Professional & Career Development

Nail UK & US Accounting Interviews: FRS 102 & GAAP Guide

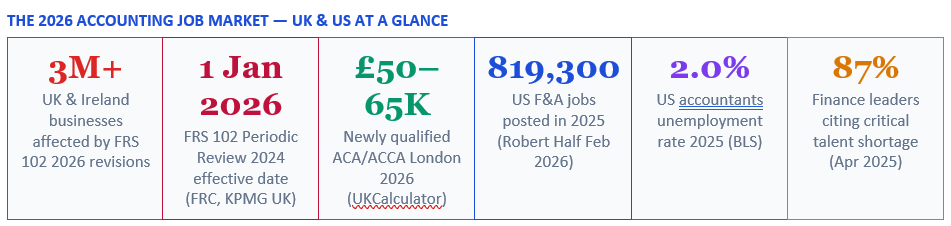

The accounting job market in 2026 has never offered more opportunity — or demanded more technical precision. The UK and Ireland are in the middle of the most significant rewrite of FRS 102 since the standard launched in 2013: revised revenue recognition and lease accounting rules are effective for periods beginning 1 January 2026, affecting over three million businesses. On the US side, hiring managers post 819,300 finance and accounting jobs in 2025 while reporting a 2.0% unemployment rate for accountants and 87% citing a critical talent shortage. Whether you are interviewing for a role in London, Manchester, New York, or Chicago, this guide gives you a step-by-step system to walk into your interview technically prepared, commercially confident, and ready to discuss the exact standards your prospective employer is navigating right now.

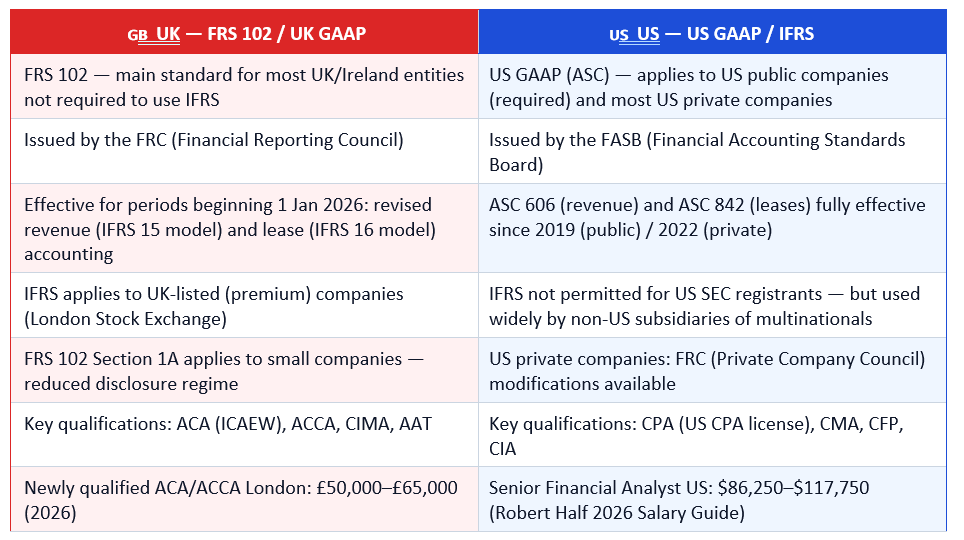

In the UK, the Financial Reporting Council's Periodic Review 2024 has introduced mandatory changes to FRS 102 that are effective for accounting periods beginning on or after 1 January 2026. These changes — summarised by KPMG UK (July 2025) and BDO (February 2026) — bring revenue recognition in line with the IFRS 15 five-step model and introduce IFRS 16-style on-balance-sheet lease accounting for all lessees. Grant Thornton estimates that over three million businesses in the UK and Ireland are affected. For any UK accounting interview in 2026, the ability to discuss these changes concisely and accurately will set you apart.

In the US, the core standards (ASC 606 for revenue, ASC 842 for leases, ASC 326 for credit losses) are now fully embedded in practice, and interviewers at all levels expect candidates to be fluent in them. Simultaneously, Robert Half's February 2026 hiring trends data shows that US employers posted 819,300 finance and accounting jobs in 2025 — with demand highest for candidates who combine technical GAAP knowledge with data analytics, FP&A skills, and technology adaptability. IFRS is also increasingly tested in US interviews, particularly for multinationals, Big 4 advisory roles, and any company with significant international operations.

Sources: ICAEW FRS 102 hub · KPMG UK (2025) · BDO UK (February 2026) · FASB.org · Robert Half 2026 Salary Guide · UKCalculator (March 2026).

The STAR method (Situation → Task → Action → Result) structures your answer to ensure it is specific, concrete, and outcomes-focused. Every STAR answer should use 'I' rather than 'we' when describing your specific actions — interviewers are assessing your individual contribution, not your team's. Results should be quantified wherever possible: percentage improvements, amounts of money, time savings, error rates.

