Financial Literacy

Your Salary After Tax 2026/27: UK vs US Comparison

TABLE OF CONTENTS

- How the UK Tax System Works in 2026/27

- How the US Tax System Works in 2026

- The Surprising Difference: Effective vs Marginal Rates

- UK Worked Examples: £30k, £50k and £75k

- US Worked Examples: $50k, $75k and $100k

- Side-by-Side Comparison at Equivalent Salaries

- The Hidden Extras: What Else Reduces Your Pay

- Scotland: A Different Picture

- How to Reduce Your Tax Bill Legally

- Conclusion

- Frequently Asked Questions

- References

How the UK Tax System Works in 2026/27

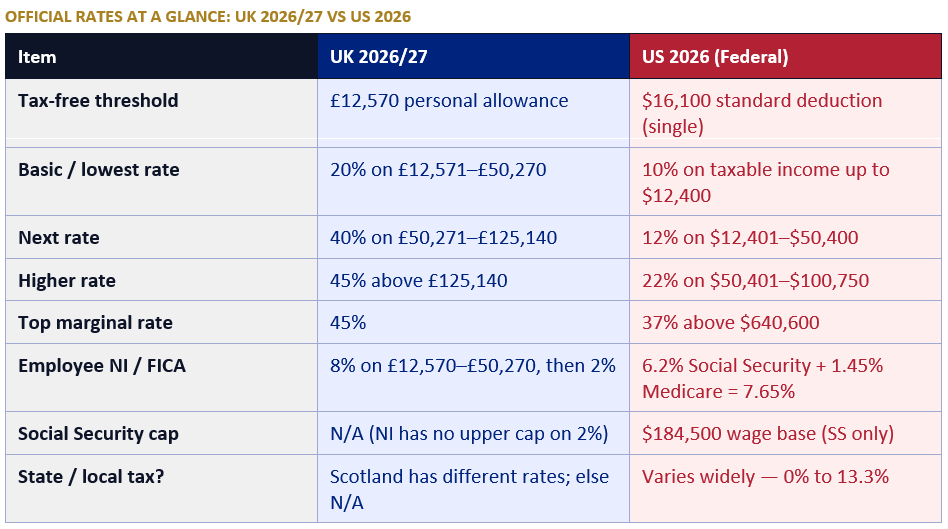

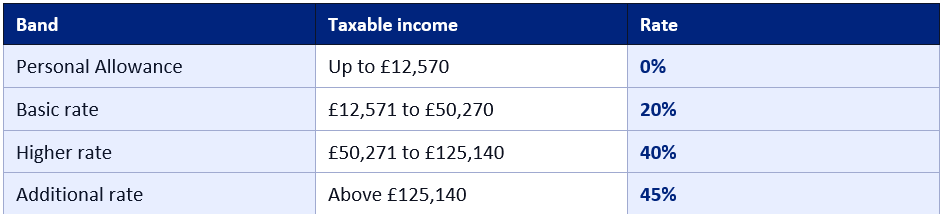

The UK tax year runs from 6 April to 5 April. For 2026/27, the headline income tax rates and thresholds are unchanged from the previous year, continuing a freeze on personal allowances and rate bands that has been in place since April 2022 and is now set to run until April 2031.Income Tax

Every UK taxpayer has a Personal Allowance — the amount they can earn before paying any income tax. For 2026/27, this is £12,570. Above that threshold, income tax is charged at three main rates (for England, Wales and Northern Ireland):

Important: If your adjusted net income exceeds £100,000, your personal allowance reduces by £1 for every £2 earned above that threshold. The allowance disappears entirely at £125,140, which creates an effective 60% marginal rate on income between £100,000 and £125,140 — one of the most poorly understood features of the UK tax system.

National Insurance Contributions (NICs)

In addition to income tax, most employed workers pay National Insurance. For 2026/27, employees pay NICs at 8% on earnings between the Primary Threshold (£12,570 per year, aligned with the personal allowance) and the Upper Earnings Limit (£50,270 per year). Earnings above £50,270 attract a reduced rate of just 2%. Importantly, these rates and thresholds are unchanged from 2025/26.This means that for a basic-rate taxpayer earning between £12,570 and £50,270, the combined marginal rate is actually 28%: 20% income tax plus 8% NI. It is this combined rate — not 20% as many people assume — that determines how much of each extra pound you keep.

