Retirement

Retirement Feels Manageable — That's Often the Problem

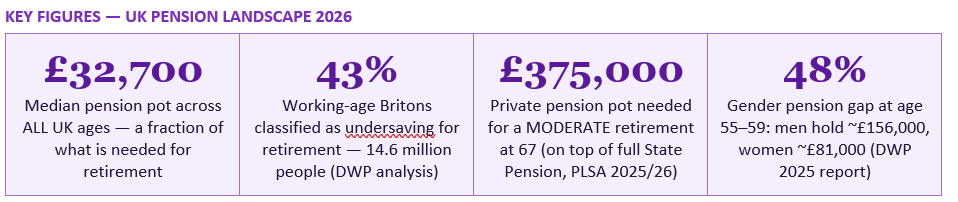

43% of working-age Britons — 14.6 million people — are currently classified as undersaving for retirement. The median pension pot across all UK ages is £32,700. The amount needed for a moderate retirement at 67, on top of the full State Pension, is approximately £375,000. And yet most people feel broadly fine about their retirement. This is the most dangerous gap in UK personal finance — not the one between what people have and what they need, but the one between what they have and what they think they have.

It is not. The median pension pot across all UK ages stands at £32,700. The pot required for a moderate retirement — one that covers essentials with a little left for a European holiday and modest additional spending — is approximately £375,000 on top of the full State Pension, according to the Pensions and Lifetime Savings Association's 2025/26 Retirement Living Standards. That is a gap of approximately £342,300 for the median saver. And at every age group, the typical British saver is significantly behind the target needed for even a moderate retirement, according to Wealthvieu's analysis of ONS Wealth and Assets Survey data.

The problem is structural. Auto-enrolment was designed to solve the participation crisis — to get people into pensions who were not saving at all. It succeeded brilliantly: 89% of eligible employees now save into a workplace pension, compared with 55% before the reforms. But the minimum contribution rate of 8% of qualifying earnings — 5% from the employee, 3% from the employer — was designed as a starting point, not a destination. The Pensions Commission that designed auto-enrolment originally envisaged contributions rising to 12% to 15% over time. That increase never happened. And every year that passes with contribution rates unchanged is a year that millions of workers fall further behind their future financial needs.

Auto-enrolment has solved the participation problem but not the adequacy problem. Getting 89% of eligible employees saving was the easy leg — raising the minimum contribution from 8% of qualifying earnings to something approaching a realistic replacement rate is the one that actually determines whether the next 40 years of retirements are comfortable.

— THE INVESTORS CENTRE — UK PENSION STATISTICS 2026

*Private pension pot required on top of full new State Pension (£12,547/year, 2026/27). Assumes homeownership. PLSA Retirement Living Standards 2025/26.

The minimum standard is notable: because the full State Pension (£12,547 per year from April 2026, after the 4.8% triple-lock increase) covers most of the minimum income requirement, only a relatively small private pot is needed to reach this standard. But the minimum standard should not be confused with a comfortable life: at £13,400 per year total, there is no budget for a car, no foreign holidays, no significant extras, and very limited ability to absorb unexpected costs. Most working adults who have maintained a reasonable standard of living during employment would find retirement at the minimum standard a significant and distressing reduction in quality of life.

By February 2026, 89% of eligible employees save into a workplace pension, and total annual workplace pension savings reached £149.7 billion in 2024 — a real-terms increase of £49.1 billion since auto-enrolment began, according to DWP data. These are extraordinary achievements.

The adequacy failure is separate from the participation success. The minimum contribution rate of 8% of qualifying earnings — applying to earnings between £6,240 and £50,270 per year — was always intended as a floor, not a target. The Pensions Commission that designed the system envisaged gradual increases to 12% to 15%. More than a decade later, the minimum remains at 8%, and the Government's 2025 Pensions Review concluded that even on current projections, a median earner contributing only at the minimum rate from age 22 will accumulate approximately £180,000 by state pension age — enough to reach the minimum living standard but nowhere near the moderate standard of £375,000.

There are also structural participation gaps that auto-enrolment does not reach. Only 20% of self-employed adults save into any pension — down from 50% in the late 1990s — because auto-enrolment does not apply to those working for themselves. This leaves 4.4 million working adults almost entirely outside the workplace pension system. Among employees at micro-employers (fewer than five employees), only 59% of eligible workers are saving — a 30-percentage-point gap below the national average. And the 3.3 million lost or unclaimed pension pots worth an estimated £31.1 billion (Pensions Policy Institute, October 2024) represent a vast pool of retirement savings that have been disconnected from their rightful owners.

