Financial Literacy

Stability Over Status: Debt-Free Living as New Luxury

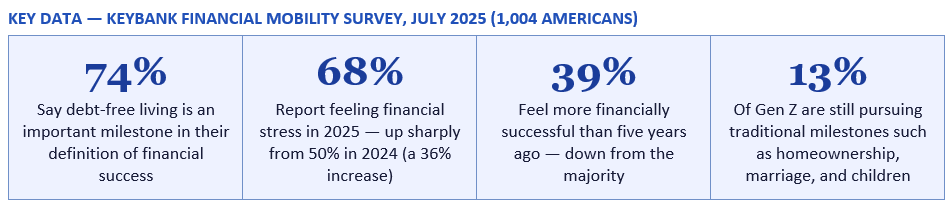

Three in four Americans now say being debt-free is the most important milestone in their definition of financial success — ahead of buying a home, getting married, or building wealth. Financial stress has risen from 50% to 68% in a single year. And the rising cost of living is pushing consumers to cut spending, switch to cheaper brands, and recalibrate what prosperity actually means. This is the full story behind America's most important financial mindset shift in a generation.

Three in four Americans — precisely 74% — say that being debt-free is an important milestone in their definition of financial success. This figure places debt-free living ahead of other traditional markers of financial achievement in the public consciousness. It is not that Americans have stopped caring about wealth — it is that the definition of what constitutes wealth has been rewritten. Freedom from debt is now seen as a form of financial prosperity in its own right, independent of income level, net worth, or the accumulation of assets.

Simultaneously, the survey found that financial stress has jumped from 50% to 68% of Americans in a single year — a 36% increase that represents one of the sharpest rises in financial anxiety recorded in any major survey in recent years. Yet — and this is the crucial nuance in the data — the majority of financially stressed Americans are not disengaging from financial planning. They are redirecting their energy. One in three (35%) respondents say they feel in control of, or proud of, how they manage their money. The pressure is being converted into purpose rather than paralysis.

The measure of success is not wealth alone, but also the ability to live debt-free and prepare for what's ahead. The financial landscape for Americans is shifting in profound ways.

— DANIEL BROWN, EVP AND DIRECTOR OF CONSUMER PRODUCT MANAGEMENT, KEYBANK (NOVEMBER 2025)

For most of the twentieth century, the American financial success narrative was built around a clear sequence of life milestones: education, employment, marriage, homeownership, children, retirement. This sequence both structured individual financial planning and defined the social meaning of success. Each milestone was simultaneously a financial achievement and a social signal — a house was both shelter and status, a wedding both a relationship and a public declaration of having 'made it.'

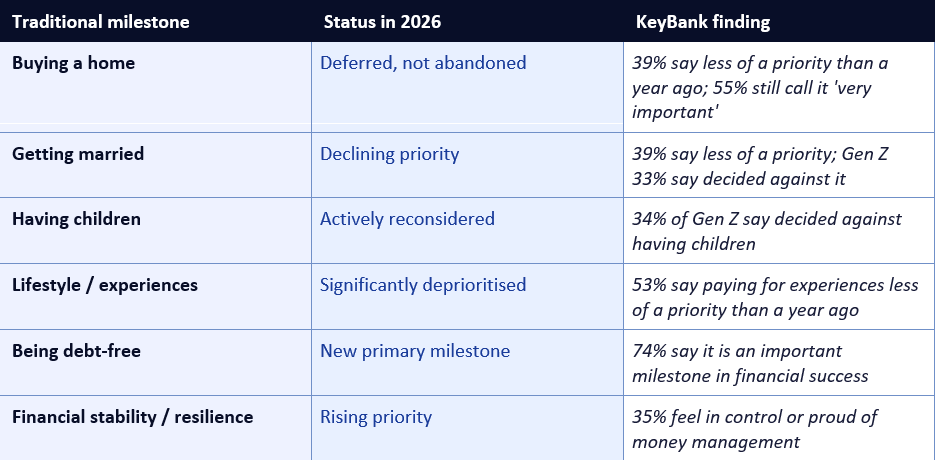

The KeyBank data shows this structure unravelling at a remarkable pace. More than half of survey respondents (53%) say that paying for experiences or a certain lifestyle is now less of a priority than one year ago. Thirty-nine per cent say that both buying a home and getting married are less of a priority than one year ago. These are not marginal adjustments — they are significant reorderings of life priority from large proportions of the American adult population.

It would be a mistake to interpret this data as a collapse of aspiration. The same survey found that 55% of Americans still consider homeownership a 'very important' part of their definition of success — indicating that the desire for homeownership has not disappeared, but rather been deferred or deprioritised in the face of affordability barriers. Similarly, the decline in marriage and children as financial priorities likely reflects a combination of cost factors (the average US wedding costs approximately $35,000; the cost of raising a child to 18 is estimated at $300,000 or more) and a genuine reorientation of values rather than a simple abandonment of tradition.

The CreditOne Bank/Pollfish survey of 1,000 US adults conducted in December 2025 and published in January 2026 reinforces this picture from a different angle. It found that 33% of US consumers define financial success as being debt-free, regardless of income or assets — placing debt freedom ahead of homeownership, investment growth, and even salary level as the primary marker of success. Notably, 31% of Gen Z respondents in the same survey said financial success means having flexible work and control over their time — suggesting that the new definition of success is not only about debt freedom but about autonomy more broadly.

