Financial Literacy

How to Build Financial Discipline from Daily Habits

Table of Contents

- The Science of Habit Formation: Why Small Actions Beat Big Resolutions

- The Current State of Financial Discipline: Key Statistics

- 10 Everyday Habits That Build Real Financial Discipline

- Habit 1: Automate a Small, Fixed Transfer the Day You Are Paid

- Habit 2: Spend Five Minutes Each Evening Logging the Day's Purchases

- Habit 3: Hold a Weekly 15-Minute Money Check-In

- Habit 4: Apply a 24-Hour Rule to Any Non-Essential Purchase Over a Set Threshold

- Habit 5: Use Round-Up Savings on Everyday Card Purchases

- Habit 6: Review All Recurring Subscriptions Once a Month

- Habit 7: Name Every Savings Account by Its Purpose

- Habit 8: Pay Yourself First, Then Build Your Spending Plan Around What Remains

- Habit 9: Conduct a Calm, Five-Minute Review After Every Significant Purchase

- Habit 10: Celebrate Small Financial Wins Explicitly

- From Daily Habit to Annual Financial Impact

- Building Your Personal System: Start With One Habit

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Financial discipline is often imagined as a dramatic act of willpower — a New Year's resolution, a strict budget spreadsheet, a complete lifestyle overhaul. In reality, the people who manage money most successfully over the long term rarely rely on willpower at all. They rely on habits: small, repeated, often automatic behaviours that quietly compound into financial stability without requiring constant conscious effort.

This distinction matters enormously, because willpower is a depleting resource. Research in behavioural psychology consistently shows that the motivation driving a strict new budget fades within weeks, which is precisely why so many financial resolutions fail by February. Habits, by contrast, do not require ongoing motivation once established — they become the default, low-effort behaviour, freeing up mental energy for everything else in life. The goal of building financial discipline, properly understood, is not to become a more disciplined person in some abstract sense, but to engineer a small set of everyday behaviours that make good financial decisions the path of least resistance.

This guide explains how habits actually form, why so many financial habits fail despite good intentions, and provides ten specific, everyday habits — each grounded in behavioural research — that compound into genuine financial discipline over time. Rather than offering another generic budgeting framework, this is a practical guide to the small daily and weekly actions that, repeated consistently, reshape your entire financial trajectory.

The Science of Habit Formation: Why Small Actions Beat Big Resolutions

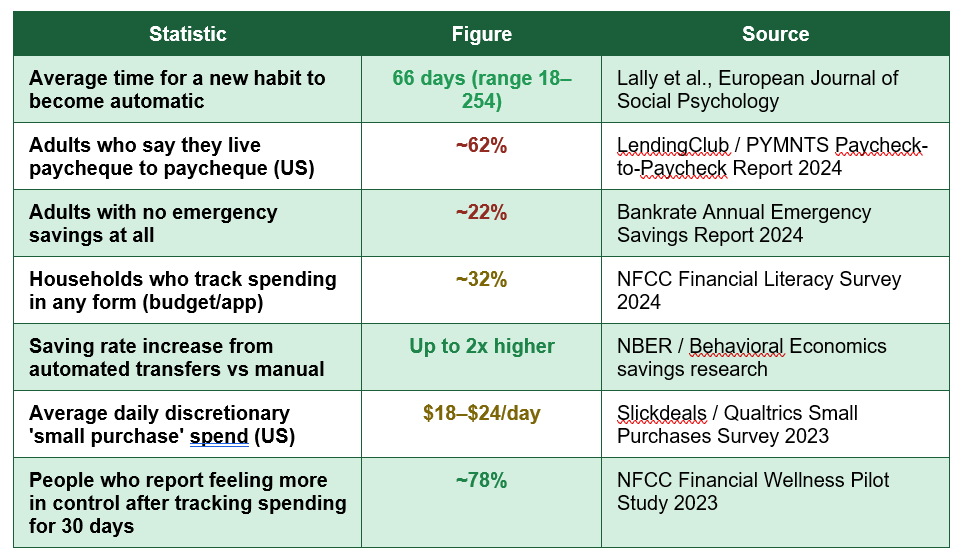

The most widely cited research on habit formation comes from a 2010 study by Dr Phillippa Lally and colleagues at University College London, published in the European Journal of Social Psychology. The study tracked participants attempting to build new habits and found that, on average, a behaviour took 66 days to become automatic — though this varied enormously, from as little as 18 days for simple habits to as long as 254 days for more complex ones.Two findings from this research are particularly relevant to financial habits. First, missing a single day occasionally did not meaningfully disrupt the habit-formation process, which means an occasional lapse in a savings habit or spending review is not a failure that requires starting over — consistency over time matters far more than perfection on any individual day. Second, and more importantly, simpler habits formed faster and more reliably than complex ones. This is the central insight behind why this guide focuses on small, specific, low-friction actions rather than sweeping financial overhauls: a habit that takes thirty seconds is dramatically more likely to survive past the first difficult week than one that requires an hour of effort.