In my previous role as a financial accountant at a mid-sized UK manufacturing company (preparing accounts under FRS 102), I was reviewing the draft year-end accounts before submission when I noticed that the lease on our main production facility — a 7-year operating lease — had not been assessed for the impact of the revised FRS 102 Section 20. The company had early-adopted the 2026 amendments, but this lease had been omitted from the transition workings. I quantified the impact: the ROU asset and corresponding lease liability were each approximately £2.1 million — a material amount relative to our total assets of £18 million. I prepared a technical memo outlining the requirement, the quantum, the journal entries needed, and the disclosure implications. I presented this to the Finance Director and the external auditor within 24 hours of identifying it. The correction was made before the financial statements were signed. I also updated our lease register to include all leases, created a checklist for future period transitions, and scheduled a briefing for the broader finance team on the new lease accounting requirements. The auditors cited our proactive identification in their management letter as a positive point. The experience reinforced for me the importance of maintaining a thorough understanding of current standards and reviewing accounting changes systematically — not just for the accounts in front of you.

UK Sources: Learnsignal ACCA Salary Guide (May 2026) · Leapscholar (April 2026) · UKCalculator (March 2026) · Get Recruited London Salary Survey (December 2025). US Sources: Robert Half 2026 Salary Guide · Workday 2026 Accounting Salary Guide.

In both markets, always counter the first offer — at least once, professionally. Use the benchmark data above as your anchor. In the UK, the Get Recruited London salary survey (December 2025) notes that under-benchmarking and hiring delays are the two most common causes of failed hires — which means employers are aware that their offers must be competitive.

The step-by-step system in this guide — researching the jurisdiction and employer, mastering FRS 102's 2026 changes (UK) and ASC standards (US), practising model answers to the most technically demanding questions, demonstrating technology literacy, answering behavioural questions with specific quantified STAR examples, asking intelligent questions about the employer's current challenges, and negotiating salary with current benchmark data — gives you everything you need to walk into any accounting interview in either market with confidence. The candidates who get hired are not the ones who know the most — they are the ones who prepare the most specifically and apply what they know most clearly.

ICAEW — Changes to UK GAAP: FRC Periodic Review 2024 (Official) https://www.icaew.com/technical/corporate-reporting/uk-gaap/changes-to-uk-gaap

KPMG UK — Upcoming Changes to FRS 102: Revenue and Lease Accounting (July 2025) https://kpmg.com/uk/en/insights/finance/upcoming-changes-frs.html

BDO UK — UK GAAP Changes to FRS 102: Periodic Review 2024 (February 2026) https://www.bdo.co.uk/en-gb/insights/audit-and-assurance/uk-gaap-and-narrative-reporting/uk-gaap-changes-to-financial-reporting-standards-frs-102

Grant Thornton — FRS 102 Updates: Key Changes Affecting UK & Irish Entities (2026) https://www.grantthorntonni.com/insights/frs-102-updates-accounting-standards/

RSM UK — UK GAAP: Preparing for Change (FRC Periodic Review 2024) https://www.rsmuk.com/insights/bridging-the-gaap/uk-gaap-preparing-for-change

House of Control — Revised FRS 102 vs Pre-2026 FRS 102: What Changes (December 2025) https://www.houseofcontrol.com/blog/revised-frs-102-vs-the-pre-2026-frs-102-and-older-uk-gaap

FinQuery — FRS 102 Changes: UK GAAP & IFRS Alignment Guide (February 2026) https://finquery.com/blog/frs-102-changes/

Robert Half — 2026 Finance and Accounting: In-Demand Roles and Salary Data https://www.roberthalf.com/us/en/insights/research/data-reveals-which-finance-and-accounting-roles-are-in-highest-demand

Learnsignal — ACCA Salary Guide 2026: What Can You Earn After Qualifying? (May 2026) https://www.learnsignal.com/blog/acca-qualifications-salary-what-you-earn-after-passing-the-acca/

UKCalculator — Accountant Salary UK 2026: Take-Home Pay (March 2026) https://ukcalculator.com/accountant-salary-calculator.html

TABLE OF CONTENTS

- Why This Interview Is Different in 2026: UK and US Standards in Flux

- Understanding the Frameworks: FRS 102, UK GAAP, US GAAP, and IFRS

- Step 1: Research the Role, Jurisdiction, and Employer Context

- Step 2: Master UK GAAP (FRS 102) — What the 2026 Changes Mean for Your Interview

- Step 3: Master US GAAP and IFRS — Core Technical Areas for US Roles

- Step 4: Practise the Most Common UK and US Accounting Interview Questions

- Step 5: Demonstrate Technology, AI Literacy, and Systems Knowledge

- Step 6: Nail the Behavioural Round with the STAR Method

- Step 7: Ask Intelligent Questions and Navigate Salary Negotiation in Both Markets

- Common Mistakes That Cost Accounting Candidates the Offer

- Conclusion

- Frequently Asked Questions

- References

Why This Interview Is Different in 2026: UK and US Standards in Flux

Accounting job interviews in 2026 are being reshaped by two simultaneous forces: the most significant overhaul of UK GAAP since FRS 102 launched in 2013, and an ongoing transformation of the US accounting role driven by AI, data analytics, and regulatory complexity. Candidates who walk into an interview able to discuss these developments specifically — and who demonstrate a command of the exact standards their prospective employer is navigating — have a decisive advantage over those who can only recite textbook definitions.In the UK, the Financial Reporting Council's Periodic Review 2024 has introduced mandatory changes to FRS 102 that are effective for accounting periods beginning on or after 1 January 2026. These changes — summarised by KPMG UK (July 2025) and BDO (February 2026) — bring revenue recognition in line with the IFRS 15 five-step model and introduce IFRS 16-style on-balance-sheet lease accounting for all lessees. Grant Thornton estimates that over three million businesses in the UK and Ireland are affected. For any UK accounting interview in 2026, the ability to discuss these changes concisely and accurately will set you apart.

