Finance

How to Claim Child Benefit in the UK: Full Guide

Table of Contents

- Who Is Eligible to Claim Child Benefit?

- Core Eligibility Criteria

- Children Aged 16 to 19: When Child Benefit Continues

- Child Benefit Rates 2026/27: What You Will Receive

- How to Claim Child Benefit: Step by Step

- The NI Credit Benefit: Why Everyone Should Claim — Even High Earners

- The High Income Child Benefit Charge (HICBC): Full Explanation

- How Much You Repay: The Full Income Table

- How the HICBC Is Collected in 2026

- The Structural Quirk: Individual vs Household Income

- Separated Parents, Blended Families, and Special Cases

- Separated and Divorced Parents

- Blended Families

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

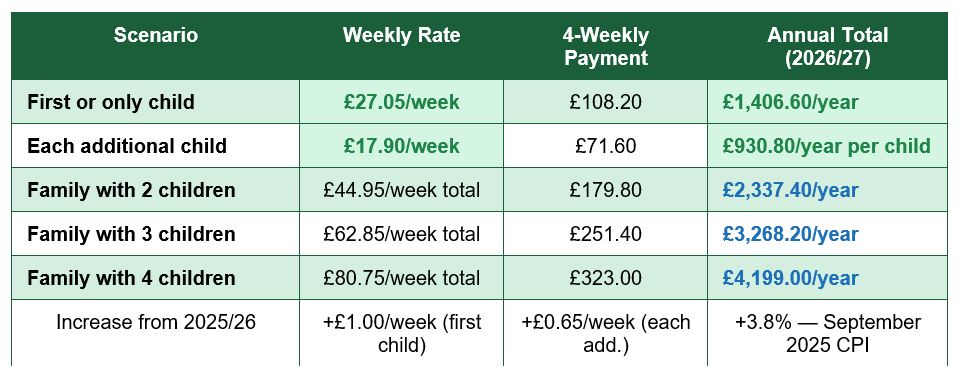

Child Benefit is one of the most accessible financial entitlements in the UK — yet HMRC estimates that more than 100,000 eligible families are not currently claiming it. From 6 April 2026, it pays £27.05 per week for a first or only child (£1,406.60 per year) and £17.90 for each additional child, following a 3.8% increase in line with the September 2025 Consumer Prices Index. Around 6.9 million UK families receive it, making it one of the most widely claimed benefits in the country.

The benefit is not means-tested at source — any eligible family can claim regardless of income, with a separate High Income Child Benefit Charge applied through the tax system for households where one earner exceeds £60,000. This crucial distinction is what leads so many eligible families to mistakenly believe they should not bother claiming. Even families where one partner earns above £80,000 and will repay the full benefit through the HICBC should still claim — because the National Insurance credits that come with an active claim are worth approximately £275 per year of future State Pension income to any non-working or low-earning parent, for every year the claim is held.

This guide explains who qualifies, the 2026/27 rates in full, the step-by-step claim process, the three-month backdating rule, the NI credit value, the HICBC explained with a worked table, the September 2025 PAYE option for managing the charge, and the retrospective NI credit route for families who never claimed from 2013 onward. If you have a qualifying child in your care and have not yet claimed — or are unsure whether to claim given your income — read this guide before deciding.

Who Is Eligible to Claim Child Benefit?

Child Benefit is available to anyone who is responsible for a qualifying child and meets the following conditions. You do not need to be the biological parent.Core Eligibility Criteria

- You are responsible for the child's day-to-day care — as a parent, step-parent, adoptive parent, grandparent, foster carer (in certain circumstances), or other guardian.

- You live in the United Kingdom or are treated as UK-resident for benefit purposes.

- The child is under 16 — or under 20 if in approved full-time education or training.

- Only one person can claim for any given child at any one time. If two people could claim, they must agree who does so.

Children Aged 16 to 19: When Child Benefit Continues

Child Benefit can continue beyond a child's 16th birthday until their 20th, provided they remain in approved full-time education or training. Qualifying programmes include A-levels, T-levels, the International Baccalaureate, NVQs up to Level 3, Scottish Highers, and certain approved traineeships. University does not qualify. Apprenticeships do not qualify. If your child leaves school at 16 without continuing in approved education, Child Benefit stops. You must notify HMRC when your child leaves approved education or training, starts paid work for more than 24 hours per week, or begins an apprenticeship.No cap on number of children: Unlike the child element of Universal Credit, Child Benefit has no two-child limit. You can claim for every qualifying child in your household, regardless of how many. A family with five children receives the first-child rate for the eldest, and the additional-child rate for each of the other four. This applies even for children for whom you cannot claim the UC child element due to the (now-abolished) UC two-child limit.

