Finance

How to Calculate Withholding and Deductions From a Paycheck

Table of Contents

- Why Your Gross Pay and Your Take-Home Pay Are Never the Same

- What Is On Your Pay Stub: The Complete Categories

- 2026 Federal Income Tax Brackets and Standard Deductions

- FICA Taxes: Social Security and Medicare in 2026

- Social Security Tax (OASDI)

- Medicare Tax (HI)

- The 2026 W-4: How It Determines Your Federal Income Tax Withholding

- The Five Steps of the 2026 W-4

- Complete Paycheck Deduction Reference: 2026 Rates and Limits

- Worked Example: Calculating Take-Home Pay on a $60,000 Salary

- Pre-Tax vs Post-Tax Deductions: Why the Distinction Matters

- When and How to Update Your W-4

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why Your Gross Pay and Your Take-Home Pay Are Never the Same

You agreed to a salary of $60,000 per year. But your first paycheck was not $2,307.69 — the number you get when you divide $60,000 by 26 biweekly pay periods. It was something considerably less, and you may have been surprised, confused, or simply uncertain about what all the line items on your pay stub mean. You are not alone. Understanding the gap between gross pay — what you earn before any deductions — and net pay — what actually lands in your bank account — is one of the most practically valuable pieces of personal finance knowledge an American worker can have.In 2026, your paycheck is subject to a series of mandatory federal deductions, possible state and local tax deductions, and voluntary pre-tax and post-tax deductions that flow from your employee benefits elections. The mandatory federal deductions include federal income tax withholding (calculated using the information on your Form W-4 and IRS Publication 15-T), Social Security tax at 6.2% of wages up to the 2026 wage base of $184,500, and Medicare tax at 1.45% of all wages with no cap. These three deductions — collectively called FICA (Federal Insurance Contributions Act) for the Social Security and Medicare components — form the foundation of what every employed American pays.

This guide explains how each deduction on a US paycheck is calculated in 2026, covering all the changes introduced by the One Big Beautiful Bill Act (OBBBA) that affect withholding calculations this year. It includes the complete 2026 federal tax bracket tables, the updated standard deductions, the new $2,200 child tax credit, a comprehensive deduction reference chart, and a fully worked numerical example that traces a $60,000 annual salary from gross pay to net pay line by line. Whether you are trying to understand your first pay stub, verify that your employer is withholding correctly, or decide how to fill out a new Form W-4, this is the complete 2026 reference.

What Is On Your Pay Stub: The Complete Categories

Every US paycheck — whether weekly, biweekly, semi-monthly, or monthly — follows the same general structure. Understanding the categories before going into the calculations makes the numbers easier to follow:- Gross Pay: Your total earnings before any deductions. For a salaried employee paid biweekly at $60,000 per year, this is $60,000 ÷ 26 = $2,307.69 per paycheck. For an hourly employee, it is hours worked multiplied by hourly rate, plus any overtime at 1.5x. Gross pay is the starting number for all withholding calculations.

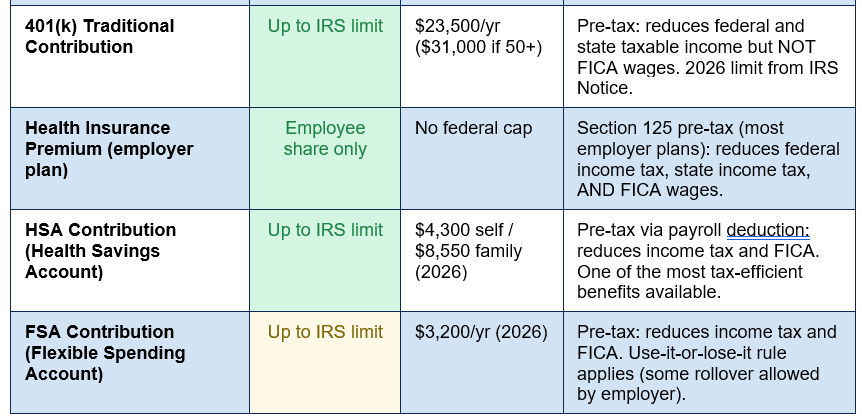

- Pre-Tax Deductions: Amounts subtracted from gross pay before federal income tax and, in many cases, before FICA taxes are calculated. These include traditional 401(k) contributions, HSA contributions, employer-sponsored health insurance premiums under Section 125, FSA contributions, and certain other benefits. Pre-tax deductions reduce your taxable income, directly lowering your tax bill.