In the US, the core standards (ASC 606 for revenue, ASC 842 for leases, ASC 326 for credit losses) are now fully embedded in practice, and interviewers at all levels expect candidates to be fluent in them. Simultaneously, Robert Half's February 2026 hiring trends data shows that US employers posted 819,300 finance and accounting jobs in 2025 — with demand highest for candidates who combine technical GAAP knowledge with data analytics, FP&A skills, and technology adaptability. IFRS is also increasingly tested in US interviews, particularly for multinationals, Big 4 advisory roles, and any company with significant international operations.

Understanding the Frameworks: FRS 102, UK GAAP, US GAAP, and IFRS

Before any interview, you need to know clearly which framework applies to the employer — and what the key distinctions between frameworks are. This determines which technical questions you will face and which standards you must be able to discuss with confidence.Sources: ICAEW FRS 102 hub · KPMG UK (2025) · BDO UK (February 2026) · FASB.org · Robert Half 2026 Salary Guide · UKCalculator (March 2026).

Research the Role, Jurisdiction, and Employer Context

Preparation for an accounting interview begins four to five days before the interview — not the night before. The most decisive differentiator between candidates who advance and those who do not is the specificity and depth of their pre-interview research. Finance and accounting interviewers at every level respect candidates who have done the work.For UK roles — what to research

- Establish which reporting framework the employer uses: FRS 102 (the default for most private UK companies), IFRS (if listed on the LSE's premium market or part of a listed group), or FRS 105 (micro-entities). This determines the technical questions you will face and the vocabulary you should use.

- Review the employer's most recent filed accounts at Companies House. Read the accounting policies section — it reveals which elections and estimates management has made (depreciation methods, revenue recognition judgements, lease classifications pre-2026). In 2026 interviews, being able to ask or comment on how the employer is transitioning to the new FRS 102 lease and revenue standards is a high-impact differentiator.

- Understand the FRC Periodic Review 2024 changes at a headline level: revenue recognition now follows the IFRS 15 five-step model; leases are now on-balance-sheet for lessees (ROU asset and lease liability). These changes affect reported EBITDA, net debt, loan covenants, and remuneration schemes — knowing this positions you as commercially aware, not just technically knowledgeable.

- Research the sector: does the employer operate in a sector with specific revenue recognition complexity (long-term contracts in construction, licences in technology, bundled deals in telecoms, variable pricing in professional services)? The FRS 102 revenue changes hit different sectors differently — showing sector-specific awareness is powerful.

For US roles — what to research

- Identify the employer's reporting requirements: SEC registrant (public company, must use US GAAP) vs private company (may use US GAAP, FRS, or modified GAAP). Multinational employers may also expect IFRS knowledge for consolidation, statutory reporting, or advisory work.

- Review the 10-K or 10-Q (public companies) on the SEC EDGAR database. Read the Critical Accounting Estimates section — this reveals the management judgements where interviewers are most likely to probe you (goodwill impairment, revenue recognition judgements, lease term estimates, credit loss provisions under ASC 326).

- Know the employer's industry: ASC 606 has specific implementation guidance for different sectors. Software and SaaS companies (performance obligations, licences, variable consideration), construction (over-time revenue recognition), and retail (loyalty programmes, right of return) all have distinct revenue recognition complexities. Demonstrating industry-specific ASC 606 awareness is a high-value signal.

Master UK GAAP (FRS 102) — What the 2026 Changes Mean for Your Interview

The Periodic Review 2024 amendments to FRS 102, published by the FRC on 27 March 2024 and effective for periods beginning 1 January 2026, represent the most far-reaching changes to UK GAAP since the standard was introduced. Every UK accounting interview in 2026 will touch on these changes — because every UK employer is living through them right now.Revenue recognition — the new five-step model under revised FRS 102 Section 23

The pre-2026 FRS 102 revenue model was based on the transfer of risks and rewards, similar to the old IAS 18. The revised Section 23, effective 1 January 2026, replaces this with a framework closely aligned to IFRS 15 — recognising revenue when control of goods or services transfers to the customer, using a five-step model:- • Step 1: Identify the contract with the customer — the agreement creates enforceable rights and obligations, has commercial substance, and collection is probable.

- • Step 2: Identify the performance obligations — each distinct good or service (capable of being distinct AND distinct in the context of the contract) is a separate performance obligation.

- Step 3: Determine the transaction price — including variable consideration (constrained by probability of no significant revenue reversal), non-cash consideration, and consideration payable to customers.

- Step 4: Allocate the transaction price to performance obligations — based on relative standalone selling prices.

- Step 5: Recognise revenue when each performance obligation is satisfied — at a point in time (customer obtains control) or over time (continuous transfer criteria met).