The mechanisms are well-documented and interconnected. The gender pay gap — currently approximately 6.9% for full-time workers according to ONS 2025 data — means lower pension contributions from the outset. Part-time work, which women are significantly more likely to undertake (35% of women work part-time vs 13% of men), further reduces contributions and, critically, may place many workers below the auto-enrolment earnings threshold of £10,000 per year, meaning they are not automatically enrolled at all. Career breaks for childcare create multi-year gaps in pension accumulation during working years that typically produce the highest earnings growth. And the compounding of all these effects over a 30 to 40-year career produces the 48% gap observed at peak pre-retirement age.

The practical consequence is that women face a retirement income crisis that is structurally more acute than men's at every income level. A woman who has worked full-time throughout her career at average female earnings, taken one career break of three years for childcare, and contributed at the auto-enrolment minimum throughout is likely to have significantly less than the £375,000 target at retirement age — and the shortfall is not attributable to any individual choice but to the cumulative effect of a system that does not adequately account for the caring responsibilities that fall disproportionately on women.

Several specific mechanisms contribute to the comfortable illusion. First, the visible pension pot creates a false sense of progress. A pension statement showing £39,500 at age 40 looks like a meaningful sum — it is four or five times what many people have in current accounts — and the psychological experience is of having 'done the right thing.' The comparison to the £112,000 required at the same age for a moderate retirement is rarely made spontaneously, because the required figure is not visible anywhere in the standard pension communication experience.

Second, the State Pension creates an anchor that reduces perceived urgency. People know — or vaguely assume — that they will receive some State Pension income. The current full new State Pension of £12,547 per year is sufficient to generate a sense that basic needs will be covered, which reduces the perceived urgency of private pension saving. But the minimum PLSA standard income of £13,400 per year is only marginally above the full State Pension — meaning even the most basic acceptable retirement standard requires meaningful private savings above the State Pension for most people.

Third, the distant time horizon makes the problem feel unreal. A 35-year-old facing a £280,000 pension shortfall is not experiencing any immediate pain from it — retirement is 30 years away, pensions are a boring topic, and more immediate financial pressures (rent, mortgage, childcare, cost of living) compete for the same cash. The behavioural economics literature consistently shows that individuals heavily discount the future — assigning psychologically much lower value to money or outcomes that are decades away than those that are immediately available.

What the State Pension covers: at the PLSA minimum standard of £13,400 per year, the State Pension alone covers 94% of the required income. A small private pension bridging the remaining £853 per year is all that is needed to reach the minimum standard. The State Pension therefore provides an important guarantee against the most severe forms of retirement poverty for people with full NI records.

What the State Pension does not cover: everything above the minimum standard. For the 37% of workers who are actively aiming for a moderate retirement — the PLSA standard most people intuitively aspire to, with a European holiday, a somewhat flexible lifestyle, and adequate financial security — the State Pension covers only 40% of the £31,700 annual income requirement. The remaining 60% — approximately £19,150 per year — must come from private pension savings. For a comfortable retirement at £43,100 per year, the State Pension covers less than 30%.

The State Pension age is currently 66, rising to 67 for those born between 6 April 1960 and 5 April 1977 — a transition beginning in April 2026 and completing in March 2028. A further increase to 68 is legislated for 2044 to 2046. For workers in physically demanding occupations, the combination of an increasing state pension age and declining health in the late 60s creates a specific retirement planning risk: the period between being unable to continue working and becoming eligible for the State Pension may need to be funded from private savings.

The stability-over-status framework that is reshaping UK attitudes to money — debt-free living, financial resilience, long-term security over short-term display — applies with full force to retirement planning. The most important thing a working person can do for their future financial security is to look honestly at the gap between their current pension trajectory and the retirement income they actually want, and to take deliberate steps to close it. Check your State Pension forecast. Find your lost pots. Maximise your employer match. Increase contributions when your salary rises. These are not exciting actions. But they are the ones that determine whether the last decades of your life are spent in financial dignity or financial constraint.

