Finance

America's New Financial Middle: Not Thriving, Not Broke

There is a vast and growing population of Americans who do not appear in the statistics for poverty or financial crisis — and yet feel profoundly financially insecure. They pay their bills. They hold down jobs. They are not behind on rent. But 54% are living paycheck to paycheck, up from 42% in 2021. Forty-eight percent say they have difficulty covering their monthly expenses, up from 36% five years ago. Fifty-three percent worry about money every single day. This is not the face of crisis as it is typically depicted. It is something quieter, more persistent, and in many ways more insidious: the financial no-man's land between struggling and thriving, where millions of Americans reside permanently. Erneroy.com calls it America's new financial middle — and this guide explains exactly what it is, why it exists, and what people living in it can do to move out of it.

America has always had a concept of financial crisis — hunger, eviction, bankruptcy, defaulting on debt. And it has always had a concept of thriving — homeownership, retirement savings, comfortable discretionary spending, financial security. What is less well defined, and far less discussed, is the enormous territory between these two poles: the financial no-man's land where millions of Americans exist not in emergency but in constant, low-grade financial precarity.

OWNTIC's analysis of the American middle class in 2025 names this condition precisely: 'Being part of the American middle class today often feels like walking a financial tightrope — too comfortable to qualify for assistance, yet too stretched to feel secure.' This is not poverty. These households pay their bills. They hold jobs. They buy groceries and put petrol in the car. But they cannot absorb a single serious financial shock without going into debt, and they carry an undercurrent of financial anxiety that never quite resolves. The Ramsey Solutions State of Personal Finance Q1 2026 report — published June 2, 2026 — provides the clearest data portrait yet of how large this population has become and how much it has grown: 54% of Americans are now living paycheck to paycheck, up from 42% in 2021. Forty-eight percent have difficulty paying their monthly expenses. Fifty-three percent worry about money every single day.

The middle class in 2025 is caught in a kind of economic limbo. You're not 'poor,' but you're not truly secure either. You're expected to be doing fine — yet that sense of security is fragile.

— OWNTIC — THE AMERICAN MIDDLE CLASS IN 2025: STILL SHIFTING, STILL STRUGGLING

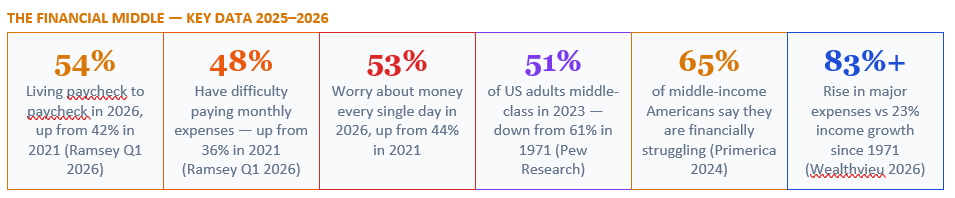

The Pew Research Center provides the longer historical context. In 1971, 61% of American adults lived in middle-class households — defined as earning between two-thirds and double the national median household income, adjusted for household size. By 2023, that figure had fallen to 51%. During the same period, the middle class's share of total US household income fell from 62% to 43%. Middle-income households' median income rose approximately 60% from 1970 to 2022 — but upper-income households experienced a 78% increase, and major expenses rose 83–312% over the same period according to Wealthvieu's May 2026 analysis. The arithmetic is unambiguous: income growth has been outpaced by cost growth, and the gap has been accumulating for decades.

Primerica's 2024 survey found that 65% of middle-income Americans say they are financially struggling, and nearly half (46%) would be unable to cover a $500 emergency expense without going into debt. The ACLI Financial Resilience Index (January 2026), which tracks middle-class households' ability to manage financial challenges and plan for the future, found that while the index remains in positive territory, middle-class households are facing worsening cost pressures for the first time in over two years.