The Vanguard Consumer Survey published in October 2025 adds a complementary data point: 84% of Americans have a financial resolution for 2026, with building an emergency fund and using a high-yield savings account as the top two goals. These are not aspirational wealth-building objectives. They are defensive resilience goals — the financial equivalent of building a wall against the next shock rather than climbing toward a higher summit. When building an emergency fund becomes the number-one financial aspiration of a majority of Americans, the redefinition of success from status to stability is essentially complete.

Yet alongside this stress, one in three Americans (35%) say they feel in control of, or proud of, how they manage their money. This is not a contradiction — it is a documented psychological response to financial difficulty. Research in behavioural economics consistently shows that periods of financial constraint, when they do not become overwhelming, often produce more deliberate and disciplined financial behaviour. The restriction of financial slack forces prioritisation; prioritisation produces clarity; clarity produces a sense of agency that coexists with — and in some cases grows out of — genuine financial hardship.

KeyBank's own framing of this dynamic is that Americans are 'turning pressure into purpose.' The survey commentary notes that 'even as 68% of Americans feel financial stress, many are channeling that pressure into purposeful financial planning and long-term resilience.' Contributing to retirement funds (32%) and saying no to plans in order to save money (30%) are identified as the top behaviours that feel most like financial 'adulting' — a term that captures the generational recalibration of what it means to be financially responsible. For many Americans in 2026, financial maturity is no longer defined by the acquisition of status symbols. It is defined by the discipline to build a financial fortress against uncertainty.

The mechanism is straightforward: when the cost of essentials rises faster than income, households are forced to eliminate non-essential spending. The goods and experiences that previously served as status signals — restaurant meals, new clothing, upgrades to technology and appliances, premium subscriptions, luxury convenience purchases — are the first categories to be cut. Over time, their absence normalises. The household discovers that their quality of life does not significantly deteriorate without these expenditures, and that the money freed up by eliminating them can be redirected toward debt repayment or savings accumulation with meaningful, visible results. The frugality forced by cost of living pressure becomes internalised as a value.

The KeyBank data shows this dynamic clearly. With a sharp eye on inflation, Americans are making deliberate trade-downs across consumer categories. The survey notes that 'the rising cost of living and increased price of everyday items are putting a strain on wallets across America' — and that households are responding not with despair but with recalibration. As the survey's framing puts it, Americans are strategically recalibrating their entire approach to money, not merely reacting emotionally to pressure.

The KeyBank survey identifies that Americans are making deliberate choices to prioritise staples and privacy over perks and popularity — a framing that captures the trade-off between the social signalling value of premium consumption and the financial utility of essentials spending. Consumers who previously defined themselves partly through their brand choices — the coffee shop they frequented, the clothing brands they wore, the restaurants they used — are increasingly separating their identity from their consumption choices.

The CreditOne Bank survey adds important nuance: 22% of respondents making under $50,000 per year say a $1,000 emergency fund would make them feel more financially secure — placing an extremely modest financial buffer as a higher priority than any consumer purchase. When the most psychologically impactful financial improvement available to a significant segment of the population is a thousand-dollar savings buffer, the entire framework of consumer aspiration has shifted away from consumption toward protection.

This is a generation that entered adulthood watching its older siblings and Millennial predecessors struggle with student loan debt that took decades to repay, housing markets that had become inaccessible, and an employment landscape disrupted first by the 2008 financial crisis and then by the pandemic and the AI transition. The rational response to this environment — to reject the financial commitments that trapped earlier generations and to build a definition of success around freedom, flexibility, and the absence of debt — is precisely what the data documents.

The CreditOne Bank survey of December 2025 provides an additional Gen Z data point: 31% of Gen Z respondents say financial success means having flexible work and control over their time — placing autonomy ahead of wealth accumulation or any traditional milestone. This finding is consistent with broader generational research showing that Gen Z prioritises work-life integration, purpose alignment, and the ability to control their schedule over traditional metrics of career advancement and salary growth. When combined with the debt-free aspiration (74% overall, likely higher for Gen Z specifically), the emerging Gen Z financial ideal is not poverty or resignation but something more like voluntary simplicity: a deliberate choice to live within means, eliminate debt, and buy back time rather than accumulate assets.

Critically, the KeyBank data notes that 'the kids are alright' — in contrast to Gen X, which the survey identifies as most squeezed and most in need of what the survey describes as a 'financial miracle.' Gen Z's rejection of traditional milestones is not driven by inability but by recalibration: a generation that has calculated the true cost — financial, psychological, and temporal — of chasing traditional success markers and decided the price is too high.

Credit card debt is the category that generates the most acute financial stress in everyday life because it carries the highest interest rates (averaging 20% to 22%) and the smallest required minimum payments relative to total balance — meaning that making only minimum payments on a $10,000 credit card balance at 21% APR will take over 30 years to pay off and cost more in interest than the original principal. The Federal Reserve Bank of New York's consumer credit data showed credit card delinquencies rising through 2024 and into 2025 — indicating that a growing share of American households are struggling to service their existing debt even before factoring in new borrowing.