The Investors Centre — Average Pension Pot UK 2026 Statistics (DWP, PLSA, ONS) https://www.theinvestorscentre.co.uk/investing/average-pension-pot-uk/

The Investors Centre — UK Pension Statistics 2026: Key Data & Trends https://www.theinvestorscentre.co.uk/investing/statistics/pension/

PoundSense — Average Pension Pot by Age UK (PLSA Retirement Living Standards 2026) https://www.poundsense.co.uk/blog/average-pension-pot-by-age-uk

PocketWise — Average Pension Pot UK by Age 2026: Are You on Track? https://pocketwise.co.uk/pensions-and-retirement/average-pension-pot-uk-by-age/

MoneyWeek — Average Pension Pot by Age UK 2026 (PensionBee, Fidelity, ONS) https://moneyweek.com/personal-finance/pensions/average-pension-pot-by-age

Nuts About Money — Average Pension Pot UK 2026 (PLSA standards, State Pension) https://www.nutsaboutmoney.com/pensions/average-pension-pot-uk

GOV.UK — Check Your State Pension Forecast https://www.gov.uk/check-state-pension

TABLE OF CONTENTS

- The Comfortable Illusion: Why Retirement Feels Fine

- The Numbers: What You Actually Have vs What You Need

- The PLSA Retirement Living Standards Explained

- Auto-Enrolment: The System That Saved Participation But Not Adequacy

- The Gender Pension Gap: A 48% Crisis at Peak Age

- Who Is Most at Risk? The Gaps Within the Gap

- Why People Systematically Underestimate Their Pension Shortfall

- The State Pension in 2026/27: What It Covers and What It Does Not

- The Three Structural Problems That Persist

- How to Check Whether You Are on Track

- Practical Steps to Close Your Pension Gap

- Conclusion

- Frequently Asked Questions

- References

The Comfortable Illusion: Why Retirement Feels Fine

The most dangerous aspect of the UK's retirement savings crisis is not that people are unaware that a crisis exists. It is that the system has been designed — unintentionally but effectively — to make inadequate saving feel like adequate saving. Automatic enrolment puts money into a pension before it touches a worker's bank account. The monthly contributions appear on a payslip. The pension provider sends an annual statement. The pot grows, slowly but visibly. And because something is happening — because the process is automated and the numbers are moving in the right direction — retirement planning feels like a task that is broadly under control.It is not. The median pension pot across all UK ages stands at £32,700. The pot required for a moderate retirement — one that covers essentials with a little left for a European holiday and modest additional spending — is approximately £375,000 on top of the full State Pension, according to the Pensions and Lifetime Savings Association's 2025/26 Retirement Living Standards. That is a gap of approximately £342,300 for the median saver. And at every age group, the typical British saver is significantly behind the target needed for even a moderate retirement, according to Wealthvieu's analysis of ONS Wealth and Assets Survey data.

The problem is structural. Auto-enrolment was designed to solve the participation crisis — to get people into pensions who were not saving at all. It succeeded brilliantly: 89% of eligible employees now save into a workplace pension, compared with 55% before the reforms. But the minimum contribution rate of 8% of qualifying earnings — 5% from the employee, 3% from the employer — was designed as a starting point, not a destination. The Pensions Commission that designed auto-enrolment originally envisaged contributions rising to 12% to 15% over time. That increase never happened. And every year that passes with contribution rates unchanged is a year that millions of workers fall further behind their future financial needs.

Auto-enrolment has solved the participation problem but not the adequacy problem. Getting 89% of eligible employees saving was the easy leg — raising the minimum contribution from 8% of qualifying earnings to something approaching a realistic replacement rate is the one that actually determines whether the next 40 years of retirements are comfortable.

— THE INVESTORS CENTRE — UK PENSION STATISTICS 2026

The Numbers: What You Actually Have vs What You Need

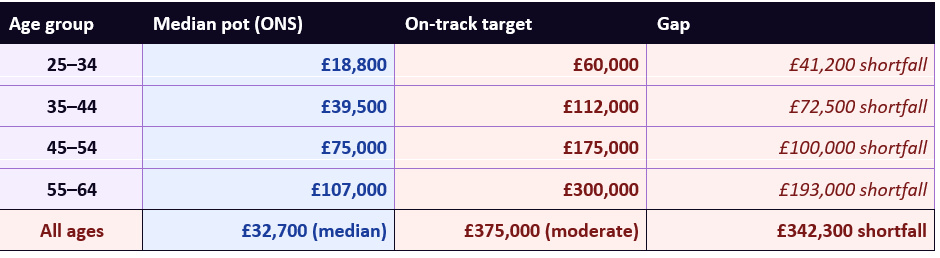

The pension gap becomes concrete when you compare median savings at each age to the benchmarks required for a moderate retirement at 67. The following table draws on ONS Wealth and Assets Survey data for median pension wealth by age group, and compares it to the approximate pot needed at each age to be on track for a moderate retirement at 67 — assuming continued contributions and approximately 6% to 7% average annual growth.

