Investing

Why Stocks Hit Records Despite the Iran War in 2026

Table of Contents

- The Disconnect That Confuses Everyone

- What Actually Happened: The Timeline

- Reason 1: The Market Is Forward-Looking, Not Present-Looking

- Reason 2: The ‘TACO Trade’ — Trump Always Chickens Out

- Reason 3: The AI Boom Doesn’t Run on Oil

- Reason 4: Corporate Earnings Have Held Up

- Reason 5: History Says Buy the War, Not Sell It

- The Risks: What Could Still Break the Rally

- What This Means for Long-Term Investors

- Conclusion: The Market Is Not Ignoring the War — It’s Pricing Its End

- Frequently Asked Questions

- External References

The Disconnect That Confuses Everyone

On April 15, 2026, traders on the floor of the New York Stock Exchange celebrated something that seemed, on its surface, almost surreal. The S&P 500 had just closed above 7,000 for the first time in history. The Nasdaq was on a winning streak not seen since 1992. And the United States was fighting an active war in the Middle East that had, just weeks earlier, produced the largest oil supply disruption in the history of the global energy market.The reaction from ordinary investors was predictable and understandable: confusion. How does a stock index hit all-time highs while Brent crude is above $100 a barrel, the Strait of Hormuz remains partially blocked, the IMF has cut global growth forecasts, and inflation is running above 4 percent? The answer requires understanding several things simultaneously: how markets actually work, what is driving the AI technology sector, what investors have learned about Donald Trump over years of observation, and what history reliably says about equity markets during wartime.

This article provides that explanation, clearly and honestly, including the very real risks that could prove the optimists wrong.

Disclaimer: This article is for general informational and educational purposes only. It is not investment, financial, or trading advice. Past market behaviour is not a guarantee of future results. Investing involves risk, including possible loss of principal. Consult a qualified financial adviser before making investment decisions.

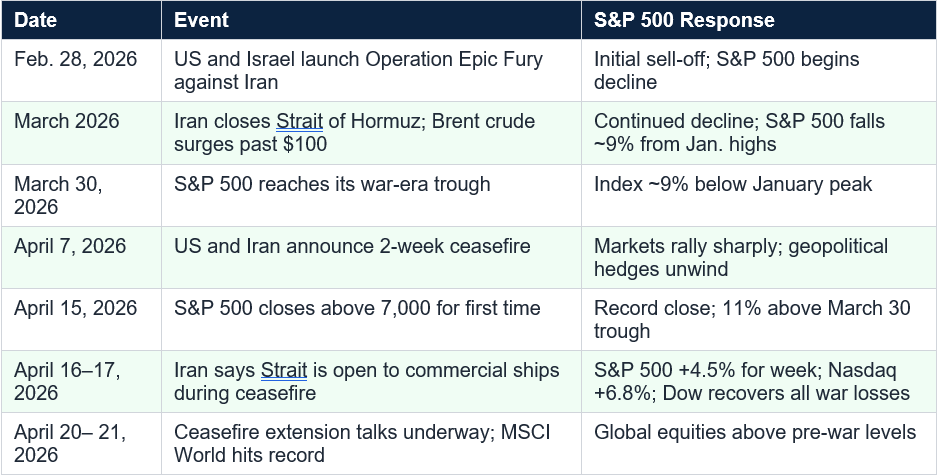

What Actually Happened: The Timeline

The speed of the recovery is itself remarkable. According to Bespoke Investment Group data cited by Yahoo Finance, the move from the S&P 500’s war-era correction to a new record high was the fastest such recovery since 1928 — a span of nearly a century. The index went from a correction trough to a new all-time high in just 11 trading days.

Reason 1: The Market Is Forward-Looking, Not Present-Looking

The most important thing to understand about a stock index is what it is not measuring. It is not a real-time assessment of current economic conditions. It is not a barometer of how ordinary Americans feel about their finances. It is a collective bet on what corporate earnings and economic conditions will look like six to twelve months from now.“The stock market isn’t trying to price what’s happening today,” Joe Seydl, a senior markets economist at J.P. Morgan Private Bank, told CNBC in April 2026. “The stock market is always trying to price what the world is going to look like six to 12 months from now.”

