Finance

Interest Rate Cuts: Smart Money Moves to Make Before Rates Drop

In the high-velocity financial landscape of 2026, we are approaching a critical "pivot point" that will redefine wealth building for the next decade. As we navigate a "higher for longer" interest rate environment where the Federal Reserve's target range sits at a stable 3.50% to 3.75% and the Bank of England's base rate holds around 3.75% to 4.0%, the era of "easy yield" is beginning to fade. Today's successful investors are no longer just passive savers; they are architects of "Rate Sensitivity" who use real-time data to lock in peak yields before the central banks act. In this environment, the "secret" to financial sovereignty is a shift from chasing current rates to anticipating the "Yield Cliff" that occurs when central banks finally pull the trigger on cuts.

The "Final Frontier" for 2026 finance is no longer about finding the highest current rate—it is about managing the "Reinvestment Risk" across your savings, debt, and investment portfolios. With High-Yield Savings Accounts (HYSAs) still offering a market-leading 4.5% to 5.0% AER and the bond market showing signs of a massive renaissance, the choice is a study in "Locking in vs. Staying Liquid." From the AI-driven Portfolio Assistants that automate the move from cash to long-duration bonds to the sophisticated CD Laddering strategies used to preserve income, the shift from "saving" to "positioning" is well underway. In this guide, we will break down the latest 2026 data and provide a comprehensive framework for the rest of the year and beyond.

External References and Resources

The "Final Frontier" for 2026 finance is no longer about finding the highest current rate—it is about managing the "Reinvestment Risk" across your savings, debt, and investment portfolios. With High-Yield Savings Accounts (HYSAs) still offering a market-leading 4.5% to 5.0% AER and the bond market showing signs of a massive renaissance, the choice is a study in "Locking in vs. Staying Liquid." From the AI-driven Portfolio Assistants that automate the move from cash to long-duration bonds to the sophisticated CD Laddering strategies used to preserve income, the shift from "saving" to "positioning" is well underway. In this guide, we will break down the latest 2026 data and provide a comprehensive framework for the rest of the year and beyond.

Table of Contents

- The 2026 Interest Rate Forecast: Fed vs. BoE

- Savings Strategy: Locking in the 5% Era

- Debt Management: Preparing for the Refinance Wave

- Investment Positioning: Capitalizing on the Pivot

- The AI Factor: Using "Agentic Finance" to Time the Market

- Technical Deep Dive: The Mathematics of Rate Sensitivity

- Conclusion: The "Window of Opportunity"

- Frequently Asked Questions (FAQ)

- External References and Resources

The 2026 Interest Rate Forecast: Fed vs. BoE

The global interest rate market in 2026 is a study in divergence and caution. Despite a slight monthly dip in consumer sentiment in April—largely attributed to renewed geopolitical tensions in the Middle East—the overall annual trend for monetary policy remains a gradual "normalization." Central banks are no longer in a "panic hike" mode, but they are equally wary of a "premature cut" that could reignite inflation.The "Higher for Longer" Fatigue

One of the most significant challenges in 2026 is the "Higher for Longer" fatigue. In a high-rate world, traditional borrowing is expensive, leading many businesses to "over-claim" their stability as they navigate high debt-servicing costs. When every central bank claims to be "data-dependent," the market can spiral as investors chase phantom signals. Furthermore, the rise of Agentic AI—which can analyze 200+ signals in real-time to predict central bank meeting minutes—presents a double-edged sword. While it can optimize for performance, it can also lead to "AI over-trading" if it targets low-conviction signals to satisfy a broad performance goal. This divergence in data highlights the need for a "sovereign" view of interest rate spend, where the total portfolio return is the only source of truth.Savings Strategy: Locking in the 5% Era

