Financial Literacy

China vs Singapore vs UK vs US: Personal Finance Compared

Table of Contents

Household Savings Rates: The Starkest Difference

China: A Savings Culture Forged by Limited Social Safety Nets

Singapore: The World's Most Comprehensive Forced-Savings System

United Kingdom: Voluntary Saving Within a Tax-Funded Safety Net

United States: High Consumer Credit Use Within a Privatised Safety Net

Structural Comparison: The Systems Behind the Numbers

What Each System Can Teach the Others

Conclusion

Frequently Asked Questions (FAQ)

External References & Further Reading

Personal finance is never purely a matter of individual choice. It is shaped profoundly by the institutions, policies, and social safety nets each person is born into — the retirement system they will eventually rely on, the housing market they must navigate, the healthcare costs they may or may not have to plan for directly, and the cultural norms around debt and saving that surround them from childhood. Comparing personal finance across countries is therefore less a comparison of individual virtue or discipline, and far more a comparison of the structural systems that shape financial behaviour at scale.

China, Singapore, the United Kingdom, and the United States offer a particularly illuminating comparison because they represent four genuinely distinct models. China combines a rapidly developing economy with deep-rooted savings norms and a property-centred wealth model. Singapore operates one of the world's most distinctive forced-savings systems through its Central Provident Fund, achieving the highest household savings rate of any major economy. The UK and the US, despite sharing a common law tradition and broadly similar financial products, diverge in meaningful ways around homeownership, healthcare-linked financial risk, and consumer credit norms.

This guide compares these four systems across the metrics that matter most in personal finance: savings rates, retirement provision, debt levels, housing and wealth composition, and the cultural and policy forces that explain the differences. The goal is not to rank these systems as superior or inferior, but to understand, with real data, why financial behaviour looks so different across these four economies — and what each can teach the others.

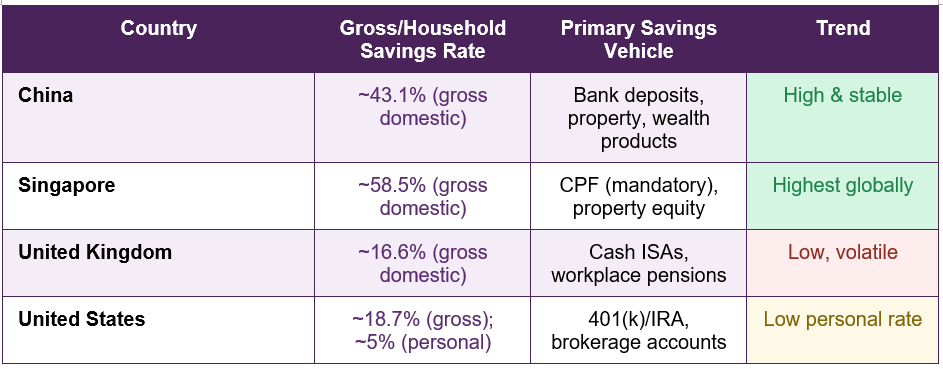

Household Savings Rates: The Starkest Difference

The most immediately striking difference between these four economies is the sheer scale of the gap in savings rates. The table below presents the most recent comparable data:

Singapore's gross domestic savings rate: ~58.5% — more than three times the UK's rate and more than ten times the US personal savings rate, driven overwhelmingly by the mandatory CPF system rather than voluntary household choice (AMFI-Crisil Factbook 2024)

- An important measurement distinction: Gross domestic savings rates (used for China and Singapore in most international comparisons) capture savings across households, businesses, and government combined, while personal savings rates (more commonly cited for the UK and US) capture only household-level saving from disposable income. This is not simply a quirk of statistics — it reflects a genuinely different structure: Singapore's rate is dominated by mandatory CPF contributions deducted before a worker ever sees the income, while UK and US savings rates capture discretionary household decisions made after wages are received, which is a fundamentally more voluntary and therefore more variable behaviour.

