Investing

Why Portfolio Diversification Pays Off: More Isn't Better

Table of Contents

- The Only Free Lunch in Investing

- The 2026 Proof: Diversification Is Winning Right Now

- The Science: Systematic vs. Unsystematic Risk

- How Many Holdings Do You Actually Need?

- The Five Dimensions of True Diversification

- The Diversification Trap: Over-Diversification and Diworsification

- What 2026’s Diversification Winners Tell Us

- Building a Genuinely Diversified Portfolio

- Conclusion: Enough Is Optimal

- Frequently Asked Questions

- External References

The Only Free Lunch in Investing

Harry Markowitz, who won the Nobel Prize in Economics for developing modern portfolio theory, described diversification as 'the only free lunch in investing.' The phrase has survived for seven decades because it describes something real: by combining assets that do not move perfectly in sync with each other, you can reduce the overall risk of a portfolio without necessarily reducing its expected return. You get risk reduction at no cost to expected performance. That is the free lunch.But the principle comes with a caveat that gets less attention than the headline: more diversification is not always better diversification. The free lunch has a portion size. Beyond a certain point, adding more holdings to a portfolio does not reduce risk meaningfully — it only dilutes the portfolio’s best ideas, increases complexity and cost, and can actually reduce returns without providing compensating risk reduction. Investment legend Peter Lynch called this phenomenon ‘diworsification’: the point at which diversification ceases to serve the investor and begins to work against them.

In 2026, understanding this distinction has never been more practically important. Morningstar’s research team published data in early 2026 showing that diversification strategies — particularly those with genuine asset class and geographic breadth — are demonstrably outperforming concentrated US equity portfolios year-to-date. This article explains why, how diversification works mechanically, what the research says about how much is enough, and the key mistakes investors make when they diversify too little or too much.

Disclaimer: This article is for general informational and educational purposes only. It is not financial or investment advice. Investing involves risk, including the possible loss of capital. Past performance is not a guarantee of future results. Always consult a qualified financial adviser before making investment decisions.

The 2026 Proof: Diversification Is Winning Right Now

By March 2026, Morningstar’s portfolio strategist Amy Arnott had assembled data from the 2025–2026 Diversification Landscape Report that illustrated the principle with striking clarity. By the end of 2025, the US stock market was more heavily concentrated in its 10 largest names than at any point since 1932. Mega-cap technology stocks driving the AI trade had propelled the S&P 500 to record highs through three consecutive years of 16 to 24 percent annual gains.Then 2026 arrived. Tariff uncertainty, the Iran war’s energy shock, and growing concerns about AI spending and competitive disruption triggered the ‘anything but AI’ trade — a rotation away from the mega-cap stocks that had dominated the previous three years. By early April 2026, the S&P 500 was down approximately 3.5 percent year-to-date, while most mega-cap technology names were in negative territory.

Investors who held genuinely diversified portfolios experienced something very different. Morningstar’s March 2026 analysis found that international stocks — which had underperformed US equities for several years — were outperforming US stocks in both 2025 and 2026. Higher-quality US bonds had outperformed US stocks in the first two months of 2026. Sectors outside technology and AI had benefited from the rotation. As Morningstar concluded: '2026 is already proving why diversification matters.'

Morningstar, March 2026: After underperforming US stocks for several years, international stocks outperformed US stocks in 2025 and have continued to do so in 2026. Non-US stock markets are less tied to technology and the AI trade and thereby are benefiting this year from the 'anything but AI' sentiment. Higher-quality US bonds have edged out US stocks for the first two months of 2026.

The Science: Systematic vs. Unsystematic Risk

To understand why diversification works, it helps to understand what it does and does not eliminate. Portfolio theory divides investment risk into two categories:Unsystematic Risk (Diversifiable Risk)

Unsystematic risk is the risk specific to an individual company or sector: the risk that a company’s earnings disappoint, that its CEO resigns unexpectedly, that a product recall damages its reputation, or that a regulatory change disrupts its business model. This risk is ‘idiosyncratic’ — it is unique to that specific holding and does not affect other unrelated companies. Adding more holdings to a portfolio reduces this type of risk, because when one company’s stock falls for company-specific reasons, other holdings in different sectors and industries are not affected in the same way.Systematic Risk (Market Risk, Non-Diversifiable Risk)

Systematic risk is the risk inherent in the entire market or a broad segment of it — the risk of an economic recession, a central bank policy shift, a geopolitical shock, or a broad market correction. This type of risk affects all stocks simultaneously and cannot be reduced by adding more stocks to the portfolio. No matter how many equities you hold, they are all exposed to the broad market falling during a crisis.The practical implication is fundamental: diversification works by eliminating unsystematic risk, not systematic risk. A well-diversified equity portfolio will still fall in a broad market downturn. What it will not suffer is the additional, avoidable loss from holding too concentrated a position in a single stock, sector, or geography that experiences a specific negative event while the rest of the market is stable.