In April 2026, what investors believe the world will look like in six to twelve months is this: the ceasefire holds or extends, the Strait of Hormuz gradually reopens, oil prices fall back toward $70 to $80 per barrel, and the US economy — insulated from Middle East energy dependence by its own domestic shale production — continues growing at a pace driven by the AI technology build-out. Whether that scenario proves correct is unknown. But it is the scenario the market is pricing, and it is internally coherent.

Mark Zandi, Moody's chief economist: “The market has remained very resilient in the face of the war and has rallied strongly on the prospect that it will be resolved. Ultimately, the stock market is signaling a collective belief that tensions will ratchet down, the war will end in the near term, and oil flows through the Strait of Hormuz will normalize.” — CNBC, April 2026

Reason 2: The ‘TACO Trade’ — Trump Always Chickens Out

One of the most discussed explanations among financial professionals for the market’s resilience is what traders have taken to calling the “TACO trade” — shorthand for the thesis that Trump Always Chickens Out.The thesis is grounded in observable pattern. During Trump’s first term and into his second, investors repeatedly watched escalating confrontations — trade wars, tariff threats, geopolitical crises — followed by de-escalation before the economic pain became severe. The most clear recent example was the Liberation Day tariff episode of April 2025, when the Trump administration announced sweeping tariffs on US trading partners. The S&P 500 fell more than 12 percent within days. Within weeks, Trump announced a 90-day pause, and markets recorded one of the largest single-day rallies in history.

Investors were conditioned by that experience to interpret each new shock through the TACO framework: the conflict will eventually de-escalate before the economic damage becomes severe enough to threaten a full recession. Joe Seydl of J.P. Morgan noted that “investors remember that Trump often de-escalates geopolitical shocks — which is why they’ve seized on positive headlines that hint at progress in peace talks.”

The limitation of this thesis is also visible in the Iran situation. A CNBC report noted that the Iran conflict “has complicated that strategy, as Trump can’t just walk away, or TACO, if the Iranians decide to hold their line and keep the strait closed.” The war involves genuine national security interests, allied commitments, and a counterparty that may not be as easily managed as a trade dispute with Canada. The TACO trade has worked consistently in economic contexts. In active military conflicts, its track record is less established.

The TACO trade in plain terms: Investors are pricing in a conflict resolution not because the evidence definitively points to one, but because they have been rewarded consistently for betting on Trump de-escalating before the damage gets too deep. That is a bet on pattern, not fundamentals, and it carries real risk if the pattern breaks.

Reason 3: The AI Boom Doesn’t Run on Oil

Perhaps the single most structurally significant explanation for the market’s resilience is one that would have been unavailable in any previous geopolitical crisis of this magnitude: technology stocks, and specifically the artificial intelligence investment cycle, have become so large a part of the US equity market that they effectively insulate the index from oil-price shocks.Technology stocks now account for nearly half of the S&P 500’s market capitalisation. The AI build-out — demand for semiconductors, cloud computing infrastructure, data centre capacity, and the software applications running on top of that infrastructure — is driven by corporate and government investment decisions that are essentially independent of oil prices.

Mark Zandi of Moody’s stated it directly to CNBC: “Those stocks run on their own dynamic independent of anything, including the war in Iran. I think we would have been down a lot more and it would have been harder for us to recover had it not been for the very, very optimistic perspectives on AI.” Jim Cramer put it even more bluntly: “This AI revolution does not know anything about Iran. It doesn’t know about bombing. It doesn’t run on gasoline. And it stops for no one.”

BNP Paribas economists added a longer-term context, writing in a client note that US GDP could grow by more than 10 percent by 2034 on the back of the AI boom. “The AI boom will be a period of optimism, in our view, in which the decisions of consumers, businesses and investors are informed by expectations of strong and sustained productivity growth.” That long-term optimism provides a powerful counterweight to the near-term disruption of the Iran conflict.

