Emotional Development

How to Manage Mental Health and Debt

Table of Contents

- Why These Two Problems Must Be Addressed Together

- The Evidence: How Debt and Mental Health Are Linked

- Understanding the Cycle: How Debt and Mental Health Reinforce Each Other

- How Debt Damages Mental Health

- How Mental Health Problems Lead to Debt

- When Mental Health Makes Managing Debt Feel Impossible: Immediate Steps

- Where to Get Help: Free Support Services for Debt and Mental Health

- Managing Your Mental Health While Dealing with Debt

- NHS Talking Therapies (Free, Self-Referral)

- Structured Daily Routine and Financial Windowing

- Using Your Rights as a Vulnerable Customer

- The Mental Health and Money Advice Service

- If You Are Supporting Someone Else With Debt and Mental Health Difficulties

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why These Two Problems Must Be Addressed Together

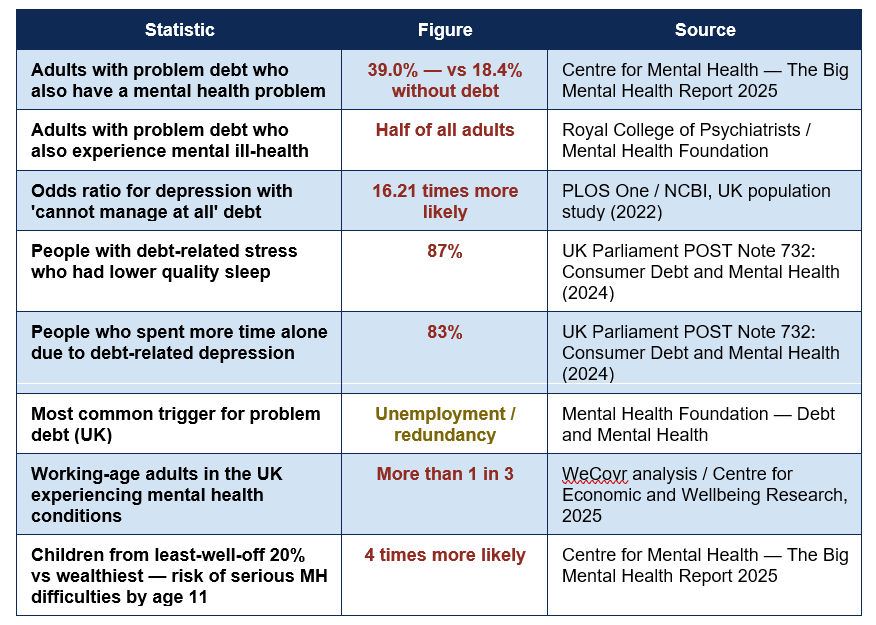

If you are struggling with debt and your mental health at the same time, you are not unusual and you are not weak. The Royal College of Psychiatrists' research, cited by the Mental Health Foundation, found that half of all adults with a debt problem also experience mental ill-health. The Centre for Mental Health's Big Mental Health Report 2025 — the most comprehensive audit of mental health in the UK in recent years — found that people in problem debt are more than twice as likely to experience a mental health problem (39.0%) compared with those without debt problems (18.4%). The relationship between financial difficulty and psychological distress is one of the most consistently documented findings in mental health research.What makes this relationship so important to understand is that it runs in both directions. Debt causes mental health problems — the constant stress of unmanageable bills, the shame and isolation, the fear of the letterbox and the phone ringing, the sleepless nights. And mental health problems cause debt — conditions like depression impair the ability to open letters, make decisions, and manage finances; anxiety can make calling a creditor feel impossible; bipolar disorder can lead to impulsive spending during elevated mood episodes. The UK Parliament's POST Note 732 on Consumer Debt and Mental Health (2024) documented that 87% of people stressed about payday loans had lower quality sleep, 83% spent more time alone, and 62% drank more alcohol as a result of that stress.

This guide addresses both sides of the cycle simultaneously, because treating them separately is part of what keeps people stuck. It covers the evidence on how debt and mental health interact, the practical steps to stabilise your financial situation even when your mental health is fragile, the UK support services that address both together, what to do when mental health makes managing debt feel impossible, and the rights you have as someone whose mental health affects your ability to deal with creditors. There is a way through. Most people who find it find it because they reached out for help — and this guide tells you exactly where to reach.

