Finance

How Open Are You About Money With Your Partner?

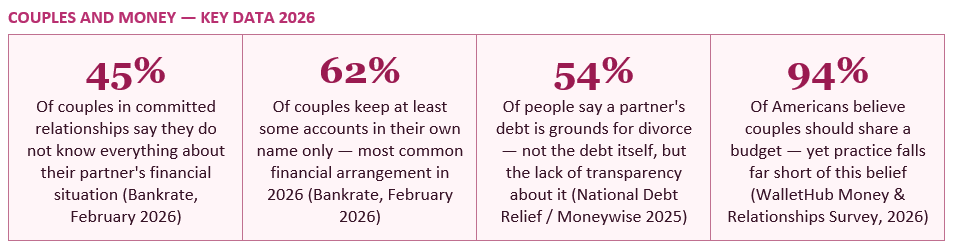

Forty-five per cent of people in committed relationships say they do not know everything about their partner's financial situation, according to Bankrate's February 2026 survey. One in three says financial infidelity is as serious as physical cheating. Yet 94% of Americans believe couples should share a budget. The gap between what people believe about financial openness and what they actually practise is one of the most quietly damaging dynamics in modern relationships — and one of the most fixable.

Financial transparency may not be the most romantic topic, but experts say honest conversations about money can strengthen relationships over time — not weaken them. The Bankrate February 2026 survey data confirms the stakes: 45% of people in committed relationships say they do not know everything about their partner's financial situation. More than one-third say financial infidelity is as serious as physical cheating. And yet the same WalletHub 2026 Money and Relationships survey found that 94% of Americans believe couples should share a budget. The gap between what people believe about financial openness and what they actually do is not a small rounding error. It is a chasm that sits at the centre of many unhappy relationships.

Money conversations in relationships are not primarily about money. They are about trust, values, priorities, and the kind of future each person is trying to build. A couple that cannot talk openly about finances is a couple that is avoiding their most significant shared project. A couple that can is one that has done the harder emotional work of making financial partnership as real and deliberate as romantic partnership.

Financial conflicts are so significant that 54% of people see a partner's debt as grounds for divorce. It's not the debt itself that's the dealbreaker for modern relationships — it's the lack of communication and transparency that's problematic.

— MONEYWISE — HOW TO MANAGE SHARED FINANCES IN A RELATIONSHIP: SURVEY 2025

The headline finding is that 45% of couples lack full financial transparency. More specifically, 62% of couples in committed relationships keep at least some financial accounts in their own name only — making partial financial separation the most common arrangement rather than the exception. This is not inherently problematic — financial independence within a relationship is legitimate and healthy for many couples. What is problematic is when the separation of accounts becomes a cover for concealment.

Moneywise's 2025 survey of 555 people in relationships found that financial secrets are more common than most people assume. When asked about the biggest challenges in managing shared finances, 42% cited difficulty balancing personal spending with shared financial responsibilities — a tension that is almost impossible to resolve without transparent communication about both. The survey also found that 27% of couples have different financial goals or priorities — a significant compatibility gap that cannot be addressed if neither partner knows what the other's financial situation actually is.

The generational picture adds another layer. North Country Now's April 2026 analysis of dater preferences found that 89% of working professionals aged 21 to 35 say financial transparency is a dealbreaker in a relationship — ranking it nearly as high as emotional honesty as a requirement for commitment. The generation that grew up watching their parents' generation fight about money has decided, at scale, that financial transparency is non-negotiable. Yet the same data shows that many couples still find it difficult to put this principle into practice.

Moneywise (2025) notes: 'Left unchecked, these financial secrets can impact trust, strain relationships and even lead to long-term financial instability.' The instability is not only financial — the relational damage of discovered financial infidelity frequently parallels the relational damage of other forms of betrayal.

The first barrier is shame. Money is deeply entangled with identity, capability, and self-worth in most cultures. Admitting to debt, low savings, financial mistakes, or a lower income than a partner feels exposing in a way that few other disclosures do. The person carrying $20,000 in student debt often fears that revealing it will change how their partner sees them — as irresponsible, as a burden, as less of an equal. This fear is usually unfounded, but it is powerful enough to sustain years of concealment.

