The Anti-Budget: The No-Budget Budget

In today's world, getting financial freedom seems hard. But a new way to handle money has come along - the anti-budget. A study found that over 60% of people using this method hit their savings goals. Some even saved 50% of their income and reached financial independence.

The anti-budget is a simple way to manage money without strict rules. It aims to save 20-30% of what you earn and lets you spend the rest freely. This method puts saving first, without needing to track every expense. It's great for those who hate the details of traditional budgets or can't stick to them.

Key Takeaways

- The anti-budget focuses on saving 20-30% of your income, with freedom to spend the rest.

- It's perfect for those overwhelmed by traditional budgeting or can't keep up with it.

- This approach helps achieve financial freedom by focusing on savings and goals, not tracking every expense.

- Starting with the anti-budget means setting up automatic savings, finding the right savings rate, and building an emergency fund.

- While simple, the anti-budget requires discipline and a commitment to saving to succeed financially.

Understanding the Anti-Budget Revolution

Traditional budgets often fail because they're too complex and take up a lot of time. The anti-budget method is a new way to handle money. It's based on three easy steps: set savings goals, make savings automatic, and spend the rest freely.

Why Traditional Budgets Often Fail

Old-fashioned budgets can be too much to handle. They require tracking every penny and organizing spending into categories. This can get frustrating and lead people to give up on budgeting. The budgeting type is simpler, perfect for those who like living simply and saving money.

Core Principles of the Anti-Budget Method

- Set Savings Goals: Decide how much you want to save each month or year, based on your financial goals.

- Automate Savings: Set up automatic transfers from your checking to savings, so you always meet your savings goals.

- Spend Freely: Use the money left in your checking for daily expenses, without needing to track every purchase.

Who Benefits Most from this Approach

- Individuals with Varying Incomes: It's great for those with changing incomes, as it doesn't require a strict spending plan.

- People Who Dislike Meticulous Tracking: For those who hate keeping detailed records, the anti-budget's simplicity is a big plus.

- Those Seeking a Low-Maintenance Financial Strategy: The anti-budget offers flexibility while still focusing on savings and goals, appealing to those who prefer a simpler financial life.

By following the this budgeting core principles, people can live more frugally and reach their financial goals without the hassle of complex budgeting.

The Anti-Budget: The No-Budget Budget

Handling personal finances can be tough, and traditional budgets often don't cut it. That's where the anti-budget, or no-budget budget, comes in. It's a simple way to focus on financial freedom and smart spending.

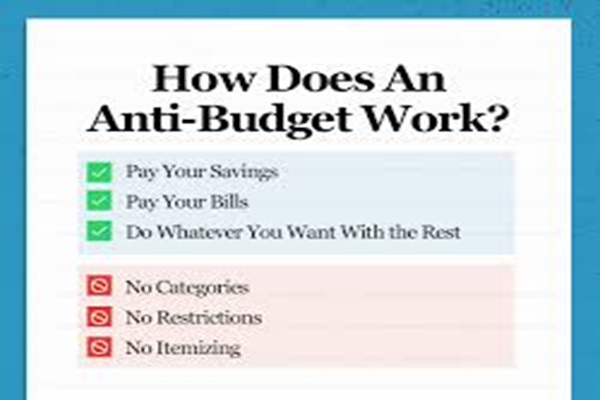

The anti-budget's main idea is to save first. You decide on a savings percentage, like 20-30% of your income. This amount goes straight to savings or investments. Then, you can use the rest for money management and spending without worrying about categories.

This method gets rid of the hassle of tracking every expense. It lets you make smart choices about how you spend your money. By setting up automatic savings, you're always moving closer to your financial goals. This makes it great for those who hate traditional budgeting.

"The anti-budget differs from a traditional budget in that it focuses on supporting goals rather than tracking expenses." - Dr. Brad Klontz

You can use your remaining money for bills, paying off debt, or fun stuff. It helps you manage your finances in a way that feels right for you. This leads to a better sense of control and financial freedom.

This budgeting type isn't for everyone, but it's a good alternative to strict budgets. It puts saving first and lets you make smart choices about your money. This way, you can work towards financial freedom and smart spending in a more flexible way.

Implementation Strategies for Financial Success

Starting with the anti-budget approach to money needs a solid plan. It's about getting rid of debt, growing your wealth, and spending wisely. A key step is to set up automatic transfers to save or invest a part of your income.

Setting Up Automatic Transfers

Making saving easy is the heart of anti-budgeting. By automating it, you ensure savings before spending. This method boosts your emergency fund and investments, keeping you from spending it elsewhere.

Determining Your Optimal Savings Rate

There's no single savings goal for everyone. Experts suggest saving 20-30% of your income. This balance helps you spend now and save for later. Adjust your savings rate for your debt elimination or wealth building goals.

Creating Emergency Fund Buffers

Building an emergency fund is key in your savings plan. Aim for 3-6 months' living expenses. This fund protects you from unexpected costs, keeping your smart spending on track.

Adopting this budgeting method requires patience and discipline. But, the rewards are worth it. Automate your savings, find your savings rate, and build an emergency fund. You'll be on the path to financial freedom and security.

Benefits and Limitations of Anti-Budgeting

This budgeting approach has many perks for those aiming for financial freedom and a simple life. It makes budgeting easier, cuts down on stress, and ensures a part of your income is saved. This is great for people with changing incomes, as it lets them spend without feeling guilty.

But, the anti-budget might not work for everyone. It can be hard for those with big debts or who are new to budgeting to track expenses. It also needs discipline to not spend too much on the "free" part of your income. And, it might need changes when your life or finances change a lot.

| Benefits of Anti-Budgeting | Limitations of Anti-Budgeting |

|---|---|

| Simplifies the budgeting process Reduces financial stress Ensures a guaranteed portion of income is saved Provides flexibility for those with variable incomes Promotes a guilt-free approach to spending | May not be suitable for individuals with significant debt or new to budgeting Lack of detailed expense tracking can make it challenging to identify areas for cost-cutting Requires discipline to avoid overspending the "free" portion of income May need adjustments during major life changes or financial shifts |

The anti-budget is a simple way to manage money that can lead to financial freedom and a simple life. It has many benefits, but it's important to think about your own financial situation and goals. This will help you decide if the anti-budget is right for you.

Conclusion

The anti-budget approach makes achieving financial freedom, money management, and wealth building simpler. It focuses on saving and allows for flexible spending. This method helps reduce financial stress and helps people reach their long-term goals.

This method might not work for everyone. But it shows the value of being flexible with finances. Success needs discipline and knowing your financial situation well. It's key to keep reviewing and adjusting the budget to fit your changing needs.

Embracing the anti-budget can help cut down on impulse buys and build emergency funds. It leads to more financial freedom and better money management. It's is a flexible, empowering choice for today's fast-changing world, helping in wealth building.