Retirement

Three Quarters of UK Workers Not on Track for Pension

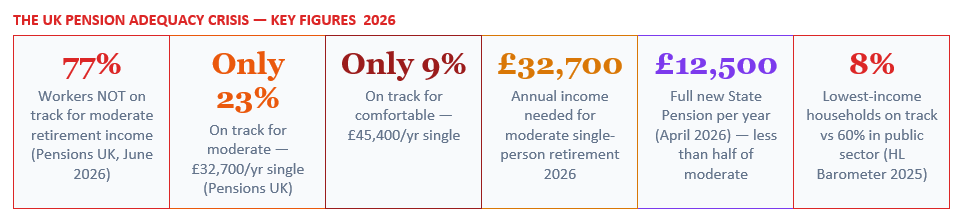

More than three quarters of UK workers are heading toward a sharp cliff-edge drop in income when they retire, a landmark new report by Pensions UK has warned. Only 23% of the working population are currently on course to achieve what the industry defines as a 'moderate' standard of living in retirement — requiring £32,700 a year for a single person. Just 9% are on track for a 'comfortable' retirement. Rising living costs, inadequate auto-enrolment contributions, a widening gap for the self-employed, and deep inequalities across income groups and renters vs homeowners are all combining to create what Pensions UK describes as an impending national retirement income crisis. This article explains what the data means, why so many people are falling short, who is most at risk, and — critically — what practical steps anyone can take right now to improve their retirement outlook.

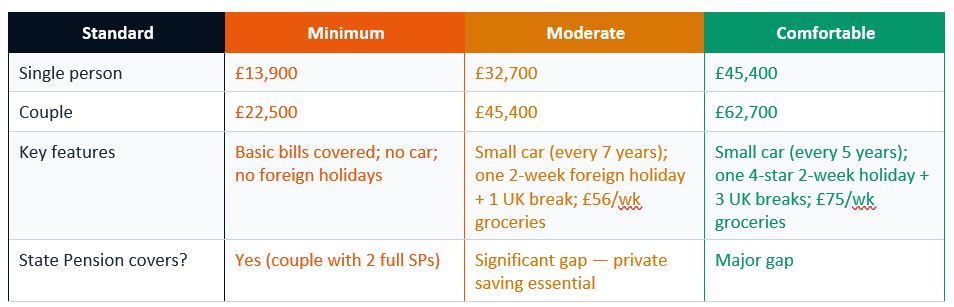

When Pensions UK warns that three quarters of workers are not on track for a 'moderate' retirement income, the word moderate deserves unpacking — because what the pensions industry means by it is more aspirational than the word implies. The Retirement Living Standards (RLS), developed independently by the Centre for Research in Social Policy at Loughborough University and published by Pensions UK, define three standards of retirement living: minimum, moderate, and comfortable. Each represents a realistic, evidence-based budget covering everyday spending across housing, food, transport, leisure, and social activities.

A moderate retirement lifestyle in 2026 is described by Pensions UK as one involving spending £56 a week on groceries, running a small car replaced every seven years, taking a three-star two-week foreign holiday plus one long weekend break in the UK per year, and having enough for some social activities, home improvements, and clothing. This is not a life of luxury — it is recognisably comfortable in the conventional sense, but decidedly unremarkable by the standards of working life for most British employees. The report estimates this costs £32,700 per year for a single person and £45,400 for a couple.

Too many people face a cliff-edge drop in income when they retire — and without action from government, employers, and savers, millions risk finding that the standard of living they worked decades to achieve disappears overnight.

— PENSIONS UK — RETIREMENT LIVING STANDARDS UPDATE 2026

The fact that only 23% of the working population are on course to reach even this standard — let alone the comfortable standard (which requires £45,400 for a single person and £62,700 for a couple) — indicates that the UK is facing not a marginal pension adequacy challenge but a systemic one.

Source: Pensions UK Retirement Living Standards Update 2026, developed in partnership with the Centre for Research in Social Policy at Loughborough University. Figures represent net annual income requirements.

The minimum standard — at £13,900 for a single person — is potentially achievable for couples where both partners receive the full new State Pension, which from April 2026 is approximately £12,548 per person per year (approximately £241.30 per week). However, single-person households, those who did not accumulate full National Insurance records, and anyone whose retirement costs include rent rather than mortgage-free ownership will find even the minimum challenging without private savings.