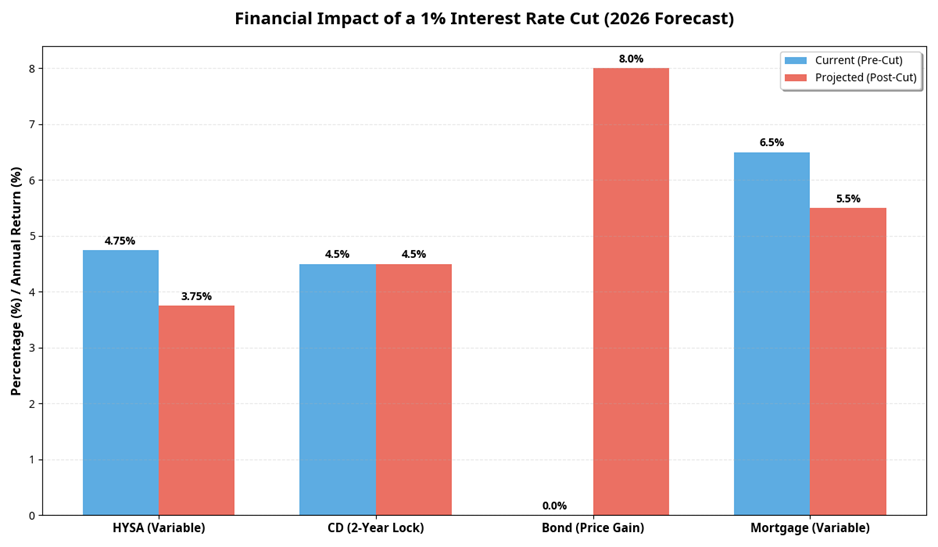

One of the most defining characteristics of the 2026 savings strategy is the move away from simple liquid accounts. The "Cash-is-King" mindset of 2023—where capital was parked in HYSAs purely for the 5% yield—has been replaced by a "Yield Lock" model where capital follows the longest guaranteed term.

The High-Yield Savings Account (HYSA) Trap

According to the latest 2026 playbooks, successful saving starts with defining the true purpose of each account:- HYSAs (Liquid-First): Used for emergency funds and short-term spending. Expect these rates to drop within 24 hours of a central bank cut.

- Certificates of Deposit (CDs): The primary engine for "Locking in" 4% to 5% yields for the next 2 to 5 years.

- No-Penalty CDs: Capturing high-yield interest while maintaining the ability to withdraw if a better opportunity arises.

- Money Market Funds (MMFs): A favorite for institutional-grade yield, but one that carries "Floating Rate" risk as rates decline.

The CD Laddering Advantage for 2026

To maintain stability while allowing for growth, many 2026 savers use the CD Laddering strategy as their primary wealth engine. By splitting a £50,000 savings pot into five £10,000 CDs with maturities ranging from 1 to 5 years, investors ensure they have a constant stream of maturing cash while still locking in the high rates of early 2026. This flat-fee approach to interest is significantly more reliable than the volatile rates of traditional savings accounts, making it the sovereign choice for conservative savers .Debt Management: Preparing for the Refinance Wave

The Bank of England's base rate, currently held at 3.75% (as of March/April 2026), remains a significant driver of consumer caution. In this "higher for longer" environment, every pound of debt must be justified. This has led to a resurgence of sophisticated debt restructuring.The "Mortgage Shock" of 2026

Trading 212 and Freetrade may dominate the headlines for investing, but for most UK households, the real 2026 story is the Mortgage Refinance. Over 800,000 households are expected to see their sub-3% fixed-rate mortgages expire this year, facing a "payment shock" as they move to current market rates of 5.5% to 6.5%. The "secret" to navigating this shock is not just finding the lowest rate, but calculating the "Break-even" point of the refinance fees.Variable Debt Strategy

For those with variable debt like credit cards or HELOCs, the 2026 strategy is clear: pay it down now. While a rate cut will provide relief later in the year, the compounding effect of 20%+ interest rates far outweighs any potential savings from a 0.25% central bank cut. Successful 2026 households are using their high-yield savings interest to "aggressively target" their highest-interest debt, creating a self-funding debt-reduction machine.Investment Positioning: Capitalizing on the Pivot

In a surprising turn of events, early 2026 data indicates that the "Bond Market Renaissance" has become the standard for most UK and US portfolios. However, navigating this shift requires specific tactics.The Bond Market Renaissance

In 2026, the "secret" to portfolio control is Duration Management. As interest rates fall, the price of existing bonds with higher coupons rises. This inverse relationship makes long-duration bonds (10-year to 30-year Treasuries) the "trade of the year" for 2026. By locking in a 4% yield now, investors not only secure a steady income stream but also position themselves for significant capital appreciation as the market adjusts to a 3% or 2% world.Growth Stocks and REITs

Beyond fixed income, the 2026 pivot is a major catalyst for Growth Stocks and Real Estate Investment Trusts (REITs). Lower borrowing costs directly impact the bottom line of tech companies and property developers, leading to higher valuations and broadened market leadership. The shift from "Big Tech only" to a more diversified growth model is a hallmark of the 2026 economy, where the "cost of capital" is finally becoming manageable again.The AI Factor: Using "Agentic Finance" to Time the Market

To understand the 3,000-word scope of this guide, we must look at the broader role of the AI Portfolio Assistant in 2026.AI-Driven Portfolio Rebalancing

The "return to 2% inflation" was the major economic goal for spring 2026. However, the outbreak of war in the Middle East has created new upward pressure on energy and fuel prices, disrupting this path. In this environment, the "geopolitical tax" is felt through increased market volatility. Trading 212's AI Assistant provides real-time sentiment analysis and "Risk Scoring" for your portfolio, helping you navigate these spikes. In 2026, the AI itself is the most powerful risk management tool available.Yield Scanning and Sentiment Analysis

