Finance

Bank of England Warns Rates Could Rise Amid Iran War

TABLE OF CONTENTS

- Background: From rate cuts to rate fears

- The Iran war and the energy shock

- The MPC decision: Hold — for now

- Three scenarios the Bank laid out

- What this means for mortgages and households

- The wider economic picture

- Conclusion

- Frequently asked questions

- References

Background: From rate cuts to rate fears

At the start of 2026, the Bank of England was on a gentle glide path towards easier monetary policy. Inflation, which had tormented British households for nearly four years, was finally behaving. The consumer price index stood at 3.4% in December 2025 — still above the 2% target, but falling steadily — and the Bank's own forecasts suggested it would reach that target by spring 2026.Expectations in financial markets mirrored that optimism. Investors were pricing in several rate cuts during 2026, bringing the Bank Rate down from 3.75% toward what many economists considered a more neutral level. Mortgage lenders were already adjusting fixed-rate deals accordingly, offering some relief to millions of homeowners facing remortgaging decisions.

Then, on 28 February 2026, the United States and Israel launched military strikes against Iran. The economic calm that had taken years to restore was shattered almost overnight.

The Iran war and the energy shock

Iran's response to the US-Israeli strikes was swift and strategically calculated. Tehran effectively closed the Strait of Hormuz, the narrow waterway through which approximately one-fifth of the world's crude oil and liquefied natural gas passes in peacetime. The disruption sent shockwaves through global energy markets that reverberated all the way to British petrol stations and household energy bills.Brent crude — the international oil benchmark — briefly surged above $126 a barrel during trading on 30 April 2026, the highest level since the aftermath of Russia's full-scale invasion of Ukraine in 2022. At its peak, crude oil cost $42 more per barrel than on the eve of the conflict, a 57% increase that exceeded even the oil price spike seen after Russia's invasion.

Ships have almost completely stopped moving through the Strait of Hormuz — a route through which about a fifth of the world's oil and liquefied natural gas passes.

— BANK OF ENGLAND, MAY 2026

The natural gas picture was less extreme than in 2022 — UK prices rose by 78 pence per therm in March 2026 before retreating, compared with a spike of more than 300 pence per therm after the Russian invasion — but the cumulative effect on UK consumers was still significant. Petrol prices climbed sharply at the pump, and household energy bills were expected to rise further in the second half of the year.

UK inflation, which had stood at 3.0% in February 2026 and was expected to fall to near the 2% target by April, instead climbed to 3.3% in March — driven largely by higher fuel costs — and was forecast to rise further still through the summer months.

The MPC decision: Hold — for now

Against this turbulent backdrop, the Bank of England's Monetary Policy Committee met on 30 April 2026 and faced a genuinely difficult dilemma. On the one hand, inflation was rising and energy prices were adding fresh pressure. On the other, the economy was slowing — GDP growth forecasts for 2026 had already been slashed by major forecasters to as low as 0.4% — and raising rates into a weakening economy risked tipping the country into recession.The committee voted 8-1 to hold Bank Rate at 3.75%, with Chief Economist Huw Pill — a known hawk — the sole dissenter calling for an immediate 25 basis-point increase to 4%. The decision aligned with what most economists had predicted, but the accompanying statement made clear that the Bank was watching the situation closely and stood ready to act.

Governor Andrew Bailey noted that the MPC's decision not to cut rates before the war had already proved to be fortunate. That caution, he said, gave the committee "a good deal of space" to absorb inflationary pressure before needing to consider rate increases. Around half of the members who voted to hold rates described themselves as placing most weight on a moderate scenario in which oil prices eventually ease.

The British pound rose 0.4% against the dollar immediately after the announcement, reaching $1.3473, suggesting markets found some relief in the measured tone — though gilt yields also fell as investors scaled back their bets on imminent rate hikes.