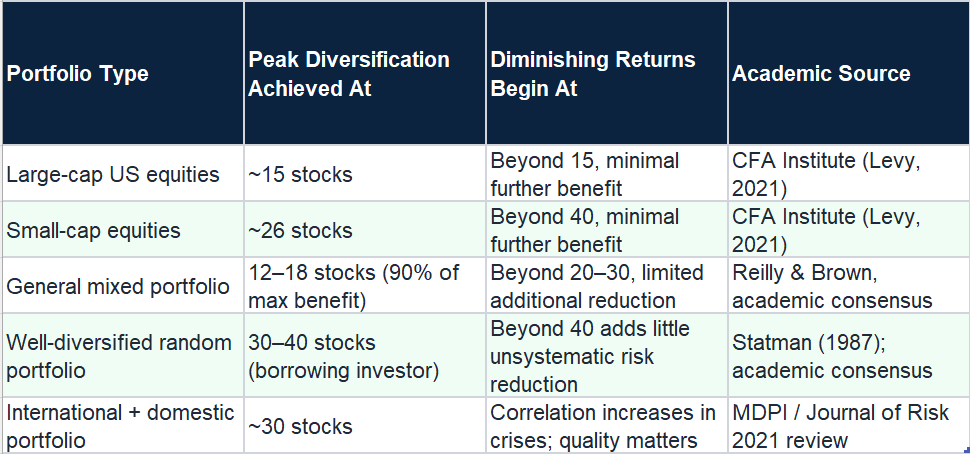

How Many Holdings Do You Actually Need?

The research on the optimal number of stocks for diversification is more nuanced than the popular ‘rule of thumb’ figures suggest. The literature review published in the Journal of Risk and Financial Management found that 'a generalized optimal number of stocks that constitute a well-diversified portfolio does not exist for whichever market, period or investor.'However, the research does converge on some useful practical guidance:

The CFA Institute’s analysis adds the most practical nuance: for large-cap portfolios, there is little to be gained by diversifying beyond 15 stocks or so. For small-cap portfolios, peak diversification is achieved with around 26 stocks. The same result appears regardless of academic era or methodology: beyond 30 to 40 holdings, additional stocks add very little in terms of risk reduction while adding monitoring complexity, transaction costs, and the dilution of your best ideas.

Reilly and Brown, cited by Behind The Balance Sheet (2025): About 90% of the maximum benefit of diversification was derived from portfolios of 12 to 18 stocks. Beyond this, the incremental risk reduction from adding further holdings becomes vanishingly small — while the dilution of your best ideas becomes increasingly real.

The Five Dimensions of True Diversification

Effective diversification operates across five distinct dimensions. Holding 50 stocks in the same sector, country, and asset class is not genuinely diversified. True diversification requires breadth across all five:1. Asset Class Diversification

The most fundamental level: spreading investments across stocks, bonds, real estate, commodities, and cash equivalents. Each asset class responds differently to economic conditions. Bonds generally rise when equities fall during recessions (flight to safety). Gold and commodities provide inflation hedging. Real estate provides income and inflation protection. In 2026, bonds outperforming stocks in the first two months — as Morningstar documented — demonstrates this effect in practice.2. Geographic Diversification

International diversification reduces concentration risk in a single country’s economy and regulatory environment. Morningstar’s 2026 data shows this working in real time: non-US stocks outperforming US stocks because they are less exposed to the AI trade’s reversal and the tariff shock’s specific US economic impact. The 2026 Diversification Landscape Report notes this explicitly as a key performance driver for diversified portfolios.3. Sector and Industry Diversification

Within equities, spreading across economic sectors — technology, healthcare, financials, energy, consumer staples, industrials, utilities — ensures that a sector-specific shock affects only a portion of the portfolio. In 2026, investors concentrated in technology and AI experienced significantly worse outcomes than those spread across defensive sectors and non-AI industries.4. Factor and Style Diversification

Academic research identifies investment factors — value, growth, quality, momentum, low volatility, dividend yield — as distinct risk and return drivers that do not always move together. Morningstar’s 2025 factor analysis found that different factors lead in different years with no consistent pattern. A portfolio diversified across factors is more resilient than one concentrated in a single style.5. Time Diversification (Dollar-Cost Averaging)