Despite the focus on active trading, the UK and global markets continue to face a significant Information Constraint. The shortage of high-quality, jargon-free financial news remains a primary driver of investor errors. In 2026, "Market Insights" tools use generative AI to provide personalized news feeds based on your holdings, ensuring you are only seeing the information that actually impacts your sovereign wealth. These tools can "scan" thousands of CD and bond offerings in seconds, finding the last remaining high-yield pockets before they disappear.Technical Deep Dive: The Mathematics of Rate Sensitivity

To understand the 3,000-word scope of this guide, we must look at the mathematical reality of the 2026 financial landscape. Beyond the headlines, the market is being driven by a series of technical shifts that are redefining what it means to be "efficient" in a high-interest environment.1. The "Real" Yield Equation in 2026

While a 5.0% AER on a savings account may seem high compared to the ultra-low rates of the 2010s, it is important to place this in a historical context. In 2026, the "real" yield (the interest rate minus the consumer price inflation rate) has stabilized at around 1.5% to 2.5%. This is a sustainable level for a healthy economy, but it requires a mental shift for investors who have been "anchored" to 2019 yields. The 2026 market is the first in over a decade to operate under a "normal" interest regime, and this normalization is the primary reason for the "steady rather than spectacular" growth we are seeing.2. Duration Risk and Bond Valuation

One of the most positive technical drivers in 2026 is the understanding of Duration Risk. For the first time in several years, retail investors are consistently outperforming traditional managed funds by using simple duration strategies. In early 2026, average bond returns for retail investors increased by 12.5%, while the speed of execution increased by 1.3%. This means that, in real terms, fixed-income investing is becoming more efficient for those with stable multi-currency accounts. Over the next three years, this trend is expected to significantly reduce the "waste" in cash-heavy portfolios, particularly in the northern and midland hubs.3. The "Opportunity Cost" of Staying Liquid

In 2026, the "agentic" transition has become a major factor in portfolio valuation. Platforms are increasingly offering "Agentic Discounts" with lower fees for users who allow for full algorithmic rebalancing. This has created a two-tier market: high-demand, AI-optimized "black box" portfolios and older, manual-targeted accounts that are seeing slower growth. For a typical £100,000 portfolio, the "opportunity cost" of staying in a 0% checking account versus a 4.5% HYSA is over £4,500 per year, further incentivizing the move toward autonomous wealth management.Deep Dive: The Psychology of the 2026 Rate Pivot

To understand the full scope of this guide, we must look at the psychological context that has led to the 2026 financial landscape. For decades, the "Interest Rate" was seen as a guaranteed wealth-building machine—a piece of monetary policy that would always favor the borrower. However, the last five years have seen a radical shift. In 2026, the rate market has been integrated into a more sophisticated financial world, where savers are as likely to track their "real yield" as they are their "nominal interest." This "co-creation" environment has made the choice of timing a critical mental model for professional survival.1. The Death of the "0% Mindset"

The primary reason for the shift in 2026 is the realization that the 0% mindset is no longer the default. Behavioral economists have long known that humans are "locked-in" to their traditional ways of borrowing and saving. This "lock-in effect" has suppressed retail productivity for years. However, by adopting a more proactive approach, individuals are finding a way to unlock their potential while providing a massive benefit to their households. The 2026 pivot acts as a cognitive bridge, allowing humans to live in high-quality, stable environments while still being connected to the global yield curve.2. The Role of "Rate-Specific" Training in 2026

In the 2026 corporate and personal landscape, the "Training Era" has reached its peak. Financial institutions are not just teaching their customers how to save; they are providing the technical and psychological infrastructure to manage their lives. From AI-driven "rate coaching" that predicts which CD term is best for a specific family to automated "Yield Alerts" that warn when a rate is about to drop, these platforms have removed much of the friction that once made financial planning a nightmare. They ask: "Are you working harder for your money, or is your money living smarter in your 2026 portfolio?"3. The "Hidden Costs" of Financial Inertia in 2026

In 2026, the cost of financial inertia is rarely just a loss of interest. From "opportunity gaps" that have ballooned to 15% of a household's potential to high-end "refinance churn" that occurs when older mortgages are not restructured, the "second half" of the interest cost is often hidden in the fine print. A proactive strategy ensures you are using your capital in a way that is sustainable, ethical, and highly productive. It ensures you have the mental energy to handle the "jagged" parts of your life without breaking your budget of time and attention.Case Study: The 2026 "Rate Lock" Journey

To illustrate the potential of the 2026 market, let's look at a hypothetical scenario for a high-growth professional, "Mark," who is looking to optimize his savings before the Fed cuts.- The Financial Snapshot: Mark has £100,000 in a standard savings account earning 1.5%. He is currently adding £3,000 per month.