The behavioural economics insight: Behavioural economists Richard Thaler and Cass Sunstein popularised the concept of 'friction' — the small amount of effort required to perform an action. Reducing friction on good financial behaviours (automating a transfer so it requires zero ongoing decisions) and increasing friction on poor ones (removing a saved card from a shopping app so a purchase requires more steps) is consistently more effective than relying on willpower to resist temptation in the moment.

The Current State of Financial Discipline: Key Statistics

The need for genuine, sustainable financial habits is underscored by current data on how most households actually manage money day to day:

Households who actively track spending: Only ~32% — the large majority of adults have no real-time visibility into where their money goes day to day, which is consistently the first habit financial educators recommend building (NFCC 2024)

These figures reveal a clear gap between financial awareness and financial behaviour. Most people know, in principle, that they should save more, track spending, and avoid impulse purchases. The gap lies not in knowledge but in the absence of structures — habits — that make those good intentions automatic rather than dependent on willpower in the moment they are needed most.

10 Everyday Habits That Build Real Financial Discipline

The following habits are deliberately small and specific, in line with the habit-formation research above. Each is something you can begin today, in under five minutes, without requiring a major lifestyle change.Habit 1: Automate a Small, Fixed Transfer the Day You Are Paid

The single most effective financial habit is also the simplest: setting up an automatic transfer of a fixed amount — even as little as $5 or £5 — from your current account to a separate savings account on the day you are paid, before you have a chance to spend it. Research from the National Bureau of Economic Research and multiple behavioural finance studies consistently shows that automated savers accumulate significantly more over time than those who rely on manually transferring leftover money at the end of the month, because there is rarely meaningful money left by the time manual transfers are attempted.The amount matters far less than the consistency and the automation itself. Starting with an amount so small it is barely noticeable removes the resistance that causes people to abandon more ambitious savings plans within the first month, and the amount can be increased gradually as the habit becomes established.

Habit 2: Spend Five Minutes Each Evening Logging the Day's Purchases

A short, consistent daily review of spending — even just noting purchases in a notes app or simple spreadsheet — creates the awareness that almost every other financial habit depends on. This is not the same as detailed budgeting; it is simply the act of seeing, in writing, where money went that day. The Hawthorne effect in behavioural psychology demonstrates that simply observing and recording a behaviour tends to change it, even without any additional rules or restrictions.Habit 3: Hold a Weekly 15-Minute Money Check-In

Once a week, at a consistent time — Sunday evening is popular — spend fifteen minutes reviewing your accounts: checking balances, scanning for unfamiliar transactions, reviewing upcoming bills, and confirming your savings transfer went through. This single weekly ritual catches billing errors, subscription price increases, and spending drift early, before they compound into a larger problem discovered only at month's end.Habit 4: Apply a 24-Hour Rule to Any Non-Essential Purchase Over a Set Threshold

Before making any discretionary purchase above a personal threshold — many people use $50 or £40 — commit to waiting 24 hours before completing the purchase. This brief pause interrupts the impulse-driven, emotionally charged decision-making that drives most regretted purchases, allowing the more rational, deliberate part of the brain to weigh in. Multiple consumer behaviour studies show this single habit reduces impulsive spending by a meaningful margin without requiring any ongoing willpower beyond the initial 24-hour wait.Habit 5: Use Round-Up Savings on Everyday Card Purchases

Many banking apps and fintech services now offer a round-up feature, automatically rounding card purchases up to the nearest pound or dollar and transferring the difference into a savings account. Because the amounts involved are tiny and entirely passive, this habit requires no ongoing decision-making at all once activated, yet it consistently produces a noticeable accumulation of savings over a year purely from spending you were already going to do.Habit 6: Review All Recurring Subscriptions Once a Month

Subscription costs are uniquely prone to invisible creep: free trials convert to paid plans, prices increase with little notice, and services go unused for months after initial enthusiasm fades. A simple monthly habit — reviewing your bank statement specifically for recurring charges — catches this drift before it becomes a meaningful, ongoing drain on your budget.Habit 7: Name Every Savings Account by Its Purpose