The second barrier is conflicting money personalities. Moneywise's survey found that 27% of couples have different financial goals or priorities — and many avoid the conversation precisely because they know the difference exists and fear the conflict it will generate. A saver and a spender in the same relationship often operate a kind of unspoken détente: as long as neither forces the conversation, both can avoid the discomfort of the disagreement. The cost is that they also never build toward shared goals.

The third barrier, identified by the Bankrate survey findings, is simply habit. Many couples never establish a pattern of financial conversation because they never started one early in the relationship, and the longer they wait, the more it seems like starting the conversation implies something is wrong. Experts cited in the Bankrate February 2026 analysis recommend planning ahead: 'Setting aside a specific time and choosing a neutral setting can help reduce tension. Establish ground rules beforehand, including no judgment and a focus on open dialogue. The goal is to share information, not assign blame.'

First, set a time and a context in advance. Do not ambush your partner with a financial conversation at the end of a long day, during dinner, or immediately after a financial tension event. Suggest it days ahead: 'I'd really like us to spend an hour this weekend talking about our finances and where we want to be in five years — is Saturday morning good?' The advance notice removes the surprise, the evening timing creates calm, and framing it as future-focused rather than problem-focused removes the implied criticism.

Second, establish ground rules before the first number is mentioned. Both people agree: no judgment, no score-keeping, no 'I told you so.' The goal is shared understanding, not winning. If one partner earns more, that is not a power card to be played. If one partner has debt, that is a fact to be understood and planned for, not a shame to be wielded. Both parties are on the same team trying to solve a shared problem.

Third, start with aspirations rather than deficits. The conversation that begins 'I'd love for us to buy a house in three years — what would we need to make that happen?' is a fundamentally different conversation from 'we never talk about money and I'm worried about our finances.' Both may lead to the same place, but the former is an invitation to a shared future. The latter feels like an accusation. Starting with what you want rather than what you are afraid of dramatically changes the emotional temperature of the conversation.

Fourth, use 'we' language throughout. 'Our debt,' 'our savings goal,' 'our spending,' 'what we earn together.' The financial situation — whatever it is — belongs to both of you as a team, not to one partner as a problem and the other as a judge. This linguistic shift is not trivial: it reframes the conversation from adversarial to collaborative at the level of language, and that reframe changes how both people hear what is being said.

Bankrate's February 2026 survey found that 62% of couples keep at least some accounts in their own name only — making partial separation the most common arrangement. This finding should not be read as a recommendation for or against joint finances. It is simply a description of what most couples do.

The specific model matters less than the agreement. Two people who agree on and actively manage any of these four structures are in a fundamentally better financial position than two people who have never explicitly discussed which model they are using.

Western & Southern Financial's 2025 study on financial transparency in marriage found a direct link between shared financial vision and relationship satisfaction. Couples who had explicitly discussed and agreed on long-term financial goals reported significantly higher relationship satisfaction than those who had not — regardless of their actual income level or net worth. The correlation was with vision, not wealth.

A practical shared financial vision has three components. First, a shared destination: the specific life milestone or financial position you are both working toward (owning a home, retiring at 60, paying for children's education, building a business). Second, a shared timeline: by when, in approximate terms. Third, a shared contribution agreement: how each partner's income and effort contributes toward the shared destination. This does not have to be perfectly equal — it has to be explicitly agreed and revisited annually as circumstances change.

The annual 'money date with a purpose' — a longer, more strategic conversation once a year covering net worth progress, goal revision, and major upcoming financial decisions — is the natural vehicle for maintaining and updating the shared vision. Couples who hold this conversation consistently navigate financial change — income shifts, unexpected expenses, changed priorities — without the financial surprises that, left unaddressed, become relationship crises.

Financial transparency is not about forcing a partner into a structure they are uncomfortable with, or about eliminating all financial individuality in a relationship. It is about ensuring both people have the information they need to build a shared life intentionally rather than blindly. A couple that knows each other's financial reality, agrees on how to structure their joint finances, works toward at least one shared goal, and holds a regular money conversation is not just financially better off — they are relationally stronger, because they have done the harder work of being genuinely honest with each other about one of the most revealing things about who they are.