Sources: ONS Wealth and Assets Survey; PLSA Retirement Living Standards 2025/26; Wealthvieu, PocketWise, PoundSense pension analyses 2026. On-track targets assume moderate PLSA standard at 67 with full State Pension and 6–7% annual growth from current age.

The table is sobering reading at every age. A typical 45-year-old with £75,000 in pension savings — broadly at the median for their age group — needs approximately £175,000 to be on track for a moderate retirement. They are £100,000 short, with 22 years to close the gap. That is achievable but requires a significant increase in contributions well above the current auto-enrolment minimum. For the typical 55 to 64 year old with £107,000, the on-track target of approximately £300,000 is £193,000 away with perhaps 10 to 12 years of working life remaining. At that stage, catching up requires either substantially higher contributions, a later retirement date, or an adjustment in expectations about the standard of living in retirement.The PLSA Retirement Living Standards Explained

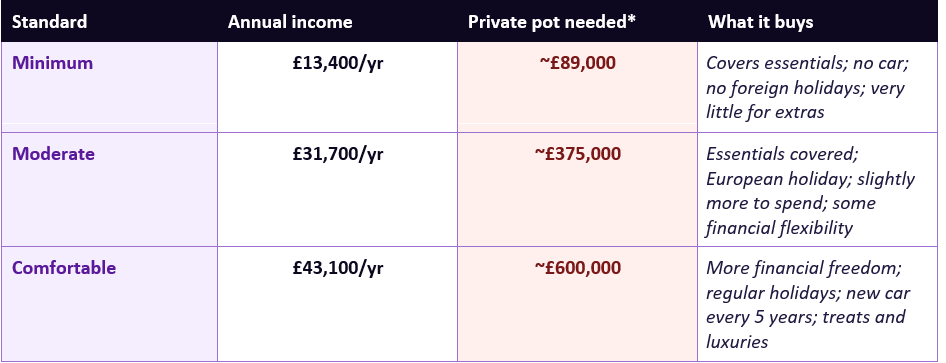

The Pensions and Lifetime Savings Association publishes annual Retirement Living Standards — benchmarks for three levels of retirement income that translate abstract pension pot sizes into real-world lifestyle descriptions. These standards are updated annually for inflation and are widely used across the UK pensions industry. The 2025/26 figures are as follows.*Private pension pot required on top of full new State Pension (£12,547/year, 2026/27). Assumes homeownership. PLSA Retirement Living Standards 2025/26.

The minimum standard is notable: because the full State Pension (£12,547 per year from April 2026, after the 4.8% triple-lock increase) covers most of the minimum income requirement, only a relatively small private pot is needed to reach this standard. But the minimum standard should not be confused with a comfortable life: at £13,400 per year total, there is no budget for a car, no foreign holidays, no significant extras, and very limited ability to absorb unexpected costs. Most working adults who have maintained a reasonable standard of living during employment would find retirement at the minimum standard a significant and distressing reduction in quality of life.

Auto-Enrolment: The System That Saved Participation But Not Adequacy

Auto-enrolment, introduced in October 2012, is one of the most successful policy interventions in UK retirement savings history. By requiring employers to automatically enrol eligible workers into a workplace pension — with opt-out available but the default being participation — it reversed decades of declining workplace pension participation and brought 11.4 million additional workers into pension saving who would otherwise not have been saving at all.By February 2026, 89% of eligible employees save into a workplace pension, and total annual workplace pension savings reached £149.7 billion in 2024 — a real-terms increase of £49.1 billion since auto-enrolment began, according to DWP data. These are extraordinary achievements.

The adequacy failure is separate from the participation success. The minimum contribution rate of 8% of qualifying earnings — applying to earnings between £6,240 and £50,270 per year — was always intended as a floor, not a target. The Pensions Commission that designed the system envisaged gradual increases to 12% to 15%. More than a decade later, the minimum remains at 8%, and the Government's 2025 Pensions Review concluded that even on current projections, a median earner contributing only at the minimum rate from age 22 will accumulate approximately £180,000 by state pension age — enough to reach the minimum living standard but nowhere near the moderate standard of £375,000.

