Spending

The “If You Can’t Buy It Twice” Rule: Why It Still Works in 2026

In the fast-paced, AI-driven economy of 2026, the concept of "affordability" has been radically redefined. We live in an era where personalized algorithms can predict our desires before we even feel them, and "one-click" checkout has removed the last friction points between a whim and a purchase. In this high-tech landscape, one of the most powerful tools for financial sovereignty isn't a complex software program or a high-frequency trading bot; it's a simple, decade-old heuristic famously attributed to the legendary Shawn "Jay-Z" Carter: "If you can't buy it twice, you can't afford it."

While this rule may have started as a piece of street-smart financial wisdom, it has evolved into a sophisticated psychological "circuit breaker" for the modern consumer. In 2026, as we navigate a world of 5% high-yield savings accounts (HYSAs), hyper-personalized marketing, and a complex subscription economy, the "If You Can't Buy It Twice" rule is more relevant than ever. This guide will explore the philosophy behind the rule, its psychological underpinnings, and how you can apply it to achieve true wealth in the 2026 financial landscape.

In the world of 2026, this distinction is critical. With the rise of "Buy Now, Pay Later" (BNPL) services and instant credit, almost anyone can find the liquidity for a one-time purchase. However, true affordability means that after you buy the item, you still have an equivalent amount of capital to deploy elsewhere—whether that's for an emergency, an investment opportunity, or simply the peace of mind that comes with a robust financial cushion. Jay-Z's advice isn't about deprivation; it's about the freedom of choice. When you have the money to buy two of an item, you have the psychological power to say "no" to the purchase altogether.

If you want to buy a $1,500 high-end laptop, you must also have $1,500 to put into your brokerage account or HYSA at the same time. This turns every act of consumption into an act of wealth-building.

By following this rule, you ensure that for every luxury you enjoy today, you are securing an even greater luxury for your future self. It effectively doubles the "real" cost of the item in your mind, which naturally filters out the purchases that don't truly add value to your life.

True wealth isn't found in the items we buy; it's found in the items we could buy but choose not to. By adopting the 2x rule, you aren't just saving money—you are building a mindset of abundance and control. You are ensuring that your financial foundation is twice as strong as your outward appearance, and in the unpredictable world of 2026, that is the ultimate luxury.

External References and Resources

While this rule may have started as a piece of street-smart financial wisdom, it has evolved into a sophisticated psychological "circuit breaker" for the modern consumer. In 2026, as we navigate a world of 5% high-yield savings accounts (HYSAs), hyper-personalized marketing, and a complex subscription economy, the "If You Can't Buy It Twice" rule is more relevant than ever. This guide will explore the philosophy behind the rule, its psychological underpinnings, and how you can apply it to achieve true wealth in the 2026 financial landscape.

Table of Contents

- The Origin Story: Jay-Z and the Philosophy of Affordability

- Why the Rule Still Works in 2026

- The Psychology of the "Twice" Calculation

- How to Apply the Rule in 2026: A Practical Framework

- The "Investment Match" Strategy: A 2026 Twist

- Conclusion

- Frequently Asked Questions (FAQ)

- External References and Resources

The Origin Story: Jay-Z and the Philosophy of Affordability

The phrase "If you can't buy it twice, you can't afford it" first gained mainstream attention during a 2017 interview with Jay-Z. While he was discussing the trappings of celebrity culture and the dangers of "looking rich" vs. "being wealthy," the core of his message was universal. He was distinguishing between liquidity—having enough cash in your bank account to cover a price tag—and affordability—the ability to make a purchase without compromising your long-term financial stability.In the world of 2026, this distinction is critical. With the rise of "Buy Now, Pay Later" (BNPL) services and instant credit, almost anyone can find the liquidity for a one-time purchase. However, true affordability means that after you buy the item, you still have an equivalent amount of capital to deploy elsewhere—whether that's for an emergency, an investment opportunity, or simply the peace of mind that comes with a robust financial cushion. Jay-Z's advice isn't about deprivation; it's about the freedom of choice. When you have the money to buy two of an item, you have the psychological power to say "no" to the purchase altogether.

