Investing

Best 3 ETF Portfolio to Build Wealth in 2026: UK Complete Guide

You do not need dozens of funds, a stockbroker, or a finance degree to build genuine long-term wealth through investing. Three carefully chosen ETFs — a global equity fund, a US equity fund, and a bond fund — held inside an ISA or SIPP and funded consistently over time can do more for your financial future than most complex strategies. This guide explains exactly why VWRP, VUSA, and VGOV work, how to allocate between them at different life stages, and how to get started.

A three-ETF portfolio — one global equity fund, one US equity fund for additional growth exposure, and one bond fund for stability — gives a UK investor access to over 4,100 different stocks and bonds across every major economy in the world, at a blended annual cost of approximately 0.10% to 0.19%. That is less than twenty pence per year for every hundred pounds invested, compared with the 1% to 1.5% typical of actively managed funds. This cost difference compounds dramatically over time: at 1.25% annual cost on a £100,000 portfolio growing at 8% per year, you pay approximately £62,000 more in fees over 30 years than you would at 0.15% annual cost. That £62,000 does not disappear — it comes directly out of your retirement pot.

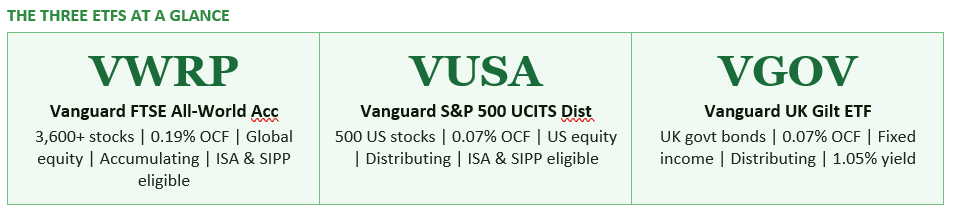

The three ETFs covered in this guide — VWRP (Vanguard FTSE All-World, accumulating), VUSA (Vanguard S&P 500 UCITS, distributing), and VGOV (Vanguard UK Gilt) — are among the most popular and most widely recommended ETFs for UK investors in 2026, according to InvestEngine's 'most bought by number of clients' rankings for February 2025 to February 2026. They are UCITS-compliant (legally appropriate for UK investors), available on major UK platforms including InvestEngine, Trading 212, Hargreaves Lansdown, and AJ Bell, and can be held inside a Stocks and Shares ISA or a SIPP for maximum tax efficiency.

S&P Global's SPIVA reports, published annually, track the percentage of actively managed funds that outperform their benchmark index after fees over rolling periods. The consistent finding, across every market and every time period, is that the majority of active funds underperform their benchmark after costs. Over 15 years, approximately 90% of active US equity funds fail to match the S&P 500 index return. Over 20 years, the figure is higher still. The intuition is straightforward: an active fund must generate enough outperformance from its investment decisions to cover its fees (typically 0.75% to 1.5% per year) and still outperform the index. Very few fund managers do this consistently over long periods.

ETFs tracking market indices sidestep this problem entirely. They do not attempt to beat the market — they own the market. By holding every stock in a given index in proportion to its market capitalisation, an index ETF captures the return of the entire market minus a very small management fee. No picking the wrong stocks, no manager style drift, no star manager leaving for a rival, no excessive trading costs. The returns are predictable in structure, if not in magnitude: you get whatever the market delivers, minus a rounding error of costs.

The S&P 500 has an excellent track record of delivering returns for investors. Over the last 50 years, the average stock market return, as measured by the S&P 500, has been 8% with dividends reinvested. The Vanguard S&P 500 ETF is a low-cost way to capture the market's returns.