China: A Savings Culture Forged by Limited Social Safety Nets

China's household savings rate, while moderating somewhat from its historic peaks, remains among the highest of any major economy, with gross domestic savings around 43% of GDP. Economists studying this phenomenon consistently point not to abstract cultural preference but to specific structural realities: the relatively recent emergence of China's modern pension and healthcare systems means many households, particularly older generations, experienced decades without comprehensive state-provided social insurance, creating powerful incentives to self-insure through personal savings against medical emergencies, job loss, and old age.The one-child policy era (1980-2015) is also frequently cited by economists as a contributing factor, as it altered family structures in ways that reduced the traditional expectation that multiple children would collectively support ageing parents, increasing the incentive for individual households to accumulate their own retirement savings. Real estate plays an outsized role in Chinese household wealth, with property estimated to represent 60-70% of typical urban household assets — a concentration that reflects both genuine investment preference and, historically, the relative scarcity of well-developed, accessible alternative investment vehicles such as mutual funds and stock markets for ordinary households.

China's household debt-to-income ratio, while historically low by Western standards, has been rising steadily, driven primarily by mortgage borrowing as homeownership rates climbed and property prices appreciated significantly over the past two decades. This represents a genuine structural shift: a generation of savers is increasingly also becoming a generation of mortgage borrowers, a transition the UK and US underwent decades earlier.

Singapore: The World's Most Comprehensive Forced-Savings System

Singapore's approach to personal finance is unique among major economies because so much of its high savings rate is not a matter of individual discretion at all — it is structurally mandated through the Central Provident Fund (CPF), a comprehensive social security savings scheme that every employed Singapore citizen and permanent resident contributes to throughout their working life.As of 2025, CPF contribution rates for younger workers total up to 37% of wages — typically 20% from the employee and 17% from the employer — split across three accounts: the Ordinary Account (usable for housing, insurance, and approved investments), the Special Account (focused on retirement and investment), and the MediSave Account (dedicated specifically to healthcare expenses, including hospitalisation and approved medical insurance premiums). This structure means a significant share of every Singaporean worker's compensation is automatically diverted into long-term savings before it is ever available for discretionary spending — a stark contrast to the voluntary, opt-in nature of UK and US retirement saving.

Singapore CPF contribution rate (under-55 workers, 2025): Up to 37% of wages — split between employer and employee, automatically allocated across retirement, housing, and healthcare-specific accounts — making Singapore's high savings rate substantially structural rather than purely behavioural (CPF Board, 2025)

This system has profound knock-on effects on the entire shape of Singaporean personal finance. The vast majority of Singaporeans purchase their primary home using CPF Ordinary Account savings to fund a Housing & Development Board (HDB) flat, meaning home equity and retirement savings are deeply intertwined in a way that is structurally different from the UK or US, where pension savings and property equity are typically separate and independently managed pools of wealth. Singapore's MediSave system similarly pre-funds healthcare costs directly from income, reducing (though not eliminating) the unplanned medical expense risk that drives much of the precautionary saving behaviour observed in both China and the United States.

United Kingdom: Voluntary Saving Within a Tax-Funded Safety Net

The UK occupies a distinctive middle ground: a comprehensive, tax-funded social safety net (most visibly the NHS, which removes most direct point-of-care healthcare costs from household financial planning) combined with a comparatively low household savings rate of around 16.6% on a gross domestic basis, and historically much lower again on a net personal savings basis during many recent years.This combination reflects a specific structural logic: because the NHS substantially reduces the precautionary savings motive that drives high savings in both China (limited historical healthcare coverage) and the US (high direct healthcare costs and insurance gaps), UK households face less structural pressure to self-insure against medical financial shock through personal savings. Auto-enrolment into workplace pensions, introduced from 2012, has meaningfully increased the proportion of UK workers saving specifically for retirement, but participation and contribution rates remain considerably below CPF-mandated levels in Singapore.