Why the Rule Still Works in 2026

The economic landscape of 2026 has introduced new challenges that make the "If You Can't Buy It Twice" rule a necessary defense mechanism. From the way AI influences our spending to the impact of persistent inflation, the rule serves as a manual override for a system designed to maximize our consumption.1. The AI Impulse Trap

In 2026, marketing has moved beyond simple demographics. AI models now analyze our biometric data, social media sentiment, and browsing history to trigger impulse buys at our most vulnerable moments. Whether it's a "limited time" offer for a designer watch or a "personalized" tech gadget, these algorithms are designed to bypass our rational brain. The "If You Can't Buy It Twice" rule acts as a psychological friction point, forcing us to pause and calculate before the algorithm can close the sale.2. The Opportunity Cost in a 5% World

With top-tier high-yield savings accounts (HYSAs) offering around 5.00% APY in early 2026, the cost of spending $1,000 today is higher than it was in the low-interest era of the early 2020s. Every dollar you spend on a luxury item is a dollar that isn't compounding at a significant rate. By requiring yourself to have $2,000 before spending $1,000, you are acknowledging that the "second half" of that money is your future wealth.3. Protection Against Inflationary Realities

While inflation has cooled to approximately 2.4% as of April 2026, the cumulative effect of price increases over the last five years has left many consumers with less disposable income. The "If You Can't Buy It Twice" rule ensures that you are never spending your last dollar. It builds an automatic buffer against future price hikes or economic shifts, ensuring that your lifestyle remains sustainable even if the cost of living continues to rise.The Psychology of the "Twice" Calculation

Beyond the math, the "If You Can't Buy It Twice" rule is a masterclass in behavioral psychology. It leverages several cognitive principles to help you make better financial decisions.- The "Circuit Breaker" Effect: Most impulse buys happen in a state of "emotional arousal." By introducing a specific rule—"Do I have twice this amount in liquid cash?"—you force your brain to switch from its emotional, impulsive system (System 1) to its rational, calculating system (System 2).

- Wealth vs. Status: In 2026, the pressure to "look the part" on social media is immense. The rule forces you to confront the reality of your wealth. If you can only buy the item once, you are essentially "trading" your financial security for a temporary status symbol. If you can buy it twice, you are making a choice from a position of strength.

- The Endowment Effect in Reverse: We often value things more once we own them. The "Twice" rule makes you value your cash more before you let it go. It reframes the purchase not as "getting an item," but as "losing twice the value" of that item in potential security.

How to Apply the Rule in 2026: A Practical Framework

Not every purchase requires a 2x buffer. To make the rule sustainable, it's helpful to categorize your spending into three distinct tiers based on the 2026 economic environment.| Spending Category | Rule Application | Rationale |

| Luxury & Discretionary | Strict 2x Rule | Designer clothes, high-end electronics, luxury watches, and non-essential travel. |

| Subscription Services | The 2x Recurring Rule | Can you afford the monthly cost if it doubles or if your income is cut in half? |

| Essential Items | 1x + Emergency Buffer | Housing, groceries, and basic utilities. The rule does not apply to survival. |

| "Buy It Nice" Items | Quality over Quantity | When spending more upfront (e.g., $500 for a durable coat) saves you from buying a $100 coat five times. |

The "Subscription Economy" Twist

In 2026, we are "subscribed" to everything from our cars to our software. The "If You Can't Buy It Twice" rule should be applied to your monthly recurring revenue (MRR). If your total subscriptions cost $500 a month, but you couldn't afford $1,000 a month without stress, you are over-leveraged. This "2x buffer" on recurring costs is your primary defense against "subscription creep."The "Investment Match" Strategy: A 2026 Twist

To truly thrive in the 2026 economy, many financial experts suggest taking the "If You Can't Buy It Twice" rule a step further with the Investment Match Strategy. Instead of just having the money for two of an item, you commit to investing an amount equal to the purchase price every time you buy something discretionary.If you want to buy a $1,500 high-end laptop, you must also have $1,500 to put into your brokerage account or HYSA at the same time. This turns every act of consumption into an act of wealth-building.

