cumulative: affordability pressure, service and product design barriers, and risk-based pricing reinforce one another, pushing households from instability into product-level exclusion and reducing their ability to recover. Key commitments in the strategy include: regulating Buy Now Pay Later (BNPL) products (new rules in force from July 2026), reforming the approach to opening bank accounts for people without standard ID (targeting homeless people and economic abuse survivors), creating a Credit Union Transformation Fund to support credit unions in upgrading technology, expanding the No Interest Loan Scheme, improving contents insurance access for social housing tenants, and addressing coerced debt in the credit files of domestic abuse survivors.

The Hogan Lovells analysis of the strategy, published in November 2025, noted that 'financial inclusion remains a particular area of focus for both the FCA and the government' and highlighted the FCA's planned 2026 focus on capability-by-design at key customer moments, plain-language financial explainers, and shared evaluation frameworks so that successful financial inclusion models can scale across the sector.

The strategy has received broadly positive but critically engaged responses from the advice sector. The Money Advice Trust's parliamentary evidence welcomed the strategy's direction but noted that 'the strategy, unfortunately, lacks detail on a longer-term plan to ensure funding for debt advice is adequate to meet the need.' Citizens Advice and StepChange have similarly called for the strategy to be supported by enforceable minimum standards rather than voluntary commitments, and for lived experience of financial exclusion to be embedded in implementation.

The Five Cross-Cutting Themes of Financial Inclusion

The UK Financial Inclusion Strategy identifies several cross-cutting themes that shape the experience of financial exclusion across different population groups.Mental health and financial difficulty

The strategy explicitly addresses the relationship between mental health conditions and financial difficulty — a relationship that runs in both directions. Financial stress is a leading trigger and exacerbator of mental health conditions; mental health conditions impair financial decision-making and create barriers to accessing help. The FCA's Consumer Duty requires firms to identify customers whose mental health affects their financial decisions and to provide appropriate support — adjusted communications, flexible payment options, signposting to specialist services. MaPS's Money Guiders programme, which trains frontline workers across sectors to identify and support people with financial difficulties, includes specific modules on trauma-informed approaches and supporting people with mental health needs.Accessibility and digital exclusion

The pace of financial services digitisation has created a practical exclusion risk for households that cannot reliably use digital services — including older adults, people with certain disabilities, and those in areas of poor digital connectivity or who cannot afford digital devices. The strategy recognises this risk and commits to maintaining non-digital access routes to financial services and guidance. Wales has launched a national Digital Inclusion programme commencing October 2025, funded to run through September 2028, specifically targeting organisations supporting people who are digitally excluded or at risk. The Minimum Digital Living Standard pilot, expanded during 2025/26, defines the baseline digital capability required to participate effectively in modern economic life.Economic abuse and coerced debt

Economic abuse — the use of financial control, coercion, and exploitation as a form of domestic abuse — is explicitly addressed in the Financial Inclusion Strategy for the first time in a major government financial policy document. Victims of economic abuse frequently find their credit files damaged by debts taken out in their name or under coercion, making it difficult to access financial products after leaving an abusive relationship. The strategy commits to working with the three largest Credit Reference Agencies, lenders, and Surviving Economic Abuse to develop an improved approach to reflecting coerced debt on credit files, and to exploring how joint mortgages are used as tools of abuse.Financial inclusion for vulnerable and marginalised groups

The strategy identifies several populations with disproportionately high financial exclusion: lone-parent households (with child poverty rates of 44% among children in lone-parent families, per JRF 2024), people with disabilities, people from racially minoritised backgrounds, and people experiencing homelessness. The Government Debt Management Strategy 2026 to 2030, published alongside the Financial Inclusion Strategy, focuses specifically on improving government's own approach to debt management with vulnerable customers — recognising that government debt (council tax arrears, benefit overpayments, DWP debts) can itself be a source of financial exclusion and harm.The FCA's Consumer Duty and Vulnerable Customers