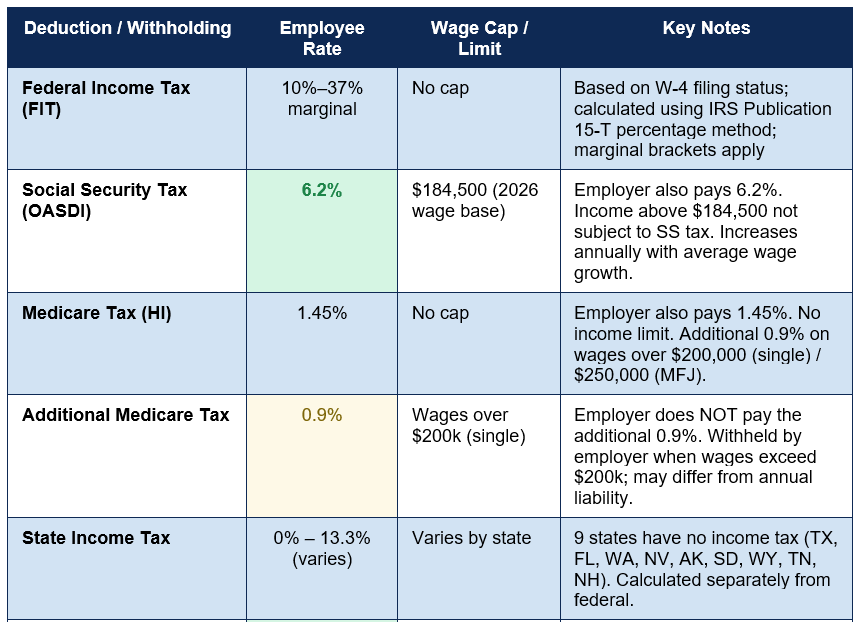

- Federal Income Tax Withholding: The amount your employer sends to the IRS on your behalf based on your W-4 filing status and the IRS Publication 15-T withholding tables. This is not a fixed rate — it is calculated based on your annualised wages and your filing status, producing a progressive result.

- FICA Taxes (Social Security + Medicare): Mandatory contributions to federal social insurance programs. Social Security is 6.2% of wages up to the 2026 wage base of $184,500. Medicare is 1.45% of all wages. Your employer matches both contributions. An Additional Medicare Tax of 0.9% applies to wages over $200,000 (single) or $250,000 (married filing jointly) — this is withheld only by the employee, not matched.

- State and Local Income Tax: Withheld based on your state of residence and, in some cases, the city or county where you work. Nine states (Texas, Florida, Washington, Nevada, Alaska, South Dakota, Wyoming, Tennessee, and New Hampshire on earned income) impose no state income tax. The remainder have rates ranging from approximately 1% to over 13%.

- Post-Tax Deductions: Amounts deducted after all taxes have been calculated — Roth 401(k) contributions, supplemental life insurance, charitable payroll deductions, and some voluntary benefits. These do not reduce your taxable income but provide other benefits.

- Net Pay: What remains after all deductions. This is the amount that transfers to your bank account or appears on your check.