— THE MOTLEY FOOL — 7 BEST ETFS TO BUY IN MAY 2026

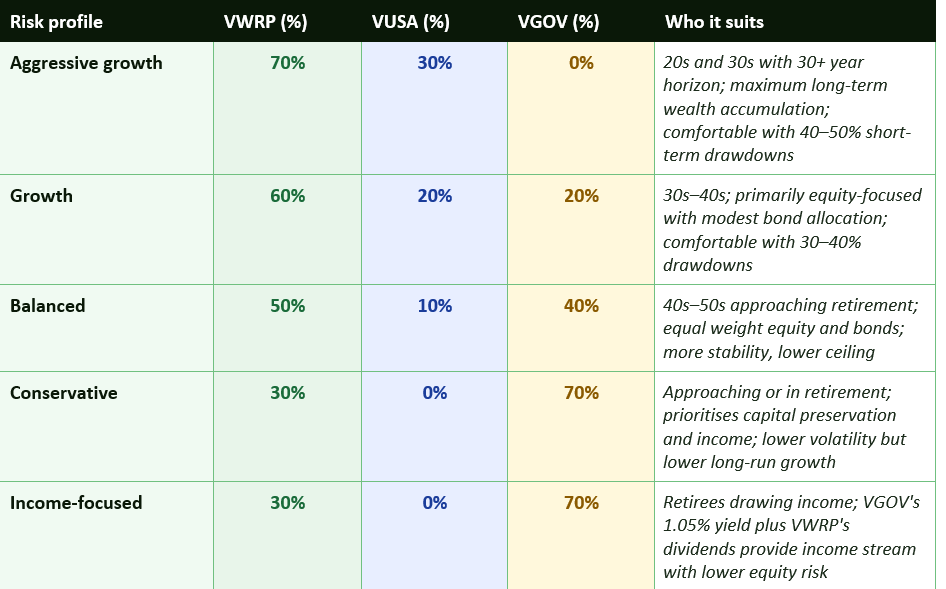

The three building blocks serve distinct roles. A global equity fund provides broad exposure to stock markets worldwide — the long-run engine of wealth creation, with higher expected returns than bonds but greater short-term volatility. A US equity fund provides concentrated exposure to the world's largest and most dynamic economy, historically the highest-returning major equity market and the engine of much of VWRP's own performance (since US stocks constitute approximately 65% of VWRP). A bond fund provides stability and a counterweight to equity volatility — bonds typically hold their value or rise when equities fall sharply, providing a buffer during market downturns and generating income in the interim.

The specific allocation between these three building blocks — how much to hold in global equity, how much in US equity, and how much in bonds — determines the risk-return profile of the portfolio. The allocation is not fixed; it should change over time as an investor's time horizon shortens and their capacity to absorb short-term losses decreases. We cover the allocation framework in Section 7.

VWRP is widely considered the best single ETF for UK investors seeking straightforward, long-term, globally diversified investment. The fund tracks the FTSE All-World Index, providing exposure to over 3,600 large and mid-cap companies across both developed and emerging markets — covering approximately 98% of the investable global stock market. Countries represented include the US (approximately 65%), UK, Japan, France, Germany, China, India, and dozens more. Sectors span technology, healthcare, financials, consumer goods, energy, and industrials. The accumulating structure automatically reinvests dividends within the fund, compounding growth without any action required from the investor. For UK investors, VWRP is domiciled in Ireland (making it UCITS-compliant and legally appropriate for UK residents), trades on the London Stock Exchange in GBP, and can be held in a Stocks and Shares ISA, SIPP, or general investment account.

✓ Why it works: Truly global diversification in a single fund at minimal cost. The accumulating structure compounds automatically — ideal for long-term ISA and SIPP holders. Covers both developed and emerging markets. Motley Fool UK rates it as 'hard to beat' for a core portfolio holding.

⚠ Watch out for: US concentration risk: approximately 65% of the fund is in US equities, so VWRP is not as geographically balanced as its 'all-world' name implies. The Magnificent Seven technology stocks (Apple, Microsoft, Nvidia, Alphabet, Meta, Amazon, Tesla) make up approximately 35% of the US market and therefore a very significant portion of VWRP. Tech sector volatility can therefore have an outsized impact.

VUSA tracks the S&P 500 — the index of the 500 largest publicly listed US companies by market capitalisation — at a tiny 0.07% annual cost. It is the most popular single-country ETF among UK investors, according to SmartInvestorUK's 2026 analysis, and for good reason. The S&P 500 has delivered an average annual return of approximately 10.26% since 1957, according to IG research published in December 2024. It has finished in positive territory in the great majority of years since 1871. The fund is physically replicated — it actually holds all 500 stocks — and tracks the index closely. VUSA is a distributing ETF, meaning it pays dividends into your account quarterly in USD rather than reinvesting them. This is worth knowing: if you want automatic reinvestment, the accumulating version (VUAG) is available on most platforms. VUSA trades on the London Stock Exchange in GBP, eliminating the FX conversion fees that would apply when buying US-listed ETFs such as VOO or SPY directly.

✓ Why it works: The S&P 500's long-term return record is the strongest of any major equity market. At 0.07% OCF it is one of the cheapest ETFs available. Buying in GBP avoids FX fees. VUSA adds a deliberate US tilt for investors who want to weight their portfolio toward the world's most dynamic economy — which already drives a significant portion of VWRP's returns.

⚠ Watch out for: Currency risk: VUSA holds US-dollar assets in a GBP-denominated wrapper. If sterling strengthens against the dollar, your GBP return will be lower than the USD return of the underlying stocks. Concentration in US mega-cap technology: the top 10 holdings make up approximately 38% of the index. As Motley Fool UK notes, 'in early 2026, the top 10 stocks in the index made up almost 40% of the S&P 500.' Combining VUSA with VWRP increases rather than decreases your US exposure.

VGOV tracks the Bloomberg UK Gilt Float Adjusted Index, providing exposure to UK government bonds — loans made to the UK government in exchange for regular interest payments and the return of capital at maturity. With a Total Expense Ratio of just 0.07%, VGOV is one of the cheapest ways to add fixed income to a UK portfolio. The fund pays a dividend yield of approximately 1.05% as of InvestEngine data, distributed to investors as income. UK gilts are considered one of the safest asset classes available to UK investors: the UK government has never defaulted on its bonds, and gilts are priced in sterling — eliminating currency risk for UK investors. In portfolio construction terms, gilts serve as a counterweight to equity volatility. During periods of equity market stress, investors typically move into government bonds, pushing gilt prices up. This negative correlation with equities (in most but not all market conditions) means a portfolio with a gilt allocation typically experiences lower peak-to-trough drawdowns during market crashes than a pure equity portfolio.