The Financial Conduct Authority's Consumer Duty, which came into force for existing products in July 2024, represents a significant regulatory ratchet in the standards required of financial services firms in their treatment of customers in vulnerable circumstances. The Duty requires firms to deliver good outcomes for retail customers — specifically around products and services, price and value, consumer understanding, and consumer support. For vulnerable customers, this means identifying them, adjusting communications and services appropriately, and not designing products that exploit their vulnerabilities.In April 2026, the FCA and the Information Commissioner's Office (ICO) issued a joint statement setting out their expectations of firms for delivering good outcomes for retail consumers in vulnerable circumstances, in line with Consumer Duty, while maintaining compliance with data protection law. This joint statement reflects the practical complexity of serving vulnerable customers: firms need their customers' personal data to identify and support vulnerability, but that data must be handled in accordance with strict privacy requirements. The joint statement provides practical guidance on how firms can navigate this balance.

The consumer protection implications of the Consumer Duty are particularly relevant for BNPL products (now being brought into FCA regulation), high-cost credit products, insurance (where the poverty premium disproportionately affects lower-income consumers), and pension drawdown decisions (where poor choices can have irreversible long-term consequences). The FCA's 2026 supervisory work is expected to focus particularly on mortgage lenders' treatment of customers in payment difficulties — a group that will grow if interest rates remain elevated and fixed-rate terms continue to expire.

The Pension Literacy Gap: A Crisis in Slow Motion

One of the most important but least visible dimensions of the financial inclusion agenda is pension literacy — the understanding and engagement with pension savings that determines whether people accumulate adequate retirement income. MaPS coordinates the UK Strategy for Financial Wellbeing, which identifies pensions as a critical area of financial capability gap across the population.The Help to Save scheme, designed to support low-income workers in building savings, illustrates the scale of the engagement gap: 575,200 accounts have been opened since the scheme's launch, against an eligible population of approximately 3 million — a take-up rate of only around 20%. Among those eligible but not enrolled, 58% report lack of awareness as the primary reason. This data point is simultaneously a success story (the scheme works for those who use it) and an indictment of financial engagement (four in five eligible people have not accessed a valuable government-backed savings incentive that could significantly improve their financial resilience).

The pension literacy gap is more acute among specific groups. Women face a structural disadvantage: career breaks, part-time working, and the gender pay gap all reduce pension accumulation, and MaPS's MoneyHelper website has been updated to include specific content on why the gender pension gap exists and how to address it. Gen X — aged 44 to 59, approaching retirement with less time to course-correct — has been identified by both the Aegon Financial Priorities Survey and the MaPS data as the generation most at risk from inadequate pension provision. The Pensions Dashboards Programme — which will allow anyone to see all their pension savings in one place — is a critical infrastructure project for improving pension engagement, though its rollout has been subject to significant delays.

BNPL, Buy Now Pay Later, and the New Debt Frontier

Buy Now Pay Later — the facility to split purchases into interest-free instalments, offered by providers including Klarna, Clearpay, and Laybuy — has grown from a niche retail payment option to a mainstream consumer finance product used by millions of UK adults, particularly younger consumers making fashion and consumer goods purchases online.The MaPS survey finding that four in ten BNPL users were assessed as needing debt advice, with a similar proportion at risk of falling into financial difficulty, is one of the most alarming statistics in the financial inclusion landscape. BNPL products are psychologically different from traditional credit in ways that make their debt risks easy to underestimate: each individual transaction is small, the interest is zero (initially), and the product is embedded seamlessly in the checkout process. But the accumulation of multiple BNPL obligations across several providers — each with separate payment schedules, late fees, and credit reporting implications — can create a debt trap that is difficult to exit.

