Budgeting

UK Budgeting Boom: Driven by Cost-of-Living Pressures

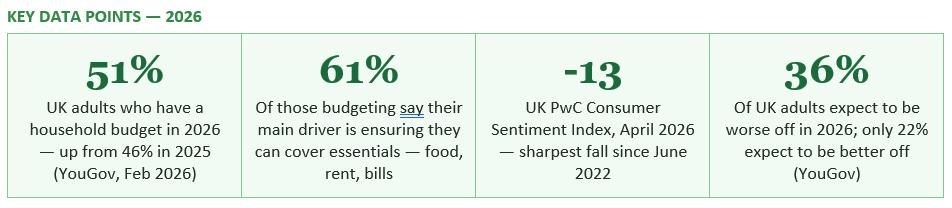

For the first time, more than half of UK adults — 51% — now have a household budget in place. That is up from 46% in 2025 and 38% in 2023. Five years of persistent inflation, rising energy bills, soaring rents, and squeezed wages have turned budgeting from an activity associated with financial hardship into a mainstream, increasingly technology-assisted habit for millions of British households. This guide examines the data behind the budgeting boom, who is driving it, and what it means for how the UK manages money in 2026.

A YouGov survey conducted in February 2026 with 2,087 nationally representative UK adults found that 51% now say they have a budget in place for 2026. This compares with 46% who reported having a budget in 2025 and an estimated 38% in 2023. In three years, the share of UK adults who actively budget has grown by 13 percentage points. For the first time, the majority of British adults are managing their spending against a plan rather than reactively.

The same survey found that 36% of UK adults expect their financial situation to be worse in 2026 than in 2025, compared with just 22% who expect improvement — an overall cautious outlook that directly translates into more deliberate financial planning. Separately, the PwC Consumer Sentiment Index, which tracks how well-off Britons feel and their future spending intentions, fell to -13 in April 2026 — its sharpest single-quarter decline since June 2022, the month when UK inflation was first rising sharply following Russia's invasion of Ukraine.

These numbers tell a coherent story: five years of cost of living pressure have pushed a majority of UK households across a threshold from reactive financial management to proactive budgeting. This is not just a statistical artefact — it reflects a genuine, observable change in financial behaviour that has significant implications for how the UK personal finance market will develop in the years ahead.

Financial expectations are translating into greater use of budgets. Just over half of UK adults — 51% — say they have a budget for 2026, an increase from 46% who say they had a budget in 2025.

— YOUGOV UK FINANCIAL OUTLOOK SURVEY, FEBRUARY 2026 (2,087 ADULTS)

The finding that 18 to 24-year-olds are the most likely age group to have a budget — at 58%, ahead of all other groups — is one of the most significant in the YouGov data and deserves particular attention. Far from being financially disengaged, the youngest UK adults are the most actively planning their spending. This reflects the structural position of under-35s in the UK economy in 2026: they are the generation most exposed to high rents (having entered the housing market during or after the rent inflation surge), most likely to be on entry-level salaries, most burdened by student loan repayments, and least likely to have the savings buffers that older households have accumulated. As the PocketWise analysis of the cost of living crisis notes, there was a 20% fall in those under 35 who feel 'financially healthy' and a 9% rise in young people struggling to pay bills.

4. What UK Households Are Cutting — and What They Are Protecting

The YouGov data provides a granular picture of exactly where UK households are planning to cut spending in 2026, and crucially, what they are prioritising. Among the 36% of adults who expect their finances to worsen, the intended cutbacks are widespread and hit discretionary categories hardest.

Two findings in this data stand out. First, only 16% of households expect to cut back on housing or bill-related spending — reflecting both that these costs are perceived as non-discretionary and that the options for reducing them (remortgaging, moving to cheaper accommodation, switching energy supplier) are limited or already exhausted for many. Second, even in the group expecting their finances to improve, 44% still plan to cut back on eating and drinking out — suggesting that the behavioural shift toward more deliberate spending is happening across income groups, not just among those under acute financial pressure.