✓ Why it works: The lowest-risk component of the three-fund portfolio. Zero default risk for UK investors, zero currency risk. Provides income via the 1.05% yield. Acts as a portfolio stabiliser during equity market downturns, reducing peak-to-trough losses. At 0.07% OCF it is extremely cost-efficient for bond exposure.

⚠ Watch out for: Lower long-term returns than equities: gilts have historically returned approximately 3% to 4% per year over the long run — significantly below the equity risk premium. Rising interest rates reduce gilt prices (there is an inverse relationship between interest rates and bond prices). In 2022, UK gilts experienced significant losses as the Bank of England raised rates sharply. Younger investors with very long time horizons often hold little or no bonds, since they have time to ride out equity market volatility.

A note on combining VWRP and VUSA: because US stocks already make up approximately 65% of VWRP, adding VUSA alongside it further concentrates your portfolio in the US market. For an 'aggressive growth' allocation of 70% VWRP plus 30% VUSA, your effective US equity exposure is approximately 75% to 80% of the total equity portion. This is a deliberate bet on continued US outperformance — which has been well-rewarded historically but is not guaranteed. Investors wanting less US concentration might substitute a portion of VUSA for an emerging markets ETF such as VFEG (Vanguard FTSE Emerging Markets, 0.22% OCF) to increase geographic diversification.

The table makes two things clear. First, time is more powerful than the amount invested. The difference between starting at 25 and starting at 35, both investing £200 per month at 8% annual return, is approximately £136,500 by age 65. Second, even modest monthly amounts produce substantial long-run outcomes when held consistently. Someone investing £200 per month from age 30 to 60 accumulates approximately £272,900 — having contributed only £72,000 in total. The remaining £200,900 is pure compound growth.

This is why 'staying invested' is the single most important investment behaviour — more important than which specific ETFs you choose, which platform you use, or whether you time your investments optimally. The investors who build significant wealth through index ETFs are almost always distinguished not by investment sophistication but by starting early, investing consistently, and not panic-selling during market downturns.

Factor investing — tilting a portfolio toward small-cap, value, or quality stocks that have historically outperformed the broad market — has academic support and can add value for investors who understand it and maintain the discipline to hold through periods of factor underperformance. But the key word is discipline: many investors who add factor tilts to their portfolio abandon them when the factor underperforms for two or three years, capturing neither the factor premium nor the market premium.

Thematic investing — concentrating in AI, clean energy, semiconductor, or other themed ETFs — has produced spectacular short-term returns in some cases and equally spectacular losses in others. The performance of themed ETFs is highly dependent on timing, and the evidence that retail investors can reliably identify winning themes in advance is weak. The investors who bought an AI-focused ETF in early 2023 did well; those who bought a clean energy ETF in 2021 at peak valuations did not.

For most investors — particularly those with fewer than ten years of experience, those without the time to research factors and themes rigorously, and those who know from experience that they are vulnerable to panic-selling during drawdowns — the three-fund portfolio is not a compromise or a starting position. It is the best strategy available. Its simplicity is not a weakness — it is the mechanism by which investors actually implement it and maintain it through the market cycles that defeat more complex approaches.

The strategy will not be exciting. It will not have a chart that goes straight up every year. It will require you to keep investing through market crashes, geopolitical scares, and periods when something else looks far more attractive. But the evidence is overwhelming that this discipline — applied consistently over long periods at low cost — produces outcomes that the vast majority of more complex strategies fail to match. The three ETFs in this guide are not the only way to build long-term wealth through passive investing. But they are among the simplest, cheapest, and most proven approaches available to UK investors in 2026.

⚠ Important: This article is for educational purposes only and does not constitute financial advice. Investing involves risk; the value of investments can fall as well as rise and you may get back less than you invest. Past performance is not a reliable indicator of future returns. Always conduct your own research or consult a qualified financial adviser before making investment decisions.

SmartInvestorUK — Best ETFs UK 2026: Global, VWRL vs SWDA, ISA Picks https://smartinvestoruk.co.uk/best-etfs-uk/

ShareInvestingUK — Best ETF Strategy Guide: Vanguard vs iShares UK 2026 https://shareinvestinguk.com/top-etfs-for-uk-investors/

Financial Interest — The Best Vanguard Funds for UK Investors in 2026 (VWRP, VUSA, VGOV) https://financialinterest.com/best-vanguard-funds/

InvestEngine — Top Vanguard ETFs for UK Investors 2026 (VWRP, VUSA, VGOV) https://blog.investengine.com/top-vanguard-etfs-top-funds-for-investors/

VWRP.co.uk — Vanguard FTSE All-World UCITS ETF Analysis 2026 https://vwrp.co.uk/

JustETF UK — Best Bond ETFs 2026 (VGOV and alternatives) https://www.justetf.com/uk/market-overview/the-best-bond-etfs.html

