Credits

No Annual Fee Credit Cards 2026: Best UK & US Picks

The best credit card is not necessarily the one with the most impressive-sounding rewards. It is the one that costs you nothing to hold, rewards you for spending you were already going to do, and never tempts you to carry a balance. No annual fee credit cards have improved dramatically in 2026 — and for most everyday spenders in both the UK and US, they deliver better net value than premium cards with fees. This guide compares the best no-fee options, explains exactly how to choose, and shows how to use them as a financial tool rather than a debt trap.

The stability-over-status movement — the growing shift in both UK and US financial culture away from conspicuous consumption and toward genuine financial resilience — has a natural relationship with no annual fee credit cards. A card that costs you nothing to hold, earns you something back on spending you were going to do anyway, and never charges you for the privilege of being a customer is the financial equivalent of a tool that works in your interest rather than against it.

Premium credit cards with annual fees — some charging £95 to £650 per year in the UK, or $95 to $695 in the US — are marketed on the basis of status, lifestyle, and aspirational perks. The airport lounge access, the concierge service, the complimentary hotel nights. And for a specific category of frequent traveller who fully utilises every benefit, the maths can work. But for the majority of cardholders, the annual fee creates a threshold of required spend before the card becomes net positive — and many people never reach it. Research from Credit Karma notes that to offset a typical $95 annual fee through 1.5% cashback, a cardholder needs to spend over $6,333 per year just to break even, and any year they fall below that spending level, the card costs them money.

No annual fee cards eliminate this calculation entirely. There is no threshold to beat, no fee to justify, no annual review of whether you are getting your money's worth. The rewards you earn are pure gain, and the card is genuinely free to hold indefinitely — including in years when you barely use it, years when you are in debt-repayment mode and barely spending, and years when your circumstances change and a premium card would become poor value.

No annual fee credit cards offer valuable features and rewards without an upfront cost. No matter your needs, these cards won't charge you every year just to keep them open.

— CREDIT KARMA — BEST NO ANNUAL FEE CREDIT CARDS FOR MAY 2026

Consider a concrete comparison. A US cardholder who spends $15,000 per year on a card earning 2% cashback with no annual fee earns $300 in rewards. A comparable card with the same 2% cashback rate but a $95 annual fee returns only $205 net. The no-fee card wins by $95 — for zero additional effort. For the fee card to justify its cost, it would need to earn rewards at a rate meaningfully above 2% on the same spending, or provide additional benefits the cardholder actually uses and values at more than $95. Many premium cards earn 3% or more in specific categories (dining, travel, grocery), which can tilt the maths toward the fee card for high spenders in those categories. But for general-purpose spending across mixed categories, the no-fee option often wins on pure cashback arithmetic.

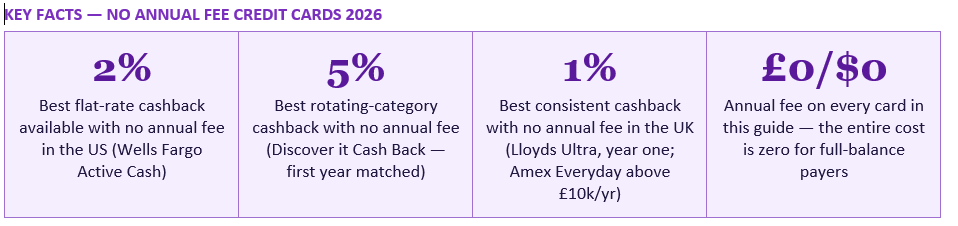

In the UK, the comparison between the American Express Platinum Cashback Everyday (no annual fee, 0.5% to 1% cashback) and the Amex Platinum Cashback (annual fee, higher rates) shows a similar dynamic. MoneySavingExpert notes that if you spend less than £10,000 per year on the card, the no-fee Everyday version typically produces better net value. At higher spend levels, the premium card's rates pull ahead — but only for those who both spend enough and reliably pay their full balance. The Lloyds Ultra Credit Card, noted by both Which? and Good Money Guide as a strong no-fee UK option, pays 1% cashback for the first year, then 0.25% thereafter, with no fees on overseas spending or ATM withdrawals if the balance is repaid in full monthly.

Discover it Cash Back is the highest-reward-potential option in year one, because Discover matches all cashback earned in the first year at the end of that year — effectively doubling the reward. On $15,000 of spending with optimised 5% category use and 1% on the remainder, year-one returns can reach $400 to $500 or more, effectively matching premium fee cards without paying any fee.

Sources: MoneySavingExpert, Which? (correct 1 May 2026), Good Money Guide, Good Money Guide. Rates and terms subject to change. Always check at provider's website before applying. American Express is not accepted by all UK merchants.