Reason 4: Corporate Earnings Have Held Up

Stock prices ultimately reflect earnings expectations. If investors believe companies will generate less profit in the future, stock prices fall. And while the Iran war has raised costs — fuel surcharges are now standard, logistics chains have been disrupted, and inflation has ticked back up toward 4 percent — corporate earnings have held up better than the headlines might suggest.S&P 500 companies were forecast to report combined profits of over $605 billion in Q1 2026, up from earlier estimates, according to Euronews’s reporting. Bank executives highlighted a strong US consumer and a healthy pipeline for deals and initial public offerings. Cleveland-Cliffs CEO Lourenco Goncalves told investors that the company’s “order book is full and the automotive original equipment manufacturers are booking more and more steel from Cliffs,” pointing to steady demand conditions despite broader uncertainty.

The US labour market has also shown remarkable resilience. Consumer spending, which accounts for approximately 70 percent of US GDP, has not collapsed under the weight of higher gas prices and general inflation. Americans are paying more, spending more cautiously, and expressing less confidence about the future — but they are still spending. That spending sustains corporate revenues, which sustains earnings, which sustains stock prices.

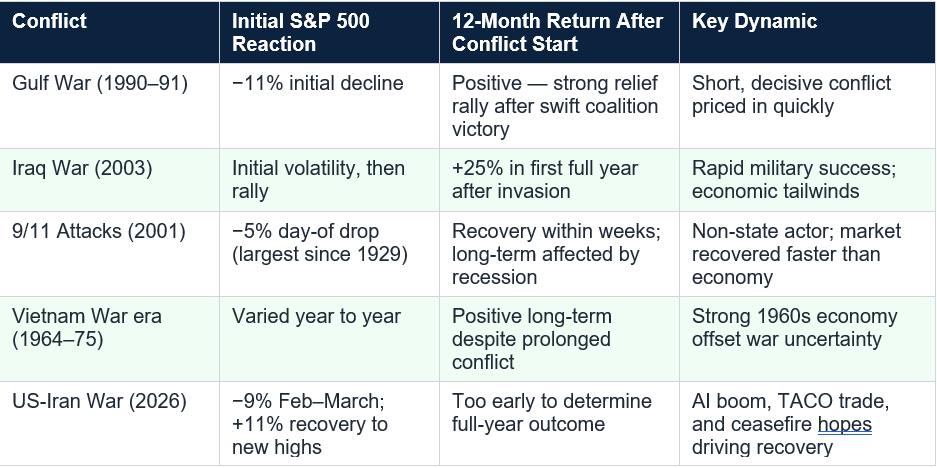

Reason 5: History Says Buy the War, Not Sell It

There is a consistent and well-documented pattern in the historical relationship between US military conflicts and equity markets, and it is more reassuring than most investors expect.

Data compiled by the Royal Bank of Canada and other institutions indicates that, across multiple conflicts, equities rose in the first year of hostilities approximately 60 percent of the time. Markets have historically tended to focus on eventual outcomes rather than immediate shocks. As Euronews summarised: “The latest record for the S&P 500 and the Nasdaq underscore this enduring pattern. While risks remain if the Iran conflict worsens, investors are currently betting that diplomacy and corporate fundamentals will prevail.”

The Risks: What Could Still Break the Rally

Explaining why markets are at record highs is not the same as endorsing the level of optimism markets are displaying. Multiple analysts have cautioned that the current rally contains assumptions that may prove incorrect.- The ceasefire breaks down and the Strait of Hormuz remains closed through summer 2026. The IMF’s forecast already includes risks of even weaker growth and higher prices in a prolonged conflict scenario. If Brent crude pushes toward $130 to $150 per barrel, consumer spending starts breaking visibly, and corporate earnings estimates are revised sharply downward, the market’s forward-looking optimism becomes backward-looking regret.

- The TACO thesis fails in a military context. Markets are pricing on the assumption that Trump will negotiate an exit before the economic damage becomes severe. But Iran is not a tariff dispute. The dynamics of military conflict are harder to reverse quickly, and an Iranian refusal to accept US nuclear terms has already broken one round of peace talks.