How the US Tax System Works in 2026

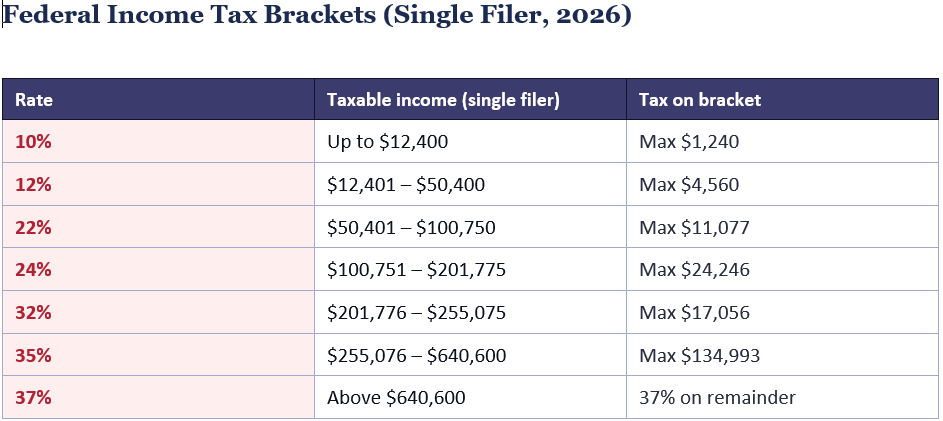

The US federal income tax system uses seven progressive brackets. Under the One Big Beautiful Bill Act (OBBBA), passed in July 2025, most provisions of the 2017 Tax Cuts and Jobs Act are now permanent, providing stability to the rate structure going forward. The 2026 thresholds have been adjusted upward by approximately 2.7% for inflation.Federal Income Tax Brackets (Single Filer, 2026)

The standard deduction for a single filer in 2026 is $16,100 (up from $15,750 in 2025). This means a single filer reduces their taxable income by $16,100 before any bracket rates apply. The brackets above apply to taxable income — income after the standard deduction (or itemised deductions, if higher) is subtracted.

FICA: Social Security and Medicare

On top of federal income tax, employees pay 6.2% in Social Security tax on earnings up to $184,500 (the 2026 wage base) and 1.45% in Medicare tax on all earnings, with no upper cap. Combined, this is 7.65% in FICA taxes — a figure that sits separately from federal income tax but meaningfully reduces take-home pay at all income levels. Your employer matches this 7.65%, meaning the total employment tax cost is 15.3%, though employees only see their half deducted from their pay.The Surprising Difference: Effective vs Marginal Rates

The number that surprises most people — whether they live in the UK or the US — is the difference between their marginal rate (the tax rate on their last pound or dollar of earnings) and their effective rate (the total tax actually paid as a percentage of gross income). Because both systems are progressive, the effective rate is always meaningfully lower than the marginal rate.In the UK, a person earning £50,000 might assume they are paying 40% tax because their income exceeds the higher rate threshold. In reality, only £730 of their income falls into the 40% band. Their effective income tax rate is around 20.7%, and their combined income tax and NI effective rate is around 25.5%.

For 2026/27, the combined marginal rate for a basic-rate UK taxpayer is 28% — not 20%. This is the figure that matters when deciding whether overtime, a pay rise, or freelance income is worth the effort.

— HOUSE OF COMMONS LIBRARY, DIRECT TAXES: RATES AND ALLOWANCES 2026/27

In the US, a single filer earning $75,000 falls into the 22% bracket, but their effective federal income tax rate after the standard deduction is approximately 13.3%. Add FICA (7.65%), and the total effective federal and payroll tax rate is around 21% — broadly comparable to the UK at similar income levels, before state taxes are considered.