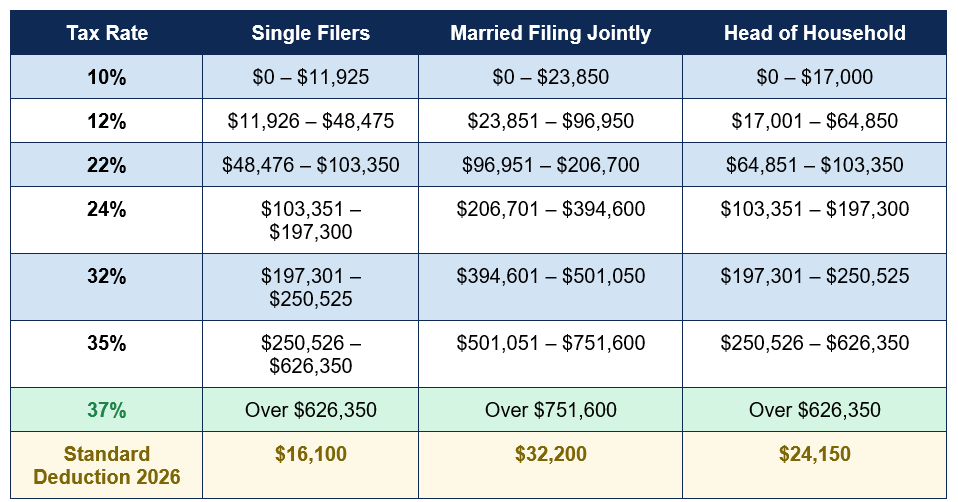

2026 Federal Income Tax Brackets and Standard Deductions

The United States uses a progressive marginal tax system — you do not pay a single flat rate on all your income. Instead, each bracket rate applies only to the income within that bracket's range. The 2026 brackets, updated for inflation by the IRS, are:

2026 OBBBA change to standard deduction: Single $16,100 / MFJ $32,200 / HoH $24,150 — plus new senior deduction — The One Big Beautiful Bill Act (OBBBA), signed in 2025, increased the standard deduction for 2026 from 2025 levels. Additionally, taxpayers aged 65 and older receive an extra $6,000 standard deduction in 2026 — a significant new benefit for senior workers and retirees with earned income (IRS Rev. Proc. 2025-32 / Tax Grids, 2026).

FICA Taxes: Social Security and Medicare in 2026

FICA taxes — the Federal Insurance Contributions Act taxes that fund Social Security and Medicare — are the most straightforward withholding calculations on your paycheck because they use fixed percentage rates rather than the bracket system of federal income tax. Unlike federal income tax, FICA is calculated on gross wages before pre-tax deductions for most voluntary benefits — your 401(k) contribution does not reduce your FICA tax bill, only your federal income tax bill. The exception is health insurance premiums and HSA/FSA contributions made under a Section 125 cafeteria plan, which do reduce FICA wages.Social Security Tax (OASDI)

The Social Security tax rate is 6.2% of covered wages, with a wage base cap that increases annually with average wage growth. For 2026, the Social Security wage base is $184,500 — up from $176,100 in 2025. This means you pay 6.2% of your first $184,500 in wages, and nothing above that threshold. Your employer matches your 6.2% contribution for a combined 12.4% going toward Social Security. A worker at exactly the wage base pays a maximum of $11,439 per year in Social Security tax in 2026.Medicare Tax (HI)

The Medicare tax rate is 1.45% of all wages, with no income cap. Your employer also pays 1.45%, for a combined rate of 2.9%. There is no upper limit — a worker earning $1 million per year pays 1.45% Medicare tax on every dollar. Additionally, the Affordable Care Act introduced an Additional Medicare Tax of 0.9% on wages above $200,000 for single filers and $250,000 for married filing jointly. This additional 0.9% is employee-only — the employer does not match it. Employers are required to withhold the additional 0.9% once a single employee's wages from that employer exceed $200,000 in a calendar year, regardless of filing status.The FICA self-employment rate: If you are self-employed, you are both the employee and the employer — meaning you pay the full 12.4% Social Security and 2.9% Medicare rates, totalling 15.3% on net self-employment income. However, the IRS allows self-employed individuals to deduct the employer-equivalent portion (7.65%) of the self-employment tax as an above-the-line deduction on their income tax return, partially offsetting the higher rate.

The 2026 W-4: How It Determines Your Federal Income Tax Withholding

Form W-4 — the Employee's Withholding Certificate — is the document you give your employer when you start a new job, and which you can update at any time when your financial situation changes. Your employer uses the information on your W-4 to look up the correct withholding amount using the IRS Publication 15-T percentage method tables. The W-4 was redesigned in 2020, eliminating the old 'allowances' system that had been in place since 1943. The 2026 W-4 continues to use the same five-step structure introduced in 2020, with several important updates from the OBBBA.The Five Steps of the 2026 W-4

- Step 1 — Personal Information and Filing Status: Enter your name, address, Social Security number, and select your filing status: Single (or Married Filing Separately), Married Filing Jointly, or Head of Household. Filing status determines which withholding table your employer uses. Married Filing Jointly has the lowest withholding rates; Single has the highest for the same income level. For most employees with one job and no other income, completing only Steps 1 and 5 is sufficient.