- AI enthusiasm overextends into a bubble. Vineta Salale, Portfolio Strategist at GMO, told Euronews: “We can see some evidence of euphoria, particularly in the application layer of the AI ecosystem. But that euphoria is more distinctly present in the private market funding of this space.” If AI capex spending decelerates or monetisation disappoints, the technology sector’s protective effect on the index reverses.

- Inflation becomes entrenched. Headline inflation at 4.4 percent for 2026, with energy prices remaining elevated, forces the Federal Reserve into an uncomfortable choice between cutting rates to support growth or holding them to control prices. Market expectations for rate cuts in December 2026 have been volatile — swinging between 20 and 50 percent probability within single sessions. A hawkish Fed pivot would reprice equity valuations.

What This Means for Long-Term Investors

For the investor sitting at home watching the S&P 500 hit records and wondering whether to act on that information, the relevant guidance is consistent across all the economists and strategists quoted in this article: stay the course.CNBC’s April 2026 coverage concluded with a specific note on this point: “The uncertainty provides yet another example of why the average investor with a long time horizon should stick to their investment plan and ignore the noise.” The evidence for trying to time markets based on geopolitical events is poor. Investors who sold at the March 30 trough missed an 11 percent rally in 11 days. Investors who bought during the correction — following the historical pattern described above — were rewarded, at least as of mid-April.

The more precise version of this guidance is that what the market is doing reflects the collective wisdom of millions of participants with access to more information, analysis, and trading sophistication than any individual. That collective judgment is not always right — markets make mistakes and overextend in both directions. But it is consistently more right than individual attempts to outsmart it based on headline news.

The appropriate response for a long-term investor to the current situation is to review your asset allocation, ensure it reflects your actual risk tolerance and time horizon, and resist the urge to make dramatic changes based on a war that the market is already analysing more carefully than any individual can.

Conclusion

The S&P 500 at 7,000 while an active war disrupts global oil supply is not evidence that markets are irrational or disconnected from reality. It is evidence that markets are doing exactly what markets do: looking past the present difficulty toward what they believe the future will look like.That future, as priced by markets in April 2026, involves a ceasefire that holds or extends, a Strait of Hormuz that gradually reopens, an AI technology cycle that continues regardless of Middle East politics, a US economy that proves more resilient than feared, and a president who, in the pattern investors have consistently observed, eventually finds an off-ramp before the pain becomes unacceptable.

Those assumptions may be correct. History and the specific dynamics of this conflict provide reasonable grounds for holding them. They may also be wrong. The ceasefire is tenuous, the nuclear negotiation has already broken down once, and the IMF has warned that a prolonged conflict carries the risk of genuine stagflation.

What the market is not doing is ignoring the war. It is pricing its end. Whether that pricing proves prescient or premature is the central uncertainty of the moment — and the answer will determine whether April 2026’s record highs are remembered as the rational beginning of a sustained advance or the complacent peak before a harder reckoning.

Frequently Asked Questions

Why is the stock market going up when there is a war happening?

Markets are forward-looking instruments that price expected future conditions, not current ones. Investors are betting that the US-Iran conflict will resolve relatively quickly, that the Strait of Hormuz will reopen, and that the US economy will continue growing driven by the AI technology boom. When those expectations dominate, stocks rise even as the present-day news is negative. JP Morgan’s Joe Seydl described it precisely: ‘The stock market is always trying to price what the world is going to look like six to 12 months from now.’What is the TACO trade?

TACO is shorthand for ‘Trump Always Chickens Out’ — a market thesis that President Trump will de-escalate economic or geopolitical crises before they cause severe economic damage. It is based on his observed pattern of escalation followed by reversal, most clearly illustrated by the Liberation Day tariff reversal in April 2025. Investors conditioned by that experience have been more willing to buy the Iran war dip, believing Trump will negotiate an exit before the economic pain becomes severe.What level did the S&P 500 reach in April 2026?