The Evidence: How Debt and Mental Health Are Linked

The data connecting debt and mental health is substantial, consistent across multiple research methodologies, and growing. The following table brings together the key statistics:

The dose-response relationship: The worse the debt, the worse the mental health impact — 16x more likely for depression at extreme debt stress — a UK population study published in PLOS One found a dose-response relationship between debt severity and depression: the odds ratio for depression rose from 2.80 at 'some problems' to 16.21 at 'cannot manage at all' — one of the strongest associations recorded between an environmental stressor and depression in peer-reviewed research.

Understanding the Cycle: How Debt and Mental Health Reinforce Each Other

The Money and Mental Health Policy Institute — the leading UK research organisation dedicated specifically to the intersection of financial difficulty and psychological wellbeing — describes a vicious cycle in which debt and mental health problems mutually worsen each other. Understanding how this cycle operates is the first step toward breaking it, because the cycle has multiple entry points and exit points.How Debt Damages Mental Health

The psychological mechanisms through which debt harms mental health are well-documented. Financial stress keeps the nervous system in a sustained state of heightened alert — the cortisol response that is appropriate for short-term danger becomes chronic when the stressor never resolves. This chronic stress manifests as difficulty concentrating, disrupted sleep, physical symptoms (headaches, digestive problems), emotional volatility, and over time, depression and anxiety as persistent conditions rather than temporary responses.The social dimension of debt compounds the psychological harm. Debt in the UK carries significant stigma, leading many people to conceal it from family and friends, creating isolation precisely when social support is most needed. UK Debt Service's analysis confirms that debt affects mental health through feelings of guilt and shame, reduced self-esteem, and social withdrawal — not just through the practical stress of managing bills. Parliamentary research found 83% of people experiencing debt-related distress were spending more time alone as a consequence.

How Mental Health Problems Lead to Debt

The reverse path — from mental health to debt — is equally well-documented and equally important to recognise, because it challenges the harmful narrative that people in debt are there due to irresponsibility. The Mental Health Foundation explicitly addresses this: 'There is a common misunderstanding that people find themselves in debt due to living an excessive lifestyle or going wild in the aisles with credit cards. The truth is that unemployment and redundancy are the most common triggers for debt problems and can happen to anyone.'Mental health conditions impair financial management in specific, predictable ways. Depression reduces motivation and cognitive function, making it harder to open and respond to letters, track spending, or make calls to creditors. Anxiety — particularly health anxiety or general anxiety disorder — can make dealing with financial correspondence feel genuinely threatening, leading to avoidance that allows small debts to become large ones through missed payments and accumulating interest. Bipolar disorder's manic or hypomanic phases can involve impulsive or elevated spending. ADHD is associated with difficulties in financial planning and impulse control. The person who appears to be 'burying their head in the sand' may be paralysed by mental health symptoms rather than acting irresponsibly.

The Debt and Mental Health Evidence Form (DMHEF): If your mental health is affecting your ability to manage your finances, you can ask a healthcare professional — your GP, psychiatrist, or community mental health worker — to complete a Debt and Mental Health Evidence Form on your behalf. This standardised form (available at moneyhealthindex.org.uk/dmhef) allows creditors to adjust how they contact you, pause collections for a period, and in some cases write off debts entirely. Many people with serious mental health conditions qualify for significant creditor forbearance that they never access because they do not know the form exists.

When Mental Health Makes Managing Debt Feel Impossible: Immediate Steps

If your mental health is making it difficult to engage with your finances at all, the most important thing to know is that you do not have to sort everything out at once. The advice that applies to people managing debt from a position of emotional stability — make a comprehensive list of all debts, contact every creditor, create a budget — can feel overwhelming and counterproductive when anxiety or depression is active. The steps below are designed for the hardest moments, when small is everything:- Open and sort the post: If unopened letters have been accumulating, you do not need to deal with their contents today. You need to sort them into two piles: things with a recent date (last two weeks) and older items. Set the older items aside. Opening and sorting without reading in detail is a manageable first step that breaks the avoidance cycle without overwhelming you.

- Tell one person: Debt thrives in secrecy. Telling one trusted person — a partner, a friend, a family member — about the situation reduces the isolation that compounds both the debt problem and the mental health impact. You do not need to share the full details. 'I am struggling with money and it is affecting how I feel' is enough to begin.