Renters have none of these protections. As Elliot Schwartz told GOBankingRates: 'The housing market stresses the middle class. For those trying to buy a home, it is unaffordable. And rent prices have skyrocketed too, forcing middle-class people to spend too much of their income on rent and struggle to save for a down payment.' Michelle White, national mortgage expert at The CE Shop, puts the precarity of the non-homeowning middle in its starkest form: 'Many US households are one flat tire away from financial ruin. Any emergency spending — a flat tire, a car repair, an ER visit, a toothache, even a funeral expense — can put a household into a dire financial position.'

New Trader U's January 2026 analysis found that roughly half of Americans tapped into their savings to meet routine expenses in 2025 — meaning their emergency reserves are being consumed not by emergencies but by the ordinary cost of living. This produces a compounding fragility: each month that savings are drawn down for routine expenses leaves less available for the inevitable actual emergency. The cycle deepens: the emergency triggers high-interest debt, the interest payment reduces the monthly margin further, the reduced margin makes saving impossible, and the household re-enters the same precarity cycle at a marginally worse starting position than before.

The GOBankingRates 2026 shrinking middle class analysis quotes finance experts recommending seven specific money moves to stay in or return to financial stability. The most consistently cited: build a dedicated emergency fund of liquid cash rather than relying on credit cards (cash does not charge interest; maxing out a credit card lowers your credit score and increases future borrowing costs). Know your net worth. Create a monthly cash-flow snapshot. See everything in one place.

Fortune's April 2026 analysis captures the paradox directly in its headline: 'The American middle class didn't die. It got richer — and felt poorer.' The explanation is structural. Under Pew's relative methodology, the middle class can appear to shrink even when everyone's income rises — because middle-class membership is defined by closeness to a median that keeps moving up. Simultaneously, the wealth that has been generated in the last decade has been disproportionately concentrated in financial assets (stocks, equities) and upper-tier real estate — neither of which is held by the average person in the financial middle. The economy is growing. The gains are not reaching them.

The ACLI Financial Resilience Index (January 2026) provides a nuanced reading: middle-class financial resilience is 'edging closer to its historical average' as resource growth has remained positive, but 'middle-class households are facing worsening cost pressures for the first time in over two years.' This is the precise definition of the financial middle: not falling, not thriving, but watching the gap between your resources and your costs narrow in the wrong direction.

Naming the financial middle honestly — not crisis, but not thriving — is the first step toward changing it. The structural forces are real. But within them, financial clarity, an emergency fund, debt reduction, employer match capture, skill investment, and fixed-cost management are the actions that move households out of the no-man's land. Not overnight. Not without effort. But consistently, reliably, and at every income level, they work. Start with one clear number: your net worth, written down. Everything builds from knowing where you actually stand.

OWNTIC Blog — The American Middle Class in 2025: Still Shifting, Still Struggling https://blog.owntic.com/the-american-middle-class-in-2025-still-shifting-still-struggling/

Wealthvieu — The Shrinking Middle Class: Data and Trends (May 2026) https://wealthvieu.com/personal-finance/income/shrinking-middle-class/

Fortune — The American Middle Class Didn't Die. It Got Richer — and Felt Poorer (April 12, 2026) https://fortune.com/2026/04/12/did-middle-class-shrink-or-get-richer-feel-poorer/

New Trader U — 10 Reasons the Middle Class Can't Afford Its Old Lifestyle in 2026 (January 2026) https://www.newtraderu.com/2026/01/21/10-reasons-why-the-middle-class-cant-afford-their-old-lifestyle-anymore-in-2026/

Yahoo Finance / GOBankingRates — The Shrinking Middle Class in 2026: 7 Money Moves to Stay There (November 2025) https://finance.yahoo.com/news/shrinking-middle-class-2026-7-194422728.html

Ponderwall — How America's Middle Class Is Struggling to Survive (May 2025) https://ponderwall.com/index.php/2025/05/18/middle-class-america/