There are also structural participation gaps that auto-enrolment does not reach. Only 20% of self-employed adults save into any pension — down from 50% in the late 1990s — because auto-enrolment does not apply to those working for themselves. This leaves 4.4 million working adults almost entirely outside the workplace pension system. Among employees at micro-employers (fewer than five employees), only 59% of eligible workers are saving — a 30-percentage-point gap below the national average. And the 3.3 million lost or unclaimed pension pots worth an estimated £31.1 billion (Pensions Policy Institute, October 2024) represent a vast pool of retirement savings that have been disconnected from their rightful owners.

The Gender Pension Gap: A 48% Crisis at Peak Age

The gender pension gap is one of the most structurally significant and least publicly discussed dimensions of the UK's retirement savings problem. The DWP's 2025 report found that women aged 55 to 59 have median pension wealth of approximately £81,000 compared with approximately £156,000 for men of the same age — a gap of roughly 48%. This is not a gap that has emerged recently; it is the accumulated product of decades of structural labour market inequality.The mechanisms are well-documented and interconnected. The gender pay gap — currently approximately 6.9% for full-time workers according to ONS 2025 data — means lower pension contributions from the outset. Part-time work, which women are significantly more likely to undertake (35% of women work part-time vs 13% of men), further reduces contributions and, critically, may place many workers below the auto-enrolment earnings threshold of £10,000 per year, meaning they are not automatically enrolled at all. Career breaks for childcare create multi-year gaps in pension accumulation during working years that typically produce the highest earnings growth. And the compounding of all these effects over a 30 to 40-year career produces the 48% gap observed at peak pre-retirement age.

The practical consequence is that women face a retirement income crisis that is structurally more acute than men's at every income level. A woman who has worked full-time throughout her career at average female earnings, taken one career break of three years for childcare, and contributed at the auto-enrolment minimum throughout is likely to have significantly less than the £375,000 target at retirement age — and the shortfall is not attributable to any individual choice but to the cumulative effect of a system that does not adequately account for the caring responsibilities that fall disproportionately on women.

Who Is Most at Risk? The Gaps Within the Gap

The 43% undersaving figure is itself an average that conceals significant variation in the distribution of pension risk. Certain groups face a materially worse outlook than the aggregate data suggests.Groups facing the greatest pension undersaving risk in 2026

- Self-employed workers: Only 20% save into any pension — down from 50% in the late 1990s. Auto-enrolment does not apply to self-employed individuals, leaving 4.4 million working adults with no employer contribution and no default savings mechanism. The National Insurance record implications of self-employment gaps also affect State Pension entitlement.

- Gig economy and zero-hours workers: Irregular and variable income makes pension saving difficult to automate and easy to deprioritise. Many gig workers do not meet the auto-enrolment earnings threshold in any given month, even if their annual income would qualify them.

- Women who have taken career breaks: The combination of contribution gaps during breaks, reduced earnings on return, and the 48% gender pension gap at peak age means that women approaching retirement with career break histories face a significantly higher retirement income shortfall than the national median data suggests.

- Pakistani and Bangladeshi workers: The Investors Centre notes a 68% pension participation rate for this group — 21 percentage points below the national average — reflecting a combination of industry concentration (in sectors with lower auto-enrolment compliance), earnings patterns, and cultural factors.

- Workers at micro-employers: Only 59% of eligible employees at employers with fewer than five staff are saving into a pension — suggesting significantly lower employer compliance or worker take-up at the smallest end of the business spectrum.

- People who opted out: Despite auto-enrolment, approximately 1.9 million people have opted out of their workplace pension. For those who opted out during the cost of living crisis of 2021 to 2024 to free up cash, each year of missed contributions — including the forgone employer match — represents a permanently compounded retirement income loss.

Why People Systematically Underestimate Their Pension Shortfall

The psychological research on retirement planning is consistent: people systematically underestimate the amount they need to save, overestimate the value of their current pension pot, and discount the future in ways that make present consumption feel more important than future security. These cognitive biases are not signs of stupidity — they are features of the human decision-making system that evolved in environments where short-term survival was more important than long-term planning.Several specific mechanisms contribute to the comfortable illusion. First, the visible pension pot creates a false sense of progress. A pension statement showing £39,500 at age 40 looks like a meaningful sum — it is four or five times what many people have in current accounts — and the psychological experience is of having 'done the right thing.' The comparison to the £112,000 required at the same age for a moderate retirement is rarely made spontaneously, because the required figure is not visible anywhere in the standard pension communication experience.