News9.com — Bankrate Survey: 45% of Couples Lack Financial Transparency (February 2026) https://www.news9.com/oklahoma-city-news/bankrate-survey-couples-financial-transparency

Moneywise — How to Manage Shared Finances in a Relationship (Survey 2025) https://moneywise.com/research/shared-finances

WalletHub — Money & Relationships Survey 2026 https://wallethub.com/blog/money-and-relationships-survey/139437

North Country Now — The 46% Ready for Commitment: What the Data Really Says About What Singles Want in 2026 (April 2026) https://www.northcountrynow.com/premium/stacker/stories/the-46-ready-for-commitment-what-the-data-really-says-about-what-singles-want-in-2026,367026

CPA Practice Advisor — Most Couples Keep At Least Some Of Their Money Separate, Survey Reveals (February 2026) https://www.cpapracticeadvisor.com/2026/02/12/most-couples-keep-at-least-some-of-their-money-separate-survey-reveals/178000/

Western & Southern Financial — Money Talks Couples Can't Afford to Skip (January 2025) https://www.westernsouthern.com/money-conversations-before-marriage-2025

Newson6 — Bankrate Survey: 45% of Couples Lack Financial Transparency (February 2026) https://www.newson6.com/yourmoneymatters/bankrate-survey-couples-financial-transparency

National Debt Relief — Financial Infidelity Statistics and Data https://www.nationaldebtrelief.com/blog/financial-infidelity-statistics/

TABLE OF CONTENTS

- Why Money Is the Last Relationship Taboo

- The Data: How Financially Transparent Are Couples Really?

- What Financial Infidelity Actually Looks Like

- Why Couples Avoid Money Conversations — and Why That Costs Them

- The Financial Compatibility Quiz: How Aligned Are You?

- The Five Money Conversations Every Couple Needs to Have

- How to Start the Money Conversation Without Starting a Fight

- Joint vs Separate vs Hybrid Finances: Finding Your Model

- Building a Shared Financial Vision

- What Good Financial Openness Looks Like in Practice

- Conclusion

- Frequently Asked Questions

- References

Why Money Is the Last Relationship Taboo

We live in an era of radical personal disclosure. People share their health struggles, their family conflicts, their career failures, and their most intimate emotional experiences with anyone who follows them on social media. And yet the question 'how much do you earn?' remains, for many couples, more uncomfortable than almost any other. Money is the last great taboo in relationships — and the cost of that silence is measurable in relationship satisfaction, financial outcomes, and in many cases, in the relationship itself.Financial transparency may not be the most romantic topic, but experts say honest conversations about money can strengthen relationships over time — not weaken them. The Bankrate February 2026 survey data confirms the stakes: 45% of people in committed relationships say they do not know everything about their partner's financial situation. More than one-third say financial infidelity is as serious as physical cheating. And yet the same WalletHub 2026 Money and Relationships survey found that 94% of Americans believe couples should share a budget. The gap between what people believe about financial openness and what they actually do is not a small rounding error. It is a chasm that sits at the centre of many unhappy relationships.

Money conversations in relationships are not primarily about money. They are about trust, values, priorities, and the kind of future each person is trying to build. A couple that cannot talk openly about finances is a couple that is avoiding their most significant shared project. A couple that can is one that has done the harder emotional work of making financial partnership as real and deliberate as romantic partnership.

Financial conflicts are so significant that 54% of people see a partner's debt as grounds for divorce. It's not the debt itself that's the dealbreaker for modern relationships — it's the lack of communication and transparency that's problematic.

— MONEYWISE — HOW TO MANAGE SHARED FINANCES IN A RELATIONSHIP: SURVEY 2025

The Data: How Financially Transparent Are Couples Really?

The research picture on financial transparency in relationships is more concerning — and more nuanced — than the headline numbers suggest. Bankrate's February 2026 survey of 2,564 US adults, conducted in partnership with YouGov, provides the most detailed recent snapshot.The headline finding is that 45% of couples lack full financial transparency. More specifically, 62% of couples in committed relationships keep at least some financial accounts in their own name only — making partial financial separation the most common arrangement rather than the exception. This is not inherently problematic — financial independence within a relationship is legitimate and healthy for many couples. What is problematic is when the separation of accounts becomes a cover for concealment.