The second driver is contribution inadequacy. The House of Commons Library (March 2026) confirms that the minimum auto-enrolment contribution has been fixed at 8% of qualifying earnings — with 3% from the employer and 5% from the employee — since April 2019. The Herbert Smith Freehills Kramer analysis of the Pensions Commission's May 2026 interim report notes that for three-quarters of employees, total contribution rates remain below 12%, which most pensions experts regard as the minimum required for retirement adequacy.

Eight percent, applied only to the band of earnings between £6,240 and £50,270, is simply not enough for most workers to build a pot capable of generating £32,700 per year in retirement.

The third driver is the shift from defined benefit to defined contribution. The Investors Centre's April 2026 UK Pension Statistics analysis notes: 'The move away from defined benefit to defined contribution has quietly stripped out the one feature of workplace pensions that protected lower-earning, part-time, and career-interrupted workers most.' Under defined benefit schemes, the employer bore the investment and longevity risk. Under defined contribution schemes, the worker bears both — and must make their own decisions about contribution rates, investment choices, and the timing and form of drawing down their pot.

But participation is not adequacy. The critical issue, highlighted by the Herbert Smith Freehills analysis of the Pensions Commission's May 2026 interim report, is that 'many savers remain at or close to auto-enrolment minima, and for three-quarters of employees, contribution rates are below 12%.' The Wealthvieu auto-enrolment guide (May 2026) provides a concrete illustration: staying enrolled from age 22 on a £25,000 salary at the minimum 8% could build a pot of over £150,000 by retirement — which, if drawn down over a 20-year retirement, provides approximately £7,500 per year. That is significantly below the moderate standard of £32,700, and underscores why the minimum is a floor, not a target.

The qualifying earnings band is a further structural issue. Contributions are calculated only on earnings between £6,240 and £50,270 in 2026/27, not on total salary. A worker earning £35,000 makes contributions on only £28,760 (£35,000 minus the £6,240 lower limit). Workers earning below £10,000 are not automatically enrolled at all — a provision that the Government's December 2025 review of the auto-enrolment earnings trigger maintained unchanged, despite calls from organisations including the Women's Budget Group and Pregnant Then Screwed to extend auto-enrolment to the first pound of earnings.

However, the gap between the State Pension and the moderate retirement standard is stark. The full State Pension of £12,548 per year covers only 38% of the £32,700 a single person needs for a moderate lifestyle. Castle Trust Bank's June 2026 analysis summarises: 'The full new State Pension is around £241.30 per week (roughly £12,500 a year) from April 2026. This is well below the £32,700 needed for a moderate lifestyle, meaning a significant gap must be filled through workplace or personal savings.'

The causes are structural and interconnected: auto-enrolment contribution rates frozen at 8% since 2019; a qualifying earnings band that excludes the lowest earners; 4.8 million self-employed workers outside the employer-matching system; a housing divide that gives homeowners a permanent adequacy advantage; and rising living costs that keep raising the target. The Pensions Commission established in July 2025 has begun diagnosing the problem formally — but individual action cannot wait for policy change. Review your contributions. Check your employer match. Open a SIPP if self-employed. Check your State Pension forecast. A moderate retirement is achievable — but it requires more than the minimum.

HRReview — Three Quarters of Workers Not Saving Enough for Retirement (June 2026) https://hrreview.co.uk/hr-news/strategy-news/three-quarters-of-workers-not-saving-enough-for-retirement/388345

AOL / PA News — Three Quarters of Workers Not on Track for Moderate Pension Income (June 2026) https://www.aol.com/articles/three-quarters-workers-not-track-230227422.html

St James's Place — Pensions UK Report: Figures Paint Dire Picture of Nation's Saving (June 2026) https://www.sjp.co.uk/individuals/news/pensions-uk-report-figures-paint-dire-picture-of-nations-saving

Castle Trust Bank — Three Quarters of UK Workers Face Pension Shortfall (June 2026) https://www.castletrust.co.uk/three-quarters-of-uk-workers-face-pension-shortfall/

Herbert Smith Freehills Kramer — Pensions Commission Delivers UK Retirement Diagnosis (May 2026) https://www.hsfkramer.com/notes/pensions/2026-posts/pensions-commission-interim-report-may-2026

Scottish Widows — National Retirement Forecast 2026 (May 2026) https://expertise.scottishwidows.co.uk/retirement-report/retirement-report-2026-saving-for-retirement/national-retirement-forecast/

TABLE OF CONTENTS

- What Does a 'Moderate' Retirement Income Actually Mean in 2026?