Second, the State Pension creates an anchor that reduces perceived urgency. People know — or vaguely assume — that they will receive some State Pension income. The current full new State Pension of £12,547 per year is sufficient to generate a sense that basic needs will be covered, which reduces the perceived urgency of private pension saving. But the minimum PLSA standard income of £13,400 per year is only marginally above the full State Pension — meaning even the most basic acceptable retirement standard requires meaningful private savings above the State Pension for most people.

Third, the distant time horizon makes the problem feel unreal. A 35-year-old facing a £280,000 pension shortfall is not experiencing any immediate pain from it — retirement is 30 years away, pensions are a boring topic, and more immediate financial pressures (rent, mortgage, childcare, cost of living) compete for the same cash. The behavioural economics literature consistently shows that individuals heavily discount the future — assigning psychologically much lower value to money or outcomes that are decades away than those that are immediately available.

The State Pension in 2026/27: What It Covers and What It Does Not

The full new State Pension from April 2026 is approximately £12,547 per year (£241.30 per week), following the 4.8% triple-lock increase — the largest in recent years, driven by wage growth. This represents a meaningful and reliable income floor for UK retirees who have accumulated the required 35 qualifying years of National Insurance contributions.What the State Pension covers: at the PLSA minimum standard of £13,400 per year, the State Pension alone covers 94% of the required income. A small private pension bridging the remaining £853 per year is all that is needed to reach the minimum standard. The State Pension therefore provides an important guarantee against the most severe forms of retirement poverty for people with full NI records.

What the State Pension does not cover: everything above the minimum standard. For the 37% of workers who are actively aiming for a moderate retirement — the PLSA standard most people intuitively aspire to, with a European holiday, a somewhat flexible lifestyle, and adequate financial security — the State Pension covers only 40% of the £31,700 annual income requirement. The remaining 60% — approximately £19,150 per year — must come from private pension savings. For a comfortable retirement at £43,100 per year, the State Pension covers less than 30%.

The State Pension age is currently 66, rising to 67 for those born between 6 April 1960 and 5 April 1977 — a transition beginning in April 2026 and completing in March 2028. A further increase to 68 is legislated for 2044 to 2046. For workers in physically demanding occupations, the combination of an increasing state pension age and declining health in the late 60s creates a specific retirement planning risk: the period between being unable to continue working and becoming eligible for the State Pension may need to be funded from private savings.

The Three Structural Problems That Persist

Despite a decade of auto-enrolment and multiple government reviews, three structural problems continue to drive the UK pension adequacy gap.Problem 1: The contribution rate is too low

Eight per cent of qualifying earnings — even with employer and tax relief contributions included — is insufficient to generate a moderate retirement income for most workers. The DWP's own modelling shows that a median earner contributing only at the minimum rate from age 22 accumulates approximately £180,000 by retirement — sufficient for the minimum standard but not the moderate. The government's Pensions Review of 2025 acknowledged this inadequacy but did not commit to a timeline for increasing minimum contribution rates. Every year of inaction compounds the problem.Problem 2: The self-employed are almost entirely outside the system

The 4.4 million self-employed workers with no employer contributions, no automatic enrolment, and pension participation rates of only 20% represent the most significant unaddressed gap in UK retirement policy. The Money Advice Trust's evidence to the Treasury Select Committee explicitly called for a policy solution to the self-employed pension participation problem — noting that the current system has 'no long-term plan' for this group despite the rapid growth of the self-employed labour force.Problem 3: The lost pots and the consolidation gap

The Pensions Policy Institute's October 2024 briefing estimated 3.3 million lost or unclaimed pension pots worth £31.1 billion. Every time a worker changes employer without consolidating their pension pots, there is a risk that the old pot becomes disconnected — especially if contact details change, the employer changes name, or the pension scheme is consolidated into a master trust. The Pensions Dashboards Programme — which will allow anyone to see all their pension savings in one place — is the critical infrastructure solution, but its rollout has been subject to repeated delays.How to Check Whether You Are on Track

The most important single action anyone reading this article can take is to check their actual pension situation against the benchmarks — today, not at some vague future point. This takes approximately 30 minutes and provides the foundation for every other decision about pension saving.A four-step pension health check

- Step 1 — Check your State Pension forecast: Visit gov.uk/check-state-pension. You will see your current State Pension forecast, your qualifying years of National Insurance contributions, and any gaps in your NI record. If you have gaps, check whether voluntary NI contributions (approximately £824 per missing year) would be cost-effective — they typically pay back in under three years of retirement.