ACLI — Middle Class Financial Resilience Index — January 2026 Results (January 27, 2026) https://www.acli.com/posting/nr26-005

WebProNews — America's Economic Middle Is Hollowing Out — Upward (April 6, 2026) https://www.webpronews.com/americas-economic-middle-is-hollowing-out-upward/

TABLE OF CONTENTS

- Defining the New Financial Middle: The No-Man's Land Between Fine and Failing

- The Numbers Behind the Feeling

- The Five Structural Forces Keeping Americans in the Middle

- The Housing Wall: Homeowners vs Everyone Else

- The Paycheck-to-Paycheck Trap: How the Middle Becomes a Cycle

- The Optimism Paradox: Why the Economy Looks Strong While People Feel Poor

- Breaking Out: What the Financial Middle Can Actually Do

- Conclusion

- Frequently Asked Questions

- References

Defining the New Financial Middle: The No-Man's Land Between Fine and Failing

America has always had a concept of financial crisis — hunger, eviction, bankruptcy, defaulting on debt. And it has always had a concept of thriving — homeownership, retirement savings, comfortable discretionary spending, financial security. What is less well defined, and far less discussed, is the enormous territory between these two poles: the financial no-man's land where millions of Americans exist not in emergency but in constant, low-grade financial precarity.OWNTIC's analysis of the American middle class in 2025 names this condition precisely: 'Being part of the American middle class today often feels like walking a financial tightrope — too comfortable to qualify for assistance, yet too stretched to feel secure.' This is not poverty. These households pay their bills. They hold jobs. They buy groceries and put petrol in the car. But they cannot absorb a single serious financial shock without going into debt, and they carry an undercurrent of financial anxiety that never quite resolves. The Ramsey Solutions State of Personal Finance Q1 2026 report — published June 2, 2026 — provides the clearest data portrait yet of how large this population has become and how much it has grown: 54% of Americans are now living paycheck to paycheck, up from 42% in 2021. Forty-eight percent have difficulty paying their monthly expenses. Fifty-three percent worry about money every single day.

The middle class in 2025 is caught in a kind of economic limbo. You're not 'poor,' but you're not truly secure either. You're expected to be doing fine — yet that sense of security is fragile.

— OWNTIC — THE AMERICAN MIDDLE CLASS IN 2025: STILL SHIFTING, STILL STRUGGLING

The Numbers Behind the Feeling

The data from Ramsey Solutions' Q1 2026 State of Personal Finance report is striking in its scale. The share of Americans who have difficulty paying their monthly expenses has climbed from 36% in 2021 to 48% in 2026 — a 33% increase in just five years. The proportion describing their financial situation as 'struggling' or 'in crisis' has risen from 22% to 34% — a 55% increase in the same period. Approximately 88 million American adults now describe themselves as struggling or in crisis. The increase has been sharpest among single adults (30% in 2021 to 45% in 2026), women (26% to 42%), and Gen X (27% to 41%).The Pew Research Center provides the longer historical context. In 1971, 61% of American adults lived in middle-class households — defined as earning between two-thirds and double the national median household income, adjusted for household size. By 2023, that figure had fallen to 51%. During the same period, the middle class's share of total US household income fell from 62% to 43%. Middle-income households' median income rose approximately 60% from 1970 to 2022 — but upper-income households experienced a 78% increase, and major expenses rose 83–312% over the same period according to Wealthvieu's May 2026 analysis. The arithmetic is unambiguous: income growth has been outpaced by cost growth, and the gap has been accumulating for decades.

Primerica's 2024 survey found that 65% of middle-income Americans say they are financially struggling, and nearly half (46%) would be unable to cover a $500 emergency expense without going into debt. The ACLI Financial Resilience Index (January 2026), which tracks middle-class households' ability to manage financial challenges and plan for the future, found that while the index remains in positive territory, middle-class households are facing worsening cost pressures for the first time in over two years.