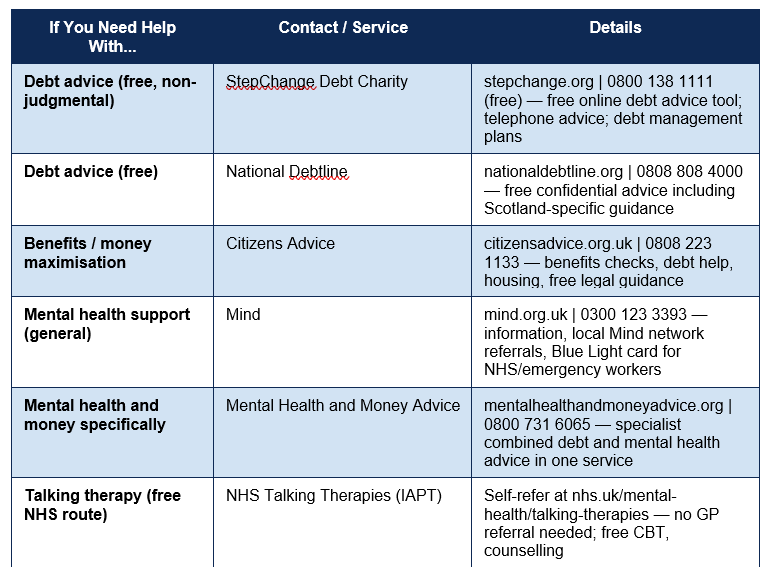

- Contact one service: You do not need to contact all your creditors, make a budget, and arrange a debt management plan in one day. You need to contact one service. StepChange (stepchange.org or 0800 138 1111) and National Debtline (nationaldebtline.org or 0808 808 4000) both offer free, non-judgmental advice. Both have trained to understand the mental health dimension of debt. Both can take over the creditor communication on your behalf once you have spoken with them, removing the source of your most acute anxiety.

- Let creditors know your situation: You are not required to explain your mental health situation in detail to a creditor. You are entitled to say: 'I am experiencing health difficulties that are affecting my ability to manage my finances right now. I need some time before I can discuss my account.' Most creditors — under FCA regulations and their obligations as regulated businesses — must treat vulnerable customers with appropriate care and flexibility. They cannot legally pressure you when you have flagged a vulnerability.

- Apply for a Breathing Space: The UK's Breathing Space scheme (Debt Respite Scheme) provides a legally enforced 60-day pause on most debt collection activity — creditors cannot contact you, add charges, or take enforcement action during this period. If you are receiving mental health crisis treatment, a Mental Health Crisis Breathing Space can last for the duration of your treatment plus 30 days. Apply through a free debt adviser (StepChange, Citizens Advice, or National Debtline).

Where to Get Help: Free Support Services for Debt and Mental Health

The table below provides every key support service available in the UK in 2026, covering both debt and mental health, including the specialist combined services most people never know exist:

BREATHING SPACE — your legal right to pause: If you are overwhelmed by debt, you have a legal right to apply for a Breathing Space — 60 days during which creditors cannot contact you, add interest, or take enforcement action. This is not just a courtesy; it is a statutory protection. Apply through StepChange, National Debtline, or Citizens Advice. For those receiving mental health crisis treatment, the Mental Health Crisis Breathing Space lasts for the full duration of treatment plus 30 days. This is one of the most powerful and least-used financial protections in the UK.

Managing Your Mental Health While Dealing with Debt

The steps above address the debt side of the cycle. The mental health side requires its own attention — not as a separate project to be tackled once the debt is sorted, but simultaneously, because your mental health capacity is the very resource that debt management requires. The following approaches are evidence-based and accessible, designed for people whose mental bandwidth is already stretched:NHS Talking Therapies (Free, Self-Referral)

NHS Talking Therapies — formerly the Improving Access to Psychological Therapies (IAPT) programme — provides free Cognitive Behavioural Therapy (CBT), counselling, and other psychological therapies through the NHS without a GP referral. You can self-refer at any NHS Talking Therapies service in England. Waiting lists exist, but assessment can often be accessed within a few weeks and the initial contact itself — making the call or filling in the form — is a meaningful first step. CBT is specifically effective for the anxiety and avoidance patterns that are central to the debt-mental health cycle.Structured Daily Routine and Financial Windowing

One of the most consistently recommended approaches from both debt advisers and mental health practitioners for people managing both simultaneously is 'financial windowing' — setting aside a specific, limited time period (perhaps 20 minutes on a Tuesday morning) to deal with financial matters, and giving yourself explicit permission to close that window and not engage with financial stress outside it. This technique, drawn from CBT principles for worry management, addresses the tendency for financial anxiety to flood every waking moment. It is not about avoiding the problem — it is about making the engagement bounded and manageable rather than omnipresent.Using Your Rights as a Vulnerable Customer