Lease accounting — on-balance-sheet for lessees under revised FRS 102 Section 20

The pre-2026 FRS 102 distinguished between finance leases (on-balance-sheet) and operating leases (expensed as incurred). The Periodic Review 2024 eliminates this distinction for lessees, adopting the IFRS 16 on-balance-sheet model. From 1 January 2026, most lessees must recognise a right-of-use (ROU) asset and a corresponding lease liability for virtually all leases — including what were previously operating leases.- Financial statement impact: total assets and total liabilities increase; lease charges shift from operating expenses to depreciation (in operating expenses) plus interest (below the EBITDA line). EBITDA often improves because the lease cost moves out of EBITDA.

- Covenant implications: net debt ratios increase (lease liabilities are now debt); loan covenants referencing debt/EBITDA or interest cover may be triggered. In interviews, the ability to explain this implication shows commercial awareness beyond pure accounting.

- Practical exemptions retained in FRS 102 (vs IFRS 16): short-term leases (12 months or less) and low-value asset leases may still be expensed — a simplification not available under IFRS 16 in the same form.

UK ACCOUNTING INTERVIEW — MODEL Q&A (FRS 102 2026)

🇬🇧 UK / FRS 102 What are the most significant changes to FRS 102 effective from 1 January 2026, and how would they affect the financial statements of a company with a significant lease portfolio and long-term contracts?

✦ MODEL ANSWER

The two principal changes are to revenue recognition (Section 23) and lease accounting (Section 20). Revenue under revised Section 23 now follows a five-step, control-based model broadly aligned with IFRS 15, replacing the risks-and-rewards approach. For a company with long-term contracts, this may shift the timing of revenue recognition depending on whether the performance obligations are satisfied over time or at a point in time. Bundled contracts must now be disaggregated into separate performance obligations, which can affect both the timing and amount of recognised revenue. For a company with a significant lease portfolio, the revised Section 20 brings most leases onto the balance sheet as right-of-use assets and lease liabilities — eliminating the operating lease off-balance-sheet treatment. This increases both reported assets and liabilities; EBITDA typically improves because what was previously an operating lease charge moves below the EBITDA line as depreciation and interest. However, net debt increases, which can put pressure on loan covenants referencing leverage ratios. Disclosures expand significantly, and the transition requires systems changes to track lease data. Early preparation and impact assessment are essential for a smooth 1 January 2026 adoption.🇬🇧 UK / FRS 102 Under the revised FRS 102 Section 23, how would you account for a three-year software licence bundled with implementation services and an annual support contract?

✦ MODEL ANSWER

This is a multi-element arrangement requiring performance obligation identification. Step 1: identify the contract — confirmed once terms are agreed and collection is probable. Step 2: identify performance obligations — the three distinct elements are: (i) the software licence, (ii) the implementation service, and (iii) the annual support. Each must be assessed for distinctness: can the customer benefit from it independently? Is it distinct in the context of the contract? If the software cannot function without the implementation, they may be combined into a single performance obligation. If distinct, each is a separate PO. Step 3: determine the transaction price — allocate the total contract value to each PO based on relative standalone selling prices. Step 4-5: recognise revenue when (or as) each PO is satisfied — the licence typically at a point in time (when control transfers), implementation over time as the service is rendered, and support ratably over the 12-month period. The shift from the pre-2026 approach (which might have recognised all consideration over the contract term) can significantly front-load or back-load revenue compared to the old model.Master US GAAP and IFRS — Core Technical Areas for US Roles

US accounting interviews in 2026 test candidates on a mature set of standards that have been fully effective for several years. Interviewers expect fluency — not just familiarity — with ASC 606, ASC 842, ASC 326, ASC 350 (goodwill), and ASC 740 (income taxes). IFRS knowledge is additionally expected for any role in a multinational, Big 4, or cross-border advisory context.Key US GAAP areas most frequently tested in 2026

- • ASC 606 — Revenue from Contracts with Customers: the same five-step model as IFRS 15, but implemented under ASC nomenclature. Focus areas in interviews: variable consideration, contract modifications, principal vs agent assessment, licences (functional vs symbolic IP), and costs to obtain/fulfil a contract.

- • ASC 842 — Leases: all operating leases (with term 12 months) now on the balance sheet as ROU assets and operating lease liabilities. Finance leases recognised similarly to capital leases. Key interview topics: the operating vs finance lease classification tests, the incremental borrowing rate determination, and practical expedients (short-term lease exemption, combining lease and non-lease components).

- • ASC 326 — CECL (Current Expected Credit Losses): replaced the incurred loss model with a forward-looking expected credit loss model, requiring entities to estimate lifetime credit losses from origination. Key interview topics: the CECL model mechanics for trade receivables (simplified approach using a provision matrix), how forward-looking information (macroeconomic forecasts) is incorporated, and the difference from the IAS 39 incurred loss model.

- • ASC 350 — Goodwill and Intangibles: goodwill is not amortised (public companies) but tested for impairment annually at the reporting unit level. Private companies may elect to amortise goodwill over 10 years (Private Company Council alternative). Single-step qualitative option 'Step 0' before quantitative impairment test.

- • ASC 740 — Income Taxes: deferred tax assets and liabilities, the valuation allowance, uncertain tax positions (FIN 48 / ASC 740-10), and the recognition threshold ('more likely than not' to be sustained upon examination).