- Step 2 — Multiple Jobs or Working Spouse: Complete this step if you have more than one job simultaneously, or if you are married filing jointly and your spouse also works. The checkbox in Step 2(c) is the simplest approach for jobs with similar pay — it instructs your employer to use higher withholding rates to prevent under-withholding from the combined income. Alternatively, the IRS online withholding estimator or the Multiple Jobs Worksheet can calculate a more precise additional withholding amount.

- Step 3 — Claim Dependents (Child Tax Credit and Other Credits): This is where the Child Tax Credit reduces your withholding. For 2026, under the OBBBA, the Child Tax Credit is $2,200 per qualifying child under age 17 — up from $2,000 in prior years. Each other dependent (who does not qualify for the full credit) generates a $500 credit. Enter the total dollar amount — for example, two children under 17 = $4,400 to enter in Step 3. This amount is subtracted from your tentative withholding, directly reducing how much is taken from each paycheck.

- Step 4 — Other Adjustments (Optional): Three optional adjustments: 4(a) Other income not from jobs (dividends, freelance, rental income) to ensure enough is withheld; 4(b) Deductions above the standard deduction if you itemize, to reduce withholding; 4(c) Any additional flat dollar amount you want withheld per pay period. For 2026, the OBBBA's Deductions Worksheet in Step 4(b) now includes lines for qualified tips and qualified overtime exemptions, reflecting new income exclusions in the law.

- Step 5 — Sign and Date: Sign and date the form and give it to your employer's payroll or HR department. It does not go to the IRS. Your employer keeps it on file. Changes to your W-4 only affect future paychecks — they are not retroactive. If you over-withheld earlier in the year, you will receive the excess back as a refund when you file your annual return.

Complete Paycheck Deduction Reference: 2026 Rates and Limits

The table below provides a complete reference for every major deduction and withholding that may appear on a 2026 US paycheck, including the employee rate, any income caps, and key notes on how each interacts with the rest of the withholding calculation:

Worked Example: Calculating Take-Home Pay on a $60,000 Salary

The following example works through the complete paycheck calculation for a single filer earning $60,000 per year, paid biweekly (26 paychecks), with one qualifying child under 17, contributing $500/paycheck to a traditional 401(k), and paying $200/paycheck for employer-sponsored health insurance under a Section 125 plan. No state income tax is assumed for simplicity. All numbers use 2026 IRS rates.- Step 1: Gross pay per paycheck $60,000 ÷ 26 = $2,307.69

- Step 2: Pre-tax deductions – $500.00 (401k traditional) – $200.00 (health insurance Section 125) = – $700.00 total

- Step 3: Wages for federal income tax $2,307.69 – $700.00 = $1,607.69 per paycheck

- Step 4: Annualise wages for withholding table $1,607.69 × 26 = $41,800 annualised

- Step 5: Apply 2026 standard deduction (single) $41,800 – $16,100 = $25,700 taxable income (annual equivalent)

- Step 6: Apply 2026 tax brackets to $25,700 10% on first $11,925 = $1,192.50 | 12% on $13,775 ($25,700 – $11,925) = $1,653.00 | Total annual tax = $2,845.50

- Step 7: Apply Child Tax Credit (1 child × $2,200) $2,845.50 – $2,200 = $645.50 annual net federal tax

- Step 8: Federal income tax per paycheck $645.50 ÷ 26 = $24.83 per paycheck

- Step 9: Social Security tax (on gross wages, not reduced by 401k/health) $2,307.69 × 6.2% = $143.08

- Step 10: Medicare tax $2,307.69 × 1.45% = $33.46

- Step 11: Net pay (take-home) $2,307.69 – $700.00 – $24.83 – $143.08 – $33.46 = $1,406.32 net per paycheck

Annual net pay: $1,406.32 × 26 = approximately $36,564 per year. This illustrates how the combination of pre-tax benefits elections, a qualifying child tax credit, and the standard deduction significantly reduces the federal income tax burden — in this case, to less than $25 per biweekly paycheck from a $60,000 salary.