The Motley Fool US — Best S&P 500 ETFs to Buy in 2026 (VUSA/VOO comparison) https://www.fool.com/investing/stock-market/indexes/sp-500/etfs/

Vanguard UK — VWRP ETF Product Page https://www.vanguard.co.uk/professional/product/etf/equity/9679/ftse-all-world-ucits-etf-usd-accumulating

MoneyHelper — Beginners' Guide to Investing and ISAs https://www.moneyhelper.org.uk/en/savings/investing

TABLE OF CONTENTS

- Why Three ETFs Is All You Need

- Why ETFs Beat Most Actively Managed Funds

- The Three-Fund Philosophy Explained

- ETF 1: VWRP — Vanguard FTSE All-World (Your Global Core)

- ETF 2: VUSA — Vanguard S&P 500 UCITS (Your US Growth Engine)

- ETF 3: VGOV — Vanguard UK Gilt ETF (Your Stability Layer)

- How to Allocate Between the Three ETFs

- The Power of Compounding: What Regular Investing Really Does

- Where to Buy: ISA, SIPP, and Platform Comparison

- Common Mistakes That Kill Long-Term Returns

- The Three-ETF Portfolio vs More Complex Strategies

- Conclusion

- Frequently Asked Questions

- References

Why Three ETFs Is All You Need

The personal investing industry has a powerful incentive to make portfolio construction seem complicated. Complicated portfolios require advisers, platforms, fund switches, and ongoing management — all of which generate fees. But the research on what actually produces superior long-term investment outcomes is remarkably consistent: low costs, broad diversification, and consistent long-term investment beat complexity in the vast majority of cases.A three-ETF portfolio — one global equity fund, one US equity fund for additional growth exposure, and one bond fund for stability — gives a UK investor access to over 4,100 different stocks and bonds across every major economy in the world, at a blended annual cost of approximately 0.10% to 0.19%. That is less than twenty pence per year for every hundred pounds invested, compared with the 1% to 1.5% typical of actively managed funds. This cost difference compounds dramatically over time: at 1.25% annual cost on a £100,000 portfolio growing at 8% per year, you pay approximately £62,000 more in fees over 30 years than you would at 0.15% annual cost. That £62,000 does not disappear — it comes directly out of your retirement pot.

The three ETFs covered in this guide — VWRP (Vanguard FTSE All-World, accumulating), VUSA (Vanguard S&P 500 UCITS, distributing), and VGOV (Vanguard UK Gilt) — are among the most popular and most widely recommended ETFs for UK investors in 2026, according to InvestEngine's 'most bought by number of clients' rankings for February 2025 to February 2026. They are UCITS-compliant (legally appropriate for UK investors), available on major UK platforms including InvestEngine, Trading 212, Hargreaves Lansdown, and AJ Bell, and can be held inside a Stocks and Shares ISA or a SIPP for maximum tax efficiency.

Why ETFs Beat Most Actively Managed Funds

Before building the portfolio, it is worth understanding why passive ETFs are the right starting point for most investors — because the evidence is overwhelming and consistently misrepresented by the active fund management industry.S&P Global's SPIVA reports, published annually, track the percentage of actively managed funds that outperform their benchmark index after fees over rolling periods. The consistent finding, across every market and every time period, is that the majority of active funds underperform their benchmark after costs. Over 15 years, approximately 90% of active US equity funds fail to match the S&P 500 index return. Over 20 years, the figure is higher still. The intuition is straightforward: an active fund must generate enough outperformance from its investment decisions to cover its fees (typically 0.75% to 1.5% per year) and still outperform the index. Very few fund managers do this consistently over long periods.

ETFs tracking market indices sidestep this problem entirely. They do not attempt to beat the market — they own the market. By holding every stock in a given index in proportion to its market capitalisation, an index ETF captures the return of the entire market minus a very small management fee. No picking the wrong stocks, no manager style drift, no star manager leaving for a rival, no excessive trading costs. The returns are predictable in structure, if not in magnitude: you get whatever the market delivers, minus a rounding error of costs.

The S&P 500 has an excellent track record of delivering returns for investors. Over the last 50 years, the average stock market return, as measured by the S&P 500, has been 8% with dividends reinvested. The Vanguard S&P 500 ETF is a low-cost way to capture the market's returns.

— THE MOTLEY FOOL — 7 BEST ETFS TO BUY IN MAY 2026

The Three-Fund Philosophy Explained

The three-fund portfolio concept — popularised by Jack Bogle, founder of Vanguard, and widely adopted in the UK investing community — is built on a single insight: most of the risk-adjusted return available in global financial markets can be captured with three holdings that are broadly diversified, low cost, and held patiently over the long term.The three building blocks serve distinct roles. A global equity fund provides broad exposure to stock markets worldwide — the long-run engine of wealth creation, with higher expected returns than bonds but greater short-term volatility. A US equity fund provides concentrated exposure to the world's largest and most dynamic economy, historically the highest-returning major equity market and the engine of much of VWRP's own performance (since US stocks constitute approximately 65% of VWRP). A bond fund provides stability and a counterweight to equity volatility — bonds typically hold their value or rise when equities fall sharply, providing a buffer during market downturns and generating income in the interim.

