AI for Personal Finance

AI-Powered Money Management & Agentic AI Explained

Agentic AI — AI that can sense, plan, act, and learn autonomously — is moving from the server room to your current account. Forty-four per cent of finance teams are using it in 2026, up 600% from 2025. This guide explains exactly what it is, what it can do with your money right now, what it cannot be trusted to do yet, and how to stay in control.

Agentic AI is different. An AI agent does not wait for a prompt. It senses its environment — reading your transaction history, monitoring your account balances, tracking market prices, scanning for better deals, watching for fraud signals — then plans the most appropriate action, executes that action autonomously using the tools and permissions available to it, and learns from the outcome to improve future decisions. The IMF's 2026 research note defines agentic AI as 'autonomous systems that sense their environment, set goals, and perform multistep tasks with little human input.' The critical word is multistep: agentic AI does not just answer questions, it completes tasks.

A practical example from the IMF's own analysis illustrates the concept clearly: in the commercial sector, an agentic AI system monitors household gas tank levels, identifies the most cost-effective propane supplier, and automatically arranges a refill — without the homeowner doing anything beyond setting the initial parameters. In finance, the equivalent is an AI agent that monitors your current account, detects that you have excess cash relative to your goals, identifies the best available savings rate, and automatically transfers the surplus to a high-yield account — all without you logging into a banking app.

Agentic AI moves finance from 'AI that answers questions' to 'AI that takes actions.' The difference for consumers is the same as the difference between a sat-nav that gives you directions and a self-driving car that does the driving.

— AI MAGICX — AGENTIC AI IN FINANCE: 12 DEPLOYMENTS, MAY 2026

The financial investment reflects the urgency. KPMG estimates global market spending on agentic AI in financial services at $50 billion in 2025, growing to a projected $7.78 billion market in 2026 at the individual deployment level and $43.52 billion by 2031 according to Mordor Intelligence — a compound annual growth rate of 41%. These are not speculative projections: they reflect capital already committed and deployments already in production.

The return on that investment is compelling. KPMG documents an average $3.50 return for every $1 invested in agentic AI across more than 17 million firms studied. In wealth management specifically, Neurons Lab reports that agentic AI is cutting advisor time on manual prospecting by 40 to 50% and increasing net new assets under management by 30 to 40%. McKinsey found that credit analysis deployments showed 20% to 60% productivity improvement within the first year. In 2025 alone, 50 of the world's largest banks announced more than 160 agentic AI use cases, according to McKinsey.

In the UK, open banking infrastructure combined with agentic AI has enabled a new generation of money management apps — including Cleo, Plum, and Chip — that go significantly beyond the passive round-up saving tools of five years ago. These apps now monitor spending patterns continuously, predict upcoming bills from transaction history, move money between current and savings accounts to optimise interest earned, and alert users to potential overdraft situations days in advance. The agentic element is the continuous monitoring and autonomous action that happens between the user's interactions with the app, not just when the user asks a question.

Citi's 2025 report on agentic AI in financial services, cited by Neurons Lab, documents deployment across wealth management (personalised portfolio rebalancing and prospecting), corporate banking (cash management and treasury optimisation), institutional investors (compliance monitoring and reporting), and insurance (claims processing and underwriting). The BIS (Bank for International Settlements) has noted that AI agents can independently manage liquidity and prioritise payments within real-time gross settlement systems.

Modern agentic fraud detection systems continuously monitor transaction streams in real time, learning the normal behaviour patterns of each individual customer. When a transaction deviates from that customer's personal baseline — rather than just from a generic population norm — the agent can take immediate autonomous action: temporarily pausing the transaction, sending a real-time verification request to the customer's registered device, logging the incident with full context, and updating the customer's risk profile for future monitoring. The entire process can complete in milliseconds.

Citizens Bank's 2026 survey found that 45% of midsize companies are currently using AI for fraud detection, with the figure rising to 62% for PE firms identifying it as a short-term AI benefit. For consumers, the practical experience is already familiar: the real-time text message asking 'Did you just make a purchase at [merchant] for [amount]?' is, in increasingly sophisticated implementations, the customer-facing output of an agentic AI system that has already taken protective action on the account before it even contacts you.

Agentic AI is changing this. By continuously synthesising data from multiple sources — your transaction history, savings balances, investment portfolio, income patterns, upcoming financial commitments, tax position, and stated goals — agentic financial AI can generate advice that is genuinely personalised to your situation, available at any time, and updated continuously as your circumstances change. This is not the same as a chatbot that answers 'how much should I save?' with a generic 4% rule. It is an agent that knows you have a £4,200 tax bill due in January, a mortgage renewal in March, and a pattern of overspending on online shopping in December, and that adjusts its recommendations accordingly.

