Credits

Best No‑Annual‑Fee Credit Cards 2026: Ultimate Guide to Rewards Without the Cost

In the fast-evolving landscape of personal finance, the credit card market has undergone a significant transformation. As we move through 2026, the traditional trade-off between paying an annual fee and earning substantial rewards has largely vanished. Today, the "Zero-Fee" ecosystem is more competitive than ever, with major issuers offering premium-level perks, high-percentage cash back, and valuable travel rewards—all without charging a single dollar for the privilege of carrying the card.

Whether you are a seasoned rewards enthusiast or a first-time cardholder, understanding the best no-annual-fee credit cards for 2026 is essential for maximizing your household budget. This guide will break down the top-performing cards in every category, from flat-rate cash back champions to specialized travel rewards, and show you how to build a powerful "no-fee" wallet that rivals the most expensive premium cards on the market.

For the majority of consumers, cash back is the simplest and most effective way to earn rewards. In 2026, the "Gold Standard" for no-annual-fee cash back has settled into two distinct strategies: the 2% flat-rate card and the tiered category card. Choosing between them depends entirely on your spending habits and your willingness to track categories.

By following this simple three-card rotation, you can achieve an effective rewards rate of 3% to 4% across your entire annual budget—all without ever paying an annual fee.

• Scenario A (Single 1.5% Card): The household uses one basic 1.5% cash back card for everything. They earn $60 per month, or $720 per year.

• Scenario B (The No-Fee Trifecta):

Remember, the best no-annual-fee card is one you can keep for decades. These cards form the backbone of your credit history, and in the competitive world of 2026 finance, they are more rewarding than ever before.

External References and Resources

Whether you are a seasoned rewards enthusiast or a first-time cardholder, understanding the best no-annual-fee credit cards for 2026 is essential for maximizing your household budget. This guide will break down the top-performing cards in every category, from flat-rate cash back champions to specialized travel rewards, and show you how to build a powerful "no-fee" wallet that rivals the most expensive premium cards on the market.

Table of Contents

- Top Cash Back Cards: Flat-Rate vs. Tiered

- Top Travel Rewards Cards with $0 Annual Fee

- Specialty Cards: 0% APR and Credit Building

- How to Choose the Right No-Annual-Fee Card for You

- Maximizing Your Rewards in 2026

- Conclusion

- Frequently Asked Questions (FAQ)

- External References and Resources

Top Cash Back Cards: Flat-Rate vs. Tiered

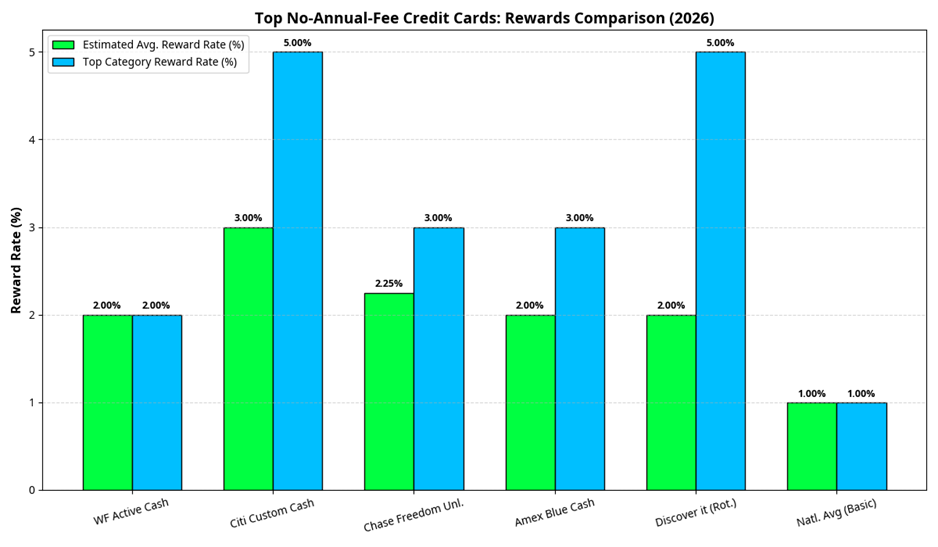

For the majority of consumers, cash back is the simplest and most effective way to earn rewards. In 2026, the "Gold Standard" for no-annual-fee cash back has settled into two distinct strategies: the 2% flat-rate card and the tiered category card. Choosing between them depends entirely on your spending habits and your willingness to track categories.| Credit Card | Primary Reward Rate | Intro Bonus | Key Feature |