The S&P 500 closed above 7,000 for the first time on April 15, 2026. It had previously fallen about 9 percent from its January 2026 highs following the outbreak of the US-Iran war on February 28. The recovery from the March 30 trough to new record highs took just 11 trading days, which Bespoke Investment Group data indicated was the fastest such move from a correction to a record since 1928.How does the AI boom affect the stock market’s response to the Iran war?

Technology stocks, primarily driven by the AI investment cycle, now account for nearly half of the S&P 500’s total market capitalisation. Because AI infrastructure investment is funded by corporate capital expenditure decisions that are largely independent of oil prices, the AI sector provides a powerful counterweight to the energy-sector headwinds from the Strait of Hormuz disruption. Moody’s chief economist Mark Zandi said the market would have fallen much further ‘had it not been for the very, very optimistic perspectives on AI.’What has history shown about stock markets during wars?

Data compiled by the Royal Bank of Canada and others shows that equities rose in the first year of hostilities approximately 60 percent of the time across major US-involved conflicts. The 2003 Iraq War saw the S&P 500 rise over 25 percent in the first full year after the invasion. The Gulf War of 1990-91 saw an initial 11 percent decline followed by a strong relief rally. Markets tend to price the eventual resolution of conflicts rather than their ongoing disruption, which is why rallies often begin before peace is formally established.Is it safe to invest in the stock market when geopolitical tensions are this high?

This is a personal decision that depends on your individual time horizon, risk tolerance, and financial situation. From a historical perspective, investors who sell during geopolitical shocks have consistently fared worse than those who stay invested, because the recovery often happens quickly and is missed by sellers. CNBC’s reporting quoted economists advising that average investors with long time horizons should stick to their investment plans and not try to time geopolitical events. That said, past performance is not a guarantee of future results. Consult a qualified financial adviser for guidance specific to your situation.What are the main risks that could reverse the stock market rally?

The primary risks are: (1) the ceasefire breaks down and the Strait of Hormuz remains closed through summer, pushing oil prices toward $130 to $150 per barrel; (2) the Iran nuclear negotiations fail permanently, eliminating a diplomatic resolution path; (3) AI investment enthusiasm overextends into bubble dynamics; (4) inflation becomes entrenched above 4 percent, forcing the Fed to maintain restrictive rates or even raise them, repricing equity valuations; and (5) a significant deterioration in the US labour market or consumer spending.Why is the Nasdaq doing better than the Dow Jones during the Iran war?

The Nasdaq is heavily weighted toward technology and AI companies, which are less directly exposed to oil price spikes than the industrial and transportation companies that have more influence on the Dow Jones Industrial Average. Companies like Nvidia, Microsoft, Alphabet, and AMD are benefiting from AI infrastructure investment regardless of Middle East conditions. The Dow, which includes more old-economy industrial and transport names, has lagged the technology-heavy indexes during the rally.What did the IMF say about the economic impact of the Iran war?

The IMF cut its 2026 global growth forecast to 3.1 percent from 3.3 percent in its April 2026 World Economic Outlook, citing energy price spikes and supply disruptions from the Iran conflict. It raised its 2026 headline inflation forecast to 4.4 percent under a short-lived conflict scenario. The IMF warned that if tensions escalated and prolonged, both growth would be weaker and inflation higher than those already-revised projections.External References

CNBC — Why the Stock Market Is Hitting Records Despite Iran War (April 16, 2026), CNBC — Global Stocks Recouped Iran War Losses to Hit Fresh Records (April 21, 2026), CNBC — Investors Are Misreading News About the Iran War, Analysts Say (April 20, 2026), CNBC — Jim Cramer Gives Four Reasons Why the Market Keeps Shrugging Off the Iran War (April 20, 2026), Euronews — S&P 500 and Nasdaq Hit New All-Time Highs Despite Iran War Effects (April 16, 2026), Yahoo Finance — S&P 500 Closes Above 7,000 for First Time: Stock Market Today (April 2026), Yahoo Finance — Dow Rises, S&P 500 and Nasdaq Notch Fresh Records as War Resolution Hopes Grow, Intellectia AI — Strait of Hormuz Crisis 2026: Oil Prices Plunge & S&P 500 at Record Highs

0 Comments Comments