Finastra's 2026 research indicates that agentic AI serving as an 'always-on relationship manager' can negotiate personalised financial products in real time, balancing customer preferences with bank risk and regulatory constraints. The practical consumer implication is that the gap between the quality of financial guidance available to a high-net-worth individual with a dedicated adviser and the quality available to an ordinary saver is narrowing for the first time.

In the UK, the open banking regime introduced by the FCA in 2019 created the data infrastructure that makes this possible. Open banking allows regulated third-party apps to access your financial data (with your consent) across multiple providers, giving them a complete view of your spending. The next step — agentic AI acting on that data — is being implemented now. Apps including Plum and Chip already move savings automatically between accounts based on the AI's assessment of your cash flow position. The extension to bill switching — with your explicit permission and a human approval step — is the frontier being crossed in 2026.

BobsGuide's prediction for 2026, building on the Visa and Mastercard standardised frameworks expected to support AI-driven transactions, is the emergence of 'Agentic Commerce': a consumer's AI agent will be authorised to 'browse, select, and transact' on their behalf in real time. In this model, you would not ask an AI to suggest a better insurance plan — the AI would be authorised to find, purchase, and integrate that plan based on real-time data from your spending, investment, and insurance accounts. The consumer receives a notification that the switch has been made and the saving confirmed, rather than a recommendation to act on manually.

Visa and Mastercard are both developing standardised frameworks for AI-driven transactions. These frameworks address the 'authentication problem' — how a payment network verifies that a transaction initiated by an AI agent was genuinely authorised by the human account holder, within the bounds of their stated preferences and spending limits. The emerging solution involves what the IMF calls 'AP2 mandates': cryptographically verifiable permissions that specify the scope, limits, actor identity, and conditions under which an AI agent is authorised to transact. An agent cannot exceed its mandate; any action outside the defined parameters requires explicit new consent from the human.

For consumers, the practical first applications will likely be familiar and low-risk: automatically purchasing the cheapest energy tariff at renewal time (within a pre-approved price range), renewing car insurance at a better rate (with human confirmation before execution), or rebalancing an investment portfolio toward a stated target allocation (with a 24-hour notification window before execution). The more ambitious vision — AI agents browsing, comparing, and purchasing across the full range of consumer spending — will take longer to implement safely and will require robust regulatory frameworks that are still being developed.

AI Magicx documents how agentic AI has transformed the process of comparable company analysis in investment banking, reducing a task that took human analysts 12 to 22 hours to 15 to 45 minutes of agent work plus 2 to 4 hours of human review — a net time saving of 65% to 80%. The same logic applies to credit risk analysis for lending. A US bank cited by McKinsey used AI agents to change the way it creates credit risk memos, achieving a 20% to 60% increase in productivity and a 30% improvement in credit turnaround time. For borrowers, faster credit analysis means faster loan decisions — reducing the time between application and funding from days to hours or minutes.

The potential for AI to consider a broader range of data than traditional credit models — including utility payment history, rent payments, and transactional cash flow patterns rather than just credit file entries — also presents an opportunity to extend credit access to underserved borrowers who have limited traditional credit histories. This is the same dynamic driving the integration of rent and utility payment data into mortgage credit scoring in the US (covered in our companion mortgage article), but applied across a wider range of lending categories.

What is changing in 2026 is the degree to which AI moves from background processing to front-of-stage action. The question for consumers is not whether to use AI-powered financial tools but how to use them wisely — claiming their genuine benefits while maintaining the oversight and understanding necessary to catch errors and stay in control.

The consumer who benefits most from agentic AI in financial services is not the one who hands everything over to automation and never checks in. It is the one who uses AI as a highly capable tool operating within clear parameters they have set, reviews AI-generated recommendations before acting on them for consequential decisions, and maintains enough personal financial literacy to recognise when the AI is wrong.

The opportunity for consumers is real: better fraud protection, more personalised financial guidance, automated savings optimisation, and eventually the ability to delegate routine financial decisions to AI agents operating within clear, consent-based parameters. The risks are also real: hallucination, inadequate guardrails, data privacy exposure, and the legal grey area around AI-agent liability are all active concerns that deserve serious attention. The right response is neither uncritical adoption nor reflexive rejection. It is informed engagement — using these tools with your eyes open, maintaining meaningful oversight, and treating AI as a powerful assistant whose outputs you verify, not an infallible oracle whose decisions you delegate without thought.