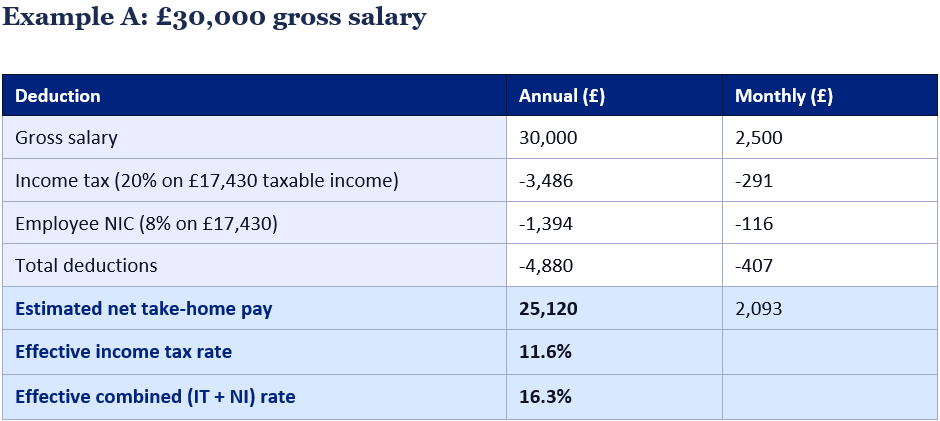

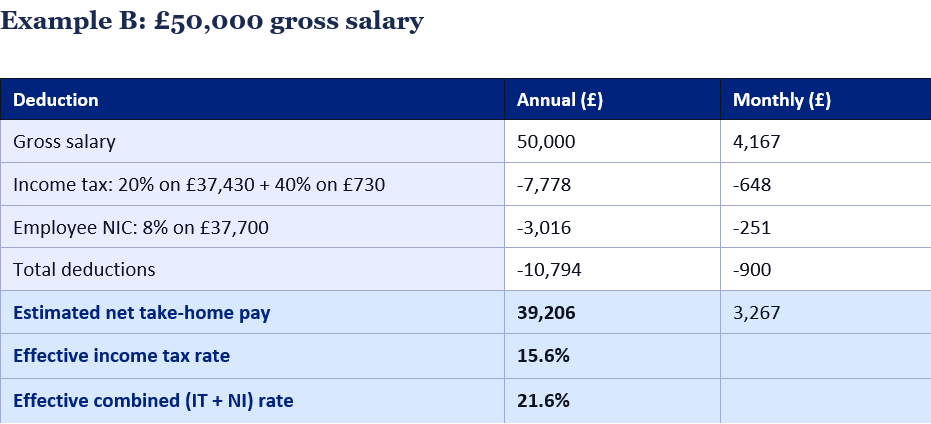

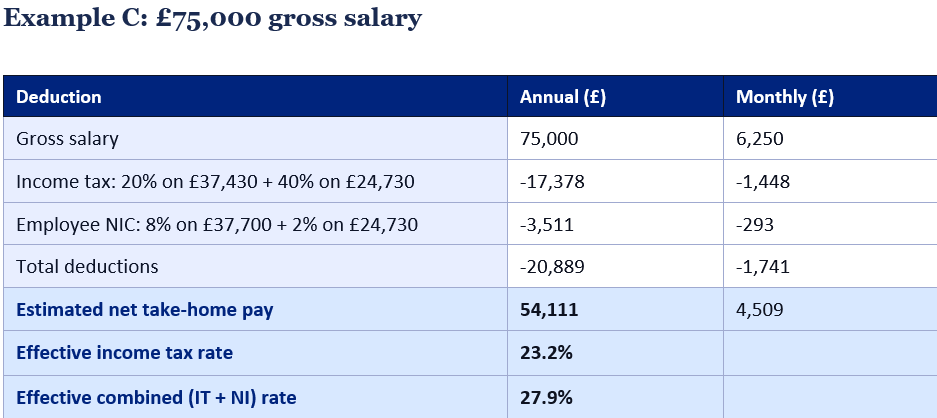

UK Worked Examples: £30k, £50k and £75k

All figures below are for the 2026/27 tax year, for a standard employee in England with the standard Personal Allowance (no pension contributions, no student loan deductions, no benefits in kind). Figures are rounded for clarity.