Investing a fixed amount at regular intervals — regardless of market conditions — diversifies across time, reducing the risk of deploying all capital at a market peak. This temporal diversification is one of the most accessible and most consistently effective diversification tools available to ordinary investors.The Diversification Trap: Over-Diversification and Diworsification

Peter Lynch, the legendary Fidelity fund manager, coined the term ‘diworsification’ to describe the phenomenon he observed in companies that expanded into unrelated businesses to ‘diversify’ their revenue streams but ended up diluting their competitive advantages. The same concept applies to investment portfolios.Over-diversification in a portfolio occurs when the addition of new holdings adds no meaningful risk reduction but does add costs, complexity, and the dilution of your most carefully researched positions. A portfolio with 150 individual stocks has effectively become a self-constructed index fund — but one that charges the trading costs of 150 individual positions, requires monitoring 150 companies, and will almost certainly underperform a low-cost index fund that achieves the same broad diversification for a fraction of the cost.

The practical signs of over-diversification:

- Holdings that duplicate each other’s sector or geographic exposure without providing differentiation

- Positions too small to meaningfully affect portfolio performance in either direction

- No clear rationale for each holding beyond vague risk reduction

- High trading costs from maintaining a large number of positions

- Performance that closely tracks a broad index, eliminating any potential benefit from individual stock selection

What 2026’s Diversification Winners Tell Us

The specific assets that performed well in early 2026 provide a practical lesson in what genuine diversification looks like:- International stocks (both developed and emerging): outperforming US equities year-to-date through March 2026, driven by lower exposure to the AI trade and benefits from dollar weakening

- Higher-quality US bonds: outperforming US equities in the first two months; providing the classic flight-to-safety diversification benefit during equity market volatility

- Non-AI sectors within US equities: healthcare, utilities, consumer staples, and industrials all providing positive returns or smaller drawdowns than the technology-heavy S&P 500

- Value and dividend stocks: maintaining better performance relative to growth during the technology rotation

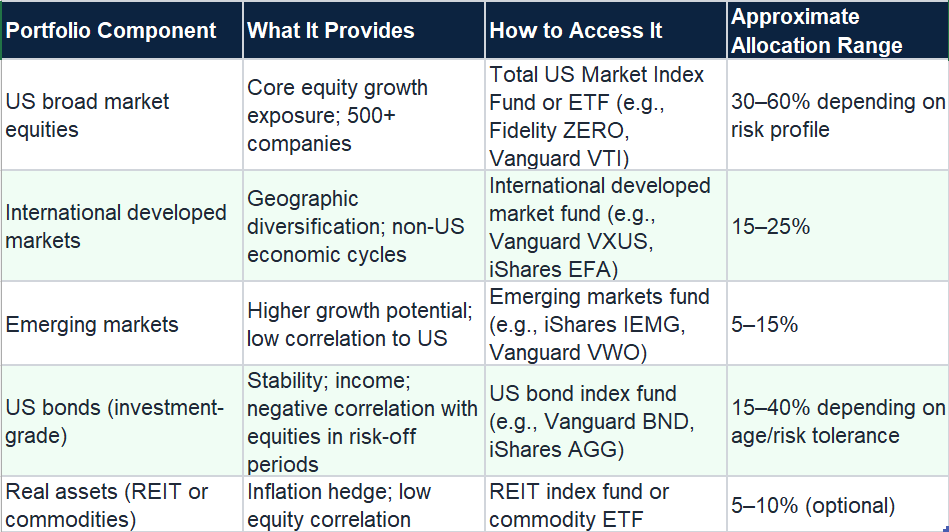

Building a Genuinely Diversified Portfolio

Practical diversification for most investors does not require exotic instruments or complex strategies. The following framework provides genuine, research-backed diversification at minimal cost:

This five-component framework with low-cost index funds achieves broad-asset, geographic, and sector diversification across thousands of individual holdings, at an average ongoing cost of 0.03 to 0.20 percent annually. It is the closest practical implementation of the theoretical maximum diversification benefit that most individual investors can access.

Conclusion

Portfolio diversification pays off — consistently, across decades, across asset classes, and across economic cycles. Morningstar’s 2026 data shows it working in real time: diversified portfolios outperforming concentrated US technology positions as the AI trade reverses and international equities, bonds, and defensive sectors provide positive returns. The principle is not new. The 2026 environment is simply its most recent demonstration.But the qualifier matters: more is not always better. The research is clear that 90 percent of the maximum diversification benefit is achieved within 12 to 18 thoughtfully selected stocks, or with a small number of genuinely broad index funds. Beyond that, additional holdings add cost and complexity without adding meaningful risk reduction. The investor who owns 150 individual US technology and growth stocks has not diversified. The investor who owns a US total market fund, an international developed markets fund, and a bond fund has achieved more genuine diversification with three instruments than the concentrated stock-picker achieves with 150.