Agentic AI refers to AI systems that can take autonomous, multi-step actions without waiting for human prompts. Unlike a chatbot that answers questions when you ask them, an agentic AI agent monitors its environment continuously, plans an appropriate response when something relevant happens, executes that response using the tools and permissions available to it, and learns from the outcome. In finance, this means AI that can detect fraud and block a suspicious transaction, find a better savings rate and move your money, or spot an insurance renewal approaching and initiate a comparison — all without you needing to ask it to.

Citizens Bank — 2026 AI Trends in Financial Management Survey (December 2025) https://www.citizensbank.com/corporate-finance/insights/ai-trends-financial-management-2026.aspx

AI Magicx — Agentic AI in Finance: 12 Ways Banks and Fintechs Are Deploying Now (2026) https://www.aimagicx.com/blog/agentic-ai-finance-banking-deployments-2026

Azilen — Agentic AI in Financial Services: 2026 Definitive Guide https://www.azilen.com/blog/agentic-ai-in-financial-services/

IMF — How Agentic AI Will Reshape Payments (IMF Notes Volume 2026 Issue 004) https://www.elibrary.imf.org/view/journals/068/2026/004/article-A001-en.xml

Finastra — AI in Banking and Financial Services: Trends for 2026 (February 2026) https://www.finastra.com/viewpoints/articles/future-of-ai-in-financial-services-2026

BobsGuide — 5 Biggest Fintech Stories of 2025 and 5 Bold Predictions for 2026 https://www.bobsguide.com/5-biggest-fintech-news-stories-of-2025-and-5-bold-predictions-for-2026/

Keyrus — Top AI Trends Transforming Financial Services for 2026 https://keyrus.com/us/en/insights/top-ai-trends-transforming-financial-services-for-2026

FCA — Open Banking and Payment Services Authorisation Register (UK) https://register.fca.org.uk/

McKinsey — Agentic AI in Financial Services Use Cases (2025 research) https://www.mckinsey.com/industries/financial-services/our-insights

TABLE OF CONTENTS

- What Is Agentic AI? And Why Is It Different?

- The Numbers: How Fast Is This Moving?

- Traditional AI vs Agentic AI in Finance: What Changed?

- What Agentic AI Is Doing With Your Money Right Now

- Use Case 1: Autonomous Fraud Detection and Prevention

- Use Case 2: Hyper-Personalised Financial Advice

- Use Case 3: Automated Bill Switching and Savings Optimisation

- Use Case 4: Agentic Commerce — AI That Spends on Your Behalf

- Use Case 5: Credit Analysis and Lending Automation

- The Risks You Need to Understand

- What This Means for You as a Consumer

- How to Stay in Control: Your Practical Guide

- Conclusion

- Frequently Asked Questions

- References

What Is Agentic AI? And Why Is It Different?

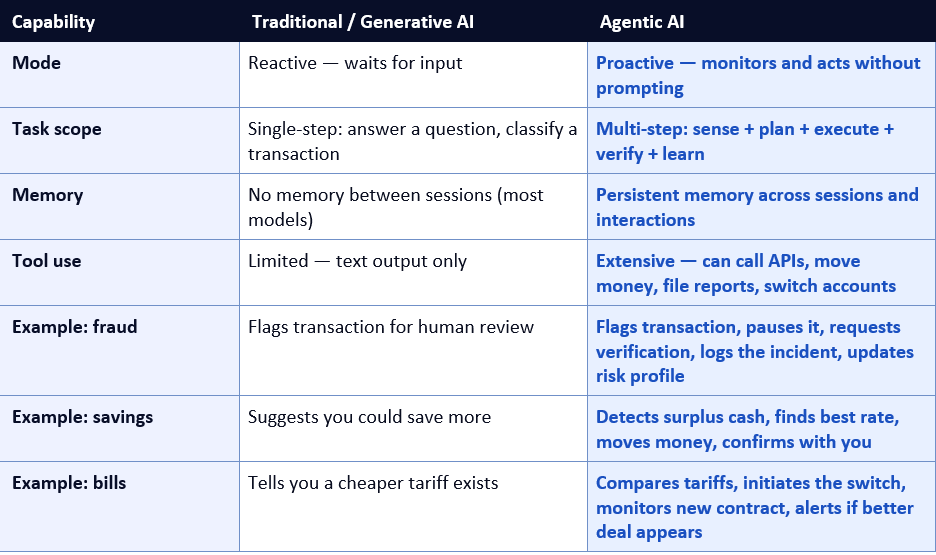

Artificial intelligence has been part of financial services for decades — from the simple rule-based fraud detection systems of the 1990s to the machine learning models that began predicting creditworthiness in the 2010s to the large language models (LLMs) that power today's customer service chatbots. Each generation has been more capable than the last. But all of them shared one fundamental characteristic: they waited to be told what to do.Agentic AI is different. An AI agent does not wait for a prompt. It senses its environment — reading your transaction history, monitoring your account balances, tracking market prices, scanning for better deals, watching for fraud signals — then plans the most appropriate action, executes that action autonomously using the tools and permissions available to it, and learns from the outcome to improve future decisions. The IMF's 2026 research note defines agentic AI as 'autonomous systems that sense their environment, set goals, and perform multistep tasks with little human input.' The critical word is multistep: agentic AI does not just answer questions, it completes tasks.