- Step 2 — Find all your pension pots: Contact all previous employers to obtain the values of any workplace pensions you hold with them. Use the DWP's Pension Tracing Service (gov.uk/find-pension-contact-details) to track down any lost pots. The average worker has held approximately 11 jobs over their career — many have multiple small pension pots with old employers.

- Step 3 — Compare your total pot to the on-track benchmark for your age: Using the table in Section 2, compare your total current pension wealth to the on-track target for your age group. If you are behind (as most people are), the gap is not a reason for panic — it is data that enables you to make better-informed decisions about contributions, retirement age, and lifestyle.

- Step 4 — Use the MoneyHelper pension calculator: The free pension calculator at moneyhelper.org.uk will project your estimated retirement income based on your current pot, contribution rate, and expected retirement age. It includes State Pension in the projection and allows you to test different contribution scenarios to see their impact on retirement income.

Practical Steps to Close Your Pension Gap

Once you know your gap, you can begin to close it. The following steps are approximately ordered by impact — start at the top and work down.Action and why it matters

- Increase your pension contribution to capture your employer's full match. Many workplace pension schemes offer employer contributions above the minimum 3% if employees contribute more than the minimum 5%. Not maximising the employer match is leaving free money on the table — this is the highest guaranteed return available in any pension.

- Use salary sacrifice if your employer offers it. Contributing to a pension via salary sacrifice reduces your gross salary before National Insurance is calculated, saving you NI on the contribution. On a £500 per month pension contribution, salary sacrifice typically saves an additional £100 in NI — an instant 20% return on the contribution.

- Fill gaps in your National Insurance record for State Pension purposes. Voluntary Class 3 NI contributions cost approximately £824 per missing year and buy approximately £329 per year of additional State Pension for life — typically paying back in under three years. For anyone with NI gaps, this is among the highest-return investments available.

- Consider a SIPP alongside your workplace pension. A Self-Invested Personal Pension gives you access to low-cost index ETFs (such as the three-fund portfolio covered in our companion ETF article) rather than the managed funds in most default workplace schemes. The combination of lower investment costs and broader investment choice can materially improve long-term outcomes.

- Trace and consolidate old pension pots. The DWP's Pension Tracing Service and the forthcoming Pensions Dashboards will help you locate lost pots. Consolidating old pots into a single SIPP or current workplace pension reduces fees and simplifies management — but check whether any old pot contains valuable guarantees (particularly defined benefit entitlements) before transferring.

- Review contribution rates every time your salary increases. The most sustainable way to increase pension savings is to redirect a proportion of every pay rise into pension contributions. Increasing contributions before the higher net pay arrives in your account means you never miss it. Even a 1% increase per year compounds dramatically over a career.

CONCLUSION

The most dangerous words in UK retirement planning are 'I'm sorted.' Auto-enrolment has created a system in which doing nothing is the default — and in which doing nothing feels, for most working people, like doing enough. It is not. The median pension pot of £32,700 is not a rounding error from the £375,000 required for a moderate retirement — it is an order of magnitude smaller. Forty-three per cent of working-age Britons are undersaving for retirement. And the comfortable illusion created by automated contributions, annual statements, and rising nominal pot values is actively preventing the urgency that the data demands.The stability-over-status framework that is reshaping UK attitudes to money — debt-free living, financial resilience, long-term security over short-term display — applies with full force to retirement planning. The most important thing a working person can do for their future financial security is to look honestly at the gap between their current pension trajectory and the retirement income they actually want, and to take deliberate steps to close it. Check your State Pension forecast. Find your lost pots. Maximise your employer match. Increase contributions when your salary rises. These are not exciting actions. But they are the ones that determine whether the last decades of your life are spent in financial dignity or financial constraint.

Frequently Asked Questions

What is the average pension pot in the UK in 2026?