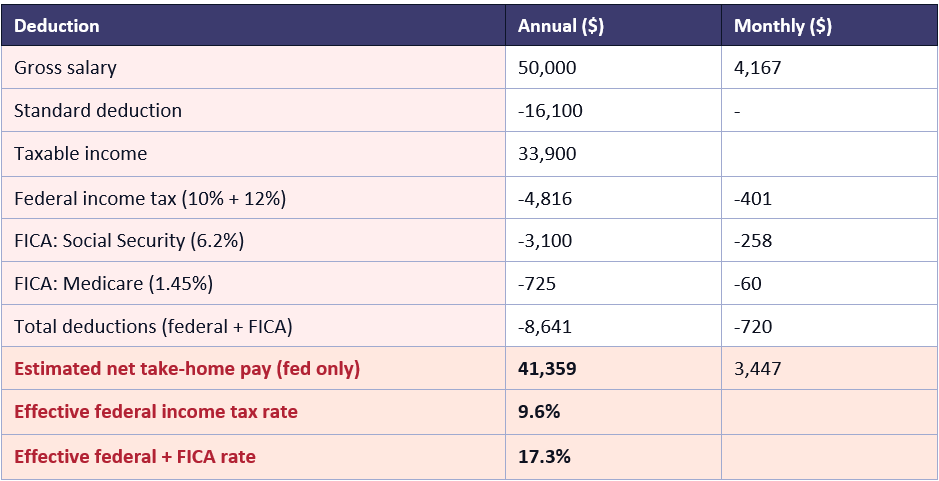

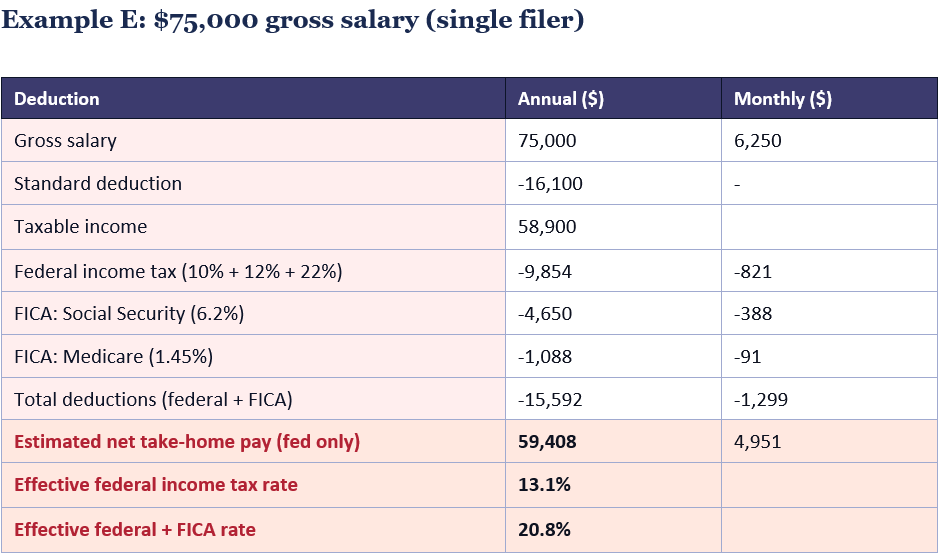

US Worked Examples: $50k, $75k and $100k

All figures are for a single filer in 2026 taking the standard deduction of $16,100, with no pre-tax deductions (no 401(k) contribution, no health insurance premium deduction). Federal income tax and FICA only — state income tax is excluded as it varies significantly by state.Example D: $50,000 gross salary (single filer)

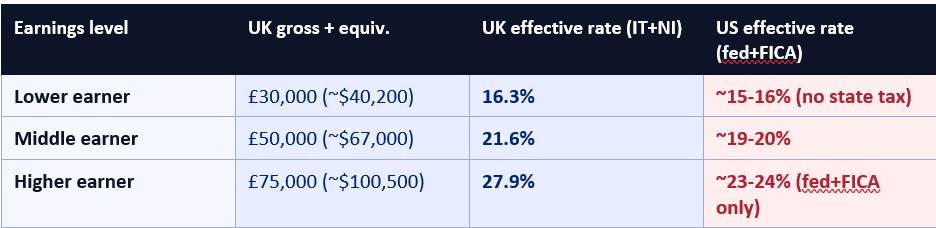

Side-by-Side Comparison at Equivalent Salaries

To compare the two systems fairly requires converting currencies. As of May 2026, the GBP/USD exchange rate is approximately 1.34. The table below uses this rate to convert equivalent UK and US salaries, allowing a direct comparison of effective total tax burdens at three earnings levels.

The surprising figure for many readers is how close the federal-only US effective rates are to UK rates at lower and middle earnings. The gap widens at higher incomes. However, US workers in most states will have state income tax on top of the federal figures shown. The average US state income tax rate is around 5%, which would push most US effective rates above UK equivalents at comparable earnings levels.

On the other hand, UK employees receive benefits funded by their NI contributions — including NHS healthcare (no co-pays at point of use), maternity and paternity pay, and ultimately the state pension — that US employees would typically need to fund privately or through employer-provided insurance. A fully loaded comparison of the total value received in exchange for taxes paid would look quite different from the raw take-home pay figures.