The American Express Platinum Cashback Everyday is the standout UK no-fee cashback card for higher spenders. Good Money Guide describes it as offering '5% cashback for the first five months (up to £125), then 0.5% on the first £10,000 spent and 1% above, with no annual fee.' The key limitation is that American Express is not accepted everywhere in the UK — many independent retailers and some chains do not accept it. For everyday use where Amex acceptance is reliable, it is the best cashback rate available at no annual cost. The Lloyds Ultra Credit Card is the best all-rounder for those who want consistent cashback with no fee and no overseas transaction charges, making it one of the most practical everyday cards for UK consumers who occasionally travel.

The average credit card APR in the US is approximately 20% to 22%. The average credit card interest rate in the UK is approximately 25% to 30% for standard purchase cards. If you carry a balance of £1,000 at 25% APR for a year, you pay approximately £250 in interest. No cashback or rewards programme at any rate currently available on a no annual fee card — including the 2% flat rate on the Wells Fargo Active Cash or the 5% first-year matching on the Discover it — comes anywhere near offsetting the cost of £250 in annual interest on a £1,000 balance. The maths is not close. Carrying a balance on a rewards card is, without exception, financially destructive regardless of the rewards rate.

The MoneySavingExpert guidance on cashback and reward cards is explicit: 'These cards are for paying like a debit card and clearing in full. Borrow or take cash and interest and fees will whack away the gain.' The stability-over-status framework applied to credit cards means using them as a payment mechanism on planned spending, treating them as a debit card psychologically, and setting up a direct debit or auto-pay for the full statement balance every month without exception. If you have any doubt about your ability to pay the full balance, a credit card is not the right tool for you at this moment — and there is no shame in that. The right tool for someone working through debt is a debt repayment plan, not a rewards card.

The specific ways a responsibly used no annual fee card improves your credit profile are well-documented. Regular, consistent payment history — the largest single component of both FICO scores (35%) and UK credit scores — is built up over time by making on-time payments every month. Credit utilisation — the ratio of your balance to your credit limit — is improved by keeping your reported balance low relative to your limit, which means paying in full and not maxing the card. Length of credit history is extended by holding the card open over time, which is directly supported by no annual fee cards: a card that costs nothing to hold can be kept open indefinitely, which benefits the average age of your credit accounts.

No annual fee cards are particularly valuable for credit building because the absence of a fee removes the cost of holding them during periods when you are actively reducing spending. A premium card with a £95 annual fee creates pressure to spend enough to justify it; a no-fee card creates no such pressure, allowing you to hold it for credit profile benefits even if you use it rarely.

Welcome bonuses on no-fee cards should be treated as a windfall on spending you were already planning to do — not as a reason to spend more than your budget allows. The $500 minimum spend threshold is comfortably reached by most cardholders simply by using the new card for groceries, utilities, petrol, and other planned monthly expenses. There is no need to manufacture spending to hit a bonus threshold that was going to be reached in normal use anyway.

The Discover it Cash Back first-year cashback matching offer deserves particular attention. Discover automatically matches all cashback earned in the first year — with no cap and no minimum. This means any cashback you earn, whether from the 5% rotating categories or the 1% base rate, is doubled at the end of year one. On $15,000 of annual spending with reasonable category utilisation, this can produce $350 to $500 of first-year rewards — competitive with any no-fee card on the market. After year one, the matching ends and the card reverts to its standard rates.

Several no annual fee cards explicitly eliminate foreign transaction fees, making them excellent travel companions with no additional cost. In the US, the Wells Fargo Active Cash, Capital One Quicksilver, and Discover it Cash Back all charge no foreign transaction fee. In the UK, the Lloyds Ultra Credit Card charges no fees on overseas spending or ATM withdrawals when the balance is repaid in full monthly — making it one of the best UK travel cards among no-fee options, as Good Money Guide confirms: it offers 'fee-free spending abroad, which you can earn cashback on too.'

Before taking any credit card abroad, check two things: whether it charges foreign transaction fees (3% on a £2,000 holiday adds £60 in unnecessary costs), and whether your card network (Visa, Mastercard, or Amex) is widely accepted at your destination. American Express has lower acceptance than Visa or Mastercard in many international markets, including parts of Europe and Asia. A no-fee Visa or Mastercard with no FX fees — such as the Barclaycard Rewards (Visa) or the Lloyds Ultra (Mastercard) in the UK — provides the widest acceptance with no additional travel cost.

Uswitch notes that '0% balance transfer cards with no fee can have shorter 0% periods' than their fee-charging counterparts, which is the trade-off. If you have a smaller balance that can be paid off within a shorter 0% period, a no-transfer-fee card is objectively better value — you pay no fee and clear the debt during the interest-free window. For larger balances that require a longer runway to pay off, the 3% transfer fee on a card with a longer 0% period may represent better value overall, since the fee is one-time but the interest saving accumulates over the extended period.