The Financial Inclusion Strategy's commitment to bringing BNPL into FCA regulation — with new rules coming into force in July 2026 — is a welcome development that will require affordability checks, clear information about missed payment consequences, and access to redress for consumers who experience problems. The Government Debt Management Strategy 2026 to 2030 also notes the importance of ensuring BNPL regulation is coherent with the broader consumer credit framework. For consumers currently using BNPL, the key practical steps are to treat each BNPL obligation as debt (because it is), to track all active BNPL balances alongside traditional debt, and to seek advice from MoneyHelper or StepChange if multiple BNPL obligations are becoming difficult to manage.

Barriers to Accessing Debt Advice — and How to Overcome Them

Despite the availability of free, high-quality debt advice from MaPS-funded services, StepChange, Citizens Advice, National Debtline, and others, demand for debt advice consistently exceeds supply and many people who need advice do not access it. Understanding the barriers is essential for overcoming them.Common barriers to accessing debt advice — and how to address them

- Shame and stigma: Debt Awareness Week 2025, organised by StepChange, focused specifically on the shame and stigma that prevent many people from seeking help. Research consistently shows that the emotional barriers to accessing debt advice — embarrassment, fear of judgment, reluctance to admit the problem even to oneself — delay help-seeking and allow debt situations to worsen significantly before advice is sought. Recognising that debt advice is used by hundreds of thousands of ordinary people each year, and that advisers are trained to respond without judgment, is the first step to overcoming this barrier.

- Lack of awareness: The single most common reason eligible people do not access Help to Save (58% of non-users) is lack of awareness that the scheme exists. The same pattern applies to debt advice: many people in problem debt do not know that free professional advice is available or do not know how to access it. MoneyHelper's debt advice locator (moneyhelper.org.uk/en/money-troubles/dealing-with-debt/debt-advice-locator) connects users with the most appropriate local or national service.

- Feeling overwhelmed: Many people delay seeking debt advice because the problem feels too large to face. Debt advisers consistently report that clients who take this view almost always feel significantly better after their first appointment — the act of getting an accurate picture of the situation, however challenging, is experienced as a relief compared with the anxiety of not knowing. The first step is the hardest.

- Digital access barriers: Not everyone can access online debt advice. MoneyHelper is available by phone (0800 011 3797, free), by WhatsApp, and through a network of face-to-face providers accessible via the debt advice locator. Citizens Advice provides in-person advice at hundreds of locations across the UK.

- Fear of consequences: Some people avoid seeking debt advice because they fear it will make their situation worse — that advisers will report them to creditors, trigger enforcement action, or damage their credit file. This fear is largely unfounded: debt advisers work in the interests of the client and cannot initiate enforcement action. The process of taking advice, including the identification of formal debt solutions where appropriate, typically gives clients more control over their situation, not less.

Help Available Right Now: A Practical Directory

For anyone in the UK who is currently struggling with debt or financial difficulty, the following services provide free, confidential, professional support.How to Move from Financial Vulnerability to Financial Resilience

Accessing debt advice is the critical first step for those in or approaching problem debt. But the journey from financial vulnerability to genuine financial resilience requires a more sustained process of rebuilding financial foundations. MaPS's UK Strategy for Financial Wellbeing identifies five goals that together constitute financial wellbeing: managing day to day, building a safety net, planning ahead, borrowing when needed, and saving for retirement.A six-stage path from financial vulnerability to financial resilience

- Stage 1 — Stabilise: Address immediate crisis — missed payments, arrears, enforcement threats. Get debt advice from a free provider (MoneyHelper, StepChange, or Citizens Advice). Stop the bleeding before building anything.

- Stage 2 — Maximise income: Check your full benefit entitlement at turn2us.org.uk or entitledto.co.uk. Millions of UK households are not claiming benefits they are entitled to, including Universal Credit, Child Benefit, Council Tax Reduction, and Carer's Allowance. For those in low-paid work, check eligibility for the Help to Save scheme — a government-backed savings account paying a 50% bonus on savings of up to £50 per month for eligible workers.

- Stage 3 — Build a minimal buffer: Before making any other financial progress, build £1,000 in accessible savings. This prevents any unexpected expense — a car repair, an appliance breakdown, a period of sick leave — from forcing new borrowing and restarting the debt cycle.

