Credits

State of Household Credit & Borrowing: UK vs US

Table of Contents

- The UK Mortgage Market in Q1 2026: The Official Data

- Why UK Mortgage Borrowing Fell: Affordability and Pricing Volatility

- The Refinancing Surge: Half a Million Transactions and Rising

- UK Arrears and Possessions: Trending Toward Historic Lows

- The US Household Credit Picture: A More Mixed Story by Debt Type

- UK vs US: Where the Patterns Converge and Diverge

- What This Means for Households Making Credit Decisions in 2026

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Household credit markets on both sides of the Atlantic are sending a strikingly consistent signal in 2026: new mortgage borrowing is cooling, refinancing activity is surging as borrowers respond to changing rates and expiring fixed deals, and arrears — the most direct measure of household credit stress — continue trending toward some of the lowest levels seen in years. This is a genuinely unusual combination, and understanding why it is happening simultaneously in both the UK and the US offers a clearer picture of household financial health than any single headline statistic can provide on its own.

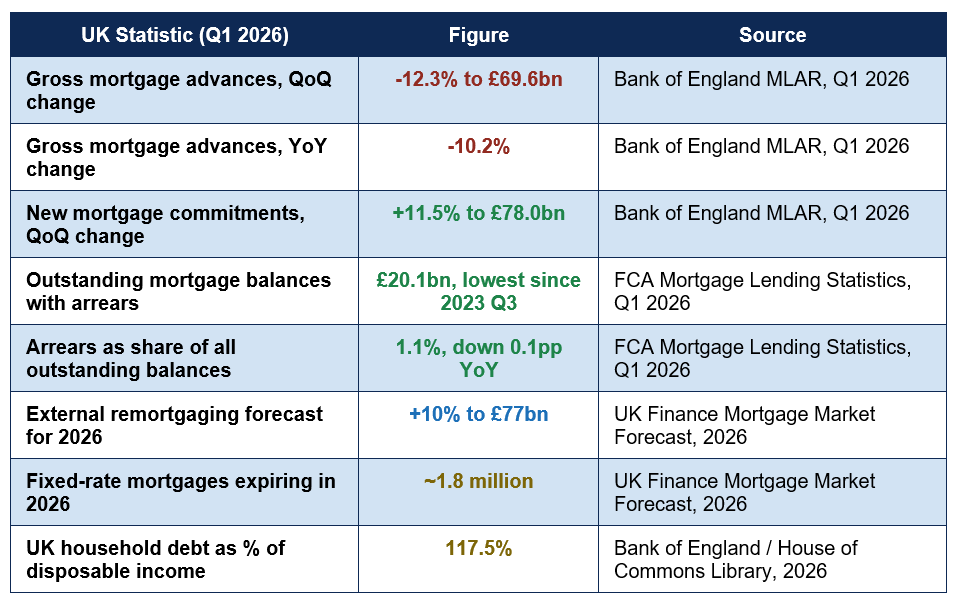

In the UK, the Bank of England's Q1 2026 Mortgage Lenders and Administrators Return shows gross mortgage advances falling 12.3% quarter-on-quarter and 10.2% year-on-year, even as new mortgage commitments — lending agreed for the months ahead — rose 11.5% over the same period, pointing to a market in transition rather than simple decline. UK Finance's official 2026 forecast separately projects a 10% rise in external remortgaging activity this year, driven by approximately 1.8 million fixed-rate mortgages reaching the end of their term. Meanwhile, outstanding mortgage balances in arrears fell to £20.1 billion in Q1 2026, the lowest level since the third quarter of 2023.

