Knowledge

8 Things to Never Keep in Your Wallet After 60

Table of Contents

- Why Wallet Security Matters More After 60: The Statistics

- The 8 Things: Quick Reference Guide

- The 8 Items in Depth

- #1 — Your Social Security Card

- #2 — Your Medicare Card

- #3 — Written-Down PINs or Passwords

- #4 — Multiple Credit and Debit Cards You Rarely Use

- #5 — Blank Checks

- #6 — Your Passport or Passport Card

- #7 — Spare House or Car Keys

- #8 — Unused Gift Cards With Significant Balances

- What a Sensible Wallet Actually Contains After 60

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Think about what is sitting in your wallet right now. Most people carry the same collection of cards and documents they have accumulated over years — adding things as they arrive without ever taking stock of what should be removed. After 60, that habit becomes a genuine financial risk, because the contents of a lost or stolen wallet can do far more damage to someone whose accounts contain decades of savings than to a younger person just starting out.

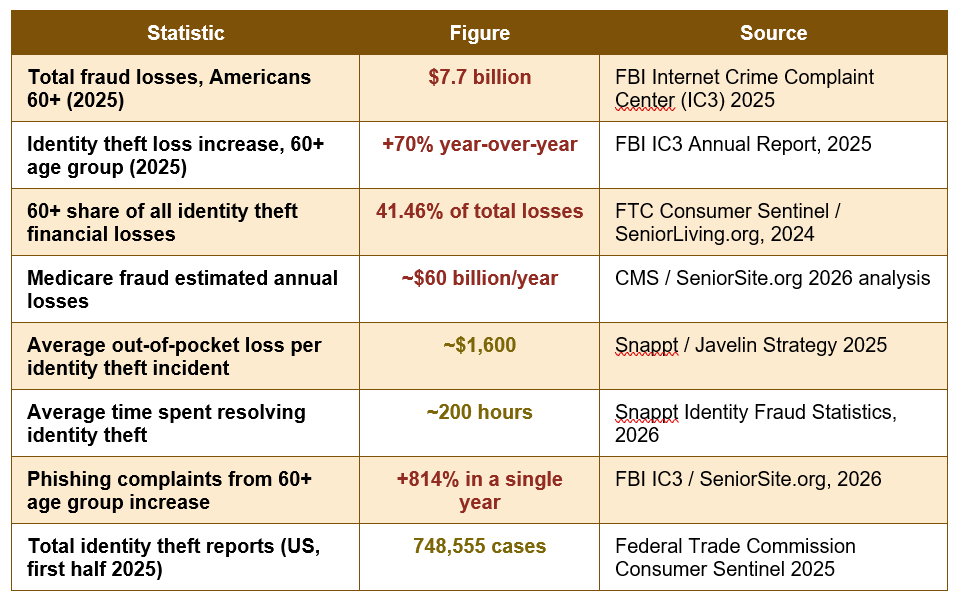

Americans aged 60 and older reported $7.7 billion in fraud losses in 2025, the highest of any age group, according to the FBI's Internet Crime Complaint Center. Identity theft losses for this age group surged 70% in a single year. These losses are not primarily driven by sophisticated digital hacking — they are driven by the theft of physical documents and cards that give criminals direct access to Social Security numbers, Medicare numbers, financial accounts, and the keys to the rest of a person's identity.

The good news is that wallet security is one of the simplest, most immediately actionable things you can do to reduce your exposure. It does not require any technology, any app, or any subscription. It requires a ten-minute audit of what you are carrying and the willingness to relocate or remove the items on this list. This guide covers exactly what those items are, why each one is specifically dangerous in a lost or stolen wallet, and what to do instead.

Why Wallet Security Matters More After 60: The Statistics

The data on fraud and identity theft affecting Americans over 60 makes a compelling case for taking wallet security seriously:

Fraud losses for 60+ Americans in 2025: $7.7 billion — highest of any age group — FBI IC3 data shows older Americans' losses exceed younger age groups not because they are targeted more often, but because they typically have larger account balances — meaning each successful fraud incident is far more financially devastating.

Why seniors experience greater losses per incident: FBI IC3 data consistently shows that fraud complaints from Americans 60 and older involve bank accounts, retirement funds, and investment portfolios at higher rates than other age groups. A single wallet theft that exposes a Social Security Number, a Medicare card, and three bank cards can give criminals access to accounts representing decades of accumulated savings — a far higher-value target than the same theft from a 30-year-old's wallet.