A practical example from the IMF's own analysis illustrates the concept clearly: in the commercial sector, an agentic AI system monitors household gas tank levels, identifies the most cost-effective propane supplier, and automatically arranges a refill — without the homeowner doing anything beyond setting the initial parameters. In finance, the equivalent is an AI agent that monitors your current account, detects that you have excess cash relative to your goals, identifies the best available savings rate, and automatically transfers the surplus to a high-yield account — all without you logging into a banking app.

Agentic AI moves finance from 'AI that answers questions' to 'AI that takes actions.' The difference for consumers is the same as the difference between a sat-nav that gives you directions and a self-driving car that does the driving.

— AI MAGICX — AGENTIC AI IN FINANCE: 12 DEPLOYMENTS, MAY 2026

The Numbers: How Fast Is This Moving?

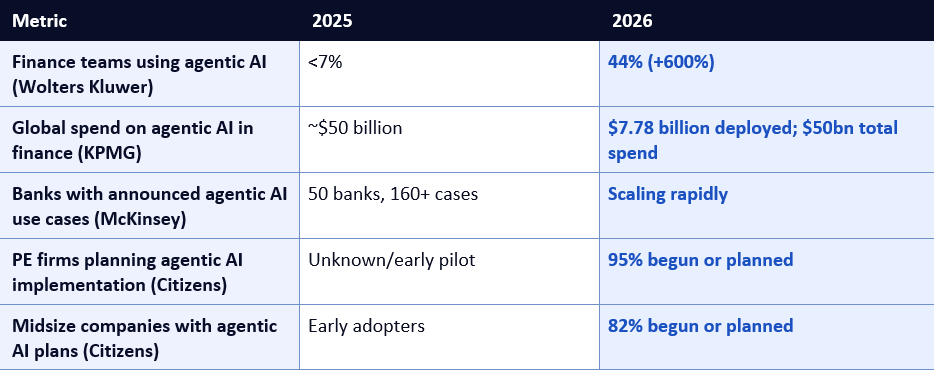

The adoption curve for agentic AI in financial services in 2025 and 2026 is one of the most dramatic in the history of enterprise technology. According to Wolters Kluwer, fewer than 7% of finance teams had deployed any form of agentic AI in January 2025. By Q1 2026, that figure had reached 44% — a 600% year-on-year increase. Citizens Bank's 2026 survey found that 82% of midsize companies and 95% of private equity firms have either begun or plan to implement agentic AI in their operations this year.The financial investment reflects the urgency. KPMG estimates global market spending on agentic AI in financial services at $50 billion in 2025, growing to a projected $7.78 billion market in 2026 at the individual deployment level and $43.52 billion by 2031 according to Mordor Intelligence — a compound annual growth rate of 41%. These are not speculative projections: they reflect capital already committed and deployments already in production.

The return on that investment is compelling. KPMG documents an average $3.50 return for every $1 invested in agentic AI across more than 17 million firms studied. In wealth management specifically, Neurons Lab reports that agentic AI is cutting advisor time on manual prospecting by 40 to 50% and increasing net new assets under management by 30 to 40%. McKinsey found that credit analysis deployments showed 20% to 60% productivity improvement within the first year. In 2025 alone, 50 of the world's largest banks announced more than 160 agentic AI use cases, according to McKinsey.

Traditional AI vs Agentic AI in Finance: What Changed?