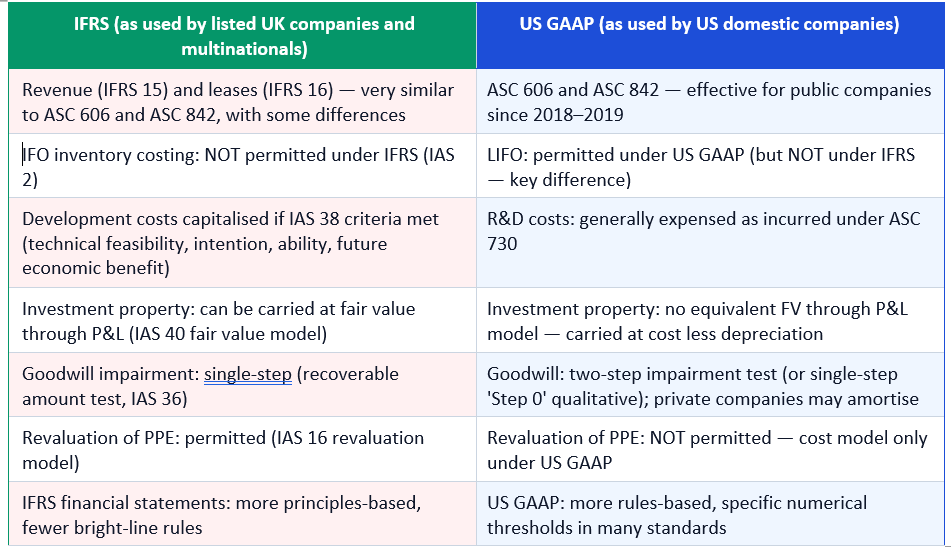

IFRS vs US GAAP — key differences interviewers test

US ACCOUNTING INTERVIEW — MODEL Q&A (US GAAP & IFRS)

🇺🇸 US GAAP Walk me through the key differences between ASC 842 lease accounting and the previous operating lease treatment under ASC 840, and why the change matters to financial statement analysis.

✦ MODEL ANSWER

Under ASC 840 (superseded), operating leases were disclosed in footnotes only — kept entirely off the balance sheet. Rent expense was recognised on a straight-line basis in operating expenses with no balance sheet impact. Under ASC 842, lessees must recognise a right-of-use (ROU) asset and a corresponding operating lease liability for leases with terms exceeding 12 months. The ROU asset is the present value of lease payments, adjusted for initial direct costs and lease incentives. For financial statement users and interviewers, the key implications are: (1) total assets and total liabilities increase — a company's leverage ratios change; (2) for operating leases, both the asset and liability are recognised but P&L treatment is unchanged (still straight-line rent expense — the 'operating lease cost'); (3) for finance leases, depreciation and interest are recognised separately, front-loading the P&L charge in early periods. From an analytical perspective, comparing companies across ASC 840 and ASC 842 periods requires adjustment. EBITDA is largely unchanged for operating leases (unlike IFRS 16 where EBITDA improves), which is a key difference between US GAAP and IFRS 16 lease accounting.🇺🇸 US GAAP / IFRS Why is LIFO inventory costing permitted under US GAAP but prohibited under IFRS, and what are the financial statement implications of the difference?

✦ MODEL ANSWER

LIFO (Last-In, First-Out) is permitted under US GAAP because the FASB has historically allowed it as a conservative, tax-efficient choice for companies in an inflationary environment — in rising price conditions, LIFO results in higher COGS (most recently purchased, higher-cost items recognised first), lower taxable income, and lower reported inventory (balance sheet reflects older, lower-cost items). The LIFO reserve (the difference between LIFO and FIFO inventory) is typically disclosed in the footnotes. IFRS (IAS 2) prohibits LIFO explicitly because it produces a balance sheet inventory value that does not represent current cost and therefore reduces comparability across periods and between entities. The IASB takes the view that inventory should reflect a reasonable approximation of current cost. For financial analysis and interviews: when comparing a US GAAP LIFO company with an IFRS FIFO company, analysts must add back the LIFO reserve to bring the LIFO company's inventory to a FIFO basis for comparability. This also affects gross margin: the LIFO company reports lower gross profit in inflationary periods, which can make it appear less profitable than an IFRS peer using FIFO. Understanding this distinction — and its financial statement implications — is a direct signal of your analytical depth.Demonstrate Technology, AI Literacy, and Systems Knowledge

In both the UK and US accounting job markets, technology capability is an increasingly non-negotiable requirement. Robert Half's 2026 Salary Guide and Addison Group's Workforce Planning Guide both identify AI literacy, data analytics, and automation skills as the top differentiators between strong and exceptional candidates. Roth Staffing's Q1 2026 hiring trends analysis notes that 39% of CFOs rank accelerating AI use in the finance function among their top five priorities, per Gartner's August 2025 survey.Technology and tools interviewers expect you to discuss — UK and US roles

- Excel (advanced): VLOOKUP, INDEX/MATCH, XLOOKUP, SUMIFS, COUNTIFS, pivot tables, Power Query, and basic macros are the baseline expectation for all accounting roles above entry level in both markets.