Among those budgeting in 2026, 39% use manual tools such as spreadsheets or pen and paper. Only 9% report using dedicated budgeting apps. This suggests that the UK budgeting boom is being powered primarily by people picking up a spreadsheet or a notebook and doing it themselves — not by a mass adoption of fintech budgeting tools. For the personal finance technology sector, this represents a significant gap between potential adoption and actual uptake that has not yet been bridged.

The reasons for the low app adoption are multiple: awareness gaps (many people are not familiar with the UK budgeting apps available to them), trust concerns (sharing open banking access to all accounts with a third-party app is a step many people are not ready to take), and the perceived complexity of setting up and maintaining a dedicated budgeting tool versus the simplicity of a spreadsheet that does exactly what you need and no more.

The 39% manual budgeting figure is also a baseline, not a ceiling. Awareness and adoption of budgeting apps in the UK has been rising consistently, driven in part by the open banking ecosystem that gives UK-regulated apps a significant technical advantage over those in most other markets. With Moneyhub — previously one of the larger UK personal finance apps — closing its consumer service in August 2026, its former users are actively seeking alternatives, and this transition is expected to accelerate adoption of newer platforms including Emma, Snoop, Plum, and the newly launched earmarkIQ.

The leading UK budgeting apps in 2026 each take a different approach. Emma focuses on spending categorisation and subscription tracking, making it easy to see where money is going and identify subscriptions that have crept up or are no longer used. Snoop specialises in bill comparison and switching alerts, using your transaction data to identify when you are overpaying for utilities, insurance, or other recurring costs. Plum automates savings and bill payments based on AI analysis of your cash flow, and also provides automatic round-up saving. Monzo and Starling — both FCA-regulated current account providers — have built increasingly sophisticated budgeting features (spending pots, salary sorters, automatic savings rules) directly into their banking apps, reducing the need for a separate budgeting tool for their customers.

earmarkIQ, launching on iOS in May 2026, introduces what it describes as AI-powered zero-based budgeting — allocating every pound of your income to a specific purpose before spending begins. The zero-based approach, best known from YNAB (You Need A Budget), has a strong evidence base for transforming financial behaviour in households that commit to it. The earmarkIQ implementation attempts to automate the most labour-intensive aspects of this method using AI and open banking data, potentially making a highly effective but historically demanding budgeting methodology accessible to a much wider audience.

For consumers choosing between these options, the earmarkIQ guide to UK budgeting apps notes that most apps do 'one or two things well and leave you needing three different apps for a complete picture' — a fragmentation problem that the next generation of AI-powered tools is attempting to solve with more holistic, joined-up financial management.

The cost of living crisis has, paradoxically, forced a more open and active relationship with money for millions of households. When the gap between income and outgoings becomes acute enough, avoidance is no longer sustainable — and the shift from avoidance to engagement, from shame to strategy, is one of the less-discussed but important cultural effects of the past five years of financial pressure. The YouGov finding that 41% of people budgeting in 2026 are doing so specifically to stop overspending — not just to cover essentials — suggests that a significant portion of the budgeting boom reflects genuine attitudinal change rather than crisis management alone.

This cultural shift is also visible in the explosion of personal finance content on social media. The 'FinTok' phenomenon on TikTok — personal finance creators sharing budgeting methods, savings challenges, and financial tips — has brought money management content to audiences who would never have sought it out in traditional personal finance formats. The normalisation of discussing money openly, particularly among younger adults, is a meaningful change from the culture of a decade ago and helps explain why 18 to 24-year-olds are now the most likely age group to have a formal budget.

The budgeting boom also signals something more enduring than a crisis response. The cultural shift — the growing openness about personal finances, the normalisation of budgeting as a mainstream activity rather than a sign of hardship, the rise of FinTok and financial content among young adults — suggests that the UK's relationship with money management is changing in ways that will persist even if the immediate cost of living pressures ease. The generation that learned to budget during the 2021–2026 inflation era is unlikely to abandon that habit when conditions improve. That is arguably the most positive legacy of one of the most financially challenging periods in recent British history.