The Five Structural Forces Keeping Americans in the Middle

The financial no-man's land is not primarily the result of individual poor decisions. It is the product of five structural forces that have converged over decades to trap middle-income households in a position where they earn enough to appear financially stable but not enough to actually be financially secure.THE FIVE STRUCTURAL FORCES OF THE FINANCIAL MIDDLE

- Wage stagnation relative to costs: income rose 23% since 1971, but major expenses rose 83–312% over the same period (Wealthvieu 2026). Elliot Schwartz, CEO of Becca's: 'Wages aren't going up as fast as inflation. Corporations focus more on profit margins and earnings per share than on increasing wages relative to the cost of living.'

- The housing affordability collapse: the median US home price has risen over 40% since 2020 alone. At least 20% of middle-class earners in every major metro area studied cannot afford to live in their own communities (New Trader U, January 2026). Rents have simultaneously risen sharply, forcing middle-class renters into spending disproportionate shares of income on shelter.

- Debt accumulation at high cost: the 2024 FinHealth Spend Report found that increasing debt balances and higher borrowing costs led to a dramatic increase in total spending on fees and interest, directly impacting middle-class families' bottom lines. Nearly 30% of workers have taken on debt to finance daily expenses (New Trader U, January 2026).

- Healthcare costs as a financial time bomb: New Trader U's January 2026 analysis found that healthcare expenses have transformed from a manageable budget item into a catastrophic financial burden for middle-class families. One serious illness can eliminate years of savings in a household that appears financially stable on paper.

- Upward mobility blocked by asset inequality: middle-class households without equity in a home or meaningful financial investments have been structurally excluded from the wealth appreciation that has defined the economic gains of the last decade — the K-shaped economy's lower arm, even at moderate income levels.

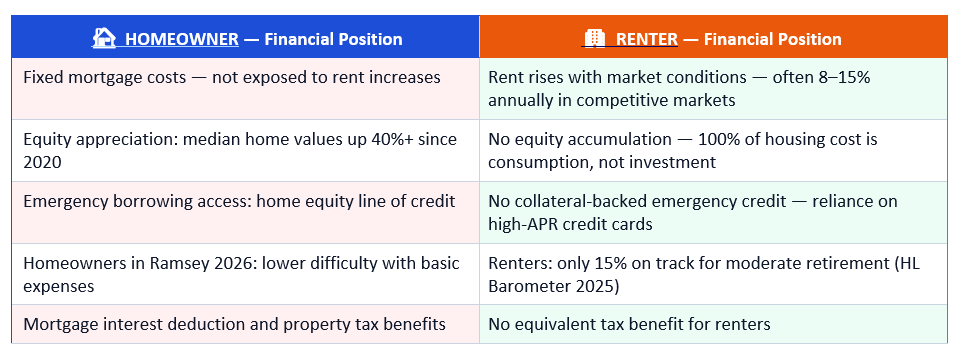

The Housing Wall: Homeowners vs Everyone Else

Perhaps no single factor divides America's financial middle more sharply than housing tenure. The Ramsey Q1 2026 data shows that homeowners have had significantly less difficulty providing the basics of life than renters across every comparable category. The reason is straightforward: homeowners benefit from equity appreciation, from payment certainty (a 30-year fixed mortgage does not rise with inflation), and from the wealth-building effect of building ownership of an appreciating asset over time.Renters have none of these protections. As Elliot Schwartz told GOBankingRates: 'The housing market stresses the middle class. For those trying to buy a home, it is unaffordable. And rent prices have skyrocketed too, forcing middle-class people to spend too much of their income on rent and struggle to save for a down payment.' Michelle White, national mortgage expert at The CE Shop, puts the precarity of the non-homeowning middle in its starkest form: 'Many US households are one flat tire away from financial ruin. Any emergency spending — a flat tire, a car repair, an ER visit, a toothache, even a funeral expense — can put a household into a dire financial position.'