Under the Financial Conduct Authority's Consumer Duty and its guidance on vulnerable customers, regulated creditors — banks, credit card companies, mortgage lenders, energy suppliers — are required to provide appropriate support to customers with mental health vulnerabilities. This includes: communicating in ways that are accessible and not distressing; providing additional processing time before taking enforcement action; not repeatedly calling at times or in ways that cause distress; and considering debt write-off in extreme circumstances. The FCA's definition of vulnerability explicitly includes mental health conditions. You are entitled to flag your situation and ask for adjusted treatment — this is a regulatory obligation, not a favour.The Mental Health and Money Advice Service

The Mental Health and Money Advice service (mentalhealthandmoneyadvice.org, 0800 731 6065) is one of the UK's most underused support resources — a specialist service that provides combined financial and mental health advice in a single contact, specifically designed for people who are dealing with both simultaneously. Unlike a debt charity or a mental health service separately, this service understands the interaction between the two and can help with both the practical financial steps and the psychological barriers that make those steps difficult.If You Are Supporting Someone Else With Debt and Mental Health Difficulties

Supporting someone who is struggling with both debt and mental health is one of the most challenging caring roles there is, partly because the two conditions reinforce each other in ways that can make progress feel invisible. Several principles are worth holding onto:- Do not take over without permission: The impulse to solve the problem by opening the post, calling the creditors, and organising the finances yourself is understandable. But taking away someone's agency over their own financial situation can reinforce feelings of shame and helplessness. Offer to sit with them while they open post, offer to make the call alongside them, offer to drive them to Citizens Advice. Support their agency rather than replacing it.

- Focus on one step at a time: The goal is not to resolve all the debts immediately. The goal is the next smallest step. Celebrating the completion of that step — opening one letter, making one call, completing one form — is not minimising the problem; it is building the psychological momentum that makes the next step possible.

- Take care of your own mental health: Caring for someone with combined debt and mental health difficulties is emotionally draining. Carers UK (carersuk.org) and Mind both offer support for people in caring roles. Seeking support for yourself is not an indulgence — it is what makes sustained support of another person possible.

Conclusion

The connection between debt and mental health is not a coincidence or a character failing — it is a well-documented, bidirectional relationship that affects half of all UK adults with problem debt. The Centre for Mental Health's 2025 data shows that people in problem debt are more than twice as likely to experience a mental health problem. The parliamentary research shows that 87% experience disrupted sleep and 83% spend more time alone. The PLOS One population study found a dose-response relationship so strong that unmanageable debt produces odds of depression more than 16 times higher than manageable debt. This is a public health issue, not a personal failure.Breaking the cycle requires action on both sides simultaneously — addressing the debt and supporting the mental health together, rather than waiting for one to improve before tackling the other. The UK has, in 2026, a better set of services for doing this than at any previous point. StepChange and National Debtline provide free, expert debt advice that takes the mental health dimension seriously. The Breathing Space scheme provides a statutory 60-day pause on debt collection for anyone who needs it. NHS Talking Therapies provides free psychological support without a GP referral. The Mental Health and Money Advice service specifically addresses both in the same conversation. The Debt and Mental Health Evidence Form can unlock creditor forbearance that most people never access.

If you are reading this guide because you are struggling with both debt and your mental health, the most important message is this: reaching out is the hardest part, and you have already begun by being here. You do not need to have everything organised before you call StepChange or self-refer to NHS Talking Therapies. You do not need to have all the debt figures ready before you call Citizens Advice. The services listed in this guide are specifically designed to meet people at the beginning, not after they have already sorted everything out. Call one number today. That is the only step that matters right now.

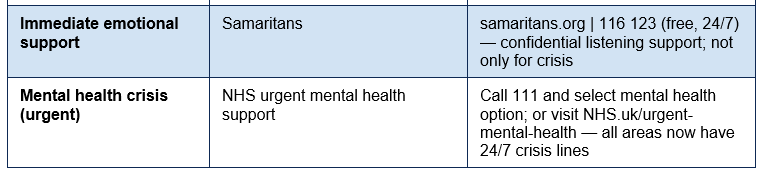

IF YOU ARE IN CRISIS RIGHT NOW: Samaritans: 116 123 (free, 24/7, not only for suicidal thoughts — for any time you need to talk). NHS urgent mental health: call 111 and select mental health. Crisis text line: text SHOUT to 85258. You are not alone. Help is available and it is free.