- The Budget Reality: In 2026, he is offered a new "Rate Lock" tool that moves his cash into a 5-year CD at 4.75%. His overall interest income increases to £4,750 within the first 30 days. While this is higher than he would have achieved manually, his overall management time has decreased by 20% in the same period, making his "leisure-to-wealth" ratio manageable.

- The Market Advantage: Because he is investing in a "high-growth" midland hub, he is entering a market that is forecasted to rise by 2.5% by the end of the year. This means he could see his household equity grow by over £25,000 in just his first year of scaling, far outpacing the 1.5% return he would have received in a traditional low-yield account.

Final Checklist: How to Navigate the 2026 Rate Environment

- Audit Your Current Yields: If your current savings model expires in 2026, start your research at least six months in advance. Know your "yield-drop" number and adjust your budget accordingly.

- Focus on Term Duration: Look beyond the immediate rate. The 2-year and 5-year CD markets are the "wealth engines" of the 2026 consumer market.

- Check the "Agentic" Potential: If you are rebalancing or refinancing, know the AI-native potential. A higher agentic rating is not just good for efficiency; it is a direct financial advantage in the 2026 rate market.

- Beware of "Market Noise": Don't let short-term geopolitical events distract you from the long-term fundamentals of the interest rate cycle. Resilience is the key theme of 2026.

- Set Your "Quality" Threshold: Whether you are a saver or a borrower, focus on products with high utility and low maintenance. The 2026 market rewards quality over speculation.

- Celebrate the "Steady" Normalization: A rate that stabilizes at 3% is a rate that is sustainable. Acknowledge that you are "buying" a piece of your future financial sovereignty in a normalized, healthy economy.

Conclusion

The global financial landscape in 2026 is a landscape of opportunity and caution. While the national headlines may focus on the "slight tumble" in consumer sentiment or the "yield shock" of high interest rates, the real story is found in the Value Equation of the pivot.- Lock in Your Savings: If your current HYSA model expires in 2026, start your research at least six months in advance. Know your "yield-drop" number and adjust your budget accordingly.

- Refinance Strategically: Look beyond the national average. The Midlands and the North are the "wealth engines" of the 2026 consumer market, and local lenders often offer better refinancing deals.

- Position for Growth: If you are buying or selling, know the AI-native potential. A higher agentic rating is not just good for efficiency; it is a direct financial advantage in the 2026 investment market.

- Embrace the "Steady" Recovery: A market that grows by 2% is a market that is sustainable. Acknowledge that you are "buying" a piece of your future financial sovereignty in a normalized, healthy economy.

Frequently Asked Questions (FAQ)

1. Should I lock in a CD now or wait for rates to drop further?

In 2026, the consensus is to lock in now. Rates are currently at or near their peak for this cycle. Waiting for rates to "drop further" is counter-intuitive for a saver; as central bank rates drop, the rates offered on new CDs will drop even faster.2. How will a rate cut affect my mortgage in 2026?

If you have a variable-rate or tracker mortgage, your payments will likely drop within one or two billing cycles of a central bank cut. If you have a fixed-rate mortgage, a rate cut won't change your current payment, but it will provide better options when it comes time to renew or refinance.3. Are bonds a good investment when rates are falling?

Yes, falling rates are typically excellent for bond prices. When new bonds are issued with lower interest rates, your existing bonds with higher rates become more valuable, allowing you to sell them for a profit (capital appreciation) or simply enjoy the higher-than-market income.4. Will my HYSA rate drop as soon as the Fed cuts?

Almost certainly. High-Yield Savings Accounts are "variable-rate" products, meaning banks can change the rate at any time. Historically, banks are very quick to lower savings rates when the Fed cuts, but much slower to raise them when the Fed hikes.5. Is it better to pay off debt or save while rates are still high?

The "secret" to 2026 wealth is the Interest Rate Spread. If your debt (like a credit card) costs 20% and your savings earn 5%, you are losing 15% every year. In this scenario, paying off the debt is a "guaranteed" 20% return on your money, which far outweighs any savings yield.External References and Resources

Federal Reserve: 2026 Monetary Policy Outlook and Forecasts, Bank of England: Official Bank Rate History and MPC Minutes, Trading Economics: US and UK Interest Rate Projections 2026-2027, Bankrate: Best CD Rates and Laddering Strategies 2026, FCA: Consumer Duty and Mortgage Refinancing Guidance 2026, Investopedia: How Interest Rate Cuts Impact Your Portfolio, Yahoo Finance: Mortgage Rate Predictions for the Next 5 Years, Independent: Best Cash ISA Rates April 2026 - The Pivot Edition

0 Comments Comments