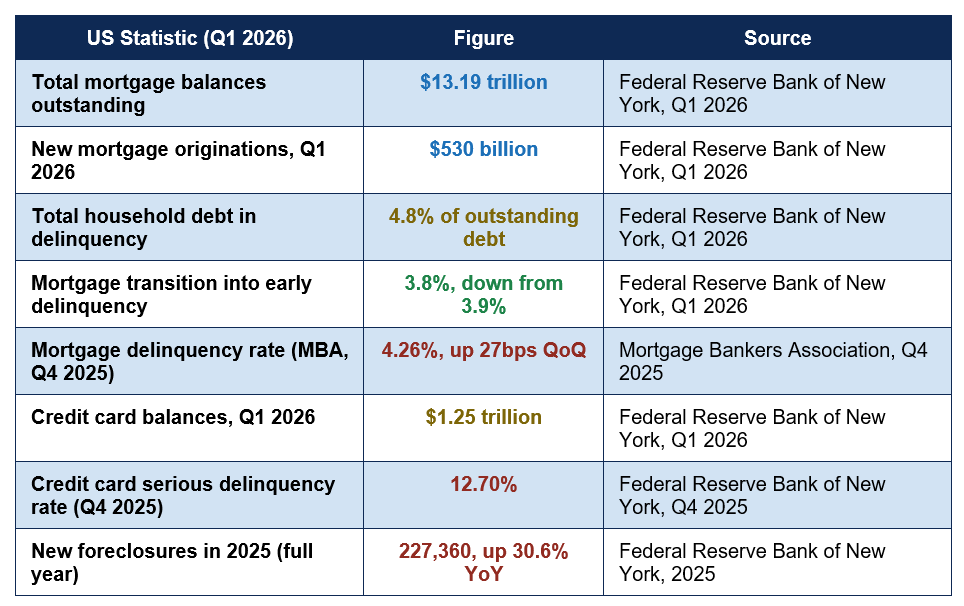

In the United States, the Federal Reserve Bank of New York's Q1 2026 Household Debt and Credit Report shows a broadly parallel pattern: mortgage origination volumes holding steady at $530 billion for the quarter, mortgage delinquency transition rates ticking down slightly, while credit card debt and serious delinquencies on unsecured credit remain considerably more elevated, revealing that not all forms of household credit are experiencing the same trajectory. This guide examines both markets in detail, comparing the data, identifying the structural forces driving each trend, and explaining what this combination of falling new lending, surging refinancing, and improving arrears actually means for households navigating credit decisions in 2026.

The UK Mortgage Market in Q1 2026: The Official Data

The table below summarises the key findings from the Bank of England and FCA's joint Q1 2026 mortgage lending statistics release, alongside UK Finance's full-year 2026 market forecast:

UK mortgage arrears trajectory: £20.1bn, lowest since 2023 Q3 — down 1.7% quarter-on-quarter and 6.3% year-on-year, with UK Finance forecasting a further 5% fall across 2026 as the market moves toward levels last seen in 2022 (Bank of England / FCA / UK Finance, 2026).

Why gross lending fell while commitments rose: The Q1 2026 fall in gross mortgage advances reflects completed transactions from applications made in late 2025, a period shaped by affordability pressures and volatile rate pricing. The rise in new commitments — lending agreed for delivery in the coming months — is a forward-looking indicator and suggests the pipeline of future lending is recovering, even as the most recently completed quarter's headline figure looks weak. This lag between commitments and completions is a normal feature of mortgage market data and explains much of the apparent contradiction in the headline numbers.

Why UK Mortgage Borrowing Fell: Affordability and Pricing Volatility

The 10.2% year-on-year decline in UK gross mortgage advances reflects two compounding pressures identified consistently across Bank of England, FCA, and UK Finance commentary. First, affordability constraints remain genuinely binding for a large share of prospective borrowers: the share of lending to borrowers with a high loan-to-income ratio reached 46.5% in late 2025, the highest level since 2022, indicating that those who are still borrowing are doing so at the very edge of what lenders consider serviceable, even as overall volumes fall.Second, mortgage pricing has remained genuinely volatile relative to the Bank of England's base rate, with the share of gross advances priced within 2 percentage points of Bank Rate falling to 94.7% in Q1 2026, the lowest proportion since 2023 — meaning a growing minority of borrowers are accessing mortgages priced at wider, more expensive spreads above the base rate. UK Finance's own market commentary describes the current environment explicitly as 'a market adjusting to structurally higher rates, tighter underwriting, and a slower housing economy' rather than either a crisis or a genuine recovery — language that captures the cautious, transitional character of the data throughout 2026.

Property transaction volumes reinforce this picture: UK Finance forecasts approximately 10,000 fewer property transactions in 2026 compared with 2025, even as overall gross mortgage lending is still expected to grow modestly across the full year, driven primarily by the refinancing surge discussed below rather than by new home-purchase activity.