Pre-Tax vs Post-Tax Deductions: Why the Distinction Matters

The distinction between pre-tax and post-tax deductions is one of the most financially significant facts about paycheck management. Pre-tax deductions reduce your taxable income — meaning you pay less in federal income tax, and in most cases less in state income tax as well. For most voluntary benefits that your employer offers, enrolling through the payroll system under a Section 125 cafeteria plan makes the contributions pre-tax automatically.The most impactful pre-tax deductions available to most US workers in 2026 are traditional 401(k) contributions (up to $23,500 per year, or $31,000 for those aged 50 and over under the catch-up contribution rules), Health Savings Account contributions (up to $4,300 for individual coverage or $8,550 for family coverage), and employer-sponsored health insurance premiums. A worker in the 22% federal income tax bracket who contributes $23,500 to a traditional 401(k) saves $5,170 in federal income tax that year alone, plus the corresponding state income tax savings and the long-term tax-deferred investment growth.

Post-tax deductions — Roth 401(k) contributions, life insurance above employer-provided limits, and some voluntary benefit elections — do not reduce your taxable income but still reduce your take-home pay. Roth 401(k) contributions are made with after-tax dollars but grow and can be withdrawn tax-free in retirement, making them valuable in a different way than traditional 401(k) contributions. The choice between traditional and Roth depends on whether you expect to be in a higher tax bracket in retirement than you are today.

When and How to Update Your W-4

Your W-4 is not a once-in-a-lifetime form. The IRS recommends reviewing your withholding every January to account for updated tax brackets and standard deduction amounts, and updating your W-4 whenever a significant life change affects your tax situation. The key triggering events are:- Marriage or divorce — filing status changes affect withholding tables significantly.

- Birth or adoption of a child — each qualifying child under 17 generates a $2,200 Child Tax Credit in Step 3.

- Starting a second job, or your spouse starting work — the combined income may push you into a higher bracket.

- A significant raise or promotion — if your income crosses a bracket threshold, you may need additional withholding.

- Starting retirement account contributions, or increasing 401(k) elections — pre-tax contributions reduce withholding.

- Purchasing a home — mortgage interest deduction may push you toward itemising instead of taking the standard deduction.

- Receiving a large tax bill or large refund — either indicates your current withholding is misaligned with your tax liability.

The most accurate way to recalibrate your withholding is to use the IRS Tax Withholding Estimator at irs.gov/W4App. It takes approximately 25 minutes and requires your most recent pay stubs and any information about other income sources. The tool generates a completed W-4 form with the specific values to enter at each step based on your individual circumstances.

Conclusion

The gap between your gross pay and your take-home pay in 2026 is determined by a sequence of calculations that, once understood, becomes entirely predictable. Federal income tax withholding — the largest variable deduction — is calculated based on your W-4 filing status and the IRS Publication 15-T percentage method, applying the 2026 standard deduction (now $16,100 for single filers and $32,200 for married filing jointly) and the updated Child Tax Credit of $2,200 per qualifying child. FICA taxes — Social Security at 6.2% on wages up to $184,500 and Medicare at 1.45% on all wages — are straightforward fixed-rate calculations. Pre-tax deductions from 401(k) contributions, health insurance, HSA, and FSA elections reduce your taxable income further, delivering immediate tax savings that multiply the value of these benefits beyond their face cost.The 2026 W-4 continues using the five-step process introduced in 2020, with updates from the OBBBA adding new lines for qualified tips and overtime exemptions in Step 4's Deductions Worksheet and raising the Child Tax Credit. The worked example in this guide shows how a $60,000 salary can produce a federal income tax withholding of under $25 per biweekly paycheck when pre-tax deductions, the Child Tax Credit, and the standard deduction are all applied correctly — a result that surprises many workers who assume their tax bill is larger.

Understanding your paycheck withholding is not just a matter of financial literacy — it is the foundation of accurate tax planning, effective benefit election decisions, and confident W-4 completion. If your employer is withholding too much, you are giving the IRS an interest-free loan and reducing your take-home pay unnecessarily. If too little is withheld, you face a surprise tax bill and possible underpayment penalties in April. Getting it right requires understanding the calculation — and this guide provides all the numbers and tools you need to do exactly that.

Frequently Asked Questions (FAQ)

What are the 2026 federal income tax brackets?