Student loan debt — approximately $1.7 trillion nationally — resumed regular repayment for millions of borrowers in late 2023 after pandemic-era forbearance, adding hundreds of dollars per month in new mandatory outgoings for millions of households precisely as other costs were rising sharply. For many borrowers, especially those in their late 20s and 30s, the resumption of student loan payments has represented the single largest financial shock of the post-pandemic period.

In this environment, the aspiration to be debt-free is not merely philosophical — it is intensely practical. A household that eliminates $800 per month in credit card and student loan payments has effectively given itself a $800 per month pay rise. The freed cash flow can be redirected to savings, investment, or simply a reduction in the financial anxiety that constrains daily decision-making. The luxury of debt-free living is not the luxury of having things — it is the luxury of options, flexibility, and peace of mind.

This inversion has a strong psychological foundation. Research in wellbeing economics consistently shows that above a certain income threshold (estimated at approximately $75,000 to $100,000 per year in the US), additional income produces diminishing returns on life satisfaction. What does continue to improve life satisfaction at higher income levels is not additional consumption but rather increased control over one's time, reduction in financial anxiety, and the ability to make choices unconstrained by financial necessity. Debt-free living delivers precisely these goods.

The anthropologist David Graeber, in his influential work on debt, observed that debt creates a form of social and psychological dependency that pervades every aspect of the debtor's life — constraining career choices, relationships, and daily behaviour in ways that the debtor often does not fully recognise until the debt is gone. The experience of paying off a significant debt is consistently described by those who have done it not in terms of the financial gain but in terms of the psychological liberation — a lightness, a sense of possibility, and a recovery of agency that is qualitatively different from any consumer experience. This psychological dimension of debt freedom is what makes it genuinely luxury in the original sense: something that provides a quality of life beyond mere material sufficiency.

This shift has profound implications for consumer behaviour, for the brands and retailers that serve American households, and for the financial system that has historically profited from the normalisation of consumer debt. But its most important implications are personal. For the millions of Americans carrying credit card balances, student loans, and auto debt through an inflationary environment while watching traditional milestones recede into unaffordability, the redefinition of success around debt freedom is not just data — it is permission.

Permission to prioritise financial stability over social performance, to make the deliberate choices that lead to genuine freedom, and to discover that the most meaningful luxury available in 2026 is not what you own but what you no longer owe.

Yahoo Finance / KeyBank — Is Debt-Free the New Luxury? KeyBank Survey Explores (November 2025) https://finance.yahoo.com/news/debt-free-luxury-keybank-survey-143000264.html

Money.com — For Most Americans, Financial Success Now Means Being Debt-Free (November 2025) https://money.com/americans-define-financial-success/

ACA International — A New Standard of Success: Americans Put 'Debt-Free' at the Top (November 2025) https://www.acainternational.org/news/a-new-standard-of-success-americans-put-debt-free-at-the-top/

Colorado Biz — Americans Redefine Financial Success as Debt-Free Living (November 2025) https://coloradobiz.com/americans-debt-free-financial-success-survey/

CreditOne Bank / Pollfish — For 1 in 3 US Consumers, the New American Dream Is About Debt Freedom (January 2026) https://www.creditonebank.com/articles/for-one-in-three-us-consumers-the-new-american-dream-is-about

Vanguard — Americans Poised for a 'Financial Resolution Rebound' in 2026 (October 2025) https://corporate.vanguard.com/content/corporatesite/us/en/corp/who-we-are/pressroom/press-release-americans-are-poised-for-a-financial-resolution-rebound-in-2026-according-to-vanguard-survey-102925.html

Consumer Financial Protection Bureau — Debt Repayment Strategies and Credit Card Resources https://www.consumerfinance.gov/consumer-tools/credit-cards/

NFCC — National Foundation for Credit Counseling: Free Debt Advice https://www.nfcc.org

Federal Reserve Bank of New York — Consumer Credit Delinquency Data https://www.newyorkfed.org/microeconomics/hhdc

TABLE OF CONTENTS

- The Survey: What the Data Actually Shows

- Why Has This Shift Happened Now?

- The Old Milestones: Marriage, Homeownership, and Status

- The New Definition: What Financial Success Looks Like in 2026

- Financial Stress Is Rising — But So Is Financial Intentionality

- The Cost of Living Is Forcing Consumers to Recalibrate

- Brand Switching and Spending Cuts: The Data on Trade-Downs

- Gen Z Is Rewriting the Rules Entirely

- The Debt Burden: Why It Feels So Heavy Right Now

- Stability as Luxury: The Psychology Behind the Shift

- How to Live Debt-Free: A Practical Framework for 2026

- Conclusion

- Frequently Asked Questions

- References

The Survey: What the Data Actually Shows

In July 2025, KeyBank commissioned Schmidt Market Research to survey 1,004 Americans aged 18 to 70, all of whom have sole or shared responsibility for household financial decisions and maintain a checking or savings account. The resulting KeyBank 2026 Financial Mobility Survey — published in November 2025 under the headline 'Stability Over Status' — is one of the most comprehensive snapshots of American financial attitudes available and its findings are striking.Three in four Americans — precisely 74% — say that being debt-free is an important milestone in their definition of financial success. This figure places debt-free living ahead of other traditional markers of financial achievement in the public consciousness. It is not that Americans have stopped caring about wealth — it is that the definition of what constitutes wealth has been rewritten. Freedom from debt is now seen as a form of financial prosperity in its own right, independent of income level, net worth, or the accumulation of assets.