The Refinancing Surge: Half a Million Transactions and Rising

The most dynamically growing segment of the UK mortgage market in 2026 is refinancing, driven by a wave of fixed-rate mortgages reaching maturity. Approximately 1.6 million fixed-rate deals expired in 2025, and UK Finance projects this will rise to around 1.8 million in 2026 — meaning a genuinely enormous share of UK mortgage holders face an active refinancing decision this year, whether they initiate it proactively or are prompted by their existing deal simply ending.External remortgaging — switching to a new lender entirely — grew 17% in 2025 to reach an estimated £71 billion, and UK Finance forecasts a further 10% rise in 2026 to approximately £77 billion. Internal Product Transfers, where a borrower stays with their existing lender but moves to a new rate, grew even more strongly, up 18% in 2025 to £256 billion, with a further 2% rise forecast for 2026. Taken together, these figures are consistent with reporting of refinancing transaction volumes surging to around half a million transactions in early 2026, up roughly a third compared with the same period in 2025 — a pace of growth that significantly outstrips the modest 4% growth forecast for overall gross mortgage lending.

Why so many borrowers are choosing internal transfers over open-market remortgaging: Industry commentary notes that many borrowers coming off ultra-low, pre-2022 fixed rates are experiencing genuine payment shocks even where headline market rates have stabilised. A meaningful share are choosing internal product transfers specifically to avoid a full affordability reassessment that an external remortgage application would require — a pragmatic response to tighter underwriting standards rather than necessarily an indication of financial distress.

UK Arrears and Possessions: Trending Toward Historic Lows

Despite the affordability pressures shaping new lending, the data on existing borrowers' ability to keep up with payments has been consistently positive throughout the data available for 2026. UK Finance's full-year data shows mortgage arrears fell to 92,100 in 2025, down from 104,800 the prior year, with a further 5% decline forecast for 2026 to approximately 87,500 — explicitly described by UK Finance as 'moving towards the historic lows seen in 2022.'The Q1 2026 FCA figures corroborate this trajectory at the balance level: arrears now account for just 1.1% of all outstanding mortgage balances, with the proportion of new arrears cases actually decreasing slightly from the previous quarter. Industry analysis attributes this resilience to a combination of factors: cost and rate pressures gradually easing from their peak, lender forbearance programmes implemented during the rate-shock period proving largely effective, and borrowers broadly adapting their budgets to the post-2022 higher-rate environment rather than falling into sustained payment difficulty.

Mortgage possessions present a more nuanced picture: the total stock of possessions in Q1 2026 fell 0.8% quarter-on-quarter, the first such decrease since 2021, but remained 20.6% higher than a year earlier, while UK Finance separately forecasts a modest further rise in possessions across 2026 to around 9,400. Industry commentary is consistent in framing this increase as a return to operational normality following an extended period of artificially suppressed activity, rather than a renewed wave of distress — possessions remain far below pre-pandemic norms even after the recent increase.

The US Household Credit Picture: A More Mixed Story by Debt Type

The US data for Q1 2026, drawn from the Federal Reserve Bank of New York's quarterly Household Debt and Credit Report, tells a broadly similar mortgage story to the UK but reveals more significant stress concentrated specifically in unsecured consumer credit:

US mortgage originations held essentially steady at $530 billion in Q1 2026, continuing a pattern of modest, stable growth rather than either a renewed boom or a sharp contraction. Mortgage delinquency transition rates actually improved slightly, with the share of mortgage balances transitioning into early delinquency falling from 3.9% to 3.8% quarter-on-quarter — though the Mortgage Bankers Association's separate survey-based measure showed the overall mortgage delinquency rate ticking up to 4.26% in Q4 2025, with the increase notably concentrated in southern states including Mississippi, Louisiana, and Maryland, illustrating that national averages can mask meaningful regional divergence.

The credit card vs mortgage stress gap in the US: 12.70% vs ~1.5% serious delinquency — credit card balances reaching serious delinquency (90+ days) hit 12.70% in Q4 2025, dramatically higher than the comparable mortgage rate, confirming that financial stress in US households is overwhelmingly concentrated in unsecured, revolving credit rather than in mortgage debt (Federal Reserve Bank of New York, Q4 2025)

UK vs US: Where the Patterns Converge and Diverge

Comparing the two markets directly reveals both a shared overarching narrative and several important structural differences worth understanding before drawing conclusions about either market in isolation.- Shared pattern — mortgage resilience amid broader caution: Both markets show mortgages remaining the most stable, best-performing category of household debt, even as overall new lending growth has slowed and affordability pressures persist for new borrowers in both countries.

- Shared pattern — refinancing as the dominant growth story: Both the UK's 1.8 million expiring fixed-rate deals and the broader US trend of borrowers responding to a changing rate environment point to refinancing and product-switching activity as the most dynamically growing segment of mortgage markets in both countries during 2026.