Moneywise's 2025 survey of 555 people in relationships found that financial secrets are more common than most people assume. When asked about the biggest challenges in managing shared finances, 42% cited difficulty balancing personal spending with shared financial responsibilities — a tension that is almost impossible to resolve without transparent communication about both. The survey also found that 27% of couples have different financial goals or priorities — a significant compatibility gap that cannot be addressed if neither partner knows what the other's financial situation actually is.

The generational picture adds another layer. North Country Now's April 2026 analysis of dater preferences found that 89% of working professionals aged 21 to 35 say financial transparency is a dealbreaker in a relationship — ranking it nearly as high as emotional honesty as a requirement for commitment. The generation that grew up watching their parents' generation fight about money has decided, at scale, that financial transparency is non-negotiable. Yet the same data shows that many couples still find it difficult to put this principle into practice.

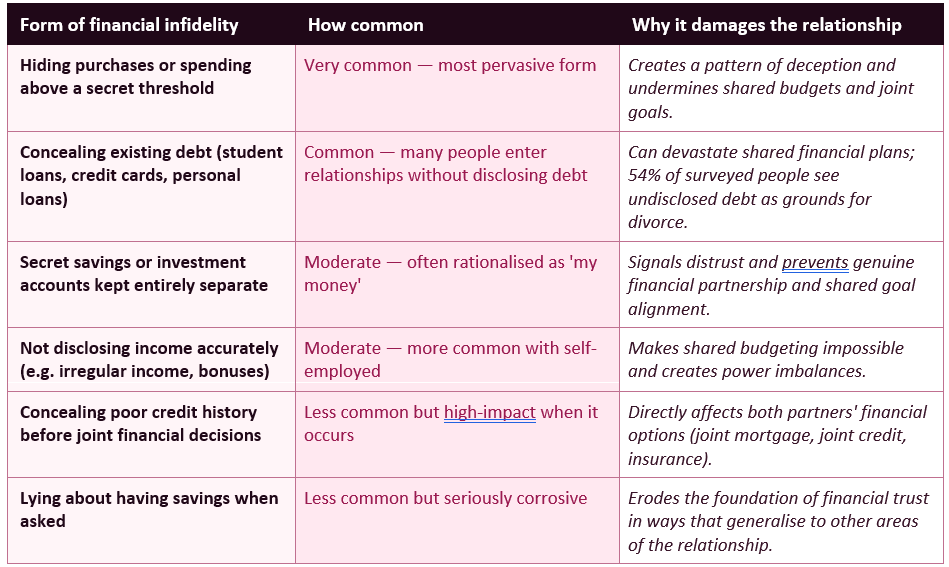

What Financial Infidelity Actually Looks Like

Financial infidelity — keeping significant financial secrets from a partner — is more common, more varied, and more damaging than most couples realise until they encounter it. It does not require hiding a second bank account or a secret gambling habit (though these do occur). It exists on a spectrum, and many people engage in milder forms without fully recognising them as a form of deception.Moneywise (2025) notes: 'Left unchecked, these financial secrets can impact trust, strain relationships and even lead to long-term financial instability.' The instability is not only financial — the relational damage of discovered financial infidelity frequently parallels the relational damage of other forms of betrayal.

Why Couples Avoid Money Conversations — and Why That Costs Them

If financial transparency is so widely valued — 94% believe couples should share a budget, 89% of younger daters say it is a dealbreaker — why do 45% of committed couples lack it? The barriers to money conversations in relationships are real and worth understanding rather than dismissing.The first barrier is shame. Money is deeply entangled with identity, capability, and self-worth in most cultures. Admitting to debt, low savings, financial mistakes, or a lower income than a partner feels exposing in a way that few other disclosures do. The person carrying $20,000 in student debt often fears that revealing it will change how their partner sees them — as irresponsible, as a burden, as less of an equal. This fear is usually unfounded, but it is powerful enough to sustain years of concealment.

The second barrier is conflicting money personalities. Moneywise's survey found that 27% of couples have different financial goals or priorities — and many avoid the conversation precisely because they know the difference exists and fear the conflict it will generate. A saver and a spender in the same relationship often operate a kind of unspoken détente: as long as neither forces the conversation, both can avoid the discomfort of the disagreement. The cost is that they also never build toward shared goals.