- ERP systems: SAP (most common in large corporates), Oracle, NetSuite, Sage (common in UK SMEs), Xero (popular in UK practice), and QuickBooks (US SMEs). Know the financial close and reporting workflows of at least one system.

- FRS 102 lease and revenue transition tools (UK): lease management software (Netgain, LeaseQuery, CoStar) is specifically relevant in 2026 as employers are actively managing the FRS 102 Section 20 and Section 23 transition. Awareness of how these tools track ROU assets and lease liabilities signals timely practical knowledge.

- Power BI and Tableau: data visualisation is increasingly expected for management accountant, FP&A, and financial controller roles. Being able to describe a dashboard you have built — even a simple one — is a differentiator.

- AI tools: generative AI (GPT-assisted analysis, variance commentary, report drafting), anomaly detection, and predictive cash flow modelling are emerging areas. Demonstrating awareness and openness to adoption is sufficient — you are not expected to be an AI engineer.

- Audit and assurance tools (UK/US): Caseware, IDEA, ACL/Galvanize — relevant for audit, internal audit, and compliance roles in both markets.

Nail the Behavioural Round with the STAR Method

Technical knowledge gets you into the shortlist. Behavioural evidence gets you the offer. Accounting interviewers — particularly at senior levels — want to know that you can exercise judgement, communicate clearly, handle pressure, and maintain ethical standards. These qualities are assessed through behavioural questions using real examples from your past.The STAR method (Situation → Task → Action → Result) structures your answer to ensure it is specific, concrete, and outcomes-focused. Every STAR answer should use 'I' rather than 'we' when describing your specific actions — interviewers are assessing your individual contribution, not your team's. Results should be quantified wherever possible: percentage improvements, amounts of money, time savings, error rates.

BEHAVIOURAL QUESTION — UK & US MODEL ANSWER

🌐 UK & US Describe a time when you identified a material accounting error or a risk to the integrity of the financial statements, and what you did about it.

✦ MODEL ANSWERIn my previous role as a financial accountant at a mid-sized UK manufacturing company (preparing accounts under FRS 102), I was reviewing the draft year-end accounts before submission when I noticed that the lease on our main production facility — a 7-year operating lease — had not been assessed for the impact of the revised FRS 102 Section 20. The company had early-adopted the 2026 amendments, but this lease had been omitted from the transition workings. I quantified the impact: the ROU asset and corresponding lease liability were each approximately £2.1 million — a material amount relative to our total assets of £18 million. I prepared a technical memo outlining the requirement, the quantum, the journal entries needed, and the disclosure implications. I presented this to the Finance Director and the external auditor within 24 hours of identifying it. The correction was made before the financial statements were signed. I also updated our lease register to include all leases, created a checklist for future period transitions, and scheduled a briefing for the broader finance team on the new lease accounting requirements. The auditors cited our proactive identification in their management letter as a positive point. The experience reinforced for me the importance of maintaining a thorough understanding of current standards and reviewing accounting changes systematically — not just for the accounts in front of you.

Ask Intelligent Questions and Navigate Salary Negotiation in Both Markets

The questions you ask at the end of an accounting interview are as revealing as your answers. In a 2026 market where both the UK and US are navigating significant accounting standard transitions, intelligent questions about how the employer is managing these changes — specifically the FRS 102 2026 transition (UK) or ASC adoption challenges (US) — signal a technically engaged candidate who is thinking about the job they are about to do.Five high-impact questions to ask in UK accounting interviews

- 'Has the business begun transitioning to the revised FRS 102 lease and revenue recognition standards effective 1 January 2026? What are the biggest implementation challenges the finance team is working through?' — shows you understand the current technical landscape and that you are ready to contribute immediately.

- 'What accounting framework does the company use — FRS 102, IFRS, or FRS 105? Is there any consideration of switching to IFRS given the closer alignment of the revised FRS 102?' — demonstrates awareness of the convergence and its strategic implications.

- 'What does your monthly or quarterly close process look like, and are there any areas where the team is looking to improve efficiency or leverage technology?' — shows process improvement mindset.

Five high-impact questions to ask in US accounting interviews

- 'How is the team managing any ongoing ASC 326 CECL implementation challenges, particularly around macroeconomic assumptions for credit loss estimates?' — specific and current.

- 'Does the company have international operations that require IFRS-to-US GAAP or US GAAP-to-IFRS conversions? How is that managed within the team?' — signals global awareness.

- 'What is the technology roadmap for the finance function — are there plans to upgrade the ERP system or implement any AI-assisted analytical tools?' — shows technology orientation.

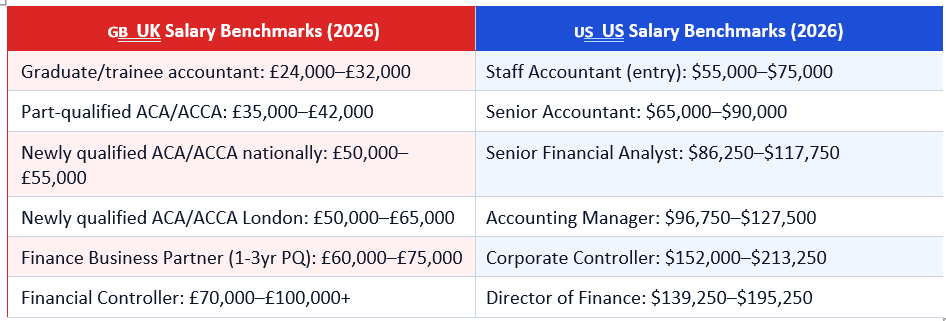

Salary benchmarks — UK and US (2026)

UK Sources: Learnsignal ACCA Salary Guide (May 2026) · Leapscholar (April 2026) · UKCalculator (March 2026) · Get Recruited London Salary Survey (December 2025). US Sources: Robert Half 2026 Salary Guide · Workday 2026 Accounting Salary Guide.