- Key divergence — where credit stress is concentrated: In the UK, the FCA and UK Finance data shows arrears falling consistently across nearly every measure. In the US, the New York Fed's data reveals a more divided picture: mortgage performance is broadly stable to improving, but credit card serious delinquency at 12.70% and a 30.6% year-on-year rise in new foreclosures during 2025 indicate that US household credit stress, where it exists, is concentrated specifically in unsecured debt and a meaningful (if still historically modest) uptick in mortgage-related distress in specific states and income segments.

- Key divergence — debt structure: UK household debt sits at 117.5% of disposable income, a figure dominated overwhelmingly by mortgage debt given the UK's owner-occupier-heavy housing finance system; US household debt is more diversified across mortgage ($13.19 trillion), credit card ($1.25 trillion), auto ($1.69 trillion), and student loan debt ($1.66 trillion), with the latter three categories collectively representing a meaningfully different risk profile than the UK's more mortgage-concentrated household balance sheet.

What This Means for Households Making Credit Decisions in 2026

For households in both markets navigating mortgage, refinancing, or broader credit decisions this year, several practical implications follow directly from the data:- If your fixed-rate mortgage is expiring in 2026, start the refinancing process early: With roughly 1.8 million UK fixed-rate deals maturing this year and refinancing volumes surging accordingly, lenders and brokers are managing exceptionally high transaction volumes; starting the process several months ahead of your deal's expiry helps secure the most competitive available terms before peak-period processing delays build up.

- Compare internal product transfers against full external remortgages: The strong growth in internal Product Transfers reflects a genuine trade-off worth understanding for your own situation: transfers are typically faster and avoid a fresh affordability assessment, but external remortgaging may unlock better rates or terms if your financial circumstances have improved since your original mortgage was arranged.

- Do not assume falling new lending means falling availability: The UK data shows new mortgage commitments rising even as completed gross advances fell — a reminder that headline 'lending fell' figures can reflect a lagging snapshot of past activity rather than current market conditions; checking live rates and product availability directly with lenders provides a more accurate current picture than backward-looking aggregate statistics alone.

- If you're a US borrower, prioritise unsecured debt over mortgage anxiety: Given that credit card serious delinquency rates are running many multiples higher than mortgage delinquency rates, US households carrying both mortgage and credit card debt should generally prioritise paying down high-interest revolving credit card balances, where genuine financial stress is concentrated, rather than over-indexing concern on mortgage performance, which remains comparatively strong by historical standards.

- Engage with your lender early if you are struggling, regardless of which country you're in: Both UK Finance and the Federal Reserve's reporting emphasise that early engagement with lenders, before payments are missed, consistently produces better outcomes than waiting until arrears have already accumulated; tailored forbearance and support options are typically more flexible and effective when accessed proactively.

Conclusion

The state of household credit and borrowing in 2026 reveals a genuinely consistent transatlantic story beneath the surface-level differences between UK and US data: mortgage markets in both countries are characterised by reduced new lending volumes amid persistent affordability pressure, a substantial surge in refinancing activity as borrowers respond to maturing fixed-rate deals and a changing rate environment, and — most encouragingly — mortgage arrears and delinquencies trending toward some of their lowest levels in years, even as wider economic conditions remain genuinely challenging for many households.The UK picture is particularly clear on this front: gross advances down double digits year-on-year, refinancing surging by roughly a third, and arrears at their lowest level since 2023, moving toward the historic lows last seen in 2022. The US data tells a complementary story with one important nuance: mortgage performance remains comparably resilient, but credit stress is clearly concentrated in unsecured consumer credit, where serious delinquency rates sit dramatically higher than anything visible in the mortgage market.

For households on both sides of the Atlantic, the practical takeaway is consistent: mortgage debt, historically the largest and most consequential form of household borrowing, is currently the most stable and best-managed category of credit in both markets, even amid a slower overall lending environment. The real areas requiring active household attention in 2026 are the refinancing decisions facing the millions of borrowers with maturing fixed-rate deals, and, in the US specifically, the genuinely elevated stress building in credit card and other unsecured consumer debt — a distinction worth keeping firmly in mind when assessing your own household's credit position this year.

Frequently Asked Questions (FAQ)

Why did UK mortgage lending fall even though the housing market hasn't collapsed?