Simultaneously, the survey found that financial stress has jumped from 50% to 68% of Americans in a single year — a 36% increase that represents one of the sharpest rises in financial anxiety recorded in any major survey in recent years. Yet — and this is the crucial nuance in the data — the majority of financially stressed Americans are not disengaging from financial planning. They are redirecting their energy. One in three (35%) respondents say they feel in control of, or proud of, how they manage their money. The pressure is being converted into purpose rather than paralysis.

The measure of success is not wealth alone, but also the ability to live debt-free and prepare for what's ahead. The financial landscape for Americans is shifting in profound ways.

— DANIEL BROWN, EVP AND DIRECTOR OF CONSUMER PRODUCT MANAGEMENT, KEYBANK (NOVEMBER 2025)

Why Has This Shift Happened Now?

The redefinition of financial success from wealth accumulation to financial stability did not happen overnight. It is the product of several converging forces that have reshaped American household finances over the past five years and fundamentally altered what feels achievable — and what feels desirable.Five years of cumulative inflation

US cumulative CPI inflation since early 2020 is approximately 25%, according to Bureau of Labor Statistics data. The price of essentials — food, housing, energy, insurance — has risen at rates that have outpaced wage growth for many households, permanently increasing the cost of maintaining a standard of living. A household that was financially comfortable in 2019 on the same income in 2025 is meaningfully less comfortable, even if their nominal salary has risen. This compression of real purchasing power has shifted the emotional centre of gravity of financial aspiration: from getting more to losing less, from accumulating assets to eliminating liabilities.Rising interest rates amplifying debt costs

The Federal Reserve raised its federal funds rate from near zero in early 2022 to above 5% by mid-2023 — the fastest rate cycle in four decades. The direct consumer effect was a dramatic increase in the cost of carrying variable-rate debt. Credit card interest rates, which track the federal funds rate with a significant markup, reached average rates of 20% to 22% by 2024. Student loan interest costs resumed after pandemic-era forbearance ended. Home equity lines of credit, which millions of Americans use for home improvements and major expenses, became significantly more expensive. In this environment, carrying debt became materially more painful than it had been in the decade of near-zero rates, and the desire to eliminate it became more intense.The homeownership dream deferred

US home prices rose 53% between 2019 and 2025, while median household incomes rose only 24% over the same period. The median age of a first-time US homebuyer reached a record 40 in 2025. For a generation that was told homeownership was the primary vehicle for building wealth and the central milestone of adult success, its inaccessibility has been a profound psychological disruption. When a traditional aspiration becomes structurally unachievable for a large proportion of the population, aspirations reorganise — and debt-free living fills the vacuum of a milestone that feels genuinely attainable by almost anyone, regardless of income level or housing market conditions.The Old Milestones: Marriage, Homeownership, and StatusFor most of the twentieth century, the American financial success narrative was built around a clear sequence of life milestones: education, employment, marriage, homeownership, children, retirement. This sequence both structured individual financial planning and defined the social meaning of success. Each milestone was simultaneously a financial achievement and a social signal — a house was both shelter and status, a wedding both a relationship and a public declaration of having 'made it.'

The KeyBank data shows this structure unravelling at a remarkable pace. More than half of survey respondents (53%) say that paying for experiences or a certain lifestyle is now less of a priority than one year ago. Thirty-nine per cent say that both buying a home and getting married are less of a priority than one year ago. These are not marginal adjustments — they are significant reorderings of life priority from large proportions of the American adult population.

It would be a mistake to interpret this data as a collapse of aspiration. The same survey found that 55% of Americans still consider homeownership a 'very important' part of their definition of success — indicating that the desire for homeownership has not disappeared, but rather been deferred or deprioritised in the face of affordability barriers. Similarly, the decline in marriage and children as financial priorities likely reflects a combination of cost factors (the average US wedding costs approximately $35,000; the cost of raising a child to 18 is estimated at $300,000 or more) and a genuine reorientation of values rather than a simple abandonment of tradition.

The New Definition: What Financial Success Looks Like in 2026

If the old definition of financial success was 'having things', the new definition is 'not owing things.' This is a profound philosophical inversion. Prosperity used to be measured by what you had accumulated — your home, your car, your investment portfolio, your lifestyle. In 2026, for a growing majority of Americans, prosperity is measured by what you no longer owe — the absence of debt, the presence of a financial buffer, the freedom to make choices without being constrained by monthly minimum payments.The CreditOne Bank/Pollfish survey of 1,000 US adults conducted in December 2025 and published in January 2026 reinforces this picture from a different angle. It found that 33% of US consumers define financial success as being debt-free, regardless of income or assets — placing debt freedom ahead of homeownership, investment growth, and even salary level as the primary marker of success. Notably, 31% of Gen Z respondents in the same survey said financial success means having flexible work and control over their time — suggesting that the new definition of success is not only about debt freedom but about autonomy more broadly.