The Week — How Your Household Budget Could Look in 2026 (December 2025) https://theweek.com/personal-finance/how-your-household-budget-could-look-in-2026

UK News Blog — UK Cost of Living 2026: New Inflation Shock Hits Households https://www.uknewsblog.co.uk/uk-cost-of-living-2026-new-inflation-shock-hits-households/

House of Commons Library — High Cost of Living: Impact on Households (January 2026) https://researchbriefings.files.parliament.uk/documents/CBP-10100/CBP-10100.pdf

GOV.UK — Budget 2025 Fact Sheet: Cutting the Cost of Living https://www.gov.uk/government/news/budget-2025-fact-sheet-cutting-the-cost-of-living

NimbleFins — Average UK Household Budget 2026 (ONS data, updated January 2026) https://www.nimblefins.co.uk/average-uk-household-budget

earmarkIQ — 7 Best Budgeting Apps UK 2026: Ranked and Reviewed (April 2026) https://earmarkiq.app/blog/best-budgeting-apps-uk

PocketWise — Cost of Living Crisis UK: What Caused It and What You Can Do https://pocketwise.co.uk/money-budgeting/economy-explained/cost-of-living-crisis-uk-guide/

StepChange Debt Charity — Free UK Debt and Budgeting Advice https://www.stepchange.org

Turn2Us — Benefits Entitlement Calculator https://www.turn2us.org.uk

TABLE OF CONTENTS

- The Budgeting Boom in Numbers: What the Data Shows

- Why Now? The Five Pressures Driving the Shift

- Who Is Budgeting and Who Is Not

- What UK Households Are Cutting — and What They Are Protecting

- How UK Households Are Budgeting: Tools and Methods

- The Rise of the Budgeting App in the UK

- The 50/30/20 Rule and Other Budgeting Frameworks That Work

- The Psychological Shift: From Shame to Strategy

- What Support Is Available for Households Under Pressure

- How to Build a Budget That Actually Works in 2026

- Conclusion

- Frequently Asked Questions

- References

The Budgeting Boom in Numbers: What the Data Shows

For most of recent British financial history, budgeting was something people associated with debt problems, benefit claims, or being 'bad with money.' It carried a stigma that kept many financially squeezed households from doing it openly or systematically. That stigma is breaking down — and the speed of the shift is remarkable.A YouGov survey conducted in February 2026 with 2,087 nationally representative UK adults found that 51% now say they have a budget in place for 2026. This compares with 46% who reported having a budget in 2025 and an estimated 38% in 2023. In three years, the share of UK adults who actively budget has grown by 13 percentage points. For the first time, the majority of British adults are managing their spending against a plan rather than reactively.

The same survey found that 36% of UK adults expect their financial situation to be worse in 2026 than in 2025, compared with just 22% who expect improvement — an overall cautious outlook that directly translates into more deliberate financial planning. Separately, the PwC Consumer Sentiment Index, which tracks how well-off Britons feel and their future spending intentions, fell to -13 in April 2026 — its sharpest single-quarter decline since June 2022, the month when UK inflation was first rising sharply following Russia's invasion of Ukraine.

These numbers tell a coherent story: five years of cost of living pressure have pushed a majority of UK households across a threshold from reactive financial management to proactive budgeting. This is not just a statistical artefact — it reflects a genuine, observable change in financial behaviour that has significant implications for how the UK personal finance market will develop in the years ahead.

Financial expectations are translating into greater use of budgets. Just over half of UK adults — 51% — say they have a budget for 2026, an increase from 46% who say they had a budget in 2025.

— YOUGOV UK FINANCIAL OUTLOOK SURVEY, FEBRUARY 2026 (2,087 ADULTS)

Why Now? The Five Pressures Driving the Shift

The UK's budgeting boom is not the product of a single event or policy. It is the cumulative result of five distinct but reinforcing financial pressures that have converged over the past five years and that show no sign of fully reversing in 2026.Pressure 1: Sustained inflation above target

UK consumer prices peaked at 11.1% annual inflation in October 2022 — a 41-year high — before falling gradually to 3.0% in February 2026 and ticking back up to 3.3% in March 2026. Despite this moderation, prices are approximately 25% higher than they were in early 2020. Crucially, slower inflation does not mean prices are falling — it means they are rising more slowly on top of an already elevated base. Every month that passes with inflation above the 2% target adds permanently to the cost of living without any corresponding automatic adjustment in incomes. The Bank of England has forecast CPI remaining between 3% and 3.5% through the second and third quarters of 2026, partly due to the energy price impact of the Iran conflict.Pressure 2: Energy bills structurally higher