Frequently Asked Questions (FAQ)

Can debt really cause depression and anxiety?

Yes — the evidence is consistent and substantial. The Centre for Mental Health's Big Mental Health Report 2025 found that people in problem debt are more than twice as likely to experience a mental health problem compared with those who are not in debt. A peer-reviewed UK population study published in PLOS One found a dose-response relationship between debt severity and depression, with the most severe debt situations producing odds of depression 16 times higher than in the general population. The relationship is causal in both directions: debt causes mental health problems, and mental health problems cause debt. If you are experiencing anxiety or depression alongside financial difficulties, these are not separate problems — they are related and both deserve attention.What is Breathing Space and how do I apply?

Breathing Space is a UK statutory scheme (the Debt Respite Scheme) that provides a legally enforced pause on most debt collection activity for 60 days. During Breathing Space, your creditors cannot contact you, add interest or charges, or take enforcement action. A standard Breathing Space lasts 60 days. A Mental Health Crisis Breathing Space — for people who are receiving mental health crisis treatment — lasts for the full duration of treatment plus 30 days. To apply, contact a free debt adviser such as StepChange (stepchange.org or 0800 138 1111), National Debtline (0808 808 4000), or Citizens Advice (0808 223 1133). You cannot apply directly — it must be done through a registered debt adviser.What is the Debt and Mental Health Evidence Form?

The Debt and Mental Health Evidence Form (DMHEF) is a standardised document that a healthcare professional — your GP, community psychiatric nurse, social worker, or mental health worker — can complete to explain to your creditors how your mental health condition affects your ability to manage your finances. Creditors who receive this form are required by FCA guidance and the Lending Standards Board's standards to adjust how they deal with your account — this may include pausing contact, stopping enforcement, adjusting payment arrangements, and in some cases considering debt write-off. The form is available at moneyhealthindex.org.uk/dmhef. You can ask your GP or mental health professional to complete it at any appointment.I can't face opening my post or calling anyone. What can I do right now?

You can start with the smallest possible action. StepChange's online debt advice tool at stepchange.org allows you to begin exploring your options without speaking to anyone — it takes about 20 minutes and gives you a personalised plan at the end. You can also use the webchat service on the Citizens Advice website. If even that feels too much today, try one thing: find one piece of post from the last two weeks and open it. Put it face down without reading it if that is as far as you can get. The act of opening is the beginning of engagement, and it is enough for today. The cycle of debt and mental health is broken by small actions, not by resolving everything at once.How do I access free mental health support without waiting months?

NHS Talking Therapies allows self-referral — you do not need a GP referral. Go to nhs.uk/mental-health/talking-therapies, find your local service by postcode, and self-refer online or by phone. Assessment appointments are often available faster than therapy itself. Mind (0300 123 3393) can refer you to local services. The Samaritans (116 123) are available 24/7 for anyone who needs to talk, not only for crisis situations. The Mental Health and Money Advice service (0800 731 6065) provides combined financial and mental health support and does not have the same waiting lists as NHS therapy services. If you are in mental health crisis, call NHS 111 and select the mental health option — all areas in England now have 24/7 crisis lines accessible through this route.External References & Further Reading

The following authoritative sources were used in researching this article and are recommended for further reading and support:1. Centre for Mental Health — The Big Mental Health Report 2025

https://www.centreformentalhealth.org.uk/publications/the-big-mental-health-report-2025/

2. Mental Health Foundation — Debt and Mental Health

https://www.mentalhealth.org.uk/explore-mental-health/a-z-topics/debt-and-mental-health

3. PLOS One — Perceived Manageability of Debt and Mental Health (UK Population Study)

https://journals.plos.org/plosone/article?id=10.1371%2Fjournal.pone.0274052

4. UK Parliament POST Note 732 — Consumer Debt and Mental Health (2024)

https://researchbriefings.files.parliament.uk/documents/POST-PN-0732/POST-PN-0732.pdf

5. StepChange Debt Charity — Free Debt Advice and Breathing Space Applications

https://www.stepchange.org/

6. Mental Health and Money Advice Service — Combined Debt and Mental Health Support

https://www.mentalhealthandmoneyadvice.org/

7. NHS Talking Therapies — Free Self-Referral to Psychological Therapies

https://www.nhs.uk/mental-health/talking-therapies-medicine-treatments/talking-therapies-and-counselling/nhs-talking-therapies/

8. Money and Mental Health Policy Institute — Research and Resources

https://www.moneyandmentalhealth.org/

0 Comments Comments