The specific allocation between these three building blocks — how much to hold in global equity, how much in US equity, and how much in bonds — determines the risk-return profile of the portfolio. The allocation is not fixed; it should change over time as an investor's time horizon shortens and their capacity to absorb short-term losses decreases. We cover the allocation framework in Section 7.

ETF 1: VWRP — Vanguard FTSE All-World (Your Global Core)

VWRP is widely considered the best single ETF for UK investors seeking straightforward, long-term, globally diversified investment. The fund tracks the FTSE All-World Index, providing exposure to over 3,600 large and mid-cap companies across both developed and emerging markets — covering approximately 98% of the investable global stock market. Countries represented include the US (approximately 65%), UK, Japan, France, Germany, China, India, and dozens more. Sectors span technology, healthcare, financials, consumer goods, energy, and industrials. The accumulating structure automatically reinvests dividends within the fund, compounding growth without any action required from the investor. For UK investors, VWRP is domiciled in Ireland (making it UCITS-compliant and legally appropriate for UK residents), trades on the London Stock Exchange in GBP, and can be held in a Stocks and Shares ISA, SIPP, or general investment account.

✓ Why it works: Truly global diversification in a single fund at minimal cost. The accumulating structure compounds automatically — ideal for long-term ISA and SIPP holders. Covers both developed and emerging markets. Motley Fool UK rates it as 'hard to beat' for a core portfolio holding.

⚠ Watch out for: US concentration risk: approximately 65% of the fund is in US equities, so VWRP is not as geographically balanced as its 'all-world' name implies. The Magnificent Seven technology stocks (Apple, Microsoft, Nvidia, Alphabet, Meta, Amazon, Tesla) make up approximately 35% of the US market and therefore a very significant portion of VWRP. Tech sector volatility can therefore have an outsized impact.

ETF 2: VUSA — Vanguard S&P 500 UCITS ETF (Your US Growth Engine)

VUSA tracks the S&P 500 — the index of the 500 largest publicly listed US companies by market capitalisation — at a tiny 0.07% annual cost. It is the most popular single-country ETF among UK investors, according to SmartInvestorUK's 2026 analysis, and for good reason. The S&P 500 has delivered an average annual return of approximately 10.26% since 1957, according to IG research published in December 2024. It has finished in positive territory in the great majority of years since 1871. The fund is physically replicated — it actually holds all 500 stocks — and tracks the index closely. VUSA is a distributing ETF, meaning it pays dividends into your account quarterly in USD rather than reinvesting them. This is worth knowing: if you want automatic reinvestment, the accumulating version (VUAG) is available on most platforms. VUSA trades on the London Stock Exchange in GBP, eliminating the FX conversion fees that would apply when buying US-listed ETFs such as VOO or SPY directly.

✓ Why it works: The S&P 500's long-term return record is the strongest of any major equity market. At 0.07% OCF it is one of the cheapest ETFs available. Buying in GBP avoids FX fees. VUSA adds a deliberate US tilt for investors who want to weight their portfolio toward the world's most dynamic economy — which already drives a significant portion of VWRP's returns.

⚠ Watch out for: Currency risk: VUSA holds US-dollar assets in a GBP-denominated wrapper. If sterling strengthens against the dollar, your GBP return will be lower than the USD return of the underlying stocks. Concentration in US mega-cap technology: the top 10 holdings make up approximately 38% of the index. As Motley Fool UK notes, 'in early 2026, the top 10 stocks in the index made up almost 40% of the S&P 500.' Combining VUSA with VWRP increases rather than decreases your US exposure.

ETF 3: VGOV — Vanguard UK Gilt ETF (Your Stability Layer)

VGOV tracks the Bloomberg UK Gilt Float Adjusted Index, providing exposure to UK government bonds — loans made to the UK government in exchange for regular interest payments and the return of capital at maturity. With a Total Expense Ratio of just 0.07%, VGOV is one of the cheapest ways to add fixed income to a UK portfolio. The fund pays a dividend yield of approximately 1.05% as of InvestEngine data, distributed to investors as income. UK gilts are considered one of the safest asset classes available to UK investors: the UK government has never defaulted on its bonds, and gilts are priced in sterling — eliminating currency risk for UK investors. In portfolio construction terms, gilts serve as a counterweight to equity volatility. During periods of equity market stress, investors typically move into government bonds, pushing gilt prices up. This negative correlation with equities (in most but not all market conditions) means a portfolio with a gilt allocation typically experiences lower peak-to-trough drawdowns during market crashes than a pure equity portfolio.

✓ Why it works: The lowest-risk component of the three-fund portfolio. Zero default risk for UK investors, zero currency risk. Provides income via the 1.05% yield. Acts as a portfolio stabiliser during equity market downturns, reducing peak-to-trough losses. At 0.07% OCF it is extremely cost-efficient for bond exposure.