The 8 Things: Quick Reference Guide

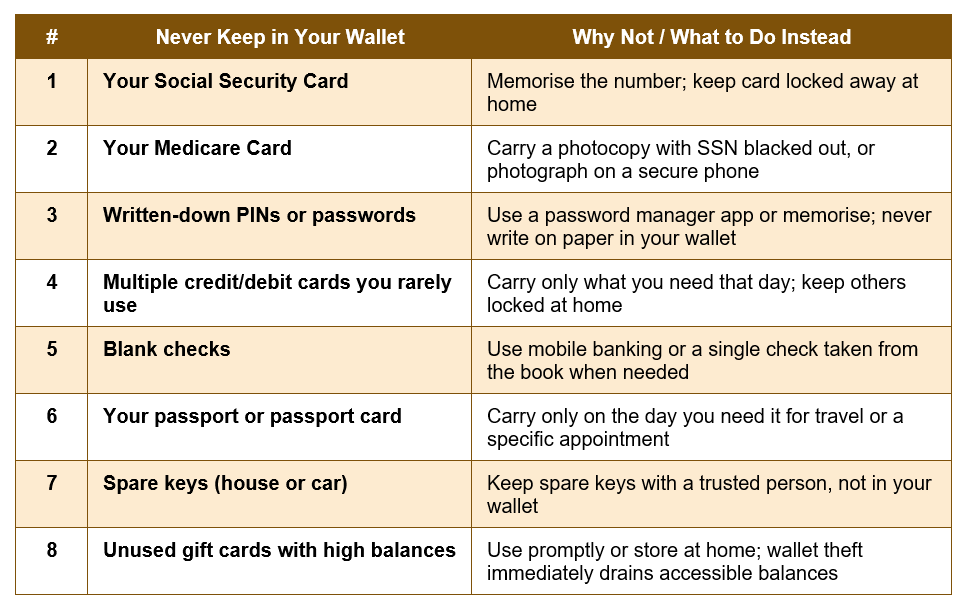

Before exploring each item in depth, the table below provides a quick-reference summary of all 8 items, the core reason to remove each, and what to do instead:

The 8 Items in Depth

#1 — Your Social Security Card

This is, without question, the single most dangerous document most Americans routinely carry — and the single most unnecessary one. Your Social Security Number is the master key to your identity: it is what criminals use to open new credit accounts in your name, file fraudulent tax returns to intercept your refund, access government benefits, and even create entirely new synthetic identities. Once your SSN is in a criminal's hands, the damage can persist for years and affect your ability to borrow, file taxes, and access benefits long after the initial theft.The solution is simple: your Social Security card almost never needs to be physically present at any appointment you attend. Healthcare providers, employers, and government offices will ask for your number verbally or on a form — they do not need to hold or copy the physical card. Memorise your number, which most people over 60 already know from decades of use, and leave the card in a locked drawer at home. The number in your head cannot be stolen from your wallet.

#2 — Your Medicare Card

Your Medicare card carries your Medicare Beneficiary Identifier (MBI) — a number that is used to bill Medicare for healthcare services and which, in the wrong hands, can be used to submit fraudulent claims for services you never received. Medicare loses an estimated $60 billion annually to fraud, errors, and abuse, and medical identity theft is among the most common schemes targeting adults over 60, in part because compromised Medicare numbers can be exploited repeatedly before the fraud is detected in billing statements.There is a practical alternative here: take a photocopy of your Medicare card, black out the last four characters of your MBI with a permanent marker, and carry that copy instead of the original. In genuine healthcare emergencies, providers can verify your identity and coverage with partial information and your ID; in routine appointments, bring the original card only when specifically required. As a secondary option, a photograph of your card stored in a password-protected folder on your smartphone (not in the standard photo gallery) provides access without the physical card being pickpocket-able.

#3 — Written-Down PINs or Passwords

It sounds almost too obvious to include — but it is on this list precisely because it is more common than most people would expect. The habit of writing down a PIN or password on a small piece of paper and tucking it somewhere in the wallet — often because a bank issued a new card and the number needs to be remembered until it is memorised — is among the most dangerous things a person can do.A stolen wallet that contains both a bank card and a note with the PIN written on it (sometimes on the back of the card itself) effectively removes every security layer the card was designed to provide. ATM withdrawals can begin immediately, with no additional verification required. If you genuinely struggle to memorise a PIN, consider changing it to a number that is personally memorable — not a birthday or obvious sequence, but something meaningful only to you — and always memorise rather than record it.