In both markets, always counter the first offer — at least once, professionally. Use the benchmark data above as your anchor. In the UK, the Get Recruited London salary survey (December 2025) notes that under-benchmarking and hiring delays are the two most common causes of failed hires — which means employers are aware that their offers must be competitive.

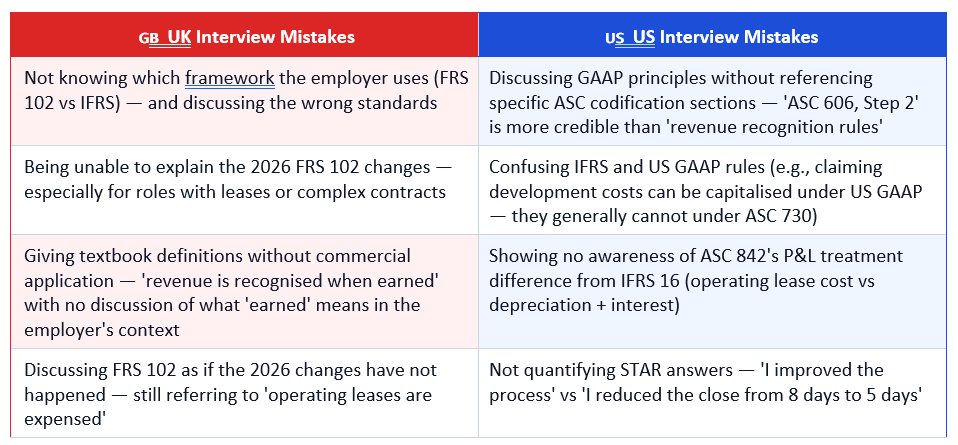

Common Mistakes That Cost Accounting Candidates the Offer

Both UK and US accounting interviews are lost most often to preparation failures — not technical inadequacy. These are the patterns seen most consistently by recruiters and hiring managers in both markets.CONCLUSION

The accounting job market in 2026 is characterised by extraordinary opportunity and correspondingly high expectations. In the UK, the Periodic Review 2024 amendments to FRS 102 — effective 1 January 2026 — are reshaping how over three million businesses recognise revenue and account for leases. Every UK accounting interview in 2026 will involve some discussion of these changes. In the US, the core standards (ASC 606, ASC 842, ASC 326) are fully embedded, the talent shortage is acute, and demand is highest for professionals who combine technical fluency with commercial awareness, data literacy, and technology adaptability.The step-by-step system in this guide — researching the jurisdiction and employer, mastering FRS 102's 2026 changes (UK) and ASC standards (US), practising model answers to the most technically demanding questions, demonstrating technology literacy, answering behavioural questions with specific quantified STAR examples, asking intelligent questions about the employer's current challenges, and negotiating salary with current benchmark data — gives you everything you need to walk into any accounting interview in either market with confidence. The candidates who get hired are not the ones who know the most — they are the ones who prepare the most specifically and apply what they know most clearly.

Frequently Asked Questions

What are the most important FRS 102 changes to know for a UK accounting interview in 2026?

The two most important changes are to revenue recognition (Section 23) and lease accounting (Section 20), both effective for periods beginning 1 January 2026. Revenue now follows a five-step, control-based model broadly aligned with IFRS 15, replacing the risks-and-rewards approach. Lessees must recognise ROU assets and lease liabilities for virtually all leases, eliminating the distinction between operating and finance leases and ending the off-balance-sheet treatment of operating leases. These changes affect reported EBITDA, net debt, leverage ratios, and loan covenants. The FRC published the Periodic Review 2024 amendments on 27 March 2024 (effective 1 January 2026, per KPMG UK). Grant Thornton (2026) estimates over three million UK and Irish businesses are affected. Being able to discuss these two changes with specific financial statement impact examples — even briefly — will immediately distinguish you from candidates who have not updated their technical knowledge.What are the key differences between UK GAAP (FRS 102) and IFRS that I should know for interviews?

The most frequently tested UK GAAP vs IFRS differences in accounting interviews are: (1) Scope: FRS 102 applies to most private UK/Irish entities; IFRS applies to UK-listed companies and is used by many multinationals. (2) Revenue recognition: after the 2026 amendments, both use a five-step model broadly aligned with IFRS 15, but FRS 102 retains some simplifications. (3) Leases: after the 2026 amendments, both bring leases on-balance-sheet, but FRS 102 retains some practical exemptions not available under IFRS 16. (4) Investment property: IFRS (IAS 40) permits a fair value model through P&L; FRS 102 does not have an equivalent model. (5) Financial instrument impairment: IFRS 9 requires the Expected Credit Loss (ECL) model; the FRC chose NOT to align FRS 102 with IFRS 9 ECL in the Periodic Review 2024 — FRS 102 retains a simpler impairment model (RSM UK 2026). This is a specific point of difference interviewers test in credit/banking contexts.What are the most important US GAAP areas for accounting interviews in 2026?