⚠ Watch out for: Lower long-term returns than equities: gilts have historically returned approximately 3% to 4% per year over the long run — significantly below the equity risk premium. Rising interest rates reduce gilt prices (there is an inverse relationship between interest rates and bond prices). In 2022, UK gilts experienced significant losses as the Bank of England raised rates sharply. Younger investors with very long time horizons often hold little or no bonds, since they have time to ride out equity market volatility.

How to Allocate Between the Three ETFs

The allocation between VWRP, VUSA, and VGOV should reflect your investment time horizon, your risk tolerance, and your financial goals. The longer your time horizon and the greater your ability to tolerate short-term losses without panic-selling, the higher your equity allocation should be. The closer you are to needing the money, the more stability your portfolio needs.A note on combining VWRP and VUSA: because US stocks already make up approximately 65% of VWRP, adding VUSA alongside it further concentrates your portfolio in the US market. For an 'aggressive growth' allocation of 70% VWRP plus 30% VUSA, your effective US equity exposure is approximately 75% to 80% of the total equity portion. This is a deliberate bet on continued US outperformance — which has been well-rewarded historically but is not guaranteed. Investors wanting less US concentration might substitute a portion of VUSA for an emerging markets ETF such as VFEG (Vanguard FTSE Emerging Markets, 0.22% OCF) to increase geographic diversification.

The Power of Compounding: What Regular Investing Really Does

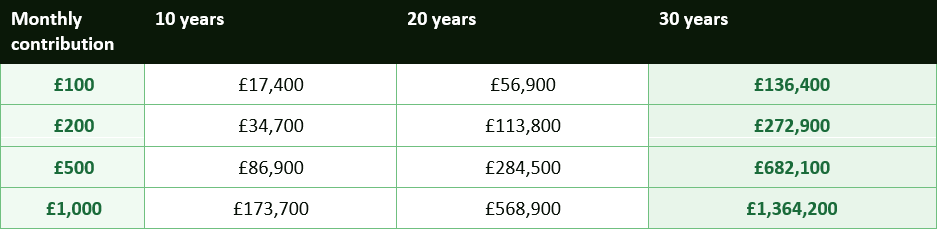

The most important force in long-term investing is compound growth — the process by which investment returns generate their own returns over time. Understanding what compound growth actually does to regular monthly investments over long periods is the most effective antidote to the temptation to time the market, wait for the 'right moment', or stop investing when markets fall.

Assumes 8% average annual return (broadly consistent with VWRP/global equity long-run historical average). Returns are before inflation and are illustrative only. Past performance is not a guide to future results.

The table makes two things clear. First, time is more powerful than the amount invested. The difference between starting at 25 and starting at 35, both investing £200 per month at 8% annual return, is approximately £136,500 by age 65. Second, even modest monthly amounts produce substantial long-run outcomes when held consistently. Someone investing £200 per month from age 30 to 60 accumulates approximately £272,900 — having contributed only £72,000 in total. The remaining £200,900 is pure compound growth.

This is why 'staying invested' is the single most important investment behaviour — more important than which specific ETFs you choose, which platform you use, or whether you time your investments optimally. The investors who build significant wealth through index ETFs are almost always distinguished not by investment sophistication but by starting early, investing consistently, and not panic-selling during market downturns.

Where to Buy: ISA, SIPP, and Platform Comparison

For UK investors, the choice of account wrapper and platform is almost as important as the choice of ETFs, because the tax treatment can have a dramatic effect on long-term returns — and platform fees can significantly erode them.Always use your ISA allowance first

The UK Stocks and Shares ISA allows you to invest up to £20,000 per tax year in stocks, ETFs, and funds with no income tax on dividends and no capital gains tax on returns. Over a 30-year investment horizon, the compounding of tax-free growth inside an ISA typically produces materially better outcomes than the same investment in a general investment account subject to dividend and capital gains taxation. If you are not filling your ISA allowance before investing outside it, you are unnecessarily reducing your long-term returns. All three ETFs — VWRP, VUSA, and VGOV — are eligible to be held inside a Stocks and Shares ISA on all major UK platforms.Consider a SIPP for pension investing

The Self-Invested Personal Pension (SIPP) offers additional tax advantages beyond the ISA: contributions receive tax relief at your marginal income tax rate (20% for basic-rate taxpayers, 40% for higher-rate), effectively meaning the government adds 25% to every basic-rate taxpayer's contribution. The trade-off is that money in a SIPP is locked away until at least age 57 (rising to 57 in 2028). For long-term retirement investing, the SIPP's tax relief can be worth significantly more than the ISA's flexibility.Platform comparison for VWRP, VUSA, and VGOV

10. Common Mistakes That Kill Long-Term Returns

Six mistakes that destroy long-term ETF portfolio returns — and how to avoid them

- Panic-selling during market downturns: Every significant market decline feels like it might be permanent when you are living through it. The investors who build the most long-term wealth are almost always those who held through the 2020 pandemic crash (the S&P 500 fell 34% in 33 days, then recovered fully within 6 months), the 2022 rate shock, and every other correction without selling. Selling in a downturn locks in losses and forfeits the recovery. The three-ETF portfolio's bond allocation (VGOV) reduces the severity of drawdowns and makes holding through volatility psychologically easier.