To understand why the shift to agentic AI matters for consumers, it helps to understand what the previous generation of AI in finance was actually capable of — and where it fell short.What Agentic AI Is Doing With Your Money Right Now

Agentic AI is not a future technology. It is already operating in production environments at major financial institutions. The most visible consumer-facing deployment is Fidelity's AI assistant Freya, described by AI Magicx as operating as 'a genuine financial advisory agent' — reviewing a customer's complete investment portfolio, identifying concentration risks, tax-loss harvesting opportunities, and rebalancing needs, then presenting options for the customer to approve. The important distinction is that Freya does not just answer questions: it continuously monitors, analyses, and surfaces actionable recommendations across the full portfolio lifecycle.In the UK, open banking infrastructure combined with agentic AI has enabled a new generation of money management apps — including Cleo, Plum, and Chip — that go significantly beyond the passive round-up saving tools of five years ago. These apps now monitor spending patterns continuously, predict upcoming bills from transaction history, move money between current and savings accounts to optimise interest earned, and alert users to potential overdraft situations days in advance. The agentic element is the continuous monitoring and autonomous action that happens between the user's interactions with the app, not just when the user asks a question.

Citi's 2025 report on agentic AI in financial services, cited by Neurons Lab, documents deployment across wealth management (personalised portfolio rebalancing and prospecting), corporate banking (cash management and treasury optimisation), institutional investors (compliance monitoring and reporting), and insurance (claims processing and underwriting). The BIS (Bank for International Settlements) has noted that AI agents can independently manage liquidity and prioritise payments within real-time gross settlement systems.

Use Case 1: Autonomous Fraud Detection and Prevention

Fraud detection is the most mature and most widely deployed agentic AI use case in consumer finance — and the one most likely to have already affected your life without you being aware of it. Traditional fraud detection systems used rule-based models: if a transaction matched certain patterns (unusual location, atypical amount, unfamiliar merchant category), it would be flagged for human review or declined. These systems were static: they applied rules that had been programmed by humans and did not adapt dynamically to new fraud patterns.Modern agentic fraud detection systems continuously monitor transaction streams in real time, learning the normal behaviour patterns of each individual customer. When a transaction deviates from that customer's personal baseline — rather than just from a generic population norm — the agent can take immediate autonomous action: temporarily pausing the transaction, sending a real-time verification request to the customer's registered device, logging the incident with full context, and updating the customer's risk profile for future monitoring. The entire process can complete in milliseconds.

Citizens Bank's 2026 survey found that 45% of midsize companies are currently using AI for fraud detection, with the figure rising to 62% for PE firms identifying it as a short-term AI benefit. For consumers, the practical experience is already familiar: the real-time text message asking 'Did you just make a purchase at [merchant] for [amount]?' is, in increasingly sophisticated implementations, the customer-facing output of an agentic AI system that has already taken protective action on the account before it even contacts you.

Use Case 2: Hyper-Personalised Financial Advice

For most of financial history, genuinely personalised financial advice has been available only to those who could afford a financial adviser — typically those with significant wealth, who pay annual fees of £2,000 to £10,000 or more. For everyone else, financial advice has meant generic online calculators, standardised robo-advisors, and product brochures designed for the average customer rather than for your specific situation.Agentic AI is changing this. By continuously synthesising data from multiple sources — your transaction history, savings balances, investment portfolio, income patterns, upcoming financial commitments, tax position, and stated goals — agentic financial AI can generate advice that is genuinely personalised to your situation, available at any time, and updated continuously as your circumstances change. This is not the same as a chatbot that answers 'how much should I save?' with a generic 4% rule. It is an agent that knows you have a £4,200 tax bill due in January, a mortgage renewal in March, and a pattern of overspending on online shopping in December, and that adjusts its recommendations accordingly.

Finastra's 2026 research indicates that agentic AI serving as an 'always-on relationship manager' can negotiate personalised financial products in real time, balancing customer preferences with bank risk and regulatory constraints. The practical consumer implication is that the gap between the quality of financial guidance available to a high-net-worth individual with a dedicated adviser and the quality available to an ordinary saver is narrowing for the first time.

Use Case 3: Automated Bill Switching and Savings Optimisation

One of the most practically useful consumer applications of agentic AI in 2026 is automated bill management — the ability of an AI agent to monitor your utility contracts, insurance policies, broadband, and other recurring costs, identify when better deals are available, and either alert you to act or, with appropriate permissions, initiate the switch on your behalf.In the UK, the open banking regime introduced by the FCA in 2019 created the data infrastructure that makes this possible. Open banking allows regulated third-party apps to access your financial data (with your consent) across multiple providers, giving them a complete view of your spending. The next step — agentic AI acting on that data — is being implemented now. Apps including Plum and Chip already move savings automatically between accounts based on the AI's assessment of your cash flow position. The extension to bill switching — with your explicit permission and a human approval step — is the frontier being crossed in 2026.

BobsGuide's prediction for 2026, building on the Visa and Mastercard standardised frameworks expected to support AI-driven transactions, is the emergence of 'Agentic Commerce': a consumer's AI agent will be authorised to 'browse, select, and transact' on their behalf in real time. In this model, you would not ask an AI to suggest a better insurance plan — the AI would be authorised to find, purchase, and integrate that plan based on real-time data from your spending, investment, and insurance accounts. The consumer receives a notification that the switch has been made and the saving confirmed, rather than a recommendation to act on manually.