The third barrier, identified by the Bankrate survey findings, is simply habit. Many couples never establish a pattern of financial conversation because they never started one early in the relationship, and the longer they wait, the more it seems like starting the conversation implies something is wrong. Experts cited in the Bankrate February 2026 analysis recommend planning ahead: 'Setting aside a specific time and choosing a neutral setting can help reduce tension. Establish ground rules beforehand, including no judgment and a focus on open dialogue. The goal is to share information, not assign blame.'

The Financial Compatibility Quiz: How Aligned Are You?

Before the conversations, it helps to understand where you and your partner currently stand relative to each other on the key financial dimensions. The following questions are designed to surface differences in values and assumptions — not to judge either position, but to make them visible.Ten financial compatibility questions every couple should discuss

- Do you know your partner's approximate take-home income? Does your partner know yours? (If either answer is no, this is the starting point.)

- Do you know the approximate total of your partner's debts — credit cards, student loans, car loans, personal loans, mortgage? Does your partner know yours?

- Do you broadly agree on what constitutes a 'big purchase' that should be discussed before being made? And do you both keep to that agreement?

- Do you have a shared financial goal that you are both actively working toward — a house deposit, a specific savings target, an investment, a holiday fund?

- If one of you lost your job tomorrow, do you know how long the household could sustain its current lifestyle on existing savings? Do you both know this?

- Do you know your partner's credit score approximately? Does your partner know yours?

- Do you agree on how retirement savings should be approached — contribution levels, when to start, what retirement might look like?

- Do you know whether your partner has a will? Does your partner know whether you have one?

- If you have children or plan to, do you have an agreed approach to how child-related costs are managed?

- When you last had a significant financial disagreement, was it resolved with both people feeling heard — or was it avoided, deferred, or won by one side?

The Five Money Conversations Every Couple Needs to Have

There are five specific financial conversations that distinguish couples who build genuine financial partnership from those who muddle through with separate, opaque money lives. These are not one-time conversations — they are ongoing dialogues that deepen over time.Conversation 1: The Financial History Talk

Before combining anything financial — a household, a joint account, a shared goal — both partners need to share their financial histories. Not in a confessional sense, but in a factual one: the debts they carry, the spending patterns they have, the financial lessons they learned (often through mistakes) in their adult lives before this relationship. This is the conversation that reveals whether there is a debt burden to plan around, a history of financial struggle to understand empathetically, or a fundamentally different relationship with money formed by different upbringings.Conversation 2: The Income and Net Worth Snapshot

Both partners should know each other's approximate take-home income, approximate total savings and investments, and approximate total debt. This is not an audit or an interrogation — it is the basic financial information without which a couple cannot make any joint financial decisions sensibly. Bankrate's survey found that 45% of couples lack this basic transparency. Without it, decisions about housing, lifestyle, savings targets, and retirement are being made in a fog.Conversation 3: The Values and Goals Alignment

Money is the operationalisation of values. Where you spend money reflects what you believe matters. A couple where one person values experiences (travel, restaurants, events) and the other values security (savings, emergency fund, owned property) will have persistent financial friction until they explicitly discuss how their values can be honoured within a shared framework. This conversation does not require both people to want the same things — it requires both people to know what the other wants and to find a plan that makes room for both.Conversation 4: The Shared Goals and Timeline Conversation

Beyond individual values, couples need at least one shared financial goal to work toward together. Moneywise's 2025 survey found that 27% of couples have different financial priorities — but different priorities are not the same as incompatible priorities, if they can be surfaced and discussed. The shared goals conversation asks: what are we building together? A house? An emergency fund? A retirement that allows early freedom? A business? Having an explicit shared goal transforms money management from a source of friction into a joint project.Conversation 5: The Ongoing Monthly Money Date

The four preceding conversations are foundations. The money date is the maintenance. A brief (30 to 60 minute) monthly conversation — not in bed, not during dinner, but in a neutral, calm setting with both people prepared — covers the state of shared finances, progress toward shared goals, any financial concerns either person wants to raise, and any major upcoming expenses to plan for. The WalletHub 2026 survey's experts recommend this explicitly: 'Setting aside a specific time and choosing a neutral setting can help reduce tension.' The monthly money date normalises financial conversation and prevents small concerns from becoming large crises.How to Start the Money Conversation Without Starting a Fight

Knowing that a money conversation is needed and knowing how to start it without it immediately becoming confrontational are different skills. The research-backed approach from the Bankrate February 2026 expert panel has four components that work together.First, set a time and a context in advance. Do not ambush your partner with a financial conversation at the end of a long day, during dinner, or immediately after a financial tension event. Suggest it days ahead: 'I'd really like us to spend an hour this weekend talking about our finances and where we want to be in five years — is Saturday morning good?' The advance notice removes the surprise, the evening timing creates calm, and framing it as future-focused rather than problem-focused removes the implied criticism.