The seven 2026 federal income tax brackets are: 10% on the first $11,925 of taxable income (single filers), 12% from $11,926 to $48,475, 22% from $48,476 to $103,350, 24% from $103,351 to $197,300, 32% from $197,301 to $250,525, 35% from $250,526 to $626,350, and 37% on income above $626,350. These are marginal rates — each rate applies only to the income within that bracket, not to all of your income. The 2026 standard deduction is $16,100 for single filers, $32,200 for married filing jointly, and $24,150 for head of household, all increased from 2025 under the One Big Beautiful Bill Act and IRS inflation adjustments.How is Social Security tax calculated on my paycheck in 2026?

Social Security tax is calculated at 6.2% of your gross wages for each pay period, up to the 2026 Social Security wage base of $184,500. This means if you earn less than $184,500 for the year, you pay 6.2% on every dollar you earn. Once your cumulative wages for the year reach $184,500, Social Security tax stops being withheld for the remainder of that year. Your employer matches your 6.2% contribution. Social Security tax is calculated on gross wages — it is not reduced by 401(k) contributions or health insurance premiums (unless the premiums are under a Section 125 cafeteria plan, in which case they do reduce FICA wages).Does my 401(k) contribution reduce my paycheck taxes?

Yes — a traditional (pre-tax) 401(k) contribution reduces your federal income tax withholding and in most states your state income tax withholding. It does NOT reduce your Social Security or Medicare tax — FICA taxes are calculated on gross wages before 401(k) deferrals for the employee contribution side. However, health insurance premiums paid through an employer's Section 125 cafeteria plan DO reduce FICA wages, giving them a broader tax advantage than the 401(k). The 2026 annual contribution limit for 401(k) accounts is $23,500, with a catch-up contribution of an additional $7,500 for workers aged 50 and older, for a total maximum of $31,000.How do I know if my employer is withholding the correct amount?

The most accurate way to check your withholding is the IRS Tax Withholding Estimator at irs.gov/W4App. It uses your actual pay stub information and W-4 details to compare your projected annual withholding against your projected annual tax liability, showing whether you are on track for a refund, a balance due, or a near-zero result. The IRS recommends using this tool in January each year and after any significant life change. If you discover you are significantly over-withheld, submit an updated W-4 to your HR department increasing your Step 3 credits or Step 4(b) deductions. If under-withheld, either update your W-4 or add an additional flat dollar amount in Step 4(c).What is the difference between federal income tax withholding and FICA?

Federal income tax withholding and FICA (Social Security and Medicare taxes) are separate withholdings that serve different purposes. Federal income tax withholding is the amount sent to the IRS in advance of your annual tax filing — it is an estimate of the income tax you will owe for the year, calculated using your W-4 information and IRS Publication 15-T tables. At the end of the year, you file a return to reconcile the amount withheld with your actual tax liability. FICA taxes, by contrast, are not a prepayment of income tax — they are separate payroll taxes that fund Social Security and Medicare programs. FICA taxes are not refunded at tax time (unless you over-pay Social Security due to multiple employers). Both appear as separate line items on your pay stub.External References & Further Reading

The following authoritative sources were used in researching this article and are recommended for further reading and calculations:1. IRS — Tax Withholding Estimator (Official IRS Tool — W4App)

https://www.irs.gov/individuals/tax-withholding-estimator

2. IRS — Publication 15-T (2026): Federal Income Tax Withholding Methods

https://www.irs.gov/publications/p15t

3. IRS — Form W-4 (2026): Employee's Withholding Certificate

https://www.irs.gov/forms-pubs/about-form-w-4

4. SmartAsset — Paycheck Calculator: Federal, State and Local Taxes

https://smartasset.com/taxes/paycheck-calculator

5. FreeFinanceCalculators — W-4 Withholding Calculator 2026 (Updated May 23, 2026)

https://freefinancecalculators.com/finance/w4-withholding-calculator

6. TaxGrids — W-4 Withholding Calculator 2026 (IRS Pub 15-T methodology)

https://taxgrids.info/w4-withholding-calculator/

7. RemoteLaws — Tax Withholding Calculator 2026 with Federal Bracket Table

https://remotelaws.com/tools/tax-withholding-calculator/

8. TurboTax — W-4 Calculator and Withholding Estimator 2026

https://turbotax.intuit.com/tax-tools/calculators/w4/

0 Comments Comments