Child Benefit Rates 2026/27: What You Will Receive

Rates increased by 3.8% from 6 April 2026, applied in line with the September 2025 CPI figure. Payments are made every four weeks into a nominated bank account, usually arriving on a Monday or Tuesday. Single parents can request weekly payments.

Families missing out: 100,000+ eligible families not claiming — HMRC estimates more than 100,000 eligible families are not currently receiving Child Benefit — the primary reason cited is confusion about the HICBC leading families to incorrectly conclude they should not bother claiming at all (UK Capital News / HMRC data, April 2026).

How to Claim Child Benefit: Step by Step

The fastest method in 2026 is the HMRC app, which allows a fully digital claim with no paper form required. The paper CH2 form remains available for those who prefer it, or for adding a subsequent child to an existing claim using the CH3 form.- Claim as soon as your child arrives: Child Benefit can only be backdated by three months. Every week you delay is money permanently lost. For a first child at 2026/27 rates, a three-month delay costs approximately £351.65.

- Gather your documents: You will need your child's birth certificate or adoption certificate, your National Insurance number, and your bank account details. For online claiming, have your Government Gateway login or HMRC app credentials ready.

- Choose your claim route: HMRC app — download and navigate to Child Benefit. GOV.UK online via your Government Gateway account at gov.uk/child-benefit. Paper form CH2 — download from gov.uk, complete, and post to the Child Benefit Office. HMRC typically processes claims within five weeks.

- Decide on payments or opt-out: If one earner in your household earns above £60,000, decide whether to receive payments or opt out and keep the claim active for NI credits only. See the HICBC section below.

- Report changes promptly: Any change affecting your claim must be reported — your child leaving education, a change in household income, or a child turning 16 or 20. Report through your HMRC Personal Tax Account, the app, or by calling 0300 200 3100.

THE 3-MONTH BACKDATING RULE — ACT NOW: Child Benefit cannot be backdated beyond three months from the date HMRC receives your claim. If your child was born six months ago and you have not yet claimed, you permanently lose three months of payments — no exceptions. For a first child, that is approximately £351.65 gone forever, plus three months of NI credits toward your State Pension. Claim today.

The NI Credit Benefit: Why Everyone Should Claim — Even High Earners

The most underappreciated feature of Child Benefit is the National Insurance credits it provides to any parent or carer who is not in paid work or who earns below the Lower Earnings Limit (£6,396/year in 2026/27). The person who holds an active Child Benefit claim receives Class 3 NI credits for every week the benefit is in payment — and these credits count directly toward the 35 qualifying NI years needed for the full new State Pension of £221.20 per week.Each missing NI year reduces the State Pension by approximately £275 per year (£5.29 per week). For a parent who takes five years out of paid work to care for children and does not have an active Child Benefit claim, that represents approximately £1,375 per year less State Pension for the rest of their retirement. Over a 20-year retirement, that is £27,500 of lost pension income — from a failure to maintain a free Child Benefit claim.

This is why the claim strategy matters so much for couples: the Child Benefit claim should ordinarily be made by the lower-earning or non-working partner, since that is the partner whose NI record most needs the protection. The higher-earning partner who is subject to the HICBC pays the charge through their own tax affairs — but the NI credits flow to whoever holds the claim. Getting this decision right at the point of claiming can protect tens of thousands of pounds of lifetime pension income.

From April 2026, parents who did not claim from 2013 onward may also be able to apply retrospectively for NI credits to fill those gaps. Check gov.uk for the current eligibility criteria and application process for retrospective credits — each year recovered is worth approximately £275 per year of additional future State Pension.