- Trying to time the market: Research by Vanguard, Fidelity, and Dalbar consistently shows that market timing — trying to buy at lows and sell at highs — destroys value for most investors compared with simply staying invested. The solution is pound-cost averaging: investing a fixed amount every month regardless of market levels, which automatically buys more shares when prices are low and fewer when they are high.

- Paying too much in platform fees: A 0.45% platform fee sounds small but on a £200,000 portfolio it costs £900 per year — more than the entire combined ETF cost of the three-fund portfolio. For ETF-only portfolios, InvestEngine and Trading 212 offer genuine £0 platform fees on UK-listed ETFs. Review your platform costs annually.

- Over-diversifying into too many funds: Adding a 4th, 5th, and 6th ETF to a three-fund portfolio rarely reduces risk meaningfully — it increases complexity, increases costs, and requires more rebalancing. VWRP alone holds over 3,600 stocks. That is already extraordinarily diversified.

- Ignoring currency risk in VUSA: VUSA holds US dollar assets in a GBP-denominated wrapper. Sterling appreciation reduces returns; sterling depreciation enhances them. For long-term investors this risk tends to average out, but it is worth being aware that short-term swings in the GBP/USD exchange rate can meaningfully affect your reported returns in any given year.

- Not rebalancing annually: Over time, a rising equity market will increase the equity proportion of your portfolio beyond your target allocation, increasing risk beyond your intended level. An annual rebalance — selling some of the best-performing asset class and buying more of the underperforming one — maintains your target allocation, reduces risk, and implements a systematic buy-low sell-high discipline without market timing.

The Three-ETF Portfolio vs More Complex Strategies

A common objection to the three-fund approach is that more sophisticated strategies — factor investing (smart beta), tactical asset allocation, satellite positions in individual sectors or themes — should outperform simple index investing over time. This objection deserves honest engagement.Factor investing — tilting a portfolio toward small-cap, value, or quality stocks that have historically outperformed the broad market — has academic support and can add value for investors who understand it and maintain the discipline to hold through periods of factor underperformance. But the key word is discipline: many investors who add factor tilts to their portfolio abandon them when the factor underperforms for two or three years, capturing neither the factor premium nor the market premium.

Thematic investing — concentrating in AI, clean energy, semiconductor, or other themed ETFs — has produced spectacular short-term returns in some cases and equally spectacular losses in others. The performance of themed ETFs is highly dependent on timing, and the evidence that retail investors can reliably identify winning themes in advance is weak. The investors who bought an AI-focused ETF in early 2023 did well; those who bought a clean energy ETF in 2021 at peak valuations did not.

For most investors — particularly those with fewer than ten years of experience, those without the time to research factors and themes rigorously, and those who know from experience that they are vulnerable to panic-selling during drawdowns — the three-fund portfolio is not a compromise or a starting position. It is the best strategy available. Its simplicity is not a weakness — it is the mechanism by which investors actually implement it and maintain it through the market cycles that defeat more complex approaches.

CONCLUSION

A portfolio of VWRP (global equity core), VUSA (US growth engine), and VGOV (stability layer) gives a UK investor access to over 4,100 different stocks and bonds across every major economy in the world at a blended cost of 0.10% to 0.19% per year. Held consistently inside an ISA or SIPP over 20 to 30 years, with regular monthly contributions and annual rebalancing, this three-fund portfolio has the structural ingredients to build genuine, life-changing long-term wealth.The strategy will not be exciting. It will not have a chart that goes straight up every year. It will require you to keep investing through market crashes, geopolitical scares, and periods when something else looks far more attractive. But the evidence is overwhelming that this discipline — applied consistently over long periods at low cost — produces outcomes that the vast majority of more complex strategies fail to match. The three ETFs in this guide are not the only way to build long-term wealth through passive investing. But they are among the simplest, cheapest, and most proven approaches available to UK investors in 2026.

⚠ Important: This article is for educational purposes only and does not constitute financial advice. Investing involves risk; the value of investments can fall as well as rise and you may get back less than you invest. Past performance is not a reliable indicator of future returns. Always conduct your own research or consult a qualified financial adviser before making investment decisions.

Frequently Asked Questions

Why choose VWRP as the core global holding rather than iShares SWDA?

Both VWRP (Vanguard FTSE All-World) and SWDA (iShares Core MSCI World) are excellent choices for the global equity core of a three-fund portfolio. The key difference is that VWRP includes emerging markets (approximately 10% of the fund in countries including China, India, Brazil, and Taiwan), while SWDA covers developed markets only (approximately 1,400 stocks). VWRP has a slightly higher OCF at 0.19% to 0.22% vs SWDA's 0.20%. For investors who want truly comprehensive global coverage — including the growth potential of emerging markets — VWRP is the stronger choice. For a slightly cheaper developed-markets-only fund, SWDA is a sound alternative, potentially paired with a separate emerging markets ETF like VFEG.If VWRP already holds 65% US stocks, why add VUSA at all?