- Stage 4 — Address the debt: Once income is maximised and a minimal buffer is in place, work with your debt adviser to implement the most appropriate debt solution — a debt management plan, a Debt Relief Order, an IVA, or simply a structured repayment plan agreed with creditors. Follow through consistently.

- Stage 5 — Start saving deliberately: Once debt is under control, redirect the cash flow freed up by reducing debt payments into regular savings. Even £20 to £50 per month into an accessible savings account begins building the financial cushion that protects against future vulnerability.

- Stage 6 — Engage with your pension: Check your State Pension forecast at gov.uk/check-state-pension. Check whether you are enrolled in your workplace pension and whether your employer offers a match above the minimum. Make additional voluntary contributions if at all possible — even small increases at an early stage compound significantly over time. Use MaPS's MoneyHelper pension calculator at moneyhelper.org.uk to understand your projected retirement income.

CONCLUSION

The rising need for debt advice in the UK is not a story of individual failure. It is the cumulative consequence of five years of cost of living pressure, structural underinvestment in financial capability, a regulatory environment that is only now beginning to address the risks of modern credit products like BNPL, and an advice system that — despite serving over 623,000 people per year and generating £48 million in extra income for its users — remains under-resourced relative to demand.The UK's new Financial Inclusion Strategy, MaPS's MoneyView data, the FCA's Consumer Duty, and the Government Debt Management Strategy 2026 to 2030 together represent the most coherent official policy framework for financial inclusion that the UK has had. But policy frameworks are only as effective as their implementation — and the advice sector is right to push for enforceable standards, adequate long-term funding, and genuine lived-experience co-production of solutions. For the 17.5 million people in financially vulnerable circumstances, the quality of that implementation is not an abstract question. It is the difference between a debt spiral that takes years to recover from and a supported path to financial stability that restores agency, reduces anxiety, and builds the foundations of long-term resilience.

Frequently Asked Questions

What is MaPS and how is it different from MoneyHelper?

The Money and Pensions Service (MaPS) is the government arm's-length body — sponsored by the Department for Work and Pensions and funded by levies on financial services firms — that coordinates the UK Strategy for Financial Wellbeing, commissions and funds debt advice services, and coordinates the Pensions Dashboards Programme. MoneyHelper is MaPS's public-facing brand: the free guidance service accessible online at moneyhelper.org.uk, by phone on 0800 011 3797, and via WhatsApp. MaPS does not provide debt advice directly — it funds a network of providers (including StepChange, Citizens Advice, and National Debtline) and directs the public to them via MoneyHelper's debt advice locator.How many people access MaPS-funded debt advice and does it work?

In 2023/24, 623,466 people were seen across all MaPS-funded debt advice services in England (MaPS commissions debt advice in England specifically). People who received that advice collectively gained an estimated £48 million in extra income — through unclaimed benefits identified, cash flow freed by debt solutions, and improved financial management. Eighty-seven per cent of recipients would recommend the service, and 65% report worrying less about their debts after advice. For the Money Advice Trust's Business Debtline, 90% of clients see their debts reduce or stabilise. The evidence base for the effectiveness of free debt advice is robust and consistent.What is the UK Financial Inclusion Strategy and what does it commit to?

The UK Financial Inclusion Strategy was published by HM Treasury on 5 November 2025 — the first comprehensive financial inclusion framework the UK government has produced. It defines financial inclusion as the ability to participate in the economy, manage finances, and plan for the future. Key commitments include: BNPL regulation coming into force July 2026, bank account access for people without standard ID, a Credit Union Transformation Fund, an expanded No Interest Loan Scheme, addressing coerced debt in domestic abuse survivors' credit files, and a focus on mental health and digital accessibility as cross-cutting themes. The advice sector has broadly welcomed the strategy's direction while calling for more enforceable standards and long-term debt advice funding commitments.What is BNPL and why is it a financial inclusion concern?