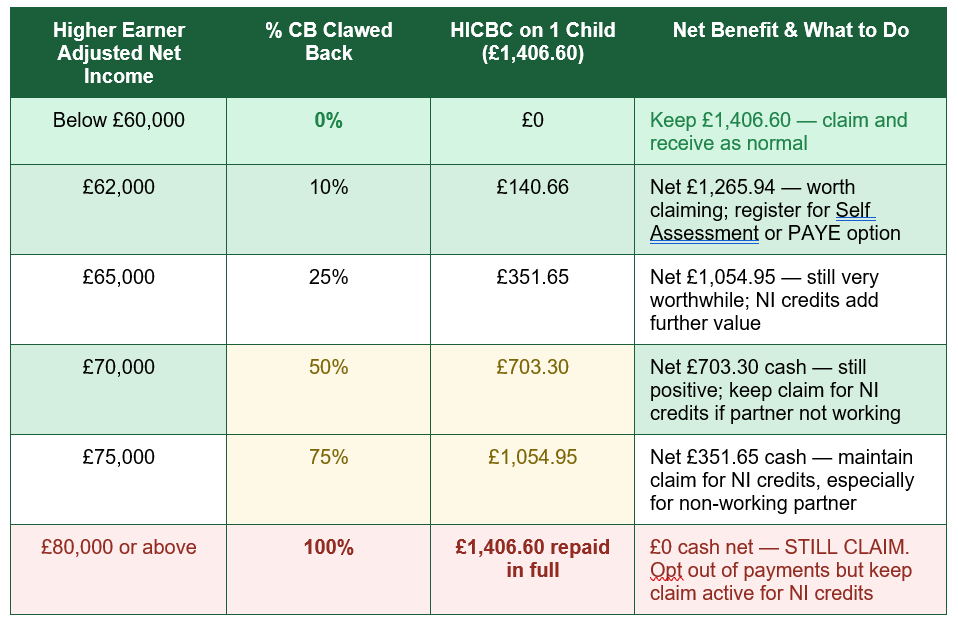

The High Income Child Benefit Charge (HICBC): Full Explanation

The HICBC was introduced in January 2013 and significantly reformed from April 2024, when the threshold rose from £50,000 to £60,000 and the full clawback point moved from £60,000 to £80,000. The charge applies to the higher earner in the household — not necessarily the Child Benefit recipient — and is calculated on adjusted net income rather than gross income. This means pension contributions that reduce adjusted net income below £60,000 can eliminate the charge entirely.

How Much You Repay: The Full Income Table

For every £200 of adjusted net income above £60,000, 1% of the annual Child Benefit received is repaid via Self Assessment or PAYE. The table below shows exactly how this plays out at different income levels for a one-child household:

HICBC in numbers: 440,000 individuals paid £525 million in HICBC in 2022/23 — the most recent year for which HMRC has published full data — and a figure that reflects only the period before the April 2024 threshold increase from £50,000 to £60,000, which removed many families from the charge (House of Commons Library / HMRC Annual Release, April 2026).

How the HICBC Is Collected in 2026

From September 2025, employed individuals whose only Self Assessment obligation is the HICBC can elect to have the charge collected through their PAYE tax code instead, removing the need to file an annual return for this purpose alone. Log into your HMRC Personal Tax Account and navigate to the HICBC section to check whether you are eligible for this option and to switch if you prefer. Those with other Self Assessment obligations — self-employment, rental income, capital gains — continue to report via their annual tax return.If the HICBC is new to you this year, register for Self Assessment by 5 October following the end of the tax year in which you first became liable. Failing to register can result in penalties, even if you subsequently pay in full. If you have missed years, HMRC typically charges interest and may reduce penalties on voluntary disclosure — seek advice from a tax adviser or Citizens Advice.

The Structural Quirk: Individual vs Household Income

The HICBC is based on individual income, not household income. Two parents each earning £59,999 — combined £119,998 — pay no HICBC at all. One parent earning £80,000 repays the full benefit. This structural unfairness has been criticised by the House of Commons Library consistently since 2013. The current government confirmed it will not reform the charge to a household-income basis. The pension contribution strategy — making contributions to reduce adjusted net income below £60,000 — remains the most effective legal response to the charge for earners near the threshold.Pension contributions and the HICBC: Adjusted net income is your gross income reduced by personal pension contributions and certain other reliefs. If you earn £65,000 and make pension contributions of £6,000 per year, your adjusted net income is approximately £59,000 — below the £60,000 HICBC threshold, eliminating the charge entirely. HMRC confirms pension contributions reduce adjusted net income for HICBC purposes. For earners between £60,000 and £80,000, calculating how much in pension contributions would bring you below the threshold is a worthwhile exercise with your accountant.

Separated Parents, Blended Families, and Special Cases

Separated and Divorced Parents

When parents separate, Child Benefit is paid to the parent the child lives with — or, if care is equally shared, to the parent HMRC determines has primary responsibility. For State Pension protection, the lower-earning or non-working parent should generally hold the claim, since NI credits flow to the claimant. The higher-earning parent who is subject to the HICBC pays it through their own tax affairs — the charge applies to the higher earner regardless of who receives the payment.Blended Families

When two families join together in one household, one parent claims Child Benefit for all children living there. The eldest child in the combined household receives the first-child rate of £27.05 per week; each other child receives £17.90 — regardless of biological parentage. If families later separate, the claiming arrangement needs to be updated with HMRC.Conclusion

Child Benefit in 2026 is a payment of £27.05 per week per first child — £1,406.60 annually — available to 6.9 million UK families, with more than 100,000 eligible families currently not claiming what they are entitled to. The three-month backdating rule means every week you delay costs money that cannot be recovered. The NI credit protection that comes with an active claim is worth approximately £275 per year of future State Pension per NI year credited — a lifetime value that makes claiming worthwhile even for families who will repay the full cash amount through the HICBC.The HICBC, reformed and raised to the £60,000-£80,000 taper from April 2024, remains complex but navigable. The new PAYE collection option from September 2025 has simplified it for many employed claimants. Pension contributions that reduce adjusted net income below £60,000 can eliminate the charge. And for the many families between £60,000 and £80,000, the combination of partial cash retention and NI credits means the claim remains financially positive even as the charge bites.