UK household debt, driven substantially by mortgage borrowing in one of the most expensive housing markets among major developed economies relative to income, sits among the highest debt-to-income ratios of the four economies compared here. The structural housing affordability challenge discussed extensively in UK personal finance commentary — median house prices around £290,000 against median earnings that have grown far more slowly — means a large share of UK household balance sheets are concentrated in mortgage debt and the corresponding property asset, a pattern that echoes China's property-heavy wealth composition despite very different underlying causes.

United States: High Consumer Credit Use Within a Privatised Safety Net

The United States combines the lowest personal savings rate of the four economies compared here — typically hovering around 4-5% of disposable income in recent years, compared to Singapore's 58.5% gross domestic rate — with one of the most extensive and widely used consumer credit systems in the world. Credit cards, buy-now-pay-later products, and revolving consumer debt are deeply embedded in everyday US financial behaviour in a way that is less pronounced in China and Singapore, and present but generally less extensive in the UK.This pattern is substantially explained by the US's comparatively privatised social safety net. Healthcare costs, predominantly funded through employer-sponsored insurance or direct private purchase rather than general taxation, create significant financial exposure for households facing medical emergencies, job loss-triggered loss of coverage, or underinsurance — exposure that, somewhat counterintuitively, often manifests as a reliance on credit in the moment of need rather than translating into higher precautionary saving in advance, particularly for lower and middle-income households operating with limited financial slack.

Retirement provision in the US similarly follows a voluntary, individually managed model through 401(k) and IRA accounts, in contrast to Singapore's mandatory CPF system. US stock market participation is the highest of the four economies compared here, both through direct retail investing and through 401(k) plans that are overwhelmingly invested in equity markets — a structural feature that exposes US retirement wealth to greater market volatility than Singapore's CPF (which combines guaranteed minimum interest rates with more conservative default allocations) or China's property-heavy household wealth model.

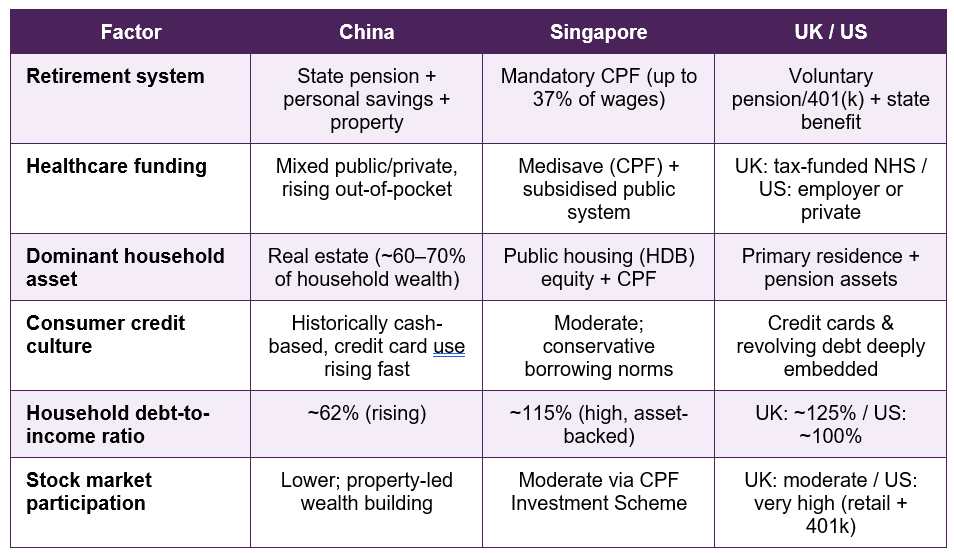

Structural Comparison: The Systems Behind the Numbers

The table below summarises the core structural differences across retirement provision, healthcare funding, dominant household assets, and debt culture that ultimately explain the savings rate gap described above:

What emerges from this comparison is that the headline savings rate gap between Singapore (highest) and the US (lowest) is not primarily a story about cultural attitudes toward thrift or discipline. It is, to a substantial degree, a story about how much of the saving and risk-protection function is handled structurally — through mandatory contributions and tax-funded services, as in Singapore and the UK — versus how much is left to individual discretion and private market solutions, as in the US, with China occupying a distinctive position shaped by its rapidly evolving social insurance system and historically strong cultural and economic incentives toward self-reliant saving.