Buy Now Pay Later (BNPL) is the facility to split purchases into interest-free instalments, offered by providers including Klarna, Clearpay, and Laybuy. It has become a mainstream consumer finance product particularly popular with younger shoppers. The financial inclusion concern is that BNPL users can easily accumulate multiple obligations across several providers, each with separate payment schedules and late fees, creating a debt trap that is psychologically difficult to recognise and practically difficult to manage. MaPS data found that 4 in 10 BNPL users surveyed were assessed as needing debt advice, with a similar proportion at risk of falling into financial difficulty. BNPL products are coming into FCA regulation from July 2026, requiring affordability checks and clear information about missed payment consequences.What should I do if I am struggling with debt in the UK?

The single most important step is to seek free professional debt advice as early as possible. Use MoneyHelper's debt advice locator at moneyhelper.org.uk to find the most appropriate service near you, or contact StepChange (stepchange.org, or 0800 138 1111), Citizens Advice (citizensadvice.org.uk, or 0800 144 8848), or National Debtline (nationaldebtline.org, or 0808 808 4000) directly. All of these services are free, confidential, and non-judgmental. Before your appointment, gather a list of all your debts, income, and essential outgoings — the more complete your picture, the more useful the advice will be. Also check your full benefit entitlement at turn2us.org.uk, as many households in financial difficulty are not claiming all the support they are entitled to.What is the pension literacy gap and why does it matter?

The pension literacy gap describes the widespread lack of awareness, understanding, and engagement with pension savings among UK adults — despite the fact that adequate pension savings are the primary determinant of financial security in retirement. The Help to Save scheme illustrates the gap concretely: 3 million people are eligible, but only around 575,200 (approximately 20%) have opened an account, primarily because they are unaware it exists. Women and Gen X face the most acute pension saving deficits due to career breaks, part-time working, and the proximity of retirement with less time to accumulate savings. MaPS coordinates the Pensions Dashboards Programme — which will allow everyone to see all their pension savings in one place — and provides free pension guidance through MoneyHelper's Pensions Helpline.References

Money and Pensions Service (MaPS) — MoneyView 2026 Survey (12,647 UK adults, Summer 2025) https://maps.org.uk/en/publications/moneyviewMaPS — Debt Advice Impact Report 2023/24: Key Findings https://maps.org.uk/en/media-centre/press-releases/2025/debt-advice-funded-by-maps-helps-boost-income

MaPS — Financial Lives of UK People with Debts (January 2026) https://maps.org.uk/en/media-centre/financial-wellbeing-blog/2026/the-financial-lives-of-uk-people-with-debts-in-2024

GOV.UK — UK Financial Inclusion Strategy (HM Treasury, November 2025) https://www.gov.uk/government/publications/financial-inclusion-strategy/financial-inclusion-strategy

Hogan Lovells — Financial Inclusion: UK Government's Strategy 2025 Analysis https://www.hoganlovells.com/en/publications/financial-inclusion-uk-governments-strategy-looks-to-embed-accessibility

Money Advice Trust — Parliamentary Evidence on Financial Inclusion Strategy https://committees.parliament.uk/writtenevidence/161537/pdf/

Shelter England — Debt Matters Round-Up April 2026 https://england.shelter.org.uk/professional_resources/debt_advice/resources_for_debt_advisers/debt_matters_round_up_april_2026

MaPS — UK Strategy for Financial Wellbeing NI Progress Report Summer 2025 https://maps.org.uk/content/dam/maps-corporate/en/our-work/uk-strategy-for-financial-wellbeing/UKSFW%20NI%20progress%20report%20Summer%202025.pdf

MoneyHelper — Free Debt Advice Locator https://www.moneyhelper.org.uk/en/money-troubles/dealing-with-debt/debt-advice-locator

Turn2Us — Benefits Entitlement Calculator https://www.turn2us.org.uk

0 Comments Comments