Behavioural research on 'mental accounting' shows that money held in an account labelled 'Emergency Fund' or 'House Deposit' is significantly less likely to be spent impulsively than money sitting in a generically named savings account, even though the funds are functionally identical. This simple labelling habit, available in virtually every modern banking app, creates a psychological barrier against casual withdrawal.Habit 8: Pay Yourself First, Then Build Your Spending Plan Around What Remains

Rather than budgeting spending first and hoping something is left to save, reverse the order: treat your savings transfer (Habit 1) as a fixed, non-negotiable expense paid immediately, and build your discretionary spending plan around whatever income remains afterward. This single reframing — savings as a bill you pay yourself, not a leftover — is one of the most consistently cited principles among people who successfully build long-term wealth.Habit 9: Conduct a Calm, Five-Minute Review After Every Significant Purchase

After any purchase above your personal discretionary threshold, take five minutes to reflect, without judgment, on how the purchase felt before, during, and after. This is not about guilt — it is about building the self-awareness that allows you to recognise your own spending patterns and emotional triggers over time, which is essential information for refining the other habits in this list to your specific tendencies.Habit 10: Celebrate Small Financial Wins Explicitly

Habit researchers consistently emphasise the importance of positive reinforcement in sustaining new behaviours. Explicitly acknowledging progress — reaching a savings milestone, completing a month of consistent tracking, paying off a specific debt — reinforces the habit loop and makes continuation more likely than treating financial discipline as a grim, joyless obligation. This does not need to involve spending money; simply noting the achievement and reflecting on the progress made is sufficient.From Daily Habit to Annual Financial Impact

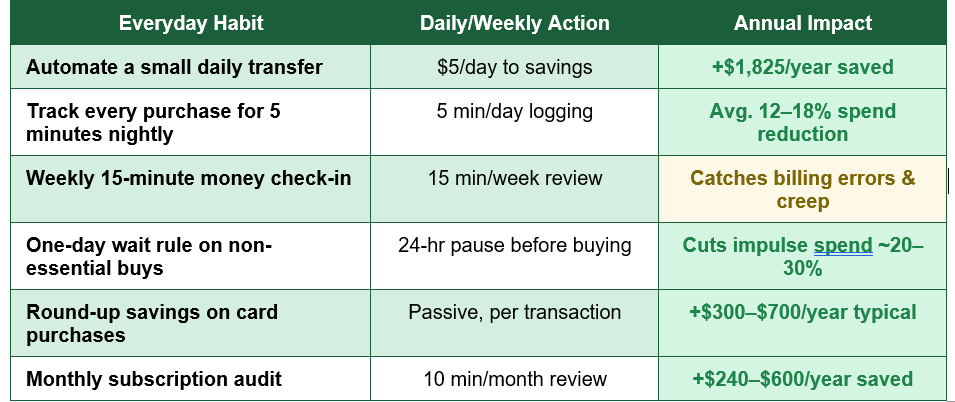

The table below illustrates how several of these everyday habits translate into measurable annual outcomes when applied consistently:

None of these individual habits requires significant time or willpower in isolation — each takes minutes, not hours. Their power lies entirely in compounding consistency: a $5 daily transfer is trivial on any single day but accumulates to $1,825 over a year purely through repetition, while a five-minute nightly spending log, repeated for a year, produces a genuinely transformed level of financial self-awareness that no single budgeting session could replicate.

Building Your Personal System: Start With One Habit

The single most common mistake people make when trying to build financial discipline is attempting to adopt all ten habits simultaneously. Habit-formation research is unambiguous on this point: attempting too many simultaneous behaviour changes significantly reduces the likelihood that any of them stick, because the cumulative willpower demand exceeds what is sustainable.The recommended approach is to choose just one habit from this list — ideally the automated savings transfer (Habit 1), since it requires only a few minutes to set up and then operates entirely without further effort — and commit to it for the first 30 days before introducing a second. Once a habit becomes genuinely automatic, typically somewhere between 18 and 70 days depending on its complexity, it requires no further conscious effort to maintain, freeing up the mental bandwidth to introduce the next habit on the list.

Stacking habits effectively: Behavioural scientist BJ Fogg's research on habit formation recommends 'habit stacking' — attaching a new habit to an existing, already-automatic routine. For example, committing to the five-minute evening spending log immediately after brushing your teeth, or the weekly money check-in immediately after a recurring Sunday activity you already do consistently. Anchoring new financial habits to existing routines significantly increases the likelihood they survive past the first few weeks.