The Vanguard Consumer Survey published in October 2025 adds a complementary data point: 84% of Americans have a financial resolution for 2026, with building an emergency fund and using a high-yield savings account as the top two goals. These are not aspirational wealth-building objectives. They are defensive resilience goals — the financial equivalent of building a wall against the next shock rather than climbing toward a higher summit. When building an emergency fund becomes the number-one financial aspiration of a majority of Americans, the redefinition of success from status to stability is essentially complete.

Financial Stress Is Rising — But So Is Financial Intentionality

The most counterintuitive finding in the KeyBank survey is the coexistence of rising financial stress with rising financial intentionality. Financial stress jumped from 50% to 68% of Americans in 2024 to 2025 — an 18-percentage-point rise that represents one of the sharpest single-year increases in financial anxiety recorded in any major study. Three in four financially stressed Americans report having less in their savings. Americans' emergency readiness is declining as costs climb.Yet alongside this stress, one in three Americans (35%) say they feel in control of, or proud of, how they manage their money. This is not a contradiction — it is a documented psychological response to financial difficulty. Research in behavioural economics consistently shows that periods of financial constraint, when they do not become overwhelming, often produce more deliberate and disciplined financial behaviour. The restriction of financial slack forces prioritisation; prioritisation produces clarity; clarity produces a sense of agency that coexists with — and in some cases grows out of — genuine financial hardship.

KeyBank's own framing of this dynamic is that Americans are 'turning pressure into purpose.' The survey commentary notes that 'even as 68% of Americans feel financial stress, many are channeling that pressure into purposeful financial planning and long-term resilience.' Contributing to retirement funds (32%) and saying no to plans in order to save money (30%) are identified as the top behaviours that feel most like financial 'adulting' — a term that captures the generational recalibration of what it means to be financially responsible. For many Americans in 2026, financial maturity is no longer defined by the acquisition of status symbols. It is defined by the discipline to build a financial fortress against uncertainty.

The Cost of Living Is Forcing Consumers to Recalibrate

The link between the cost of living crisis and the shift to stability-over-status thinking is direct and evidenced. KeyBank's survey explicitly identifies the rising cost of living and inflation as the primary driver among the 22% of respondents who feel less financially successful than five years ago — cited by 71% of that group. Economic uncertainty is the second factor at 45%, followed by job changes or career burnout at 26%.The mechanism is straightforward: when the cost of essentials rises faster than income, households are forced to eliminate non-essential spending. The goods and experiences that previously served as status signals — restaurant meals, new clothing, upgrades to technology and appliances, premium subscriptions, luxury convenience purchases — are the first categories to be cut. Over time, their absence normalises. The household discovers that their quality of life does not significantly deteriorate without these expenditures, and that the money freed up by eliminating them can be redirected toward debt repayment or savings accumulation with meaningful, visible results. The frugality forced by cost of living pressure becomes internalised as a value.

The KeyBank data shows this dynamic clearly. With a sharp eye on inflation, Americans are making deliberate trade-downs across consumer categories. The survey notes that 'the rising cost of living and increased price of everyday items are putting a strain on wallets across America' — and that households are responding not with despair but with recalibration. As the survey's framing puts it, Americans are strategically recalibrating their entire approach to money, not merely reacting emotionally to pressure.

Brand Switching and Spending Cuts: The Data on Trade-Downs

One of the most visible consumer consequences of the stability-over-status shift is the systematic trade-down across spending categories — from premium to value, from branded to own-brand, from new to secondhand, from experiences to essentials. This behaviour is not unique to the US, but the American data provides a particularly clear picture of the scale and structure of the trade-down.The KeyBank survey identifies that Americans are making deliberate choices to prioritise staples and privacy over perks and popularity — a framing that captures the trade-off between the social signalling value of premium consumption and the financial utility of essentials spending. Consumers who previously defined themselves partly through their brand choices — the coffee shop they frequented, the clothing brands they wore, the restaurants they used — are increasingly separating their identity from their consumption choices.

The CreditOne Bank survey adds important nuance: 22% of respondents making under $50,000 per year say a $1,000 emergency fund would make them feel more financially secure — placing an extremely modest financial buffer as a higher priority than any consumer purchase. When the most psychologically impactful financial improvement available to a significant segment of the population is a thousand-dollar savings buffer, the entire framework of consumer aspiration has shifted away from consumption toward protection.

How the stability-over-status shift is changing consumer behaviour

- Brand switching at scale: Consumers are systematically moving from premium branded products to store-brand or value alternatives across grocery, personal care, household products, and clothing. This is not merely opportunistic discount-seeking — it is a deliberate repriorisation of spending that reflects changed values as much as changed budgets.

- Subscription audit and cancellation: The accumulation of digital subscriptions — streaming, software, delivery, box services — has become one of the highest-visibility targets for household spending reduction. Many households discovering during cost-of-living belt-tightening that they use fewer than half the subscriptions they pay for are cancelling and not re-subscribing.