Claim immediately using the HMRC app or the gov.uk online form. Ensure the lower-earning partner holds the claim to maximise NI credit value. Check retrospective NI credit eligibility from 2013 if you never claimed during that period. And if you are near the £60,000 threshold, speak to an accountant about whether pension contributions can bring your adjusted net income below it. Every step is practical, every benefit is real, and the only wrong decision is not claiming at all.

Frequently Asked Questions (FAQ)

How much is Child Benefit in 2026/27?

From 6 April 2026, Child Benefit pays £27.05 per week for a first or only child (£1,406.60 per year) and £17.90 per week for each additional child (£930.80 per year per child). These rates represent a 3.8% increase from 2025/26 in line with the September 2025 CPI. Payments are made every four weeks into a bank account. There is no upper limit on the number of children you can claim for — unlike the child element of Universal Credit, Child Benefit has no two-child limit.How far back can Child Benefit be backdated?

Child Benefit can only be backdated by a maximum of three months from the date HMRC receives your completed claim. If your child was born six months ago and you have not yet claimed, you will receive payment from three months ago — the first three months are permanently lost, with no exceptions. At the 2026/27 first-child rate, three months of missed benefit equals approximately £351.65, plus three months of NI credits toward your State Pension.Should I claim Child Benefit if I earn over £60,000?

Yes. Even if one earner in your household earns above £80,000 and will repay the full benefit through the HICBC, you should still make an active claim. If your partner is not working or earning below the NI threshold, they receive NI credits worth approximately £275 per year of State Pension for each year the claim is active. Opt out of receiving the cash payments (via your HMRC Personal Tax Account) to avoid the Self Assessment obligation while keeping the NI credits running. For earners between £60,000 and £80,000, you keep a portion of the cash and receive NI credits — the net position is positive.What is the new PAYE option for paying the HICBC?

From September 2025, employed individuals whose only Self Assessment obligation is the HICBC can elect to have the charge collected through their PAYE tax code instead of filing an annual return. Log into your HMRC Personal Tax Account to check eligibility and switch if you prefer. This is not available to those who have other Self Assessment obligations such as self-employment or rental income. For new HICBC liabilities, the registration deadline for Self Assessment remains 5 October following the end of the relevant tax year.Can grandparents and other non-parents claim Child Benefit?

Yes. Child Benefit is available to anyone who is responsible for a qualifying child's day-to-day care — not just biological or adoptive parents. Grandparents, other relatives, foster carers in certain circumstances, and other guardians can all claim if they are the primary carer. The HICBC, if applicable, is assessed against the claimant's own income. Only one person can claim for any given child at any one time.External References

The following authoritative sources were used in researching this article:1. GOV.UK — Child Benefit: How to Claim

https://www.gov.uk/child-benefit/how-to-claim

2. GOV.UK — Child Benefit: What You'll Get (2026/27 rates)

https://www.gov.uk/child-benefit/what-youll-get

3. GOV.UK — High Income Child Benefit Charge

https://www.gov.uk/child-benefit-tax-charge

4. Which? — Child Benefit Rates and Calculator 2026/27

https://www.which.co.uk/money/tax/tax-credits-and-benefits/child-benefit-ajRMh2r8Efbr

5. House of Commons Library — The High Income Child Benefit Charge (April 2026)

https://commonslibrary.parliament.uk/research-briefings/cbp-8631/

6. Wealthvieu — UK Child Benefit 2026/27: Amounts, Eligibility and HICBC (May 2026)

https://wealthvieu.com/uk/personal-finance/child-benefit-uk/

7. WhatsMyy — Child Benefit Guide 2026/27: Rates, Eligibility and Claiming (May 2026)

https://whatsmy.co.uk/guides/child-benefit-guide/

8. Tax Rebate Services — Child Benefit Tax Trap 2026: HICBC Bites as Rates Rise

https://www.taxrebateservices.co.uk/child-benefit-tax-trap-2026/

0 Comments Comments