The Paycheck-to-Paycheck Trap: How the Middle Becomes a Cycle

Living paycheck to paycheck at 54% of Americans is not primarily a story about low wages. It is a story about the absence of financial margin — the gap between what comes in and what goes out that would normally provide the buffer to absorb shocks, build savings, and make deliberate financial decisions. When there is no margin, every financial decision is reactive. Every unexpected expense becomes a crisis. Every month ends with the same zero balance.New Trader U's January 2026 analysis found that roughly half of Americans tapped into their savings to meet routine expenses in 2025 — meaning their emergency reserves are being consumed not by emergencies but by the ordinary cost of living. This produces a compounding fragility: each month that savings are drawn down for routine expenses leaves less available for the inevitable actual emergency. The cycle deepens: the emergency triggers high-interest debt, the interest payment reduces the monthly margin further, the reduced margin makes saving impossible, and the household re-enters the same precarity cycle at a marginally worse starting position than before.

The GOBankingRates 2026 shrinking middle class analysis quotes finance experts recommending seven specific money moves to stay in or return to financial stability. The most consistently cited: build a dedicated emergency fund of liquid cash rather than relying on credit cards (cash does not charge interest; maxing out a credit card lowers your credit score and increases future borrowing costs). Know your net worth. Create a monthly cash-flow snapshot. See everything in one place.

The Optimism Paradox: Why the Economy Looks Strong While People Feel Poor

One of the most disorienting features of life in America's financial middle in 2026 is the disconnect between aggregate economic indicators and lived experience. GDP has grown. Unemployment is low. Stock markets have reached record highs. And yet 53% of Americans worry about money every day. Forty-eight percent struggle to pay monthly expenses. The Allianz Life study (December 2025) found that 48% of Americans said they were more financially stressed at the end of 2025 than they were at the start — up from 43% in 2024.Fortune's April 2026 analysis captures the paradox directly in its headline: 'The American middle class didn't die. It got richer — and felt poorer.' The explanation is structural. Under Pew's relative methodology, the middle class can appear to shrink even when everyone's income rises — because middle-class membership is defined by closeness to a median that keeps moving up. Simultaneously, the wealth that has been generated in the last decade has been disproportionately concentrated in financial assets (stocks, equities) and upper-tier real estate — neither of which is held by the average person in the financial middle. The economy is growing. The gains are not reaching them.

The ACLI Financial Resilience Index (January 2026) provides a nuanced reading: middle-class financial resilience is 'edging closer to its historical average' as resource growth has remained positive, but 'middle-class households are facing worsening cost pressures for the first time in over two years.' This is the precise definition of the financial middle: not falling, not thriving, but watching the gap between your resources and your costs narrow in the wrong direction.

Breaking Out: What the Financial Middle Can Actually Do

The structural forces creating the financial middle are real and, in large part, not individually addressable. A single person cannot change housing policy, healthcare costs, or wage growth relative to corporate profit margins. But within those structural constraints, there are deliberate actions that move a household out of the no-man's land and toward genuine financial stability. These are not hacks or shortcuts — they are the evidence-backed fundamentals that Erneroy.com's 21 years of accountancy experience identifies as the actions that actually work.FROM THE FINANCIAL MIDDLE TO STABILITY — 7 EVIDENCE-BACKED ACTIONS

- Get a clear net-worth statement and monthly cash-flow snapshot today. Melissa Murphy Pavone, CFP: 'Many people feel stressed simply because they don't know where they stand. A clear net-worth statement and monthly cash-flow snapshot can be incredibly grounding. Most of us have assets spread across multiple places — seeing everything on one page often brings immediate relief.'

- Build the emergency fund before anything else: £1,000 / $1,000 in a separate, high-yield savings account is the first structural change that breaks the flat-tyre-to-debt cycle. Not a credit card. Cash.