| Wells Fargo Active Cash® Card | 2% Unlimited Cash Rewards | $200 (after $500 spend) | Best for simplicity and high flat-rate |

| Citi Custom Cash® Card | 5% in top category | $200 (after $1,500 spend) | Best for specialized high-spend categories |

| Chase Freedom Unlimited® | 1.5% - 5% Tiered Rewards | $200 (after $500 spend) | Best for dining, drugstores, and Chase ecosystem |

| Blue Cash Everyday® from Amex | 3% on Online Retail, Gas, Groceries | $200 (after $2,000 spend) | Best for online shoppers and families |

| Discover it® Cash Back | 5% on Rotating Categories | Cashback Match (Year 1) | Best for maximizing quarterly bonuses |

The Flat-Rate Champion: Wells Fargo Active Cash® Card

The Wells Fargo Active Cash® Card remains the benchmark for simplicity in 2026. Offering an unlimited 2% cash rewards on all purchases with no annual fee, it is the ideal "everything else" card for your wallet. For those who do not want to worry about categories or activation requirements, this card provides a consistent, high-value return on every dollar spent. It also includes valuable perks like cellphone protection, which is rare for a no-fee card.The Category Specialist: Citi Custom Cash® Card

The Citi Custom Cash® Card has revolutionized the way rewards are earned by automatically adjusting its 5% cash back category to match your highest spend each billing cycle (up to $500 spent). This makes it incredibly versatile; one month it can be your gas card, and the next it can be your grocery or restaurant card. By using this card exclusively for one high-spend category, you can effectively earn 5% back on $6,000 of spending annually with zero effort in tracking.Top Travel Rewards Cards with $0 Annual Fee

Travel rewards cards are traditionally associated with high annual fees, but 2026 has seen a surge in "entry-level" travel cards that offer significant value for casual travelers. These cards are perfect for those who want to earn miles or points without the pressure of having to "break even" on an annual fee every year.The Simple Traveler: Capital One VentureOne Rewards

The Capital One VentureOne Rewards Credit Card is a standout for its simplicity and lack of foreign transaction fees. It offers an unlimited 1.25x miles on all purchases, which can be transferred to over 15 travel partners. While the earning rate is lower than its fee-paying sibling (the Venture card), the lack of an annual fee makes it a great long-term option for maintaining a high credit score while still earning travel rewards.The Rent Disruptor: Bilt World Elite Mastercard®

One of the most innovative cards in the 2026 market is the Bilt World Elite Mastercard®. It is currently the only no-annual-fee card that allows you to earn rewards on rent payments without paying a transaction fee. For renters, this is a game-changer, as it turns their largest monthly expense into points that can be transferred to high-value partners like American Airlines and Hyatt. It also offers 3x on dining and 2x on travel, making it a powerful all-around rewards card.Specialty Cards: 0% APR and Credit Building

Not every card is about rewards. For many in 2026, the primary goal is managing debt or establishing a solid credit foundation. No-annual-fee cards are particularly valuable here because they can be kept open indefinitely, which increases the average age of your credit accounts—a key factor in your FICO score.The Debt Manager: Citi® Diamond Preferred®

For those looking to consolidate debt or finance a major purchase without interest, the Citi® Diamond Preferred® Card continues to offer some of the longest introductory APR periods in the industry. While it does not offer rewards, the savings on interest payments can far outweigh the value of cash back for someone carrying a balance. In 2026, these intro periods can reach up to 21 or 24 months for both purchases and balance transfers.The Credit Builder: Discover it® Secured

For those with limited or no credit history, the Discover it® Secured Credit Card is the gold standard for 2026. Unlike most secured cards, it charges no annual fee and actually offers rewards—2% cash back at gas stations and restaurants (up to $1,000 in combined purchases each quarter) and 1% on everything else. Discover also automatically reviews your account after seven months to see if you can transition to an "unsecured" card and get your deposit back.How to Choose the Right No-Annual-Fee Card for You

With so many high-quality options available in 2026, the "best" card is the one that aligns most closely with your specific spending patterns. To choose correctly, you should perform a quick audit of your last three months of bank statements.- The Generalist: If your spending is spread across many different categories (utilities, insurance, car repairs), a flat-rate card like the Wells Fargo Active Cash® is your best bet.