The fall in gross mortgage advances reflects ongoing affordability pressures (with high loan-to-income lending reaching its highest share since 2022) and continued volatility in mortgage pricing relative to the Bank of England base rate, rather than a collapse in housing demand. Importantly, new mortgage commitments — lending agreed for the months ahead — actually rose 11.5% in the same quarter, indicating the pipeline of future lending is recovering even as the most recently completed quarter's headline figure looked weak. UK Finance describes the overall market as 'stabilising, not recovering' — a deliberately cautious characterisation of a market adjusting to a structurally different rate environment rather than either booming or collapsing.Why is mortgage refinancing surging if borrowing overall is falling?

These two trends are not contradictory — they reflect different parts of the mortgage market. The fall in gross advances primarily reflects fewer new property purchase transactions amid affordability pressure. The refinancing surge is driven by a separate, largely unrelated factor: approximately 1.8 million UK fixed-rate mortgages are reaching the end of their term in 2026, requiring those borrowers to refinance regardless of broader market conditions for new purchases. This wave of maturing deals is mechanically driving refinancing volumes up even as new purchase-related lending remains subdued.Are mortgage arrears really at historic lows, or is this misleading?

The data genuinely supports the trend, though 'historic lows' should be understood relative to the period since 2022 rather than as an all-time record. UK Finance's full-year data shows arrears falling from 104,800 to 92,100 cases between 2024 and 2025, with a further 5% decline forecast for 2026, explicitly described as 'moving towards the historic lows seen in 2022.' The FCA's Q1 2026 data corroborates this at the balance level, with arrears now representing just 1.1% of all outstanding mortgage balances. This is a genuine, multi-source-confirmed improvement, not a statistical artefact.Is US household credit stress getting worse overall?

The picture is mixed and depends heavily on which type of debt is being examined. Mortgage debt, the largest category of US household debt at $13.19 trillion, shows broadly stable to slightly improving delinquency transition rates in the Federal Reserve's Q1 2026 data. However, credit card debt shows considerably more stress, with serious delinquency rates reaching 12.70% in Q4 2025, and new foreclosures rose 30.6% year-on-year in 2025, albeit from a historically low base. The accurate characterisation is that US household credit stress in 2026 is concentrated in specific categories — unsecured credit and certain regional/income segments of the mortgage market — rather than being uniformly elevated across all household debt.Should I remortgage now or wait if my fixed-rate deal is ending soon?

This depends on your specific circumstances, including how far in advance of your deal's expiry you are, your current lender's available options, and broader rate expectations, and is not something this article can advise on directly. What the data does support is starting the process early: with roughly 1.8 million UK borrowers facing the same maturity wave in 2026, lenders and brokers are managing high volumes, and securing a rate several months ahead of your deal's expiry — most UK lenders allow this — is generally advisable regardless of which specific option (internal transfer or external remortgage) ultimately suits you best. Speaking with a regulated mortgage adviser about your specific situation is recommended for a personalised recommendation.External References

The following official and authoritative sources were used in researching this article and are recommended for further reading:1. Bank of England — Mortgage Lenders and Administrators Statistics, 2026 Q1

https://www.bankofengland.co.uk/statistics/mortgage-lenders-and-administrators/2026/2026-q1

2. Financial Conduct Authority — Commentary on Mortgage Lending Statistics Q1 2026

https://www.fca.org.uk/data/commentary-mortgage-lending-statistics-q1-2026

3. UK Finance — Mortgage Market Forecast 2026

https://www.ukfinance.org.uk/data-and-research/data/mortgage-market-forecasts

4. UK Finance — Modest Growth Forecast for Mortgage Lending in 2026

https://www.ukfinance.org.uk/news-and-insight/press-release/modest-growth-forecast-mortgage-lending-in-2026

5. Federal Reserve Bank of New York — Quarterly Report on Household Debt and Credit, Q1 2026

https://www.newyorkfed.org/microeconomics/hhdc

6. Federal Reserve Bank of New York — Household Debt Balances Rise Slightly as Delinquency Transition Rates Hold Steady (Q1 2026 Press Release)

https://www.newyorkfed.org/newsevents/news/research/2026/20260512

7. Mortgage Bankers Association — National Delinquency Survey Data (via Bankrate)

https://www.bankrate.com/mortgages/average-mortgage-debt/

8. Bank of England — Statistics: Money and Credit, Household Debt to Disposable Income

https://www.bankofengland.co.uk/statistics

0 Comments Comments