What Each System Can Teach the Others

- From Singapore — the power of structural defaults: Singapore's CPF demonstrates how automatic, structurally embedded savings mechanisms can achieve consistently high savings rates that voluntary systems struggle to replicate, even when individuals in those voluntary systems express a strong intention to save. The UK's auto-enrolment pension reform and the US's growing use of automatic 401(k) escalation features are both, in effect, partial adoptions of this same behavioural insight.

- From China — the risk of concentrated wealth in a single asset class: China's heavy concentration of household wealth in real estate illustrates both the power of a strong cultural savings ethic and the genuine risk of insufficient diversification, a lesson increasingly visible as Chinese property markets have experienced significant volatility in recent years. Both the UK and US, with their own substantial concentration of middle-class wealth in primary residences, face a related (if less extreme) version of this same diversification challenge.

- From the UK — the savings-reducing effect of comprehensive public services: The UK's relatively low household savings rate, sitting alongside a comprehensive tax-funded healthcare system, demonstrates that strong public provision can legitimately reduce the precautionary savings burden households need to carry individually — a trade-off involving higher general taxation in exchange for reduced direct financial risk at the household level.

- From the US — the depth and accessibility of capital markets: Despite its low savings rate, the US has the most developed and widely accessible capital markets of the four economies, providing US households who do save with comparatively strong long-term wealth-building tools through diversified, low-cost investment vehicles — a genuine structural advantage that partially offsets the lower savings rate for those households who do participate consistently.

Conclusion

The differences in personal finance behaviour between China, Singapore, the UK, and the US are real, substantial, and well documented in the data — but they are differences in systems and structures far more than they are differences in individual character or financial wisdom. Singapore's extraordinarily high savings rate reflects a mandatory contribution system, not simply a uniquely disciplined population. China's strong savings culture reflects decades of limited social insurance provision driving rational precautionary behaviour. The UK's comparatively modest savings rate sits alongside one of the world's most comprehensive tax-funded healthcare systems. The US's high consumer credit use and low savings rate reflect a more privatised, individually managed approach to both retirement and healthcare risk.Understanding personal finance through this comparative, structural lens is valuable regardless of which of these systems you personally navigate. It reveals that the financial behaviours your own country considers 'normal' — whether that is the UK's comparatively low savings rate, the US's extensive credit card use, China's property-heavy wealth concentration, or Singapore's mandatory retirement contributions — are not universal human tendencies but the product of specific policy choices and historical circumstances. This understanding can inform genuinely useful personal decisions: recognising the value of automating savings the way Singapore's CPF does by default, diversifying wealth beyond a single asset class as China's property concentration illustrates the risk of, and weighing the trade-offs between higher individual financial discipline and the kind of structural, system-level support that reduces the burden of that discipline in the first place.

No single one of these four systems is unambiguously superior across every measure — each involves genuine trade-offs between individual flexibility, government-mandated discipline, and the social provision of risk protection. What is clear is that personal finance outcomes at a national scale are shaped overwhelmingly by policy and institutional design, a fact worth remembering both when comparing countries and when considering what kind of system, or what kind of personal habits within whatever system you live under, might serve your own financial future best.

Frequently Asked Questions (FAQ)

Why does Singapore have such a dramatically higher savings rate than the UK or US?

The primary driver is structural rather than behavioural: Singapore's Central Provident Fund mandates contributions of up to 37% of wages for younger workers, automatically allocated to retirement, housing, and healthcare-specific accounts before the money is ever available for discretionary spending. The UK and US, by contrast, rely on voluntary pension and retirement saving systems, where individuals choose how much (if anything) to contribute. This structural difference, not a difference in individual thriftiness, explains the overwhelming majority of the savings rate gap.Is China's high savings rate purely cultural, or are there other explanations?