- The Retirement Living Standards: Minimum, Moderate, and Comfortable

- Why Three Quarters of Workers Are Falling Short

- Who Is Most at Risk — The Adequacy Inequality Gap

- Auto-Enrolment: Why the Minimum Is Not Enough

- The State Pension: An Indispensable Foundation With a Significant Gap

- What You Can Do Right Now to Close the Gap

- Conclusion

- Frequently Asked Questions

- References

What Does a 'Moderate' Retirement Income Actually Mean in 2026?

When Pensions UK warns that three quarters of workers are not on track for a 'moderate' retirement income, the word moderate deserves unpacking — because what the pensions industry means by it is more aspirational than the word implies. The Retirement Living Standards (RLS), developed independently by the Centre for Research in Social Policy at Loughborough University and published by Pensions UK, define three standards of retirement living: minimum, moderate, and comfortable. Each represents a realistic, evidence-based budget covering everyday spending across housing, food, transport, leisure, and social activities.A moderate retirement lifestyle in 2026 is described by Pensions UK as one involving spending £56 a week on groceries, running a small car replaced every seven years, taking a three-star two-week foreign holiday plus one long weekend break in the UK per year, and having enough for some social activities, home improvements, and clothing. This is not a life of luxury — it is recognisably comfortable in the conventional sense, but decidedly unremarkable by the standards of working life for most British employees. The report estimates this costs £32,700 per year for a single person and £45,400 for a couple.

Too many people face a cliff-edge drop in income when they retire — and without action from government, employers, and savers, millions risk finding that the standard of living they worked decades to achieve disappears overnight.

— PENSIONS UK — RETIREMENT LIVING STANDARDS UPDATE 2026

The fact that only 23% of the working population are on course to reach even this standard — let alone the comfortable standard (which requires £45,400 for a single person and £62,700 for a couple) — indicates that the UK is facing not a marginal pension adequacy challenge but a systemic one.

The Retirement Living Standards: Minimum, Moderate, and Comfortable

The Pensions UK Retirement Living Standards 2026, developed with Loughborough University, set out three distinct annual income thresholds. The minimum standard covers basic needs without the ability to save or respond to unexpected costs. The moderate standard provides security and some of the pleasures of retirement. The comfortable standard provides financial freedom and the ability to help family members.Source: Pensions UK Retirement Living Standards Update 2026, developed in partnership with the Centre for Research in Social Policy at Loughborough University. Figures represent net annual income requirements.

The minimum standard — at £13,900 for a single person — is potentially achievable for couples where both partners receive the full new State Pension, which from April 2026 is approximately £12,548 per person per year (approximately £241.30 per week). However, single-person households, those who did not accumulate full National Insurance records, and anyone whose retirement costs include rent rather than mortgage-free ownership will find even the minimum challenging without private savings.

Why Three Quarters of Workers Are Falling Short

The Pensions UK report identifies rising living costs as the primary driver of the widening adequacy gap. The annual income required for a minimum retirement lifestyle for a couple rose from £21,600 in 2025 to £22,500 in 2026 — a 4.2% increase, driven by higher food, energy, and transport costs. This means the target has moved faster than most workers' pension savings, widening the gap for everyone who was already close to the margin.The second driver is contribution inadequacy. The House of Commons Library (March 2026) confirms that the minimum auto-enrolment contribution has been fixed at 8% of qualifying earnings — with 3% from the employer and 5% from the employee — since April 2019. The Herbert Smith Freehills Kramer analysis of the Pensions Commission's May 2026 interim report notes that for three-quarters of employees, total contribution rates remain below 12%, which most pensions experts regard as the minimum required for retirement adequacy.

Eight percent, applied only to the band of earnings between £6,240 and £50,270, is simply not enough for most workers to build a pot capable of generating £32,700 per year in retirement.

The third driver is the shift from defined benefit to defined contribution. The Investors Centre's April 2026 UK Pension Statistics analysis notes: 'The move away from defined benefit to defined contribution has quietly stripped out the one feature of workplace pensions that protected lower-earning, part-time, and career-interrupted workers most.' Under defined benefit schemes, the employer bore the investment and longevity risk. Under defined contribution schemes, the worker bears both — and must make their own decisions about contribution rates, investment choices, and the timing and form of drawing down their pot.