The Ofgem energy price cap stood at approximately £1,849 per year in April 2026, compared with approximately £1,280 before the energy crisis. The promise of a sustained return to pre-crisis energy prices has not materialised — and the Iran conflict's upward pressure on global gas prices suggests the near-term outlook remains elevated. Average utilities costs for a UK household have reached approximately £4,200 per year according to NimbleFins analysis of ONS data, representing a significant permanent increase in fixed household costs.Pressure 3: Housing costs — rents and mortgages

UK private rents rose approximately 30% between 2022 and early 2026. Average UK rents reached £1,336 per month nationally according to ONS data for December 2025, with London substantially higher. For mortgage holders, the transition from pandemic-era fixed rates of 1–2% to current rates of around 6% has added hundreds of pounds per month to housing costs for those remortgaging. The House of Commons Library notes that around 30% of UK households have a mortgage, and those coming off fixed rates in 2026 face materially higher monthly payments.Pressure 4: Wages not fully recovering lost ground

UK average weekly earnings grew 3.6% in the three months to February 2026 against a CPI of 3.0% — a small positive real gain. However, this recent positive trend follows two years (October 2021 to June 2023) in which wage growth consistently failed to keep pace with inflation, meaning real wages fell materially. Workers in the lowest income quartile have seen little to no inflation-adjusted wage growth over the full post-pandemic period, even as headline wages appear to have recovered. The National Living Wage rose to £12.71 per hour for over-21s from April 2026, benefiting approximately 2.4 million workers — but this still falls short of the voluntary Real Living Wage of £13.45 (£14.80 in London).Pressure 5: Renewed economic anxiety in 2026

The Iran conflict's impact on global energy prices has injected fresh uncertainty into UK household finances at a point when many households were beginning to recover from the 2021–2023 crisis. The British Retail Consortium has forecast food price inflation remaining above 5% in 2026, the PwC Consumer Sentiment Index has fallen to its lowest since mid-2022, and approximately 80% of UK consumers say they plan to reduce non-essential spending over the next three months.Who Is Budgeting and Who Is Not

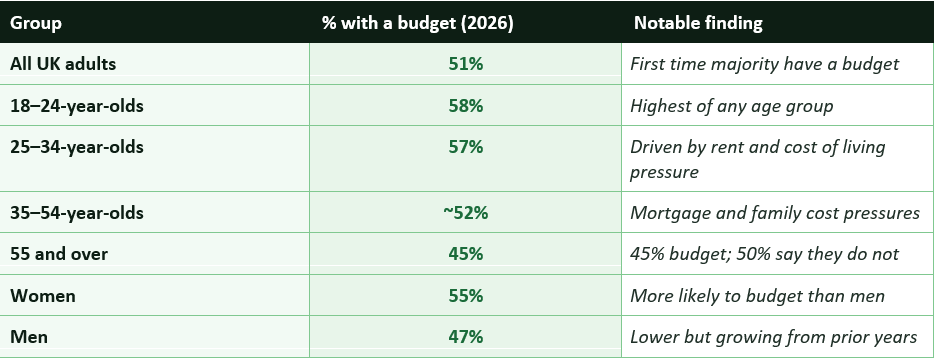

The YouGov 2026 data allows a detailed picture of the demographics of the UK budgeting boom. The findings challenge several assumptions about who budgets and reveal important gaps.The finding that 18 to 24-year-olds are the most likely age group to have a budget — at 58%, ahead of all other groups — is one of the most significant in the YouGov data and deserves particular attention. Far from being financially disengaged, the youngest UK adults are the most actively planning their spending. This reflects the structural position of under-35s in the UK economy in 2026: they are the generation most exposed to high rents (having entered the housing market during or after the rent inflation surge), most likely to be on entry-level salaries, most burdened by student loan repayments, and least likely to have the savings buffers that older households have accumulated. As the PocketWise analysis of the cost of living crisis notes, there was a 20% fall in those under 35 who feel 'financially healthy' and a 9% rise in young people struggling to pay bills.