Second, establish ground rules before the first number is mentioned. Both people agree: no judgment, no score-keeping, no 'I told you so.' The goal is shared understanding, not winning. If one partner earns more, that is not a power card to be played. If one partner has debt, that is a fact to be understood and planned for, not a shame to be wielded. Both parties are on the same team trying to solve a shared problem.

Third, start with aspirations rather than deficits. The conversation that begins 'I'd love for us to buy a house in three years — what would we need to make that happen?' is a fundamentally different conversation from 'we never talk about money and I'm worried about our finances.' Both may lead to the same place, but the former is an invitation to a shared future. The latter feels like an accusation. Starting with what you want rather than what you are afraid of dramatically changes the emotional temperature of the conversation.

Fourth, use 'we' language throughout. 'Our debt,' 'our savings goal,' 'our spending,' 'what we earn together.' The financial situation — whatever it is — belongs to both of you as a team, not to one partner as a problem and the other as a judge. This linguistic shift is not trivial: it reframes the conversation from adversarial to collaborative at the level of language, and that reframe changes how both people hear what is being said.

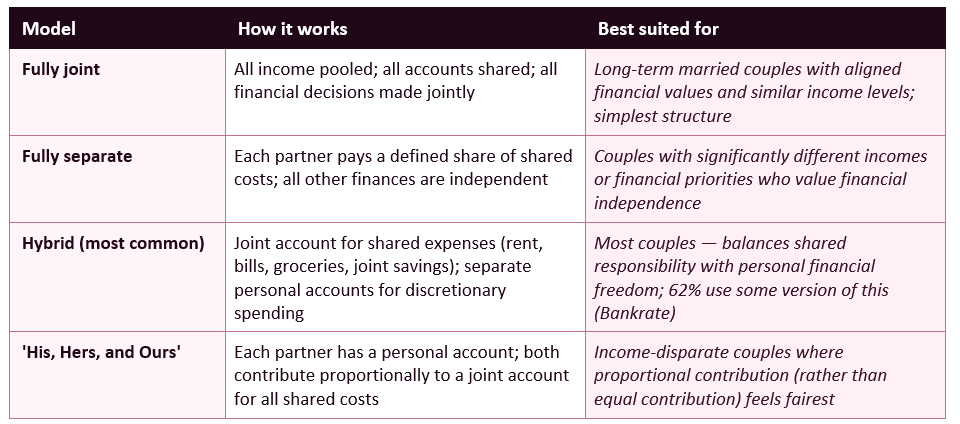

Joint vs Separate vs Hybrid Finances: Finding Your Model

One of the most common practical questions couples face is how to actually structure their finances — and the answer is that there is no universally correct structure, only the one that fits your specific relationship, income levels, and financial goals.Bankrate's February 2026 survey found that 62% of couples keep at least some accounts in their own name only — making partial separation the most common arrangement. This finding should not be read as a recommendation for or against joint finances. It is simply a description of what most couples do.

The specific model matters less than the agreement. Two people who agree on and actively manage any of these four structures are in a fundamentally better financial position than two people who have never explicitly discussed which model they are using.

Building a Shared Financial Vision

The most resilient financial partnerships are built not on perfect alignment of personality or spending habits — those rarely exist — but on a shared vision of what money is for in this relationship. A shared financial vision answers one question: what kind of life are we building together, and how does money serve that life?Western & Southern Financial's 2025 study on financial transparency in marriage found a direct link between shared financial vision and relationship satisfaction. Couples who had explicitly discussed and agreed on long-term financial goals reported significantly higher relationship satisfaction than those who had not — regardless of their actual income level or net worth. The correlation was with vision, not wealth.