While cultural factors around thrift and family financial responsibility are frequently cited, economists studying Chinese savings behaviour place at least as much emphasis on structural factors: the relatively recent development of comprehensive public pension and healthcare systems, meaning many households have strong precautionary incentives to self-insure; demographic shifts including the one-child policy era altering traditional family support structures; and historically limited access to diversified investment alternatives, which concentrated savings heavily into bank deposits and real estate. Treating the savings rate as purely a cultural trait overlooks these substantial policy and demographic drivers.Why is consumer credit and debt so much more prevalent in the US compared to Singapore or China?

US consumer credit prevalence is linked substantially to the comparatively privatised nature of healthcare funding and retirement provision, which creates financial exposure that households often manage reactively through credit rather than proactively through high precautionary savings. The US also has one of the world's most developed consumer credit infrastructures and reward/rewards-card cultures, making credit both more accessible and more deeply embedded in everyday spending norms than in Singapore's more conservative borrowing culture or China's historically more cash- and savings-based consumer environment, though credit card use in China has grown substantially in recent years.Does a higher savings rate always mean better personal finance outcomes?

Not necessarily, and this is an important nuance. A high savings rate driven by mandatory contributions (Singapore) or strong precautionary motives in the absence of social insurance (historically, China) reflects a different reality than a high savings rate arising from genuine surplus income and deliberate wealth-building choices. Equally, a lower savings rate (UK, US) does not automatically indicate poor financial management if it coexists with strong public risk-pooling mechanisms, such as tax-funded healthcare, that reduce the need for individual precautionary saving in the first place. The right way to interpret a savings rate is always in the context of the surrounding social and institutional system, not in isolation.What can individuals in lower-saving countries like the UK or US learn from Singapore's CPF model?

The most transferable lesson is the behavioural power of automation and defaults. Singapore's CPF demonstrates that structurally embedded, automatic savings consistently outperform voluntary saving, even among individuals with good intentions, simply because automation removes the need for ongoing willpower and decision-making. UK and US savers can apply this insight at the individual level by maximising employer pension/401(k) auto-enrolment defaults, setting up automatic transfers to retirement and investment accounts, and treating these contributions as non-negotiable, much as CPF contributions are non-negotiable for Singaporean workers — effectively building a personal, voluntary version of the same structural discipline.External References & Further Reading

The following authoritative sources were used in researching this article and are recommended for further reading:1. CEIC Data — China Gross Savings Rate (Historical and Current Data)

https://www.ceicdata.com/en/indicator/china/gross-savings-rate

2. AMFI-Crisil Factbook 2024 — Global Domestic Savings Rate Comparison

https://upstox.com/news/personal-finance/latest-updates/higher-than-us-japan-but-lower-than-china-how-india-compares-with-top-countries-in-domestic-savings-rate/article-149336/

3. CPF Board (Singapore) — CPF Contribution Rates from 1 January 2025

https://www.cpf.gov.sg/employer/infohub/news/cpf-related-announcements/new-contribution-rates

4. World Bank — Gross Domestic Savings (% of GDP) by Country

https://data.worldbank.org/indicator/NY.GDS.TOTL.ZS

5. OECD — Household Savings Indicator Database

https://www.oecd.org/en/data/indicators/household-savings.html

6. World Population Review — Personal Savings Rate by Country 2026

https://worldpopulationreview.com/country-rankings/personal-savings-rate-by-country

7. Bank of England / ONS — UK Household Debt and Savings Statistics

https://www.ons.gov.uk/economy/nationalaccounts/uksectoraccounts

8. Federal Reserve — US Personal Saving Rate and Household Debt Statistics

https://www.federalreserve.gov/releases/g19/current/

0 Comments Comments