4. What UK Households Are Cutting — and What They Are Protecting

The YouGov data provides a granular picture of exactly where UK households are planning to cut spending in 2026, and crucially, what they are prioritising. Among the 36% of adults who expect their finances to worsen, the intended cutbacks are widespread and hit discretionary categories hardest.

Two findings in this data stand out. First, only 16% of households expect to cut back on housing or bill-related spending — reflecting both that these costs are perceived as non-discretionary and that the options for reducing them (remortgaging, moving to cheaper accommodation, switching energy supplier) are limited or already exhausted for many. Second, even in the group expecting their finances to improve, 44% still plan to cut back on eating and drinking out — suggesting that the behavioural shift toward more deliberate spending is happening across income groups, not just among those under acute financial pressure.

How UK Households Are Budgeting: Tools and Methods

One of the most revealing findings in the YouGov 2026 data is the breakdown of budgeting tools UK adults are using. Despite the growth of sophisticated financial apps and open banking technology, manual methods dominate.Among those budgeting in 2026, 39% use manual tools such as spreadsheets or pen and paper. Only 9% report using dedicated budgeting apps. This suggests that the UK budgeting boom is being powered primarily by people picking up a spreadsheet or a notebook and doing it themselves — not by a mass adoption of fintech budgeting tools. For the personal finance technology sector, this represents a significant gap between potential adoption and actual uptake that has not yet been bridged.

The reasons for the low app adoption are multiple: awareness gaps (many people are not familiar with the UK budgeting apps available to them), trust concerns (sharing open banking access to all accounts with a third-party app is a step many people are not ready to take), and the perceived complexity of setting up and maintaining a dedicated budgeting tool versus the simplicity of a spreadsheet that does exactly what you need and no more.

The 39% manual budgeting figure is also a baseline, not a ceiling. Awareness and adoption of budgeting apps in the UK has been rising consistently, driven in part by the open banking ecosystem that gives UK-regulated apps a significant technical advantage over those in most other markets. With Moneyhub — previously one of the larger UK personal finance apps — closing its consumer service in August 2026, its former users are actively seeking alternatives, and this transition is expected to accelerate adoption of newer platforms including Emma, Snoop, Plum, and the newly launched earmarkIQ.

The Rise of the Budgeting App in the UK

The UK has a uniquely favourable environment for personal finance apps, thanks to the open banking framework introduced by the FCA from 2018. Open banking allows FCA-authorised apps to connect securely to all your bank accounts (with your explicit consent), giving them a complete, real-time view of your spending across multiple providers. This is the data infrastructure that makes sophisticated, personalised budgeting assistance possible.The leading UK budgeting apps in 2026 each take a different approach. Emma focuses on spending categorisation and subscription tracking, making it easy to see where money is going and identify subscriptions that have crept up or are no longer used. Snoop specialises in bill comparison and switching alerts, using your transaction data to identify when you are overpaying for utilities, insurance, or other recurring costs. Plum automates savings and bill payments based on AI analysis of your cash flow, and also provides automatic round-up saving. Monzo and Starling — both FCA-regulated current account providers — have built increasingly sophisticated budgeting features (spending pots, salary sorters, automatic savings rules) directly into their banking apps, reducing the need for a separate budgeting tool for their customers.

earmarkIQ, launching on iOS in May 2026, introduces what it describes as AI-powered zero-based budgeting — allocating every pound of your income to a specific purpose before spending begins. The zero-based approach, best known from YNAB (You Need A Budget), has a strong evidence base for transforming financial behaviour in households that commit to it. The earmarkIQ implementation attempts to automate the most labour-intensive aspects of this method using AI and open banking data, potentially making a highly effective but historically demanding budgeting methodology accessible to a much wider audience.

For consumers choosing between these options, the earmarkIQ guide to UK budgeting apps notes that most apps do 'one or two things well and leave you needing three different apps for a complete picture' — a fragmentation problem that the next generation of AI-powered tools is attempting to solve with more holistic, joined-up financial management.