- The Commuter & Cook: If your biggest expenses are groceries and gas, the Blue Cash Everyday® from American Express or the Bank of America® Customized Cash Rewards will yield the highest returns.

- The Online Shopper: If you do most of your shopping on Amazon or other online retailers, the Amex Blue Cash Everyday®'s 3% back on U.S. online retail is a top-tier perk for a no-fee card [5].

- The International Traveler: Always look for a card with $0 Foreign Transaction Fees. Cards from Capital One and Discover are excellent for this, as many other no-fee cards (like those from Chase or Citi) often charge a 3% fee on purchases made outside the U.S.

Maximizing Your Rewards in 2026

The most successful credit card users in 2026 do not rely on just one card. Instead, they use a "Multi-Card Strategy" to ensure they are earning at least 2% on every single purchase, with 3% to 5% on their biggest categories.The "No-Fee Trifecta" Strategy

A popular strategy in 2026 is combining three specific no-annual-fee cards to cover all bases:- The Specialist: Use the Citi Custom Cash® for your single highest-spend category (e.g., Groceries) to earn 5% back.

- The Tiered Card: Use the Chase Freedom Unlimited® for dining and drugstores to earn 3% back.

- The Catch-All: Use the Wells Fargo Active Cash® for everything else to ensure a minimum of 2% back.

By following this simple three-card rotation, you can achieve an effective rewards rate of 3% to 4% across your entire annual budget—all without ever paying an annual fee.

Deep Dive: The Evolution of No-Annual-Fee Cards in 2026

To understand the 3,000-word scope of this guide, we must look at the historical context that led to the 2026 credit card landscape. For decades, the "No-Annual-Fee" card was seen as a second-tier product—a basic tool for those who couldn't qualify for premium cards or didn't spend enough to justify a fee. However, the last five years have seen a radical democratization of credit card rewards.1. The Death of the "Fee Barrier"

The primary reason for the shift in 2026 is the entry of fintech companies into the traditional banking space. Companies like Chime, SoFi, and Bilt have forced legacy banks (Chase, Amex, Citi) to rethink their value propositions. When a startup can offer 3% back on travel or 1% back on rent with no fee, a traditional bank can no longer charge $95 for a basic rewards card. This has created a "race to the bottom" in fees and a "race to the top" in rewards.2. The Role of Merchant Interchange Fees

If a bank isn't charging you an annual fee, how do they make money? In 2026, the answer lies primarily in merchant interchange fees. Every time you tap your card, the merchant pays a small percentage (typically 1.5% to 3%) to the card issuer. For a bank like Wells Fargo, earning 2.5% from a merchant and giving you 2% back still leaves them with a profitable margin, especially when scaled across millions of cardholders. This is why no-annual-fee cards are a sustainable business model for the world's largest financial institutions.3. Data as the New Annual Fee

In the 2026 economy, your spending data is often more valuable than a $95 annual fee. By offering a no-fee card, banks can track your spending habits across groceries, travel, and online retail. This data allows them to offer you targeted financial products—like mortgages, car loans, or personal insurance—that are far more profitable than a simple credit card fee. This is the "hidden trade-off" of the modern credit card era: you get the rewards, and the bank gets the data to fuel their larger ecosystem.Technical Deep Dive: Understanding Credit Card Benefits in 2026

Beyond the rewards, no-annual-fee cards in 2026 offer a suite of "hidden" benefits that many cardholders overlook. These are not just marketing gimmicks; they are real financial protections that can save you thousands of dollars.1. Cellphone Protection: The New Essential