Conclusion

Financial discipline is not a personality trait that some people possess and others lack. It is a set of small, learnable behaviours that, repeated consistently, become automatic — removing the need for the daily willpower that most ambitious financial resolutions ultimately exhaust. The data on habit formation is consistent and encouraging: simple, specific actions form reliably within weeks to a few months, and once established, require little ongoing effort to sustain.The ten habits outlined in this guide — from automating a tiny daily transfer to naming your savings accounts by purpose to celebrating small wins explicitly — are each individually modest. Their combined and compounding effect, sustained over months and years, is what actually produces financial stability and long-term wealth. This is precisely why the people who appear to have remarkable financial discipline rarely describe their approach in terms of willpower or sacrifice; they describe a system of small, automatic behaviours that quietly do the work in the background of an otherwise normal life.

Begin with a single habit today. Choose the one that feels easiest to start, set it up in the next ten minutes if you can, and resist the urge to add several more at once. The financial discipline you are looking to build is not a single decision but the accumulated result of dozens of small, repeated choices — and the earlier you start making them automatic, the sooner they begin compounding in your favour.

Frequently Asked Questions (FAQ)

How long does it actually take to build a new financial habit?

Research from University College London found that habits take an average of 66 days to become automatic, though this ranges from as few as 18 days for very simple behaviours to as many as 254 days for more complex ones. Simple, specific habits — like an automated transfer or a brief daily spending log — tend to form toward the faster end of this range, which is one reason this guide emphasises small, specific actions over broad, complex changes.What if I miss a day or fall off a financial habit?

The same UCL research found that occasional missed days did not meaningfully disrupt the overall habit-formation process, provided the behaviour resumed afterward. This is genuinely useful to know: a missed weekly check-in or a skipped daily log does not mean starting over from zero. Consistency over weeks and months matters far more than unbroken daily perfection, and treating an occasional lapse as a minor setback rather than a failure significantly improves the odds of the habit ultimately sticking.Should I start with budgeting or with these smaller habits?

For most people, starting with one or two small, automatic habits — particularly the automated savings transfer and the daily spending log — is more sustainable than attempting a comprehensive budget immediately. A budget requires ongoing decisions and categorisation that can feel burdensome before the underlying habits of awareness and automatic saving are established. Many people find that after a few months of consistent small habits, building a more detailed budget becomes considerably easier, because they already have the spending visibility and savings momentum a budget depends on.Are financial habit-tracking apps worth using?

For many people, yes — apps that automatically categorise spending, send round-up savings, or send weekly summary notifications can meaningfully reduce the friction involved in maintaining habits like spending tracking and review. However, the underlying behaviour matters more than the specific tool. A simple notes app or paper notebook used consistently is more effective than a sophisticated app used inconsistently. Choose whichever tool you are most likely to actually use every day or week.Can these habits work even on a very tight budget with little to save?

Yes — and arguably they matter most in this situation. The habits in this guide are deliberately designed to work at any income level, because they emphasise consistency and automation over the absolute amount involved. A $1 or £1 daily automated transfer, a free spending-tracking app, and a 24-hour pause before non-essential purchases cost nothing to implement and build the awareness and momentum that make larger financial improvements possible once income increases or expenses decrease. Financial discipline built through habits is accessible regardless of current financial circumstances.External References

The following authoritative sources informed this article and are recommended for further reading:1. Lally, P. et al. — How Are Habits Formed: Modelling Habit Formation in the Real World (European Journal of Social Psychology)

https://onlinelibrary.wiley.com/doi/10.1002/ejsp.674

2. National Foundation for Credit Counselling (NFCC) — Financial Literacy and Spending Tracking Survey 2024

https://www.nfcc.org/

3. Bankrate — Annual Emergency Savings Report 2024

https://www.bankrate.com/banking/savings/emergency-savings-report/

4. LendingClub / PYMNTS — Paycheck-to-Paycheck Consumer Report 2024

https://www.pymnts.com/study/paycheck-to-paycheck-living-consumer-finance/

5. National Bureau of Economic Research (NBER) — Behavioural Research on Automated Savings

https://www.nber.org/topics/household-finance

6. Thaler, R. & Sunstein, C. — Nudge: Improving Decisions About Health, Wealth, and Happiness (Overview)

https://www.penguinrandomhouse.com/books/184879/nudge-by-richard-h-thaler-and-cass-r-sunstein/

7. Consumer Financial Protection Bureau — Building Healthy Financial Habits

https://www.consumerfinance.gov/consumer-tools/educator-tools/youth-financial-education/teach/

8. BJ Fogg — Tiny Habits: The Small Changes That Change Everything (Behaviour Model Overview)

https://tinyhabits.com/

0 Comments Comments