The 50/30/20 Rule and Other Budgeting Frameworks That Work

Whether using an app, a spreadsheet, or pen and paper, the households that report the most benefit from budgeting are generally those who use a consistent framework rather than simply tracking spending after the fact. Three frameworks dominate personal finance discussion in 2026.The 50/30/20 rule

The 50/30/20 rule divides after-tax income into three categories: 50% to needs (rent/mortgage, food, utilities, transport, minimum debt payments), 30% to wants (eating out, entertainment, subscriptions, clothing), and 20% to savings and debt repayment above the minimum. It is the most widely recommended starting framework because it is simple to apply, easy to explain, and immediately reveals whether a household's cost structure is sustainable. A household spending 70% of income on needs — as many low-to-middle income UK households do in 2026 given high rent and energy costs — can see immediately that the 20% savings target requires either a cut to wants or an increase in income.Zero-based budgeting

Zero-based budgeting (ZBB) requires you to allocate every pound of your income to a specific purpose before the month begins, so that income minus all allocations equals zero. Nothing is left unassigned. This is the most demanding of the common approaches and the one with the most transformative results for households that commit to it. YNAB's own data, based on users who connect their accounts and use the app actively for 90 days, shows an average saving of over $600 in the first two months. The principle works because it forces a decision about every pound — housing, food, debt, entertainment, and savings all compete explicitly for the available money rather than some categories expanding implicitly at the expense of others.Envelope budgeting (digital and physical)

The envelope method — allocating a fixed cash amount to each spending category at the start of the month and spending only from that envelope until it is empty — predates all digital tools but remains highly effective. Many budgeting apps implement a digital version of this approach (Monzo's spending pots, YNAB's category allocations, earmarkIQ's salary allocation). The psychological power of the method is that it makes the trade-off between categories concrete and visible in a way that a bank balance does not.The Psychological Shift: From Shame to Strategy

One of the most significant aspects of the UK budgeting boom is what it reveals about changing attitudes to personal finance. In the UK, money has traditionally been a subject surrounded by social taboo — more difficult to discuss openly than almost any other personal matter. This cultural reluctance to engage openly with personal finances has historically contributed to avoidant financial behaviour, where many households managed anxiety about money by not looking too closely at it.The cost of living crisis has, paradoxically, forced a more open and active relationship with money for millions of households. When the gap between income and outgoings becomes acute enough, avoidance is no longer sustainable — and the shift from avoidance to engagement, from shame to strategy, is one of the less-discussed but important cultural effects of the past five years of financial pressure. The YouGov finding that 41% of people budgeting in 2026 are doing so specifically to stop overspending — not just to cover essentials — suggests that a significant portion of the budgeting boom reflects genuine attitudinal change rather than crisis management alone.

This cultural shift is also visible in the explosion of personal finance content on social media. The 'FinTok' phenomenon on TikTok — personal finance creators sharing budgeting methods, savings challenges, and financial tips — has brought money management content to audiences who would never have sought it out in traditional personal finance formats. The normalisation of discussing money openly, particularly among younger adults, is a meaningful change from the culture of a decade ago and helps explain why 18 to 24-year-olds are now the most likely age group to have a formal budget.

What Support Is Available for Households Under Pressure

For households who are budgeting out of necessity rather than choice — those struggling to cover essential costs despite careful management — the 2025 Autumn Budget introduced several measures designed to ease pressure in 2026.Government and institutional support available to UK households in 2026

- National Living Wage increase: From April 2026, the National Living Wage rose to £12.71 per hour for over-21s, benefiting approximately 2.4 million workers. Full-time workers on the National Living Wage see an annual increase of approximately £900.

- State pension increase: Under the triple lock, the full new State Pension rose by 4.8% to £12,548 per year from April 2026, benefiting all pensioners on the full new State Pension.

- Two-child benefit limit removal: From April 2026, the two-child benefit limit has been removed in full, benefiting families with three or more children who were previously restricted from receiving Child Tax Credit or the child element of Universal Credit for third or subsequent children. This is expected to lift 450,000 children out of poverty.

- Universal Credit standard allowance increase: The UC standard allowance for a single person aged 25+ rose by approximately £295 per year from April 2026 — around £110 more than it would have been if uprated by inflation alone.