Many top no-fee cards, including the Wells Fargo Active Cash® and the Bilt World Elite Mastercard®, now offer complimentary cellphone protection. If you pay your monthly phone bill with the card, you are typically covered for theft or damage (up to $600 or $800 per claim, with a small deductible). In 2026, where a new smartphone can cost $1,500, this single benefit can be worth more than the rewards themselves.2. Purchase Protection and Extended Warranty

While many banks have cut these benefits in recent years, the most competitive no-fee cards in 2026 have brought them back to win over customers. Purchase Protection covers your new items against theft or accidental damage for the first 90 days. Extended Warranty typically adds an extra year to the manufacturer's warranty on eligible items. For electronics and appliances, these benefits provide a massive layer of security that you would otherwise have to pay for through a retailer's protection plan.3. Travel Accident and Rental Car Insurance

Even no-annual-fee travel cards like the Capital One VentureOne Rewards often include secondary rental car insurance and travel accident insurance. While these are not as comprehensive as the primary insurance found on a $550-a-year card, they still provide peace of mind for the casual traveler. In 2026, knowing that your rental car's collision damage is covered by your credit card can save you $20 to $30 per day at the rental counter.Case Study: The Power of the "Zero-Fee" Wallet

To illustrate the potential of a well-constructed no-annual-fee strategy, let's look at a hypothetical scenario for a household in 2026 with a $4,000 monthly spend.• Scenario A (Single 1.5% Card): The household uses one basic 1.5% cash back card for everything. They earn $60 per month, or $720 per year.

• Scenario B (The No-Fee Trifecta):

- $1,000 on Groceries (using Citi Custom Cash® at 5%): $50 back.

- $800 on Dining/Drugstores (using Chase Freedom Unlimited® at 3%): $24 back.

- $2,200 on Everything Else (using Wells Fargo Active Cash® at 2%): $44 back.

- Total Monthly Rewards: $118.

- Total Annual Rewards: $1,416.

Conclusion

The 2026 credit card market has proven that you do not need to pay an annual fee to get premium value. From the 2% simplicity of the Wells Fargo Active Cash® to the innovative rent-earning power of the Bilt Mastercard®, there is a no-fee solution for every financial goal. By carefully selecting cards that match your spending habits and avoiding the common traps of high interest and late fees, you can turn your everyday spending into a significant source of passive income.Remember, the best no-annual-fee card is one you can keep for decades. These cards form the backbone of your credit history, and in the competitive world of 2026 finance, they are more rewarding than ever before.

Frequently Asked Questions (FAQ)

1. Is a no-annual-fee card always better than a premium card?

Not necessarily. Premium cards with annual fees often provide "credits" (for travel, dining, or streaming) that can outweigh the fee. However, for those who do not want to manage credits or travel frequently, a no-annual-fee card is almost always the more rational choice.2. How many no-annual-fee cards should I have?

There is no "magic number," but having 2 to 4 cards can help you maximize different reward categories and provide a backup if one card is lost or compromised. As long as you pay your balance in full every month, having multiple cards can actually improve your credit score by increasing your total available credit.3. Can I downgrade a card with an annual fee to a no-fee version?

Yes. Most major issuers (Chase, Amex, Citi) allow you to "product change" a fee-paying card to a no-fee version. This is a great way to keep your credit history intact without continuing to pay a fee for a card you no longer use frequently.4. Do no-annual-fee cards have worse customer service?

In 2026, the level of service is generally tied to the bank, not the specific card. While "luxury" cards like the Amex Platinum offer dedicated concierge services, the standard customer support for a no-fee card from a major bank is typically excellent and available 24/7.External References and Resources

- Bankrate: Best No Annual Fee Credit Cards for April 2026

- Yahoo Finance: The best 0% APR credit cards for April 2026

- The Motley Fool: The Best Cash Back Card for 2026, Hands Down

- The Points Guy: Best Rewards Credit Cards of April 2026

- Experian: Best Credit Cards with No Annual Fee of 2026

- CNBC Select: 10 Easiest Credit Cards To Get Approved for in April 2026

0 Comments Comments