A practical shared financial vision has three components. First, a shared destination: the specific life milestone or financial position you are both working toward (owning a home, retiring at 60, paying for children's education, building a business). Second, a shared timeline: by when, in approximate terms. Third, a shared contribution agreement: how each partner's income and effort contributes toward the shared destination. This does not have to be perfectly equal — it has to be explicitly agreed and revisited annually as circumstances change.

The annual 'money date with a purpose' — a longer, more strategic conversation once a year covering net worth progress, goal revision, and major upcoming financial decisions — is the natural vehicle for maintaining and updating the shared vision. Couples who hold this conversation consistently navigate financial change — income shifts, unexpected expenses, changed priorities — without the financial surprises that, left unaddressed, become relationship crises.

What Good Financial Openness Looks Like in Practice

Eight markers of genuine financial openness in a relationship

- Both partners know each other's approximate income: Not necessarily the exact payslip figure, but a realistic approximation that allows meaningful shared financial planning. This is the baseline without which nothing else is possible.

- Both partners know the full picture of shared and individual debts: No hidden credit card balances, no undisclosed loans, no minimum-only payments being concealed. This is the non-negotiable that 54% of people surveyed say matters as much as any other form of trust in a relationship.

- Major purchases are discussed before being made: Whatever the threshold — $100, $500, $1,000 — there is an explicit and mutually agreed definition of what constitutes a major purchase that should be discussed first, and both partners keep to it.

- Shared goals are written down and regularly reviewed: Not just discussed once. Visible, revisited, and updated. The physical act of writing down 'we are saving for a house deposit by 2028' makes it real and reduces the likelihood of either partner spending in ways that undermine it.

- The monthly money conversation is a normal and expected part of the relationship: Not a special event triggered by a crisis, but a routine check-in as normal as a weekly dinner or a joint decision about a holiday. The normalisation of financial conversation is itself the goal.

- Neither partner feels financial shame in the relationship: Both people can talk about financial mistakes, shortfalls, and fears without expecting judgment or criticism. The relationship is a safe space for financial honesty, not a performance of financial competence.

- Financial decisions are made jointly when they affect both people: The pattern where one partner manages all finances and the other is passive, or where one partner has no say in decisions that significantly affect their life, is not financial openness — it is financial control. Genuine openness requires genuine participation.

- Both partners have financial agency: In fully financially open relationships, both partners know how to access all accounts, know where all assets are held, and could manage the finances independently if necessary. Financial dependency created by one partner's deliberate monopoly of financial knowledge is one of the most serious forms of financial control.

CONCLUSION

The 45% of couples who lack financial transparency are not, in most cases, bad partners. They are couples who have never created the specific conditions — the right time, the right language, the right ground rules, the right framing — for a conversation that carries more emotional weight than most relationships have been explicitly prepared to handle. The data from 2026 is clear: what couples want is financial openness. What they often struggle with is how to get there.Financial transparency is not about forcing a partner into a structure they are uncomfortable with, or about eliminating all financial individuality in a relationship. It is about ensuring both people have the information they need to build a shared life intentionally rather than blindly. A couple that knows each other's financial reality, agrees on how to structure their joint finances, works toward at least one shared goal, and holds a regular money conversation is not just financially better off — they are relationally stronger, because they have done the harder work of being genuinely honest with each other about one of the most revealing things about who they are.

Frequently Asked Questions

Why do so many couples avoid talking about money?

The three most common barriers identified by research are shame, the fear of conflict, and habit. Money is deeply entangled with identity and self-worth, so disclosing debt or financial mistakes feels personally exposing in a way that other disclosures do not. Fear of conflict leads couples to maintain an unspoken détente — if neither raises the subject, neither has to face the disagreement. And many couples simply never establish a pattern of financial conversation early in the relationship, making it feel increasingly abnormal to start one later. Bankrate's February 2026 survey experts note that 'avoiding money conversations can create long-term stress and misunderstandings' — and that the practical solution is planning the conversation in advance, choosing a neutral setting, and establishing no-judgment ground rules before any numbers are discussed.What is financial infidelity and how serious is it?