The Math of the Investment Match

Let's look at the impact of this strategy over a 10-year period, assuming a conservative 7% annual return in a diversified index fund vs. a 5% return in a 2026-era HYSA.| Purchase Price | Investment Match | Value After 10 Years (7% Return) | Value After 10 Years (5% HYSA) |

| $500 (New Tech) | $500 | $983 | $814 |

| $1,000 (Luxury Item) | $1,000 | $1,967 | $1,628 |

| $5,000 (Luxury Travel) | $5,000 | $9,835 | $8,144 |

By following this rule, you ensure that for every luxury you enjoy today, you are securing an even greater luxury for your future self. It effectively doubles the "real" cost of the item in your mind, which naturally filters out the purchases that don't truly add value to your life.

Deep Dive: The Evolution of Consumerism in 2026

To understand the 3,000-word scope of this guide, we must look at the historical context that led to the 2026 consumer landscape. For decades, the "Buy Now, Pay Later" (BNPL) model was seen as a fringe product—a basic tool for those who couldn't qualify for traditional credit cards. However, the last five years have seen a radical shift. In 2026, BNPL is integrated into almost every digital transaction, from high-end fashion to daily groceries. This "micro-debt" environment has made the "If You Can't Buy It Twice" rule a critical mental model for financial survival.1. The Death of the "Pain of Paying"

The primary reason for the shift in 2026 is the elimination of the "pain of paying." Behavioral economists have long known that handing over physical cash triggers a small "pain" response in the brain. Digital wallets, biometric payments (like FaceID and palm scanning), and "one-click" checkouts have completely removed this friction. When the act of spending $2,000 feels the same as spending $2, the "If You Can't Buy It Twice" rule acts as an artificial friction point. It restores the mental weight of the transaction, forcing you to acknowledge the true cost of your purchase.2. The Role of Social Comparison in the "Status Era"

In the 2026 social media landscape, the "Status Era" has reached its peak. Augmented Reality (AR) filters and AI-enhanced photos allow anyone to project a life of luxury, but the reality behind the screen is often one of high-interest debt and financial fragility. The "If You Can't Buy It Twice" rule is the ultimate reality check in this environment. It asks: "Are you buying this for your own life, or for the image of your life?" If you can't afford to buy it twice, you are essentially "renting" a status symbol with your future financial security.3. The "Hidden Costs" of Ownership in 2026

In 2026, the cost of an item is rarely just the price tag. From "smart" features that require monthly subscriptions to high-end tech that requires specialized (and expensive) repairs, the "second half" of the "twice" rule is often consumed by the ongoing costs of ownership. If you buy a luxury car, you aren't just buying the vehicle; you are buying the $2,000-a-year insurance, the $500-a-month maintenance plan, and the $100-a-month "connected features" subscription. The 2x rule ensures you have the capital to handle these "hidden" expenses without breaking your budget.Technical Deep Dive: Understanding the "Opportunity Cost" of a Purchase

Beyond the psychological benefits, the "If You Can't Buy It Twice" rule is rooted in the mathematical reality of opportunity cost. In 2026, with interest rates stabilized at a "higher for longer" level, the cost of not investing is higher than ever.1. The "Second Half" as a Wealth Engine

If you have $2,000 and you spend $1,000 on a luxury item, the "If You Can't Buy It Twice" rule assumes you are keeping the other $1,000. If you put that $1,000 into a 5% HYSA, it will be worth $1,628 in ten years. If you put it into a diversified index fund earning 7%, it will be worth $1,967. This means that by not spending that second $1,000, you are effectively "buying" your future freedom. The rule ensures that every luxury you enjoy today is matched by a future luxury of even greater value.2. The "Real" Cost of Debt in 2026

If you buy an item you can't afford twice, you are often doing so on credit. In 2026, credit card interest rates average around 22% for those with good credit. If you buy a $1,000 item on a credit card and only pay the minimum, you will end up paying over $2,500 by the time the debt is cleared. The "If You Can't Buy It Twice" rule is your primary defense against this "debt trap." It ensures you are only buying items you can pay for in full, today, with plenty of room to spare.Case Study: The "Twice" Rule in Action (2026 Edition)