Use Case 4: Agentic Commerce — AI That Spends on Your Behalf

Agentic Commerce represents the most far-reaching consumer application of agentic AI — and the one that raises the most important questions about consent, liability, and control. The premise is straightforward: rather than you researching and executing purchases, your AI financial agent does it for you, authorised within parameters you have defined. The IMF's 2026 research note provides a concrete example: an agent that tracks household gas tank levels, identifies the most cost-effective supplier, and arranges a refill automatically.Visa and Mastercard are both developing standardised frameworks for AI-driven transactions. These frameworks address the 'authentication problem' — how a payment network verifies that a transaction initiated by an AI agent was genuinely authorised by the human account holder, within the bounds of their stated preferences and spending limits. The emerging solution involves what the IMF calls 'AP2 mandates': cryptographically verifiable permissions that specify the scope, limits, actor identity, and conditions under which an AI agent is authorised to transact. An agent cannot exceed its mandate; any action outside the defined parameters requires explicit new consent from the human.

For consumers, the practical first applications will likely be familiar and low-risk: automatically purchasing the cheapest energy tariff at renewal time (within a pre-approved price range), renewing car insurance at a better rate (with human confirmation before execution), or rebalancing an investment portfolio toward a stated target allocation (with a 24-hour notification window before execution). The more ambitious vision — AI agents browsing, comparing, and purchasing across the full range of consumer spending — will take longer to implement safely and will require robust regulatory frameworks that are still being developed.

Use Case 5: Credit Analysis and Lending Automation

One of the most commercially significant applications of agentic AI in 2026 is the transformation of credit analysis — a process that has traditionally been labour-intensive, slow, and expensive, and that frequently produces outcomes that are inequitable due to reliance on historical data biased toward established borrowers.AI Magicx documents how agentic AI has transformed the process of comparable company analysis in investment banking, reducing a task that took human analysts 12 to 22 hours to 15 to 45 minutes of agent work plus 2 to 4 hours of human review — a net time saving of 65% to 80%. The same logic applies to credit risk analysis for lending. A US bank cited by McKinsey used AI agents to change the way it creates credit risk memos, achieving a 20% to 60% increase in productivity and a 30% improvement in credit turnaround time. For borrowers, faster credit analysis means faster loan decisions — reducing the time between application and funding from days to hours or minutes.

The potential for AI to consider a broader range of data than traditional credit models — including utility payment history, rent payments, and transactional cash flow patterns rather than just credit file entries — also presents an opportunity to extend credit access to underserved borrowers who have limited traditional credit histories. This is the same dynamic driving the integration of rent and utility payment data into mortgage credit scoring in the US (covered in our companion mortgage article), but applied across a wider range of lending categories.

The Risks You Need to Understand

The rapid deployment of agentic AI in financial services brings genuine risks alongside its benefits — and transparency about those risks is essential for any consumer or institution engaging with these systems.Key risks of agentic AI in money management — what you need to know

- Hallucination and incorrect outputs: Large language models, which power many agentic AI systems, are inherently non-deterministic — the same prompt can produce different outputs, and models can generate plausible but incorrect statements (hallucinations). The IMF's 2026 research note explicitly identifies this as 'a key concern in payment, compliance, and settlement contexts'. Although successive model generations show reduced hallucination rates, the risk has not been eliminated.

- Inadequate guardrails: An Infosys 2025 study found that only 2% of companies had adequate AI guardrails in place, and 95% of respondents had experienced at least one AI incident — including privacy violations (33%), systemic failures (33%), and inaccurate or harmful predictions (32%). A separate EY report noted that 30% of financial services firms studied had limited or no controls to ensure AI was free from bias.

- Data privacy risks: Agentic AI agents must access and act on large amounts of sensitive consumer financial data. The aggregation of transaction history, account balances, income, insurance, and investment data in a single system creates a significant privacy exposure if that system is breached or misused.

- Liability when AI makes mistakes: If an agentic AI agent makes an unauthorised transaction, executes a trade at the wrong price, or switches you to an inferior financial product, who is responsible? The legal and regulatory frameworks for AI agent liability in financial services are still being developed. Consumers should understand their rights before granting AI agents transactional authority.

- AI-enabled fraud and deepfakes: Neurons Lab's 2026 analysis notes that agentic AI also threatens to 'accelerate mass production of deepfakes' that can be used for synthetic identity fraud and automated large-scale scamming. The same technology that protects consumers from fraud can, in the hands of bad actors, be used to commit it more effectively.