The five most consistently tested US GAAP areas in 2026 accounting interviews are: ASC 606 (Revenue from Contracts with Customers) — five-step model, variable consideration, licences, principal vs agent; ASC 842 (Leases) — operating vs finance lease classification, ROU asset and liability measurement, P&L impact (straight-line for operating leases vs depreciation + interest for finance leases); ASC 326 (CECL) — forward-looking expected credit loss model for financial assets, provision matrix for trade receivables, contrast with IAS 39 incurred loss; ASC 350 (Goodwill and Intangibles) — annual impairment test at reporting unit level, qualitative 'Step 0' assessment, private company amortisation election; and ASC 740 (Income Taxes) — deferred tax, valuation allowance, uncertain tax positions. IFRS knowledge is additionally expected for multinational or Big 4 roles — key additional areas: IAS 2 (LIFO prohibition), IAS 38 (development cost capitalisation), and IAS 36 (goodwill impairment — recoverable amount model vs US GAAP fair value approach).How do salary expectations differ between UK and US accounting roles in 2026?

UK salary benchmarks (2026, national averages, excluding London premium): graduate/trainee accountant £24,000–£32,000; part-qualified ACA/ACCA £35,000–£42,000; newly qualified £50,000–£55,000 nationally; newly qualified in London £50,000–£65,000 (UKCalculator, March 2026); finance business partner (1–3 years PQ) £60,000–£75,000; financial controller £70,000–£100,000+. The IFA (February 2026) notes Hays UK Salary Survey data showing accounting salaries grew by an average of 2.2% in 2025, below inflation of approximately 3.0%. US salary benchmarks (2026 national averages): staff accountant $55,000–$75,000; senior accountant $65,000–$90,000; senior financial analyst $86,250–$117,750; accounting manager $96,750–$127,500; corporate controller $152,000–$213,250; director of finance $139,250–$195,250 (Robert Half 2026 Salary Guide). In both markets, professional qualification (ACA, ACCA, CIMA in the UK; CPA, CMA in the US) commands a meaningful premium over non-qualified candidates at every level.Should I reference both US GAAP and IFRS if I am applying for a UK role?

It depends on the employer. For a private UK company using FRS 102, focus on FRS 102 and its 2026 changes — interviewers at SMEs and mid-market companies will be more impressed by specific FRS 102 knowledge than by general IFRS fluency. For a UK-listed company or the UK subsidiary of a global group, IFRS knowledge is directly relevant and should be discussed alongside FRS 102 awareness. For Big 4 or Top 10 accounting practice roles, both are expected — you will encounter clients under both frameworks. In either case, demonstrating awareness of the convergence between FRS 102 and IFRS (the 2026 revisions specifically close many of the gaps) shows a sophisticated understanding of the UK GAAP landscape that the average candidate does not have.References

ICAEW — FRS 102 The Financial Reporting Standard: Guidance Hub (Official) https://www.icaew.com/technical/corporate-reporting/uk-gaap/frs-102-the-financial-reporting-standardICAEW — Changes to UK GAAP: FRC Periodic Review 2024 (Official) https://www.icaew.com/technical/corporate-reporting/uk-gaap/changes-to-uk-gaap

KPMG UK — Upcoming Changes to FRS 102: Revenue and Lease Accounting (July 2025) https://kpmg.com/uk/en/insights/finance/upcoming-changes-frs.html

BDO UK — UK GAAP Changes to FRS 102: Periodic Review 2024 (February 2026) https://www.bdo.co.uk/en-gb/insights/audit-and-assurance/uk-gaap-and-narrative-reporting/uk-gaap-changes-to-financial-reporting-standards-frs-102

Grant Thornton — FRS 102 Updates: Key Changes Affecting UK & Irish Entities (2026) https://www.grantthorntonni.com/insights/frs-102-updates-accounting-standards/

RSM UK — UK GAAP: Preparing for Change (FRC Periodic Review 2024) https://www.rsmuk.com/insights/bridging-the-gaap/uk-gaap-preparing-for-change

House of Control — Revised FRS 102 vs Pre-2026 FRS 102: What Changes (December 2025) https://www.houseofcontrol.com/blog/revised-frs-102-vs-the-pre-2026-frs-102-and-older-uk-gaap

FinQuery — FRS 102 Changes: UK GAAP & IFRS Alignment Guide (February 2026) https://finquery.com/blog/frs-102-changes/

Robert Half — 2026 Finance and Accounting: In-Demand Roles and Salary Data https://www.roberthalf.com/us/en/insights/research/data-reveals-which-finance-and-accounting-roles-are-in-highest-demand

Learnsignal — ACCA Salary Guide 2026: What Can You Earn After Qualifying? (May 2026) https://www.learnsignal.com/blog/acca-qualifications-salary-what-you-earn-after-passing-the-acca/

UKCalculator — Accountant Salary UK 2026: Take-Home Pay (March 2026) https://ukcalculator.com/accountant-salary-calculator.html

0 Comments Comments