THE MAIN CAUSES OF THE UK PENSION SHORTFALL — 2026

- Rising living costs: the income required for moderate retirement rose 4.2% in 2026, outpacing average contribution growth (Pensions UK RLS Update 2026).

- Contribution rates too low: 8% of qualifying earnings since 2019 is below the 12%+ most experts consider adequate for a moderate lifestyle (Herbert Smith Freehills, May 2026).

- Qualifying earnings gap: contributions are calculated only on earnings between £6,240 and £50,270 — workers earning below £10,000 are excluded from auto-enrolment altogether.

- Self-employed excluded: 4.8 million self-employed workers have no employer matching and often no pension at all — only 21% are on track for moderate income (HL Barometer 2025).

- DB to DC shift: the move away from guaranteed defined benefit pensions places all investment and longevity risk on individuals with no professional support.

- Gender pension gap: women's career breaks, part-time work, and lower average earnings produce systematically lower pension outcomes throughout working life.

Who Is Most at Risk — The Adequacy Inequality Gap

The aggregate figure of 23% masks profound inequality in retirement preparedness. Hargreaves Lansdown's Savings and Resilience Barometer (January 2025) provides the clearest picture of who is most and least likely to achieve a moderate retirement income based on current saving patterns. The data reveals that adequacy varies dramatically by income level, housing tenure, family structure, and employment type.- Lowest-income households: only 8% are on track for a moderate retirement, compared with 68% of the highest-income households — a gap of 60 percentage points that reflects a lifetime of lower earnings, lower employer contributions, and fewer assets.

- Renters: only 15% are on track, compared with 47% of homeowners. Homeownership provides both a capital asset and — in retirement — a significant cost saving (no rent to pay), which dramatically improves the adequacy of a given pension income.

- Single parents: only 18% are on track for a moderate retirement, compared with 44% of couples without children — reflecting the combined effect of lower household income, greater childcare costs, more career interruptions, and less ability to save.

- Self-employed: only 21% are on track, compared with 60% of public sector employees. Self-employed workers have no employer contributions (the equivalent of a 3% pay cut compared to an employed peer), no auto-enrolment safety net, and face the highest uncertainty around income continuity.

Auto-Enrolment: Why the Minimum Is Not Enough

Auto-enrolment, introduced in October 2012, has been one of the most successful public policy interventions in UK personal finance history. By February 2026, 11.4 million eligible jobholders had been automatically enrolled into a qualifying workplace pension scheme (The Investors Centre, April 2026). The participation rate among eligible employees now stands at around nine in ten — a transformational increase from the pre-2012 baseline.But participation is not adequacy. The critical issue, highlighted by the Herbert Smith Freehills analysis of the Pensions Commission's May 2026 interim report, is that 'many savers remain at or close to auto-enrolment minima, and for three-quarters of employees, contribution rates are below 12%.' The Wealthvieu auto-enrolment guide (May 2026) provides a concrete illustration: staying enrolled from age 22 on a £25,000 salary at the minimum 8% could build a pot of over £150,000 by retirement — which, if drawn down over a 20-year retirement, provides approximately £7,500 per year. That is significantly below the moderate standard of £32,700, and underscores why the minimum is a floor, not a target.

The qualifying earnings band is a further structural issue. Contributions are calculated only on earnings between £6,240 and £50,270 in 2026/27, not on total salary. A worker earning £35,000 makes contributions on only £28,760 (£35,000 minus the £6,240 lower limit). Workers earning below £10,000 are not automatically enrolled at all — a provision that the Government's December 2025 review of the auto-enrolment earnings trigger maintained unchanged, despite calls from organisations including the Women's Budget Group and Pregnant Then Screwed to extend auto-enrolment to the first pound of earnings.

The State Pension: An Indispensable Foundation With a Significant Gap

The full new State Pension for 2026/27 is approximately £241.30 per week — around £12,548 per year. The Herbert Smith Freehills analysis of the Pensions Commission's May 2026 interim report describes it as 'now an indispensable foundation, accounting for more than three-quarters of retirement income for those at the lowest end of the distribution.' The triple lock — which ensures the State Pension rises by the highest of earnings growth, inflation, or 2.5% — has protected its real value over time.However, the gap between the State Pension and the moderate retirement standard is stark. The full State Pension of £12,548 per year covers only 38% of the £32,700 a single person needs for a moderate lifestyle. Castle Trust Bank's June 2026 analysis summarises: 'The full new State Pension is around £241.30 per week (roughly £12,500 a year) from April 2026. This is well below the £32,700 needed for a moderate lifestyle, meaning a significant gap must be filled through workplace or personal savings.'