- Attack the highest-APR debt with every available pound or dollar above the minimum payments on all other accounts. Each percentage point of high-interest debt eliminated is a guaranteed return on that capital.

- Capture the employer pension/401(k) match fully before doing anything else with discretionary income. Not capturing the full match is leaving guaranteed, immediate return on the table.

- Invest in income-generating skills: FiTHMedia's 2026 financial resilience analysis found that investing in skills that raise earning capacity by 10–30% over five years beats any financial instrument in risk-adjusted return for most middle-income households.

- Review and renegotiate fixed costs annually: insurance, subscriptions, phone plans, utilities. A single phone call can save $50–$200 per month — reclaimed margin that either builds the emergency fund or pays down debt.

- Consider homeownership seriously as a wealth-building strategy once the emergency fund is established and high-interest debt is cleared — the homeowner/renter divide in financial outcomes is one of the most consistently documented inequalities in American household finance.

CONCLUSION

America's new financial middle is not a temporary condition or a post-pandemic anomaly. It is a structural state that 54% of Americans now inhabit permanently — too financially intact to be recognised as struggling, too financially fragile to be genuinely secure. The Ramsey Q1 2026 data published this week is the clearest portrait yet of how this population has grown: 48% have difficulty covering monthly expenses, 53% worry about money daily, and 88 million Americans describe themselves as struggling or in crisis. The Pew Research data tells the 50-year story: middle-class membership fell from 61% to 51%, real income growth lagged behind cost growth by 60 percentage points or more, and the gains of the strongest decade for financial markets went overwhelmingly to those who already held financial assets.Naming the financial middle honestly — not crisis, but not thriving — is the first step toward changing it. The structural forces are real. But within them, financial clarity, an emergency fund, debt reduction, employer match capture, skill investment, and fixed-cost management are the actions that move households out of the no-man's land. Not overnight. Not without effort. But consistently, reliably, and at every income level, they work. Start with one clear number: your net worth, written down. Everything builds from knowing where you actually stand.

Frequently Asked Questions

What does 'America's new financial middle' mean?

It describes the condition of millions of Americans who exist between genuine financial crisis and genuine financial security — paying their bills and holding jobs, but living paycheck to paycheck, carrying financial anxiety, and one serious expense away from debt. The Ramsey Solutions Q1 2026 State of Personal Finance report, published June 2, 2026, found that 54% of Americans are living paycheck to paycheck (up from 42% in 2021), 48% have difficulty paying monthly expenses (up from 36%), and 53% worry about money every single day. This is not the population in poverty or in acute financial crisis — it is the larger, quieter population for whom financial security feels perpetually just out of reach. OWNTIC's 2025 analysis calls it 'economic limbo': too comfortable to qualify for assistance, yet too stretched to feel secure.Is the middle class really shrinking in America?

The data is clear on the headline trend but more complex in its meaning. The Pew Research Center defines middle class as households earning between two-thirds and double the median household income, adjusted for household size and local cost of living. Under this definition, the middle class fell from 61% of US adults in 1971 to 51% in 2023 — an 11-percentage-point decline over five decades. The middle class's share of total US household income fell from 62% to 43% over the same period. However, Fortune's April 2026 analysis and the WebProNews April 2026 review of the same data point out that much of this 'shrinkage' reflects upward mobility — people moving into higher income tiers — rather than purely downward pressure. The more concerning number is not the raw percentage but the experience within the remaining middle: Primerica's 2024 survey found 65% of middle-income Americans saying they are financially struggling despite technically holding middle-class income levels.Why do middle-income Americans feel poor even when the economy is growing?