- Secondhand as primary, not fallback: The growth of platforms including ThredUp, Poshmark, Mercari, and eBay has moved secondhand purchasing from a budget option of last resort to a primary channel for a growing share of Gen Z and Millennial consumers. This shift is partly financial and partly values-driven — circular consumption carries social cachet among younger demographics that premium brand consumption once provided.

- Experience selectivity: Rather than eliminating experiences entirely, consumers are becoming more selective — preserving genuinely high-value experiences (a significant holiday, a concert by a favourite artist, a special occasion meal) while eliminating habitual low-value experiences (routine restaurant meals, impulse entertainment spending, convenience food).

- Debt repayment as conspicuous frugality: Paying down debt has acquired a social status in online personal finance communities that premium consumption previously held. Sharing 'debt-free screams' on YouTube, posting debt payoff progress on Reddit personal finance forums, and celebrating zero-balance milestones on TikTok has created a new form of financial social signalling built around freedom rather than acquisition.

Gen Z Is Rewriting the Rules Entirely

The generational dimension of the stability-over-status shift is most extreme among Gen Z — those born between approximately 1997 and 2012, now aged 14 to 29. The KeyBank data found that only 13% of Gen Z respondents are still pursuing traditional milestones. One-third have decided against buying a home, one-third against getting married, one-third against having children, and one-third against pursuing higher education — all on the grounds that these no longer align with their definition of success.This is a generation that entered adulthood watching its older siblings and Millennial predecessors struggle with student loan debt that took decades to repay, housing markets that had become inaccessible, and an employment landscape disrupted first by the 2008 financial crisis and then by the pandemic and the AI transition. The rational response to this environment — to reject the financial commitments that trapped earlier generations and to build a definition of success around freedom, flexibility, and the absence of debt — is precisely what the data documents.

The CreditOne Bank survey of December 2025 provides an additional Gen Z data point: 31% of Gen Z respondents say financial success means having flexible work and control over their time — placing autonomy ahead of wealth accumulation or any traditional milestone. This finding is consistent with broader generational research showing that Gen Z prioritises work-life integration, purpose alignment, and the ability to control their schedule over traditional metrics of career advancement and salary growth. When combined with the debt-free aspiration (74% overall, likely higher for Gen Z specifically), the emerging Gen Z financial ideal is not poverty or resignation but something more like voluntary simplicity: a deliberate choice to live within means, eliminate debt, and buy back time rather than accumulate assets.

Critically, the KeyBank data notes that 'the kids are alright' — in contrast to Gen X, which the survey identifies as most squeezed and most in need of what the survey describes as a 'financial miracle.' Gen Z's rejection of traditional milestones is not driven by inability but by recalibration: a generation that has calculated the true cost — financial, psychological, and temporal — of chasing traditional success markers and decided the price is too high.

The Debt Burden: Why It Feels So Heavy Right Now

To understand why debt-free living has assumed such psychological and practical significance in 2026, it is necessary to understand the scale and structure of American debt. The Federal Reserve's most recent data shows US consumer debt at approximately $17 trillion — a figure that has grown consistently through the past decade and encompasses mortgage debt, student loans, auto loans, credit card balances, and other personal borrowing.Credit card debt is the category that generates the most acute financial stress in everyday life because it carries the highest interest rates (averaging 20% to 22%) and the smallest required minimum payments relative to total balance — meaning that making only minimum payments on a $10,000 credit card balance at 21% APR will take over 30 years to pay off and cost more in interest than the original principal. The Federal Reserve Bank of New York's consumer credit data showed credit card delinquencies rising through 2024 and into 2025 — indicating that a growing share of American households are struggling to service their existing debt even before factoring in new borrowing.

Student loan debt — approximately $1.7 trillion nationally — resumed regular repayment for millions of borrowers in late 2023 after pandemic-era forbearance, adding hundreds of dollars per month in new mandatory outgoings for millions of households precisely as other costs were rising sharply. For many borrowers, especially those in their late 20s and 30s, the resumption of student loan payments has represented the single largest financial shock of the post-pandemic period.

In this environment, the aspiration to be debt-free is not merely philosophical — it is intensely practical. A household that eliminates $800 per month in credit card and student loan payments has effectively given itself a $800 per month pay rise. The freed cash flow can be redirected to savings, investment, or simply a reduction in the financial anxiety that constrains daily decision-making. The luxury of debt-free living is not the luxury of having things — it is the luxury of options, flexibility, and peace of mind.

Stability as Luxury: The Psychology Behind the Shift

The reframing of stability as luxury rather than limitation is perhaps the most intellectually interesting aspect of the shift documented in the KeyBank survey. In a consumer culture that has historically equated luxury with excess — with having more, spending more, and displaying more — the idea that freedom from financial obligation constitutes a form of luxury represents a genuine inversion of values.This inversion has a strong psychological foundation. Research in wellbeing economics consistently shows that above a certain income threshold (estimated at approximately $75,000 to $100,000 per year in the US), additional income produces diminishing returns on life satisfaction. What does continue to improve life satisfaction at higher income levels is not additional consumption but rather increased control over one's time, reduction in financial anxiety, and the ability to make choices unconstrained by financial necessity. Debt-free living delivers precisely these goods.