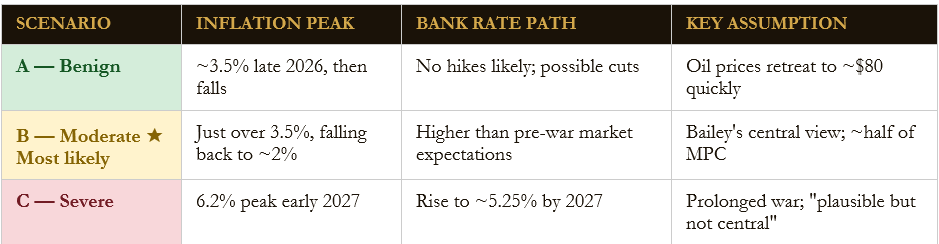

Three scenarios the Bank laid out

Rather than commit to a fixed path, the Bank of England published a highly unusual set of three economic scenarios reflecting the deep uncertainty around the conflict's duration and severity. Each was premised on different assumptions about how long oil prices would remain elevated and how far the effects would ripple through wages and business costs.

Deputy Governor Clare Lombardelli emphasised that the severe scenario was not the Bank's base case, but acknowledged it was "plausible and would require policy to respond more forcefully to inflationary pressures." She added that any rate hikes in that scenario would reduce the inflation peak but would "come at the cost of a larger output gap" — meaning more unemployment and lower growth.

The International Monetary Fund, assessing the same situation from Washington, predicted UK inflation would peak at 4% in the coming months — a more pessimistic near-term view than the Bank's own Scenario B, though still well short of the catastrophic Scenario C.

What this means for mortgages and households

For the millions of UK homeowners on variable-rate mortgages or facing upcoming fixed-rate renewals, the Bank's statement carries important implications. Although no rate increase was announced on 30 April, the clear message from Threadneedle Street is that cuts are off the table for the foreseeable future — and rises remain possible if inflation proves more stubborn than hoped.UK 10-year gilt yields rose by more than those of any other G7 country except Italy during March 2026, reflecting the UK's combination of sticky inflation and stretched public finances. This translated directly into higher mortgage rates: the yield rise pushed the cost of a typical first-time buyer refinancing in March up by roughly £100 a month compared with someone who had locked in a deal in February.

Energy costs add another layer of pressure. Economists estimate that a sustained period of elevated oil and gas prices could see British households collectively spending around £11 billion more on fuel and energy in 2026 than they would have if prices had stayed at early-year levels. While significant, this is less than half the household income impact of the 2021-22 energy shock — partly because the natural gas spike this time has been far smaller than in 2022.

The wider economic picture

The Iran war has not merely raised inflation — it has also knocked growth. Prior to the conflict, the Office for Budget Responsibility had forecast UK GDP growth of 1.1% in 2026. That figure has since been revised sharply downward by almost every major forecaster: Barclays and KPMG now expect 0.7% growth, Oxford Economics 0.4%, and Pantheon Macroeconomics 0.6%.The Bank of England finds itself in a situation economists sometimes describe as stagflationary — rising prices combined with slowing growth. Unlike demand-driven inflation, which can be tackled decisively with rate rises, supply-side inflation caused by an energy shock is harder to tame without inflicting significant pain on an already fragile economy.

The Resolution Foundation, a UK think tank, has argued that the Bank should resist the temptation to hike rates aggressively. In a research note published in April 2026, it suggested the situation is different from 2022, when the Bank was criticised for being slow to act. Today there is more slack in the economy, unemployment is higher, and the gas price shock is far smaller in relative terms.

The next MPC rate decision is scheduled for Thursday 18 June 2026. By then, the committee will have two more months of inflation data, a clearer picture of whether the fragile Middle East ceasefire is holding, and updated readings on wage growth — the so-called "second-round effects" that the Bank is most anxious to prevent taking hold.

CONCLUSION

The Bank of England finds itself navigating some of the most complex economic conditions since the COVID-19 pandemic. The Iran war has derailed what looked, at the start of 2026, like a straightforward path toward lower inflation and lower interest rates. Oil prices at four-year highs, a closing Strait of Hormuz, and surging pump prices have pushed UK inflation back up and forced the Monetary Policy Committee to shelve its rate-cutting plans indefinitely.For now, the Bank has chosen to wait and watch — a pragmatic response to genuine uncertainty about how long the conflict and its economic consequences will last. But the door to rate rises is firmly open, and in the most severe scenario modelled by the Bank, rates could climb as high as 5.25% by 2027. The decisions made at Threadneedle Street over the coming months will shape the finances of millions of UK households and businesses for years to come.

0 Comments Comments