- Over-reliance and human skill atrophy: As AI agents manage more financial decisions autonomously, there is a risk that consumers become less engaged with and less knowledgeable about their own financial position. Maintaining meaningful human oversight — even of well-performing AI systems — is both a regulatory requirement and a personal financial prudence matter.

What This Means for You as a Consumer

The shift to AI-powered and agentic money management is happening whether individual consumers actively engage with it or not. The fraud detection system protecting your bank account is already AI-driven. The credit scoring model assessing your mortgage application is being updated to include AI analysis. The recommendations your investment platform shows you are increasingly generated by machine learning models, not human advisers.What is changing in 2026 is the degree to which AI moves from background processing to front-of-stage action. The question for consumers is not whether to use AI-powered financial tools but how to use them wisely — claiming their genuine benefits while maintaining the oversight and understanding necessary to catch errors and stay in control.

The consumer who benefits most from agentic AI in financial services is not the one who hands everything over to automation and never checks in. It is the one who uses AI as a highly capable tool operating within clear parameters they have set, reviews AI-generated recommendations before acting on them for consequential decisions, and maintains enough personal financial literacy to recognise when the AI is wrong.

How to Stay in Control: Your Practical Guide

Practical steps to use agentic AI in money management safely

- Start with read-only access: Most AI money management tools offer a read-only mode that analyses your finances and makes recommendations without taking any action. This is the right starting point — benefit from the analysis before granting any transactional authority.

- Grant transactional access only with explicit limits: If you authorise an app or AI agent to take actions with your money (such as moving savings or switching bills), ensure you understand the specific permissions granted, the maximum amounts involved, and how to revoke access immediately if needed.

- Always have a notification before execution: Any legitimate AI financial agent should send you a notification before executing any consequential action — a bill switch, a savings transfer, a purchase — with sufficient time for you to cancel if you disagree. Instant execution without notification is a red flag.

- Review AI recommendations for large or complex decisions: AI tools are excellent for optimising routine decisions (cashback maximisation, savings rate comparison, minor rebalancing). For large, complex, or once-in-a-lifetime financial decisions (buying a home, retirement planning, major investments), treat AI analysis as one input among several and consider engaging a qualified human financial adviser.

- Understand what data the app can access and share: Before connecting any AI financial tool via open banking, read exactly which accounts and data it can access, what it can share with third parties, and how to disconnect. The FCA's open banking register (UK) lists all authorised providers; only use registered services.

- Monitor your accounts regularly regardless of AI protection: AI fraud detection is highly effective but not infallible. Maintaining a habit of reviewing your transaction history at least monthly ensures that any errors — whether from fraud or from an AI acting incorrectly — are caught quickly.

- Stay informed about new permissions you grant: Financial apps update their terms and permission scope over time. When any connected financial app requests new permissions or updates its terms, review what is changing before consenting.

CONCLUSION

Agentic AI in money management is not a distant future scenario — it is a 2026 reality. Forty-four per cent of finance teams are already using it, up 600% in twelve months. Major banks have deployed autonomous agents for fraud detection, credit analysis, wealth management, and customer service. The apps on your phone are already acting on your finances between your interactions with them. And the regulatory and commercial frameworks for AI agents to transact on your behalf are being built right now by Visa, Mastercard, and the FCA.The opportunity for consumers is real: better fraud protection, more personalised financial guidance, automated savings optimisation, and eventually the ability to delegate routine financial decisions to AI agents operating within clear, consent-based parameters. The risks are also real: hallucination, inadequate guardrails, data privacy exposure, and the legal grey area around AI-agent liability are all active concerns that deserve serious attention. The right response is neither uncritical adoption nor reflexive rejection. It is informed engagement — using these tools with your eyes open, maintaining meaningful oversight, and treating AI as a powerful assistant whose outputs you verify, not an infallible oracle whose decisions you delegate without thought.

Frequently Asked Questions

What is agentic AI in simple terms?Agentic AI refers to AI systems that can take autonomous, multi-step actions without waiting for human prompts. Unlike a chatbot that answers questions when you ask them, an agentic AI agent monitors its environment continuously, plans an appropriate response when something relevant happens, executes that response using the tools and permissions available to it, and learns from the outcome. In finance, this means AI that can detect fraud and block a suspicious transaction, find a better savings rate and move your money, or spot an insurance renewal approaching and initiate a comparison — all without you needing to ask it to.

Is agentic AI already managing ordinary people's money in 2026?