This is what Fortune's April 2026 headline calls the paradox of the 'richer middle class that feels poorer.' Multiple structural explanations converge. First, cost inflation has outpaced wage growth: Wealthvieu's May 2026 data shows major expenses rose 83–312% since 1971, while median incomes rose only 23%. Second, the economic gains of the last decade — stock market appreciation, corporate profit growth, premium real estate appreciation — have been concentrated in asset-holding upper-income households, not distributed broadly through wages. Third, as Fortune notes, the very definition of 'adequate' has shifted: what constitutes a middle-class life (homeownership, children's education, reliable healthcare, retirement savings) now requires income levels that were considered upper-middle just decades ago. The ACLI Financial Resilience Index (January 2026) confirmed that middle-class households are facing worsening cost pressures for the first time in over two years, even as the overall index remains in positive territory.What is the single most important first step for someone trapped in the financial middle?

Financial clarity — specifically, a written net-worth statement and a monthly cash-flow snapshot. Melissa Murphy Pavone, CFP and founder of Mindful Financial Partners, states it directly in her work with middle-class clients: 'Many people feel stressed simply because they don't know where they stand. A clear net-worth statement and a monthly cash-flow snapshot can be incredibly grounding. Most of us have assets spread across multiple places — bank accounts, retirement plans, brokerage accounts — and seeing everything on one page often brings immediate relief.' Without financial clarity, every other action (budgeting, debt paydown, saving) is operating blind. Once you know your exact net worth, your exact income, and your exact monthly outflows by category, you have the information needed to make every other decision effectively.Does living paycheck to paycheck always mean financial crisis?

Not in the conventional sense — but it reliably produces a structurally vulnerable financial position that can become a crisis quickly. The Ramsey Q1 2026 data shows 54% of Americans living paycheck to paycheck in 2026, up from 42% in 2021. The critical issue is not the paycheck-to-paycheck status itself but what it prevents: emergency fund accumulation, retirement saving, debt paydown, and any margin for financial shock absorption. New Trader U's January 2026 analysis found that roughly half of Americans tapped into savings to meet routine expenses in 2025 — meaning their reserves are being consumed not by emergencies but by ordinary costs. The recommendation from financial experts including those cited in the GOBankingRates 2026 shrinking middle class guide: the first priority is a dedicated liquid emergency fund (cash, not credit), because cash does not charge interest, does not lower your credit score when used, and breaks the flat-tyre-to-debt cycle that keeps the financial middle in place.References and Further Reading

Ramsey Solutions — State of Personal Finance in America Q1 2026 (Published June 2, 2026) https://www.ramseysolutions.com/budgeting/state-of-personal-financeOWNTIC Blog — The American Middle Class in 2025: Still Shifting, Still Struggling https://blog.owntic.com/the-american-middle-class-in-2025-still-shifting-still-struggling/

Wealthvieu — The Shrinking Middle Class: Data and Trends (May 2026) https://wealthvieu.com/personal-finance/income/shrinking-middle-class/

Fortune — The American Middle Class Didn't Die. It Got Richer — and Felt Poorer (April 12, 2026) https://fortune.com/2026/04/12/did-middle-class-shrink-or-get-richer-feel-poorer/

New Trader U — 10 Reasons the Middle Class Can't Afford Its Old Lifestyle in 2026 (January 2026) https://www.newtraderu.com/2026/01/21/10-reasons-why-the-middle-class-cant-afford-their-old-lifestyle-anymore-in-2026/

Yahoo Finance / GOBankingRates — The Shrinking Middle Class in 2026: 7 Money Moves to Stay There (November 2025) https://finance.yahoo.com/news/shrinking-middle-class-2026-7-194422728.html

Ponderwall — How America's Middle Class Is Struggling to Survive (May 2025) https://ponderwall.com/index.php/2025/05/18/middle-class-america/

ACLI — Middle Class Financial Resilience Index — January 2026 Results (January 27, 2026) https://www.acli.com/posting/nr26-005

WebProNews — America's Economic Middle Is Hollowing Out — Upward (April 6, 2026) https://www.webpronews.com/americas-economic-middle-is-hollowing-out-upward/

0 Comments Comments