- Rail fare freeze: Regulated rail fares in England were frozen by the government, saving commuters hundreds of pounds on annual season tickets.

- Energy bill levy removal: The Autumn Budget removed certain energy levies to save families an average of £150 per year, with up to £300 for some lower-income households.

- Free debt advice: StepChange (stepchange.org) and Citizens Advice (citizensadvice.org.uk) both provide free, confidential debt and budgeting advice for households struggling with their finances. These services are completely free and are available online, by phone, and face-to-face.

- Benefits entitlement check: Millions of UK households are not claiming all benefits to which they are entitled. Use the Turn2Us benefits calculator (turn2us.org.uk) or entitledto.co.uk to check your entitlement.

How to Build a Budget That Actually Works in 2026

The most important thing about a budget is that you use it — consistently and with enough detail to change your behaviour. The best budgeting system is always the one you will actually follow. Here is a practical, straightforward approach for 2026.Steps

- Calculate your true monthly after-tax income: Include all sources — salary after tax and NI, any Universal Credit, Child Benefit, maintenance payments, freelance income. Use your actual take-home pay, not your gross salary.

- List all fixed monthly outgoings: Rent or mortgage, all direct debits and standing orders, minimum debt payments, subscriptions. Check your bank statement for the last three months to catch anything you have forgotten. This is often where people first notice subscriptions they no longer use.

- Calculate variable essential costs: Estimate your monthly spend on food, fuel/transport, utilities (if not on a fixed direct debit), and clothing essentials. Use three months of bank statements to get a realistic average.

- Check where you stand: Income minus fixed outgoings minus variable essentials. If the result is negative, you have a structural gap that needs addressing — either by increasing income, reducing fixed costs (switching energy or broadband, remortgaging), or cutting variable essentials. If it is positive, that surplus needs to be deliberately allocated.

- Allocate the surplus: Assign every pound of surplus to a specific purpose before the month begins — emergency fund building, debt repayment, savings, and then discretionary spending. The amount left for discretionary spending is your true budget for eating out, entertainment, and personal spending.

- Track and review weekly: At the end of each week, compare actual spending to budget. Most budgeting apps do this automatically. A weekly review catches problems early — before an overspend in one category has derailed the whole month.

- Revisit the budget when circumstances change: A pay rise, a bill increase, a new subscription, a change in travel costs — any change in income or outgoings should trigger a budget review. A budget based on last year's costs will not work for this year's prices.

CONCLUSION

The UK budgeting boom of 2026 is a direct, rational response to five years of sustained financial pressure. When prices rise 25%, energy bills increase by 45%, rents climb by 30%, and mortgage payments jump by hundreds of pounds a month, the households that survive and recover best are those that manage their money deliberately. The YouGov data confirms that this is precisely what is happening: a majority of UK adults now budget, the youngest adults are the most engaged, and the primary motivation is ensuring essential costs are covered rather than simply optimising discretionary spending.The budgeting boom also signals something more enduring than a crisis response. The cultural shift — the growing openness about personal finances, the normalisation of budgeting as a mainstream activity rather than a sign of hardship, the rise of FinTok and financial content among young adults — suggests that the UK's relationship with money management is changing in ways that will persist even if the immediate cost of living pressures ease. The generation that learned to budget during the 2021–2026 inflation era is unlikely to abandon that habit when conditions improve. That is arguably the most positive legacy of one of the most financially challenging periods in recent British history.

Frequently Asked Questions

How many UK adults have a budget in 2026?

According to YouGov's survey of 2,087 nationally representative UK adults conducted in February 2026, 51% of UK adults say they have a budget in place for 2026. This compares with 46% in 2025 and an estimated 38% in 2023, representing a significant and accelerating increase in the share of UK adults actively managing their spending against a plan. For the first time, a majority of British adults have a budget.Why are young people in the UK the most likely to budget?

YouGov's 2026 data shows that 58% of 18 to 24-year-olds and 57% of 25 to 34-year-olds have a budget — the highest proportions of any age group. This reflects the structural financial pressures on under-35s in 2026: they are the generation most exposed to high private rents (having entered the rental market during or after the rent inflation surge), most likely to be on entry-level salaries, most burdened by student loan repayments under Plans 2 and 5, and least likely to have savings buffers accumulated before the cost of living crisis. The PocketWise analysis of cost of living data notes a 20% fall in the number of under-35s who feel 'financially healthy' and a 9% rise in young people struggling to pay bills.What tools do UK households use to budget?