Yes, in several ways. Agentic fraud detection is already protecting most current account holders at major UK and US banks — the real-time SMS verification you receive when your bank detects unusual activity is the consumer-facing output of an AI agent. Apps including Plum, Cleo, and Chip already autonomously move money between your accounts based on AI-assessed cash flow predictions. Fidelity's Freya agent is a production deployment for investment customers. The 'agentic commerce' applications — AI agents that switch bills and make purchases on your behalf — are in development and early deployment rather than fully mainstream, but the infrastructure is being built now.What is open banking and how does it enable AI money management?

Open banking is a regulatory framework that requires banks to give authorised third-party providers secure access to your financial data (with your explicit consent). In the UK, the FCA implemented open banking requirements from 2018. In the US, the CFPB's Section 1033 rulemaking is expanding open banking rights. The practical effect is that AI financial apps can, with your permission, connect to all your accounts across multiple banks, see your complete transaction history and balances, and — with extended permissions — initiate payments or transfers. Open banking is the data infrastructure that makes personalised agentic AI financial management technically possible at scale.What are the main risks of letting AI manage my money?

The main risks are: AI hallucination (generating incorrect outputs, particularly problematic in payment and compliance contexts); inadequate safety guardrails (an Infosys 2025 study found only 2% of companies had adequate AI controls); data privacy exposure from aggregating sensitive financial data; unclear liability when AI makes a financial error; AI-enabled fraud (the same technology used to protect accounts can be used by bad actors to attack them); and over-reliance leading to reduced personal financial oversight. The mitigation is starting with read-only access, granting transactional permissions only with explicit limits and notification requirements, and maintaining regular personal account reviews.Should I trust AI to make financial decisions for me?

For routine, low-stakes, clearly defined decisions — moving £50 of surplus cash to a savings account, flagging a suspicious transaction, comparing two energy tariffs — AI is reliable and the benefit of automation is clear. For complex, high-stakes, once-in-a-while decisions — choosing a pension strategy, deciding whether to fix or track a mortgage, planning for retirement — AI analysis is a valuable input but should not be the sole basis for action. These decisions involve personal circumstances, values, and uncertainties that benefit from human judgment, potentially including a qualified financial adviser. The rule of thumb: the more consequential and irreversible the decision, the more human oversight it deserves.How do I know if a financial app is using agentic AI?

Look for features that take actions automatically rather than just providing information: automatic savings transfers based on cash flow analysis, proactive bill comparison with a switch option, real-time fraud blocks with autonomous temporary holds, and investment rebalancing suggestions or actions. If an app describes itself as 'proactive', 'autonomous', or mentions AI agents or agentic capabilities, it is likely using some form of agentic AI. Read the app's permissions page carefully — particularly any permissions that allow it to initiate transactions, not just read data. Check that it is authorised by the FCA (UK) at register.fca.org.uk or by relevant state and federal regulators (US) before connecting any financial accounts.References

Neurons Lab — Agentic AI in Financial Services: A Research Roundup for 2026 (April 2026) https://neurons-lab.com/article/agentic-ai-in-financial-services-2026/Citizens Bank — 2026 AI Trends in Financial Management Survey (December 2025) https://www.citizensbank.com/corporate-finance/insights/ai-trends-financial-management-2026.aspx

AI Magicx — Agentic AI in Finance: 12 Ways Banks and Fintechs Are Deploying Now (2026) https://www.aimagicx.com/blog/agentic-ai-finance-banking-deployments-2026

Azilen — Agentic AI in Financial Services: 2026 Definitive Guide https://www.azilen.com/blog/agentic-ai-in-financial-services/

IMF — How Agentic AI Will Reshape Payments (IMF Notes Volume 2026 Issue 004) https://www.elibrary.imf.org/view/journals/068/2026/004/article-A001-en.xml

Finastra — AI in Banking and Financial Services: Trends for 2026 (February 2026) https://www.finastra.com/viewpoints/articles/future-of-ai-in-financial-services-2026

BobsGuide — 5 Biggest Fintech Stories of 2025 and 5 Bold Predictions for 2026 https://www.bobsguide.com/5-biggest-fintech-news-stories-of-2025-and-5-bold-predictions-for-2026/

Keyrus — Top AI Trends Transforming Financial Services for 2026 https://keyrus.com/us/en/insights/top-ai-trends-transforming-financial-services-for-2026

FCA — Open Banking and Payment Services Authorisation Register (UK) https://register.fca.org.uk/

McKinsey — Agentic AI in Financial Services Use Cases (2025 research) https://www.mckinsey.com/industries/financial-services/our-insights

0 Comments Comments