The Hidden Extras: What Else Reduces Your Pay

The worked examples above show income tax and NI/FICA only. In practice, additional deductions can significantly reduce take-home pay beyond these headline figures.In the UK, a student loan repayment is one of the most significant additional deductions. Plan 2 (the most common for graduates who started university after 2012) repayments begin when earnings exceed £27,295 and are charged at 9% of earnings above that threshold. A worker earning £50,000 would repay approximately £2,041 per year in Plan 2 student loan deductions — equivalent to a further 4.1 percentage points on their effective rate. Plan 5 (for students who started from 2023 onwards) has a lower threshold of £25,000, meaning repayments begin sooner.

Pension contributions are another major variable. Auto-enrolment means most UK employees are paying into a workplace pension unless they actively opt out — at a minimum contribution of 5% of qualifying earnings (usually earnings between £6,240 and £50,270). On a £50,000 salary, this is approximately £2,198 per year. The money is not lost — it builds your pension — but it does reduce current take-home pay.

In the US, comparable deductions include 401(k) contributions (up to $24,500 in 2026), which reduce taxable income as well as current take-home pay, and employer health insurance premiums. Most US workers pay a portion of their employer-provided health insurance — often $100 to $400 per month depending on the plan and employer — directly from pre-tax salary. This is a cost without a direct UK equivalent, since NHS healthcare is funded through taxation and requires no additional employee contribution.

Scotland: A Different Picture

Scotland sets its own income tax rates and bands for non-savings income. For 2026/27, Scottish taxpayers face a more complex and in some respects heavier income tax regime than the rest of the UK. Scotland has five income tax bands — starter, basic, intermediate, higher, and top — rather than the three applicable in England, Wales, and Northern Ireland.The key difference is at middle incomes. A Scottish taxpayer earning £50,000 pays income tax at 42% on income between £43,662 and £50,000 — higher than the 40% that applies at the same income level in England. The starter rate of 19% also means Scotland's lowest earners face a slightly higher rate than the 20% basic rate elsewhere, though this is partially offset by the rate applying to a smaller band of income.

National Insurance rates and thresholds for Scottish taxpayers are set by Westminster and are unchanged from the rest of the UK. So a Scottish taxpayer's NI bill is identical to that of an English taxpayer on the same salary — only the income tax differs.

How to Reduce Your Tax Bill Legally

Understanding your effective tax rate is the first step to managing it. Both the UK and US systems offer meaningful opportunities to reduce your tax liability through planning — all within the law.UK: Key ways to reduce your income tax and NI bill in 2026/27

- Pension contributions: Contributions to a workplace or personal pension attract full income tax relief. For higher-rate taxpayers, a £1,000 pension contribution costs only £600 after tax relief. Contributions also reduce your income for the purpose of the personal allowance taper at £100,000.

- ISA allowance: The annual ISA allowance is £20,000 for 2026/27 (with up to £12,000 in cash). Returns within an ISA are free of income tax and capital gains tax.

- Marriage allowance: If your income is below the personal allowance (£12,570), you can transfer up to £1,260 of your personal allowance to a basic-rate taxpayer spouse, saving up to £252 in tax.

- Salary sacrifice: Arrangements to receive benefits (such as electric vehicles or childcare) in place of salary can reduce the income and NI on which you are taxed.

- Gift Aid: Donations to charity under Gift Aid extend your basic-rate band by the grossed-up value of the donation, which can pull income out of the higher-rate band.

US: Key ways to reduce your federal tax bill in 2026

- 401(k) pre-tax contributions: Traditional 401(k) contributions (up to $24,500 in 2026, or $32,500 for age 50+) reduce your taxable income dollar-for-dollar.

- IRA contributions: Traditional IRA contributions (up to $7,500 in 2026) may be deductible depending on income and whether you have a workplace plan.

- Health Savings Account (HSA): If you have a High Deductible Health Plan, HSA contributions (up to $4,300 single / $8,550 family in 2026) are fully deductible and grow tax-free.

- Itemised deductions: If your eligible deductions (mortgage interest, state and local taxes up to $10,000, charitable gifts, medical expenses above 7.5% of AGI) exceed the $16,100 standard deduction, itemising can reduce your taxable income further.

- Roth IRA: Contributions are made with after-tax dollars but all future growth and qualified withdrawals are tax-free — valuable if you expect to be in a higher bracket in retirement.