The median pension pot across all UK ages is approximately £32,700, according to analysis drawing on ONS Wealth and Assets Survey data. This figure is significantly below the amounts needed for a comfortable or even moderate retirement. The average (mean) figure is pulled upward by a small number of high earners and is not a useful benchmark — the median is the most honest guide to what a typical British saver has accumulated. By age group, the median pots are approximately: 25–34: £18,800; 35–44: £39,500; 45–54: £75,000; 55–64: £107,000. At every age group, the typical saver is significantly behind the target needed for a moderate retirement at 67.How much do I need in my pension for a comfortable retirement in the UK?

The Pensions and Lifetime Savings Association publishes annual Retirement Living Standards that provide widely used benchmarks. For 2025/26, the private pension pot needed (on top of the full State Pension of £12,547 per year) is approximately: minimum standard (£13,400/yr total): ~£89,000; moderate standard (£31,700/yr total): ~£375,000; comfortable standard (£43,100/yr total): ~£600,000. These figures assume you own your home outright and receive the full new State Pension. If you expect a partial State Pension due to NI gaps, your private pot needs to make up the difference. Use the free MoneyHelper pension calculator at moneyhelper.org.uk for a personalised projection.Is the 8% auto-enrolment minimum enough to save for retirement?

For most workers, no. DWP modelling shows that a median earner contributing only at the 8% auto-enrolment minimum from age 22 accumulates approximately £180,000 by state pension age — sufficient for the minimum PLSA living standard but well short of the £375,000 required for a moderate retirement. The Pensions Commission that designed auto-enrolment envisaged minimum contributions rising to 12–15% over time; that increase has not happened. The Government's 2025 Pensions Review acknowledged the adequacy gap but did not commit to a contribution rate increase timeline. Pension experts consistently recommend targeting contributions of 12–15% of salary (including employer contributions) for a moderate retirement outcome.What is the gender pension gap and what causes it?

The DWP's 2025 report found that women aged 55–59 have median pension wealth of approximately £81,000 compared with approximately £156,000 for men — a gap of roughly 48%. The gap is driven by interconnected structural factors: the gender pay gap (approximately 6.9% for full-time workers, ONS 2025); higher rates of part-time working among women (35% vs 13% for men); career breaks for childcare that create contribution gaps during peak earning years; and the auto-enrolment earnings threshold of £10,000, which excludes many part-time workers — disproportionately women — from automatic enrolment. These factors compound over a 30 to 40-year career to produce the substantial gap observed at pre-retirement ages.How do I find lost pension pots?

The DWP's Pension Tracing Service is the official UK tool for tracing old workplace pension pots: gov.uk/find-pension-contact-details. You provide your old employer's name and address, and the service provides the contact details of any associated pension scheme. It is free to use and can help locate pots from every previous employer. The forthcoming Pensions Dashboards Programme will eventually allow anyone to see all their pension savings in one place, but its full rollout has been subject to repeated delays. In the meantime, the Pension Tracing Service and direct contact with old employers remain the most reliable routes to finding lost pots. The Pensions Policy Institute estimates 3.3 million lost or unclaimed pots worth £31.1 billion across the UK.References

Wealthvieu — Average Pension Pot by Age UK 2026 (ONS WAS data) https://wealthvieu.com/uk/average-pension-pot-by-age/The Investors Centre — Average Pension Pot UK 2026 Statistics (DWP, PLSA, ONS) https://www.theinvestorscentre.co.uk/investing/average-pension-pot-uk/

The Investors Centre — UK Pension Statistics 2026: Key Data & Trends https://www.theinvestorscentre.co.uk/investing/statistics/pension/

PoundSense — Average Pension Pot by Age UK (PLSA Retirement Living Standards 2026) https://www.poundsense.co.uk/blog/average-pension-pot-by-age-uk

PocketWise — Average Pension Pot UK by Age 2026: Are You on Track? https://pocketwise.co.uk/pensions-and-retirement/average-pension-pot-uk-by-age/

MoneyWeek — Average Pension Pot by Age UK 2026 (PensionBee, Fidelity, ONS) https://moneyweek.com/personal-finance/pensions/average-pension-pot-by-age

Nuts About Money — Average Pension Pot UK 2026 (PLSA standards, State Pension) https://www.nutsaboutmoney.com/pensions/average-pension-pot-uk

GOV.UK — Check Your State Pension Forecast https://www.gov.uk/check-state-pension

0 Comments Comments