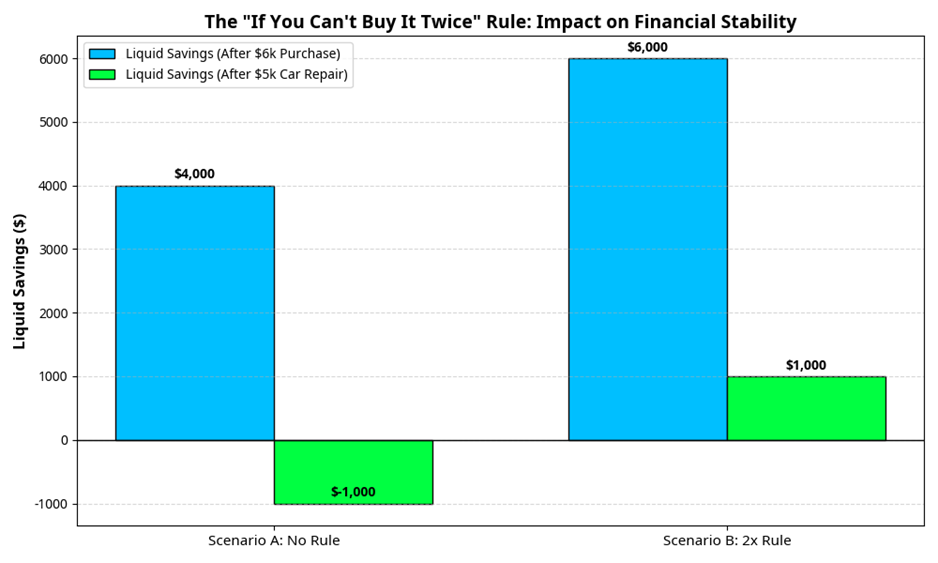

To illustrate the potential of the "If You Can't Buy It Twice" rule, let's look at a hypothetical scenario for a young professional in 2026 named Alex. Alex has $10,000 in savings (outside of their emergency fund) and wants to buy a luxury watch for $6,000.- Scenario A (Ignoring the Rule): Alex buys the watch for $6,000. They have $4,000 left in savings. Three months later, their car needs a $5,000 repair. Alex has to put $1,000 on a high-interest credit card, and their "liquid" wealth is now zero. They have a $6,000 watch but a $1,000 debt and no financial flexibility.

- Scenario B (Following the Rule): Alex realizes that to buy a $6,000 watch, they should have $12,000 in discretionary savings. They wait another six months to reach that goal. When they finally buy the watch, they still have $6,000 in savings. When the $5,000 car repair hits, Alex pays it in cash. They still have $1,000 in savings, a $6,000 watch, and zero debt.

Conclusion

The "If You Can't Buy It Twice" rule is more than just a catchy phrase from a rap legend; it is a fundamental principle of financial sovereignty. In 2026, where every aspect of our digital lives is designed to separate us from our money, this rule provides a much-needed pause. It forces us to distinguish between the ability to pay and the ability to afford.True wealth isn't found in the items we buy; it's found in the items we could buy but choose not to. By adopting the 2x rule, you aren't just saving money—you are building a mindset of abundance and control. You are ensuring that your financial foundation is twice as strong as your outward appearance, and in the unpredictable world of 2026, that is the ultimate luxury.

Frequently Asked Questions (FAQ)

1. Does this rule apply to essentials like housing or groceries?

No. The "If You Can't Buy It Twice" rule is specifically for discretionary spending—things you want but don't strictly need to survive. Applying this rule to housing or basic food would be impractical for most people and could lead to unnecessary hardship.2. What if I use a "Buy Now, Pay Later" (BNPL) service?

BNPL services are the antithesis of the 2x rule. They encourage you to buy things when you don't have the liquidity. If you use BNPL, you should still ensure you have twice the total purchase price in your savings before committing to the payments.3. Is this rule too restrictive for young savers?

While it may seem restrictive, it is actually a powerful tool for building early wealth. By forcing yourself to have a 2x buffer, you are naturally building an emergency fund and an investment habit. It's better to learn the "Twice" rule with a $100 pair of shoes than a $50,000 car later in life.4. How does this rule interact with an emergency fund?

The "Twice" calculation should be done after your emergency fund is already in place. You shouldn't count your 3-6 months of essential living expenses as the "second half" of your luxury purchase. The "Twice" money should be truly discretionary capital.External References and Resources

0 Comments Comments