You do not have to. Many UK investors build their entire equity portfolio with VWRP alone — it is genuinely diversified and highly cost-effective as a standalone holding. Adding VUSA is a deliberate choice to tilt the portfolio more heavily toward US equities, based on the argument that the US market is the world's most productive economy and has historically delivered the highest equity returns. However, this is a concentration bet, not a diversification strategy. If you add VUSA alongside VWRP, you are increasing your US exposure significantly and reducing the weight of all other countries in your effective portfolio. This is a reasonable choice, but it should be a deliberate one rather than a default assumption that more is better.Is VGOV the best bond ETF for UK investors, or should I look at alternatives?

VGOV (Vanguard UK Gilt, 0.07% OCF) is an excellent choice for UK investors wanting low-risk, sterling-denominated fixed income exposure with no currency risk. It is one of the most cost-effective government bond ETFs available in the UK. Alternatives worth considering depending on your objectives include: iShares Core UK Gilts (IGLT, 0.07% OCF) — very similar to VGOV and a direct alternative; Vanguard Global Aggregate Bond (VAGP, 0.10% OCF) — broader global bond exposure including corporate bonds, but with some currency risk; iShares USD Treasury Bond ETFs — for investors comfortable with US dollar exposure seeking higher nominal yields. For UK investors prioritising capital preservation and minimum complexity, VGOV is the simplest and most appropriate choice.What is the best platform to hold VWRP, VUSA, and VGOV in an ISA?

For an ETF-only ISA in 2026, InvestEngine and Trading 212 currently offer zero platform fees on GBP-denominated UK-listed ETFs — meaning you pay only the ETFs' own ongoing charges (0.07% to 0.19%). This makes them the most cost-effective option for pure ETF portfolios, particularly for investors making regular monthly contributions where per-trade dealing fees would otherwise accumulate. Vanguard Investor is excellent for Vanguard-only portfolios at 0.15% platform fee (capped at £375 annually). Hargreaves Lansdown and AJ Bell offer the best features and customer service but charge higher platform fees. Compare costs annually as they change.How often should I rebalance the three-ETF portfolio?

Once per year is the broadly recommended rebalancing frequency for a passive ETF portfolio — sufficient to maintain your target allocation without excessive trading friction. A practical approach is to rebalance on the same date each year (for example, your ISA subscription anniversary). If markets move dramatically — say, equities rise 40% in a single year and significantly exceed your target allocation — an interim rebalance may be warranted. Inside an ISA, rebalancing is tax-free. In a General Investment Account, selling an ETF that has appreciated to rebalance may crystallise a capital gain subject to CGT — factor this into your rebalancing decisions outside a tax wrapper.How much should I invest each month to build meaningful long-term wealth?

The most honest answer is: as much as you sustainably can, started as early as possible. The compound growth table in Section 8 shows that £200 per month invested at 8% annual return for 30 years produces approximately £272,900 — with only £72,000 contributed and the rest generated by compound growth. Start with whatever amount you can afford without compromising your emergency fund or your debt repayment strategy — even £50 to £100 per month builds meaningful foundations. The single most important variable is consistency over time, not the exact monthly amount. Increase your contribution whenever your income rises, and resist the temptation to stop investing during market downturns.References

The Motley Fool UK — 7 Best ETFs to Buy in May 2026 (VWRP, VUSA) https://www.fool.co.uk/2025/12/27/3-top-vanguard-etfs-to-consider-for-an-isa-or-sipp-in-2026/SmartInvestorUK — Best ETFs UK 2026: Global, VWRL vs SWDA, ISA Picks https://smartinvestoruk.co.uk/best-etfs-uk/

ShareInvestingUK — Best ETF Strategy Guide: Vanguard vs iShares UK 2026 https://shareinvestinguk.com/top-etfs-for-uk-investors/

Financial Interest — The Best Vanguard Funds for UK Investors in 2026 (VWRP, VUSA, VGOV) https://financialinterest.com/best-vanguard-funds/

InvestEngine — Top Vanguard ETFs for UK Investors 2026 (VWRP, VUSA, VGOV) https://blog.investengine.com/top-vanguard-etfs-top-funds-for-investors/

VWRP.co.uk — Vanguard FTSE All-World UCITS ETF Analysis 2026 https://vwrp.co.uk/

JustETF UK — Best Bond ETFs 2026 (VGOV and alternatives) https://www.justetf.com/uk/market-overview/the-best-bond-etfs.html

The Motley Fool US — Best S&P 500 ETFs to Buy in 2026 (VUSA/VOO comparison) https://www.fool.com/investing/stock-market/indexes/sp-500/etfs/

Vanguard UK — VWRP ETF Product Page https://www.vanguard.co.uk/professional/product/etf/equity/9679/ftse-all-world-ucits-etf-usd-accumulating

MoneyHelper — Beginners' Guide to Investing and ISAs https://www.moneyhelper.org.uk/en/savings/investing

0 Comments Comments