The anthropologist David Graeber, in his influential work on debt, observed that debt creates a form of social and psychological dependency that pervades every aspect of the debtor's life — constraining career choices, relationships, and daily behaviour in ways that the debtor often does not fully recognise until the debt is gone. The experience of paying off a significant debt is consistently described by those who have done it not in terms of the financial gain but in terms of the psychological liberation — a lightness, a sense of possibility, and a recovery of agency that is qualitatively different from any consumer experience. This psychological dimension of debt freedom is what makes it genuinely luxury in the original sense: something that provides a quality of life beyond mere material sufficiency.

How to Live Debt-Free: A Practical Framework for 2026

Understanding why debt-free living has become the new luxury is one thing. Achieving it is another. The journey from where most Americans are — carrying multiple forms of debt in an inflationary environment — to genuine debt freedom requires a framework, not just motivation.A practical debt-freedom framework for 2026

- Step 1 — Get a complete picture: List every debt you carry — credit cards, student loans, auto loans, personal loans, medical debt, and any informal borrowing. For each debt record the current balance, interest rate, minimum monthly payment, and lender. Most people who do this for the first time discover one or two items they had partially forgotten or mentally minimised. You cannot plan your way out of debt you are not looking at.

- Step 2 — Build a minimal emergency fund first: Before accelerating debt repayment, build a $1,000 emergency fund (as the CreditOne Bank survey identified as the most impactful financial buffer for lower-income households). Without this buffer, any unexpected expense will force new borrowing, immediately undoing debt repayment progress. Once you have $1,000 in savings, proceed to aggressive debt repayment.

- Step 3 — Choose a debt repayment method and commit: The two most researched methods are the avalanche (pay minimums on all debts, apply every extra dollar to the highest-interest debt first — mathematically optimal) and the snowball (pay minimums on all debts, apply extra to the smallest balance first — behaviourally effective because early wins build motivation). Either method works; the critical variable is sustained commitment rather than method selection.

- Step 4 — Generate extra cash flow: Every dollar of additional cash flow applied to debt repayment accelerates the journey. The most effective sources are: subscription auditing (eliminating unused or low-value subscriptions), dining-out reduction (even two fewer restaurant meals per week frees $150 to $250 per month in many households), and a targeted salary negotiation or side income (see our guide to 15 ways to earn extra money while working full-time). Even $200 per month extra applied to a $10,000 credit card at 21% APR reduces the payoff period from over 30 years to approximately 5 years.

- Step 5 — Cut strategically, not universally: The stability-over-status framework does not mean eliminating all enjoyment. It means being intentional about which spending delivers genuine value and which has become habitual, social, or aspirational spending that does not actually make you happier. Audit each spending category for the value it delivers relative to its cost. The experiences you protect are more meaningful when they are chosen rather than defaulted into.

- Step 6 — Use windfalls wisely: The Vanguard survey found that building an emergency fund is the top financial resolution for 2026. When a bonus, tax refund, or inheritance arrives, the temptation to spend it is strong. The financially transformative choice is almost always to apply at least 50% to high-interest debt repayment and 25% to emergency savings before spending the remainder. A $3,000 tax refund applied to credit card debt can save more in avoided interest over the following 12 months than most people earn from investments.

- Step 7 — Reframe debt payoff as wealth creation: Every dollar of high-interest debt you eliminate is, in financial terms, equivalent to an investment returning 20%+ tax-free. No investment available to most retail investors consistently returns anything close to the interest rate on consumer credit card debt. Paying off a 21% APR credit card is the highest-return investment most Americans can make — and achieving debt freedom is the most reliable path to financial stability, flexibility, and the kind of luxury that money cannot buy: peace of mind.

CONCLUSION

The stability-over-status shift captured in the KeyBank 2026 Financial Mobility Survey is not a trend toward austerity or resignation. It is a generational and cultural recalibration of what prosperity means in an era of sustained cost pressure, elevated debt costs, and inaccessible traditional milestones. When 74% of Americans say debt-free living is the most important milestone in their definition of financial success, they are not saying they have given up on aspiration. They are saying they have changed the object of their aspiration — from having more to owing less, from performing prosperity to experiencing it.This shift has profound implications for consumer behaviour, for the brands and retailers that serve American households, and for the financial system that has historically profited from the normalisation of consumer debt. But its most important implications are personal. For the millions of Americans carrying credit card balances, student loans, and auto debt through an inflationary environment while watching traditional milestones recede into unaffordability, the redefinition of success around debt freedom is not just data — it is permission.

Permission to prioritise financial stability over social performance, to make the deliberate choices that lead to genuine freedom, and to discover that the most meaningful luxury available in 2026 is not what you own but what you no longer owe.

Frequently Asked Questions

What is the source of the 74% debt-free living statistic?

The figure comes from the KeyBank 2026 Financial Mobility Survey, conducted online by Schmidt Market Research in July 2025, polling 1,004 Americans aged 18 to 70. All respondents had sole or shared responsibility for household financial decisions and maintained a checking or savings account. The survey found that approximately 74% to 75% of Americans agree that debt-free living is an important milestone in their definition of financial success. The full executive summary is available at key.com. The survey was widely covered by Money.com, ACA International, Colorado Biz, and other financial publications in November 2025.Is the 'debt-free as new luxury' idea limited to the US?