CONCLUSION

The figure that most surprises people in both countries is the effective rate — the total deductions as a percentage of gross pay. In the UK, a £50,000 earner takes home roughly £39,206 after income tax and NI: an effective combined rate of 21.6%. In the US, a $75,000 earner (broadly equivalent before state taxes) takes home around $59,408 after federal income tax and FICA: an effective rate of 20.8% on federal deductions alone. Before state taxes, the headline difference is smaller than most people expect.The deeper surprise is what each system provides in return. UK workers get NHS healthcare, statutory sick pay, auto-enrolled pensions, and eventually the state pension from their combined income tax and NI contributions. US workers on equivalent salaries often pay significantly more for private health insurance, may need to fund their own retirement more actively, and face state income taxes that can add 3% to 10% to their total burden. The take-home pay figure is only part of the story — but it is an important place to start.

Frequently Asked Questions

What is the personal allowance in the UK for 2026/27?

The Personal Allowance — the amount you can earn before paying income tax — is £12,570 for 2026/27. This has been frozen at this level since April 2022 and is due to remain there until April 2031. If your adjusted net income exceeds £100,000, the allowance reduces by £1 for every £2 above that threshold, disappearing entirely at £125,140.How much is National Insurance in the UK for 2026/27?

Employee NI in 2026/27 is 8% on earnings between £12,570 and £50,270 per year, and 2% on earnings above £50,270. These rates are unchanged from 2025/26. NI is separate from income tax — the combined marginal rate for a basic-rate taxpayer is 28% (20% tax + 8% NI), not 20% as many assume.What are the 2026 federal income tax brackets in the US?

For 2026, the seven federal income tax rates are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. For single filers, the 10% rate applies to taxable income up to $12,400, 12% applies to $12,401–$50,400, and 22% applies to $50,401–$100,750. The standard deduction for a single filer is $16,100, reducing gross income before brackets are applied.What is FICA and how much do US employees pay?

FICA stands for the Federal Insurance Contributions Act and covers Social Security and Medicare taxes. Employees pay 6.2% in Social Security tax on earnings up to the 2026 wage base of $184,500, and 1.45% in Medicare tax on all earnings (no cap). Combined, employees pay 7.65% in FICA taxes, with their employer matching the same amount.Is the UK tax burden higher than the US?

It depends on the income level, US state, and what you include in the comparison. On federal-only deductions, the headline effective rates at similar income levels are broadly comparable, with the US slightly lower at most salary points. However, when US state income taxes (averaging around 5%) are included, US workers in most states pay a similar or slightly higher total effective rate. The crucial difference is that UK income taxes and NI fund NHS healthcare, which US workers must fund separately — often at significant personal cost.What is fiscal drag and how does it affect UK taxpayers in 2026/27?

Fiscal drag occurs when income tax thresholds are frozen while wages and prices rise, which means that each year a higher proportion of workers are pulled into higher tax bands without any change in the official tax rates. The UK personal allowance has been frozen at £12,570 since April 2022. With wage growth averaging 4-6% per year, millions of workers have seen their real-terms tax burden increase significantly without any rate changes. The Office for Budget Responsibility estimated that freezing thresholds until 2031 would generate approximately £25 billion a year in additional tax revenue by 2027/28 compared with indexing to earnings.References

House of Commons Library — Direct Taxes: Rates and Allowances for 2026/27 (CBP-10618) https://commonslibrary.parliament.uk/research-briefings/cbp-10618/GOV.UK (HMRC) — Rates and Thresholds for Employers 2026 to 2027 https://www.gov.uk/guidance/rates-and-thresholds-for-employers-2026-to-2027

The Private Office — UK Tax Allowances and Brackets for 2026/27 https://www.theprivateoffice.com/tax-planning/uk-tax-allowances-and-brackets

Nichols & Co — UK Tax Rates 2026/27: Key Changes Affecting Your Income https://nichols.co.uk/news/uk-tax-rates-2026-27/

Tax Foundation — 2026 Tax Brackets and Federal Income Tax Rates https://taxfoundation.org/data/all/federal/2026-tax-brackets/

IRS — Topic 751: Social Security and Medicare Withholding Rates (2026) https://www.irs.gov/taxtopics/tc751

U.S. Bank — Tax Laws and Tax Brackets 2026 https://www.usbank.com/wealth-management/financial-perspectives/financial-planning/tax-brackets.html

AARP — The Federal Income Tax Brackets for 2026 https://www.aarp.org/money/taxes/income-tax-brackets-2026/

Deloitte UK — Tax Rates 2026/27 Autumn Budget 2025 https://taxscape.deloitte.com/taxtables/deloitte-uk-tax-rates-2026-27.pdf

HMRC — Income Tax Rates and Personal Allowances https://www.gov.uk/income-tax-rates

0 Comments Comments