What You Can Do Right Now to Close the Gap

The Pensions UK report, while stark in its diagnosis, is not intended to produce despair — it is intended to produce action. St James's Place's June 2026 analysis notes: 'Seven out of 10 people from our 2026 Financial Health Report said that a plan made them feel more confident in their finances.' The earlier you understand the gap, the more time you have to close it. Even modest increases in contributions, made consistently over time, can produce significant differences in retirement income.PRACTICAL STEPS TO IMPROVE YOUR RETIREMENT OUTLOOK — 2026

- Increase your pension contributions above the auto-enrolment minimum: even raising your contribution from 5% to 8% can significantly boost your final pot — and if your employer matches additional contributions (many do), you effectively receive an immediate 50-100% return on the extra contribution before any investment growth.

- Check whether your employer offers contribution matching above the minimum: Wealthvieu's 2026 guide shows that an employer increasing their contribution from 3% to 6% can raise total contributions from 8% to 14% of qualifying earnings — close to the adequacy threshold identified by experts.

- Use tax-advantaged accounts: contributions to pensions receive income tax relief. A basic-rate taxpayer contributes £80 and their pension is credited with £100. A higher-rate taxpayer can claim an additional £20 relief. ISAs can supplement pension income in a tax-efficient wrapper for flexible access before age 57.

- Check your State Pension forecast: use the government's Check Your State Pension service (gov.uk/check-state-pension) to see your projected State Pension and National Insurance record. Voluntary Class 3 NI contributions (£824.20 per year in 2026/27) can fill gaps and add significantly to your lifetime State Pension income.

- Self-employed: open a SIPP or stakeholder pension immediately. Contributions receive the same tax relief as employed workers. The annual allowance (up to £60,000 or 100% of earnings, whichever is lower) provides ample room to save, and contributions can be made flexibly to reflect variable income.

- Consider consolidating old pension pots: the average UK worker has 11 different jobs during their career, often accumulating multiple small pension pots. Consolidating these into a single plan can reduce fees, simplify management, and make it easier to track progress toward the RLS targets.

CONCLUSION

Pensions UK's June 2026 Retirement Living Standards Update delivers a stark and urgent diagnosis: three quarters of UK workers are on course for a retirement income that falls below what the industry considers moderate — a standard that is itself considerably more modest than most working people would recognise as comfortable. Only 23% are on track for moderate. Only 9% for comfortable. The gap between the State Pension (£12,548) and the moderate income standard (£32,700 for a single person) is £20,152 per year that must come from private savings — savings that the majority of workers are currently not accumulating fast enough.The causes are structural and interconnected: auto-enrolment contribution rates frozen at 8% since 2019; a qualifying earnings band that excludes the lowest earners; 4.8 million self-employed workers outside the employer-matching system; a housing divide that gives homeowners a permanent adequacy advantage; and rising living costs that keep raising the target. The Pensions Commission established in July 2025 has begun diagnosing the problem formally — but individual action cannot wait for policy change. Review your contributions. Check your employer match. Open a SIPP if self-employed. Check your State Pension forecast. A moderate retirement is achievable — but it requires more than the minimum.

Frequently Asked Questions

How much do I need to retire comfortably in the UK in 2026?

According to the Pensions UK Retirement Living Standards Update 2026, developed in partnership with Loughborough University, a moderate lifestyle requires £32,700 per year for a single person and £45,400 for a couple. A comfortable lifestyle requires £45,400 for a single person and £62,700 for a couple. A minimum standard — covering basic needs without financial flexibility — costs £13,900 for a single person and £22,500 for a couple. The full new State Pension (from April 2026) is approximately £12,548 per year — covering the minimum standard for a couple with two full State Pensions but leaving a significant gap for anyone targeting a moderate or comfortable retirement.Why are only 23% of UK workers on track for a moderate retirement income?