#4 — Multiple Credit and Debit Cards You Rarely Use

Many people accumulate cards over the years — a retail store card opened for a one-time discount, an old bank card from an account that was never closed, a second debit card from a joint account, a credit card kept for emergencies that has not been used in two years. Carrying all of these simultaneously multiplies your exposure in a wallet loss: each card requires a separate cancellation call, each may have its own PIN or account details compromised, and each adds recovery time and complexity that can leave fraudulent transactions slipping through while you work through the list.The practical approach is to conduct a regular wallet audit: carry only the one or two cards you expect to use on a given day or week. Keep the rest in a secure location at home. If you have cards you genuinely never use, consider whether the account should remain open at all — a dormant card that generates a credit report inquiry can sometimes indicate fraud before you would otherwise notice.

#5 — Blank Checks

A blank check from your checkbook is an extraordinarily powerful document in a thief's hands. It contains your full name, your bank's routing number, and your account number — the three pieces of information needed to initiate an unauthorised electronic payment from your account, print counterfeit checks, or set up fraudulent direct debit arrangements. Unlike a credit card, where fraud liability is limited under the Fair Credit Billing Act, recovering money withdrawn from a checking account via forged check can be significantly more difficult and time-consuming.If you write checks regularly, take individual checks from your checkbook on a per-use basis rather than carrying a folded blank in your wallet 'just in case.' For most routine transactions that once required a check, mobile banking apps, bill pay services, and bank transfers now provide a safer and faster alternative.

#6 — Your Passport or Passport Card

A full passport or passport card should only leave its secure storage on days when you specifically need it — international travel, certain visa or legal appointments, or situations where it is the designated acceptable form of ID. Carrying it as routine identification in a daily wallet is unnecessary in the vast majority of situations where a driver's license serves the same purpose and exposes considerably less personal and citizenship information.A stolen passport, particularly in combination with other documents already in the wallet, provides enough information to open financial accounts, apply for government benefits, or commit more serious identity fraud than most card-based theft. If you are in a situation where you need to carry significant ID — travelling to a new medical provider, completing a legal transaction — bring only what is specifically required for that day.

#7 — Spare House or Car Keys

This item belongs on the list for a different reason than the others: it is not about financial fraud but about physical security. A wallet that contains a spare house key or car key does not just expose you to identity theft — it potentially tells a thief exactly where you live (via the address on your driver's license, loyalty cards, or any mail) and gives them a means to enter your home.The conventional advice to keep a spare key 'somewhere easy to find' — under a mat, in a wallet, in a magnetic box in the wheel arch — is exactly the same advice that experienced burglars know and rely on. Keep spare keys with a trusted family member, neighbour, or in a combination lockbox, never in your wallet.

#8 — Unused Gift Cards With Significant Balances

Gift cards are the payment method of choice for financial scammers — they are easy to liquidate remotely, often anonymous, and untraceable once redeemed. Carrying a high-balance gift card in your wallet exposes it to immediate, irrecoverable loss if the wallet is stolen. Unlike a credit or debit card, a gift card typically has no fraud protection mechanism: if it is stolen and the balance is spent before you report the loss, that money is almost certainly gone.Use gift cards promptly or store them securely at home until you are ready to use them. If you regularly receive gift cards and tend to save them, consider taking a photograph of the card number and redemption code before storing it — this allows you to use the balance online even if the physical card is lost or stolen, though the value should be treated as spent as soon as the card goes missing.

What a Sensible Wallet Actually Contains After 60

After removing the eight items above, a practical, genuinely secure everyday wallet typically contains:- A single primary credit or debit card (or one of each if you use both daily).

- Your driver's license or state-issued photo ID.

- Your health insurance card (private insurer only — not your Medicare card except on appointment days).

- A small amount of cash for everyday transactions.

- Emergency contact information on a small card — not listing account numbers but naming a trusted person to contact and their phone number.

If your wallet is lost or stolen, this reduced set is dramatically faster to cancel and replace, and it limits the information available to anyone who finds or takes it. The 10 minutes spent on a wallet audit today could save you 200 hours of fraud resolution later — the average time identity theft victims spend recovering from an incident, according to Snappt's 2026 identity fraud statistics.