Financial infidelity is keeping significant financial secrets from a partner — hidden debt, undisclosed accounts, secret spending above an agreed threshold, or misrepresenting income or savings. It exists on a spectrum from mild (occasional undisclosed purchases) to severe (a wholly hidden credit card balance or secret savings account). Moneywise's 2025 survey found that 54% of people consider a partner's debt grounds for divorce — importantly, it is not the debt itself that is seen as the dealbreaker but the lack of transparency about it. Bankrate's February 2026 survey found that more than one-third of respondents consider financial infidelity as serious as physical infidelity. Left unaddressed, financial secrets erode trust in ways that generalise beyond financial matters and frequently prove very difficult to recover from.Should couples combine all their finances?

Not necessarily — and Bankrate's February 2026 survey of 2,564 US adults found that 62% of committed couples keep at least some accounts in their own name only. The most important principle is not which structure couples choose but that both partners explicitly agree on the structure and understand how it works. A fully joint model, a fully separate model, and a hybrid 'His, Hers, and Ours' model are all legitimate — their relative suitability depends on income levels, financial personalities, and relationship dynamics. What is not legitimate is an arrangement where one partner has no agency, no information about shared finances, or no financial independence. Whatever model a couple uses should preserve both people's financial understanding, participation, and dignity.When is the right time to have a money conversation with a partner?

There are two types of timing to consider: when in the relationship, and when in the day. For when in the relationship: the research suggests earlier is better. Couples who establish financial transparency before making major shared financial commitments (moving in together, buying property, having children) are significantly better positioned than those who try to retrofit it after the fact. North Country Now's April 2026 analysis found 89% of working professionals aged 21 to 35 say financial transparency is a dealbreaker — suggesting that younger generations understand the importance of early financial openness. For when in the day: Bankrate's expert advice is to set a specific, planned time in a neutral, calm setting — not during dinner, not in bed, not in the heat of a financial disagreement. The advance scheduling removes the ambush element and signals that the conversation is important and deliberate.What if my partner refuses to talk about money?

Persistent refusal to discuss finances in a committed relationship is itself a significant relationship signal. It may indicate financial shame that requires empathetic and patient engagement to overcome, financial anxiety that would benefit from professional support, a learned pattern from their family of origin around financial secrecy, or in more serious cases, a deliberate concealment of financial information that constitutes financial control. The approach recommended by financial and relationship experts is to start with curiosity and no-judgment framing ('I'd love to understand our finances together — not to judge anything, but because it matters to both of us'), to use a relationship therapist or financial planner as a neutral third party if direct conversations remain unproductive, and to recognise that if a partner consistently refuses any financial transparency in a relationship that involves shared commitments, that refusal is a form of financial incompatibility that deserves honest evaluation.References

Bankrate — Survey: Most Couples Keep At Least Some Of Their Money Separate (February 2026) https://www.bankrate.com/credit-cards/news/couples-finances/News9.com — Bankrate Survey: 45% of Couples Lack Financial Transparency (February 2026) https://www.news9.com/oklahoma-city-news/bankrate-survey-couples-financial-transparency

Moneywise — How to Manage Shared Finances in a Relationship (Survey 2025) https://moneywise.com/research/shared-finances

WalletHub — Money & Relationships Survey 2026 https://wallethub.com/blog/money-and-relationships-survey/139437

North Country Now — The 46% Ready for Commitment: What the Data Really Says About What Singles Want in 2026 (April 2026) https://www.northcountrynow.com/premium/stacker/stories/the-46-ready-for-commitment-what-the-data-really-says-about-what-singles-want-in-2026,367026

CPA Practice Advisor — Most Couples Keep At Least Some Of Their Money Separate, Survey Reveals (February 2026) https://www.cpapracticeadvisor.com/2026/02/12/most-couples-keep-at-least-some-of-their-money-separate-survey-reveals/178000/

Western & Southern Financial — Money Talks Couples Can't Afford to Skip (January 2025) https://www.westernsouthern.com/money-conversations-before-marriage-2025

Newson6 — Bankrate Survey: 45% of Couples Lack Financial Transparency (February 2026) https://www.newson6.com/yourmoneymatters/bankrate-survey-couples-financial-transparency

National Debt Relief — Financial Infidelity Statistics and Data https://www.nationaldebtrelief.com/blog/financial-infidelity-statistics/

0 Comments Comments