The Pensions UK report and supporting analysis identify several structural causes. Auto-enrolment contributions have been fixed at 8% of qualifying earnings since April 2019 — the Herbert Smith Freehills analysis of the May 2026 Pensions Commission interim report notes that three-quarters of employees contribute below 12%, which is the approximate minimum for adequacy. The qualifying earnings band (£6,240 to £50,270) means contributions are not made on all earnings. Rising living costs have increased the income required in retirement at a rate that outpaces typical contribution growth. The self-employed — approximately 4.8 million workers — have no employer match and are frequently excluded from workplace schemes. And the shift from defined benefit to defined contribution pensions has placed investment and longevity risk entirely on individuals.What is the difference between minimum, moderate, and comfortable retirement in the UK?

These are the three tiers of the Pensions UK Retirement Living Standards (RLS), developed with Loughborough University. The minimum standard (£13,900 single / £22,500 couple) covers basic bills and essential spending with no car, no foreign holidays, and limited social activity. The moderate standard (£32,700 single / £45,400 couple) includes a small car replaced every seven years, one two-week foreign holiday per year, one long UK weekend break, £56 per week on groceries, and some home improvements and social spending. The comfortable standard (£45,400 single / £62,700 couple) includes a small car replaced every five years, one four-star two-week holiday per year plus three UK breaks, £75 per week on groceries, and the ability to help family members financially.Is the 8% auto-enrolment contribution enough for a moderate retirement?

For most workers, no. The minimum total auto-enrolment contribution of 8% of qualifying earnings — split as 3% employer and 5% employee — is widely regarded by pensions experts as insufficient for a moderate retirement lifestyle. The Herbert Smith Freehills analysis of the Pensions Commission's May 2026 interim report states that for three-quarters of employees, contribution rates are below 12%, which is closer to the adequacy threshold. Additionally, the 8% is applied only to earnings between £6,240 and £50,270, not to total salary, further reducing the effective contribution rate. Wealthvieu's May 2026 auto-enrolment guide estimates that staying enrolled from age 22 on a £25,000 salary at minimum contributions could build a pot of over £150,000 — which, drawn over 20 years, provides approximately £7,500 per year, far below the moderate standard of £32,700.What can I do if I am not on track for a moderate pension income?

The most effective immediate steps are: (1) increase your pension contribution above the auto-enrolment minimum — even 1–2 additional percentage points compounded over decades makes a significant difference; (2) check whether your employer offers matching above 3%, and contribute at least to the level that captures the full match; (3) use the government's Check Your State Pension service at gov.uk/check-state-pension to see your projected income and identify any gaps in your National Insurance record that can be filled with voluntary contributions; (4) if self-employed, open a SIPP or stakeholder pension immediately to access the same tax relief available to employed workers; (5) consider consolidating multiple old pension pots from previous employers into a single plan to reduce fees and improve oversight. Castle Trust Bank's June 2026 analysis notes: 'The latest figures aren't about creating worry — they're about creating awareness. The earlier you understand the gap, the more time you have to close it.'References

Pensions UK — Retirement Living Standards Update 2026 (Official, developed with Loughborough University) https://www.pensionsuk.org.uk/research/retirement-living-standards/HRReview — Three Quarters of Workers Not Saving Enough for Retirement (June 2026) https://hrreview.co.uk/hr-news/strategy-news/three-quarters-of-workers-not-saving-enough-for-retirement/388345

AOL / PA News — Three Quarters of Workers Not on Track for Moderate Pension Income (June 2026) https://www.aol.com/articles/three-quarters-workers-not-track-230227422.html

St James's Place — Pensions UK Report: Figures Paint Dire Picture of Nation's Saving (June 2026) https://www.sjp.co.uk/individuals/news/pensions-uk-report-figures-paint-dire-picture-of-nations-saving

Castle Trust Bank — Three Quarters of UK Workers Face Pension Shortfall (June 2026) https://www.castletrust.co.uk/three-quarters-of-uk-workers-face-pension-shortfall/

Herbert Smith Freehills Kramer — Pensions Commission Delivers UK Retirement Diagnosis (May 2026) https://www.hsfkramer.com/notes/pensions/2026-posts/pensions-commission-interim-report-may-2026

Scottish Widows — National Retirement Forecast 2026 (May 2026) https://expertise.scottishwidows.co.uk/retirement-report/retirement-report-2026-saving-for-retirement/national-retirement-forecast/

0 Comments Comments