Conclusion

Your wallet is not a filing cabinet. It is, ideally, a minimal daily-use tool containing only what you need for the day ahead — and nothing that would cause serious, lasting financial or personal damage if it were lost or stolen this afternoon. After 60, the stakes are higher than for most other age groups: older Americans carry more accumulated savings, have more to lose from Medicare and Social Security fraud, and tend to experience greater financial damage per incident than younger victims. The $7.7 billion in fraud losses reported by Americans over 60 in 2025 is not an abstract statistic — it reflects real, life-altering financial damage that often begins with a lost or stolen wallet.The eight items on this list are not rare or unusual things to find in an older American's wallet. They are common — so common that removing them may feel like going against the habits of a lifetime. But the reason they belong at home rather than in your pocket is straightforward and consistent: each one provides significantly more value to a criminal who steals your wallet than it provides to you as a daily carry item. Your Social Security number is already memorised. Your Medicare card is only needed at specific appointments. Your spare key belongs with a trusted person.

Spend ten minutes today doing the wallet audit this article describes. Remove what should not be there, put it securely away, and carry forward with the confidence that even the worst-case scenario of a lost wallet will be an inconvenience rather than a financial catastrophe.

Frequently Asked Questions (FAQ)

Is it really that risky to carry my Social Security card in my wallet?

Yes. The Social Security Administration explicitly advises against carrying your Social Security card with you. Your SSN is the single most useful piece of information a criminal needs to commit identity theft, apply for credit in your name, file a fraudulent tax return, or access government benefits. The physical card itself is almost never required at any appointment — healthcare providers, financial institutions, and government offices ask for the number, not the card. Memorise the number and leave the card in a locked location at home.What should I do if my wallet is lost or stolen?

Act quickly and systematically. Call your bank or card issuers to cancel every card in the wallet — even cards you did not think were at risk. File a report with your local police, both because some insurers require it and because it creates a documented timeline for any fraud that follows. Place a fraud alert or credit freeze with all three major credit bureaus (Equifax, Experian, TransUnion) — a freeze is free and prevents new accounts from being opened in your name. If your Medicare card was in the wallet, call 1-800-MEDICARE (1-800-633-4227) to report the potential compromise. If your Social Security card was included, report it to the Social Security Administration at ssa.gov/pass.I need my Medicare card for a doctor's appointment tomorrow. Should I carry it?

For specific appointments where your Medicare card is genuinely needed, it is fine to carry it for that day — the key is not making it a permanent wallet resident. A practical middle approach is to keep a photocopy of your Medicare card with the last four digits of your MBI obscured, which gives your provider enough information for routine verification while reducing the value of the card if it is lost. Alternatively, a secure, password-protected photo on your phone provides quick access without a physical card to lose.How do I remember my PINs and passwords without writing them down?

The best approach depends on your comfort with technology. A reputable password manager app (such as 1Password, Bitwarden, or the built-in options in iPhone and Android) stores and encrypts all your passwords behind a single master password. For those less comfortable with apps, a dedicated password notebook kept at home (not in the wallet) is far safer than notes in the wallet itself. For bank PINs specifically, choosing a number meaningful only to you — derived from a personal memory rather than a birthday or sequence — makes it easier to memorise and harder to guess.How often should I audit what is in my wallet?

Financial security experts generally recommend a wallet audit at least twice a year — perhaps when clocks change in spring and autumn as a memorable prompt — plus immediately after any significant life event such as a new card arriving, a change of address, or a situation where you were asked to show more documentation than usual. The audit itself takes less than ten minutes and should include checking not just what is in the wallet but whether the cards you are carrying are still active, whether their contact numbers are current, and whether anything has been added since the last check that does not need to be there.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. FBI Internet Crime Complaint Center (IC3) — 2025 Annual Report

https://www.ic3.gov/Media/PDF/AnnualReport/2025_IC3Report.pdf

2. Fox News / CyberGuy — Identity Theft Losses Surge 70% for Older Americans (April 2026)

https://cyberguy.com/scams/identity-theft-losses-surge-70-older-americans/

3. SeniorLiving.org — 2026 Statistics on Senior Identity Theft

https://www.seniorliving.org/identity-theft-protection/statistics/

4. Federal Trade Commission — IdentityTheft.gov: Report and Recover From Identity Theft

https://www.identitytheft.gov/

5. Social Security Administration — Protect Your Social Security Number

https://www.ssa.gov/fraud/

6. Medicare.gov — Protect Your Medicare Number

https://www.medicare.gov/basics/get-started-with-medicare/medicare-basics/protect-yourself-medicare-fraud

7. Annual Credit Report — Free Credit Reports from All Three Bureaus

https://www.annualcreditreport.com/

8. Snappt — Identity Fraud Statistics 2026

https://snappt.com/blog/identity-fraud-statistics/

0 Comments Comments