The KeyBank survey is US-specific, but the underlying dynamic — a shift from status-driven to stability-driven financial aspiration driven by cost of living pressure and elevated debt costs — is visible across multiple international markets. In the UK, YouGov's February 2026 Financial Outlook Survey found that 51% of UK adults now have a budget (up from 38% in 2023), with the primary driver being the desire to ensure essential costs are covered. The UK FinWell Index documents similar patterns of financial anxiety driving more defensive saving and debt reduction behaviour. The debt-free aspiration is characteristically more prominent in the US data, reflecting higher levels of consumer credit card and student loan debt relative to other countries, but the broader trend toward stability over status is visible across most high-income economies.Why has financial stress risen so sharply — from 50% to 68% in a year?

The KeyBank survey does not provide a single explanatory factor for the rise, but the data it presents points to a combination: the resumption of student loan repayments in late 2023 after pandemic-era forbearance, sustained consumer price inflation that has compressed real purchasing power (US cumulative CPI since 2020 is approximately 25%), the higher cost of carrying variable-rate debt following Federal Reserve rate increases (credit card rates averaging 20% to 22% by 2024), and ongoing economic uncertainty. Among the 22% of Americans who feel less financially successful than five years ago, 71% cite rising living costs and inflation as the primary factor, 45% cite economic uncertainty, and 26% cite job changes or career burnout.What does 'financial adulting' mean according to the KeyBank survey?

KeyBank uses the term 'financial adulting' to describe behaviours that Americans — particularly younger adults — associate with genuine financial maturity and responsibility. The survey found that contributing to retirement funds (32%) and saying no to plans in order to save money (30%) are the behaviours most commonly described as feeling like financial adulting. Notably, the traditional markers of adulthood — buying a home, getting married — do not feature prominently. The redefinition of financial maturity around discipline, prioritisation, and long-term planning rather than consumption and milestone accumulation is consistent with the broader stability-over-status shift.What is the best way to start becoming debt-free?

The most evidence-backed starting point is a full debt audit: list every debt you carry, its balance, interest rate, and minimum payment. Then build a minimal $1,000 emergency fund before beginning aggressive repayment, to avoid the cycle of paying down debt only to rebuild it after an unexpected expense. Choose either the avalanche method (highest interest rate first — mathematically optimal) or the snowball method (smallest balance first — behaviourally effective) and apply every available dollar of extra cash flow to the priority debt. Free resources for debt management include the NFCC (nfcc.org) for US households, and the Consumer Financial Protection Bureau (consumerfinance.gov) for education on debt repayment strategies.How is Gen Z's attitude to financial success different from previous generations?

The KeyBank survey found that only 13% of Gen Z respondents are still pursuing traditional milestones — buying a home, getting married, having children, or pursuing higher education. One-third have decided against each of these traditional milestones, saying they no longer align with their definition of success. The CreditOne Bank/Pollfish survey found that 31% of Gen Z define financial success as flexible work and control over time — prioritising autonomy over wealth accumulation. Rather than interpreting this as resignation or lack of ambition, the data suggests a deliberate rejection of financial commitments that previous generations found either trapping or unachievable, in favour of a more autonomous, debt-light approach to adult life.References

KeyBank — 2026 Financial Mobility Survey: Stability Over Status (November 2025) https://www.key.com/content/dam/kco/documents/personal/financial-mobility-survey-2026.pdfYahoo Finance / KeyBank — Is Debt-Free the New Luxury? KeyBank Survey Explores (November 2025) https://finance.yahoo.com/news/debt-free-luxury-keybank-survey-143000264.html

Money.com — For Most Americans, Financial Success Now Means Being Debt-Free (November 2025) https://money.com/americans-define-financial-success/

ACA International — A New Standard of Success: Americans Put 'Debt-Free' at the Top (November 2025) https://www.acainternational.org/news/a-new-standard-of-success-americans-put-debt-free-at-the-top/

Colorado Biz — Americans Redefine Financial Success as Debt-Free Living (November 2025) https://coloradobiz.com/americans-debt-free-financial-success-survey/

CreditOne Bank / Pollfish — For 1 in 3 US Consumers, the New American Dream Is About Debt Freedom (January 2026) https://www.creditonebank.com/articles/for-one-in-three-us-consumers-the-new-american-dream-is-about

Vanguard — Americans Poised for a 'Financial Resolution Rebound' in 2026 (October 2025) https://corporate.vanguard.com/content/corporatesite/us/en/corp/who-we-are/pressroom/press-release-americans-are-poised-for-a-financial-resolution-rebound-in-2026-according-to-vanguard-survey-102925.html

Consumer Financial Protection Bureau — Debt Repayment Strategies and Credit Card Resources https://www.consumerfinance.gov/consumer-tools/credit-cards/

NFCC — National Foundation for Credit Counseling: Free Debt Advice https://www.nfcc.org

Federal Reserve Bank of New York — Consumer Credit Delinquency Data https://www.newyorkfed.org/microeconomics/hhdc

0 Comments Comments