According to YouGov 2026 data, 39% of those budgeting use manual tools such as spreadsheets or pen and paper, while only 9% use dedicated budgeting apps. The majority of the UK budgeting boom is therefore driven by people doing it manually rather than through fintech adoption. Popular budgeting apps available in the UK include Emma (spending categorisation), Snoop (bill comparison), Plum (automated savings), and Monzo or Starling (budgeting features within challenger bank accounts). earmarkIQ, launching in mid-2026, offers AI-powered zero-based budgeting.What are the main reasons UK adults give for budgeting in 2026?

YouGov's February 2026 survey found that 61% of those budgeting in 2026 say their primary motivation is to ensure they have enough money for essentials such as food, rent, and bills. The second most common reason is to increase savings (43%), followed by stopping overspending (41%). The dominance of 'covering essentials' as the primary driver confirms that the budgeting boom is primarily a response to sustained cost of living pressure rather than a proactive financial optimisation choice.What spending categories are UK households cutting in 2026?

Among those expecting their finances to worsen in 2026, YouGov data shows the largest intended cutbacks are: eating and drinking out (62%), clothing and fashion (52%), everyday conveniences such as takeaway coffee or taxis (47%), events and days out (44%), holidays and travel (40%), and subscriptions (39%). Even among those expecting their finances to improve, 44% plan to cut back on eating and drinking out and 32% on everyday conveniences — suggesting the behavioural shift toward deliberate spending is cross-income. Only 16% plan to cut back on housing or bill spending, reflecting that these costs are largely seen as fixed.What government support is available for households struggling with costs in 2026?

Several measures took effect from April 2026: the National Living Wage rose to £12.71/hour (up £900 per year for full-time workers); the State Pension rose by 4.8% to £12,548 per year; the two-child benefit limit was removed, lifting an estimated 450,000 children out of poverty; Universal Credit standard allowances increased by approximately £295 per year for single adults; and regulated rail fares in England were frozen. Energy bill levies were also removed, saving an average of £150 per household. For free budgeting and debt advice, StepChange (stepchange.org) and Citizens Advice (citizensadvice.org.uk) are available at no charge. Use Turn2Us (turn2us.org.uk) to check your full benefits entitlement.References

YouGov — UK Financial Outlook 2026: Consumer Spending Trends, Budgeting Habits and Financial Expectations (Feb 2026) https://yougov.com/en-gb/articles/54168-uk-financial-outlook-2026-consumer-spending-trends-budgeting-habits-and-financial-expectationsThe Week — How Your Household Budget Could Look in 2026 (December 2025) https://theweek.com/personal-finance/how-your-household-budget-could-look-in-2026

UK News Blog — UK Cost of Living 2026: New Inflation Shock Hits Households https://www.uknewsblog.co.uk/uk-cost-of-living-2026-new-inflation-shock-hits-households/

House of Commons Library — High Cost of Living: Impact on Households (January 2026) https://researchbriefings.files.parliament.uk/documents/CBP-10100/CBP-10100.pdf

GOV.UK — Budget 2025 Fact Sheet: Cutting the Cost of Living https://www.gov.uk/government/news/budget-2025-fact-sheet-cutting-the-cost-of-living

NimbleFins — Average UK Household Budget 2026 (ONS data, updated January 2026) https://www.nimblefins.co.uk/average-uk-household-budget

earmarkIQ — 7 Best Budgeting Apps UK 2026: Ranked and Reviewed (April 2026) https://earmarkiq.app/blog/best-budgeting-apps-uk

PocketWise — Cost of Living Crisis UK: What Caused It and What You Can Do https://pocketwise.co.uk/money-budgeting/economy-explained/cost-of-living-crisis-uk-guide/

StepChange Debt Charity — Free UK Debt and Budgeting Advice https://www.stepchange.org

Turn2Us — Benefits Entitlement Calculator https://www.turn2us.org.uk

0 Comments Comments