The free lunch that Markowitz identified is real. Claiming it requires only that you diversify genuinely — across asset classes, geographies, and sectors — and resist both the under-diversification of concentration risk and the over-diversification of diworsification. Enough is optimal.

Frequently Asked Questions

Why is portfolio diversification important?

Diversification reduces the unsystematic (company-specific) risk in a portfolio without necessarily reducing its expected return. This is what Markowitz called the free lunch of investing. By holding assets that do not move perfectly in sync, you reduce the impact of any single negative event on your overall portfolio. Morningstar’s 2026 data demonstrates this concretely: investors with genuinely diversified portfolios significantly outperformed those concentrated in US technology stocks as the AI trade reversed.How many stocks do I need for a diversified portfolio?

Research from multiple academic and industry sources suggests 90% of the maximum diversification benefit is achieved with 12 to 18 stocks (Reilly and Brown). The CFA Institute’s 2021 analysis found peak diversification for large-cap portfolios at around 15 stocks, and for small-cap portfolios at around 26. For randomly selected stocks, full diversification requires 30 to 40 (Statman, 1987). Beyond this range, each additional holding adds very little risk reduction while adding cost and complexity.What is the difference between systematic and unsystematic risk?

Unsystematic risk is company-specific risk — a CEO departure, product recall, regulatory change, or earnings miss that affects one company without affecting others. This type of risk can be virtually eliminated through diversification. Systematic risk is market-wide risk — a recession, interest rate shift, or geopolitical shock that affects all or most assets simultaneously. This type of risk cannot be eliminated through diversification, no matter how many holdings a portfolio contains.What is diworsification?

Diworsification is a term coined by fund manager Peter Lynch for portfolios that have been diversified beyond the point of benefit. When a portfolio holds so many positions that additional holdings provide no meaningful risk reduction but do add monitoring costs, trading costs, and the dilution of the portfolio’s best ideas, it has become diworsified. For individual investors, diworsification typically occurs when holding dozens of funds that substantially overlap each other, or when individual stock positions are too small to affect overall portfolio performance.Is international diversification still effective in 2026?

Yes, and Morningstar’s 2026 data shows it working better than it has for years. International stocks outperformed US stocks in both 2025 and 2026 year-to-date through March, as non-US markets benefited from lower exposure to the AI trade reversal and the tariff shock’s specific impact on US corporate earnings. After years of underperformance, international stocks have provided exactly the diversification benefit their theoretical role predicts: positive returns when US equities are under pressure.What is the best way to diversify a portfolio for most investors?

For most investors, genuine diversification is most efficiently achieved through a small number of broad, low-cost index funds covering different asset classes and geographies: a US total market fund, an international developed markets fund, and a bond index fund. This three-fund approach achieves diversification across thousands of individual holdings at an annual cost of 0.03 to 0.20%, far below what a self-constructed diversified stock portfolio would cost to build and maintain.Can a portfolio be over-diversified?

Yes. Over-diversification occurs when additional holdings provide no meaningful risk reduction but do add cost and complexity. Practical signs include positions too small to affect performance, holdings that duplicate each other’s exposure, and portfolio performance that closely tracks a broad index without the cost efficiency of an actual index fund. For individual stock selectors, over-diversification dilutes the research advantage of selecting superior companies by spreading capital across mediocre ones.External References and Further Reading

Morningstar — These Diversification Strategies Are Winning in 2026 (March 4, 2026), Morningstar — Portfolio Diversification Is Winning in 2025, CFA Institute Enterprising Investor — Peak Diversification: How Many Stocks Best Diversify an Equity Portfolio? (May 2021), MDPI Journal of Risk and Financial Management — How Many Stocks Are Sufficient for Equity Portfolio Diversification? A Review of the Literature (2021), Fidelity — Portfolio Diversification: Investing Strategies for Volatile Markets, BlackRock iShares — Navigating Volatility: Learning from History, The Land Geek — Portfolio Diversification 2026: Complete Guide (December 2025), Behind The Balance Sheet — Does Your Portfolio Have Too Many Stocks? (June 2025), Statman (1987) — How Many Stocks Make a Diversified Portfolio? — ResearchGate

SEC Investor.gov — Diversification and Asset Allocation

0 Comments Comments