The balance transfer no-fee card is a tool for debt elimination, not a reason to accumulate new debt. The stability-over-status framework applied here is clear: use the 0% window to pay down existing debt as fast as possible, making consistent monthly payments that fully clear the transferred balance before the interest-free period ends. Missing this deadline and allowing the balance to roll into standard APR territory eliminates all the benefit of the transfer.

Travel benefits and airport lounge access are the clearest area where premium fee cards outperform no-fee alternatives. A card paying a $550 annual fee but including Priority Pass lounge access, comprehensive travel insurance, trip delay reimbursement, and hotel status can generate well over $1,000 in annual value for a frequent business traveller who uses all the benefits. No no-fee card provides this level of travel infrastructure. Similarly, the best dining rewards (often 4% to 5% at restaurants) and grocery rewards (4% to 6%) are typically found on fee cards rather than no-fee alternatives.

Sign-up bonuses are generally more generous on fee cards: 60,000 to 100,000 points offers on premium travel cards regularly represent $600 to $1,500 in value, compared with $200 to $300 on most no-fee cards. For cardholders who churn bonuses systematically — applying for a card, earning the bonus, and then potentially downgrading or cancelling — fee cards offer more attractive one-time value, though this strategy requires discipline and a good understanding of credit score implications.

The conclusion is not that premium cards are never worth it — it is that most everyday, non-travelling spenders who are focused on financial stability rather than rewards optimisation get better overall value from a no annual fee card that costs them nothing and earns them something. The absence of a fee means the card is never a liability, never requires a break-even calculation, and never tempts you to overspend to justify an annual charge.

The stability-over-status philosophy applied to credit cards is simple: use the card as a tool that works for you, not against you. Pay the full balance every month, automatically. Direct the cashback into savings or debt repayment rather than absorbing it back into consumption. Hold the card open for credit history benefits. Review its competitiveness annually. And never — under any circumstances — allow the pursuit of rewards to justify spending beyond your budget. A no-fee card used correctly is genuinely free money on spending you were going to do anyway. A credit card used incorrectly is one of the most expensive forms of consumer debt available. The difference between the two is entirely within your control.

MoneySavingExpert — Best Cashback and Reward Credit Cards (updated May 2026) https://www.moneysavingexpert.com/credit-cards/best-credit-card-rewards/

Which? — Best Cashback and Reward Credit Cards 2026 (correct 1 May 2026) https://www.which.co.uk/money/credit-cards-and-loans/credit-cards/best-credit-card-deals/best-cash-back-credit-cards-akfnR0Q4GK6X

Good Money Guide — Best Rewards Credit Cards Compared UK 2026 https://goodmoneyguide.com/banking/credit-cards/reward-credit-cards/

MoneySuperMarket — Best No Annual Fee Credit Cards UK May 2026 https://www.moneysupermarket.com/credit-cards/no-annual-fee/

Uswitch — Compare No Annual Fee Credit Cards UK May 2026 https://www.uswitch.com/credit-cards/no-annual-fee-credit-card/

Credit Karma — Best No Annual Fee Credit Cards for May 2026 https://www.creditkarma.com/credit-cards/no-annual-fee

Firstcard — Best Cash Back Credit Cards With No Annual Fee 2026 https://www.firstcard.app/learn/highest-cash-back-credit-card-no-annual-fee

StepChange — Free UK Debt Advice (if credit card debt has become unmanageable) https://www.stepchange.org

Consumer Financial Protection Bureau — Credit Card Basics for US Consumers https://www.consumerfinance.gov/consumer-tools/credit-cards/

TABLE OF CONTENTS

- Why No Annual Fee Cards Fit the Stability-Over-Status Philosophy

- Annual Fee vs No Annual Fee: The Maths That Matters

- The Best No Annual Fee Credit Cards in the US (2026)

- The Best No Annual Fee Credit Cards in the UK (2026)

- No Annual Fee Cards by Category: Choosing the Right One

- The One Non-Negotiable Rule: Always Pay in Full

- How No Annual Fee Cards Help Build and Protect Your Credit Score

- Welcome Bonuses and Introductory Offers: Getting the Most from Day One

- Foreign Transaction Fees: What to Check Before You Travel

- Balance Transfer No-Fee Cards: A Debt-Free Tool

- What No Annual Fee Cards Cannot Do Well

- How to Use a No Annual Fee Card as Part of a Financial Strategy

- Red Flags: How Credit Cards Lure You Into Debt

- Conclusion

- Frequently Asked Questions

- References

Why No Annual Fee Cards Fit the Stability-Over-Status Philosophy

The stability-over-status movement — the growing shift in both UK and US financial culture away from conspicuous consumption and toward genuine financial resilience — has a natural relationship with no annual fee credit cards. A card that costs you nothing to hold, earns you something back on spending you were going to do anyway, and never charges you for the privilege of being a customer is the financial equivalent of a tool that works in your interest rather than against it.Premium credit cards with annual fees — some charging £95 to £650 per year in the UK, or $95 to $695 in the US — are marketed on the basis of status, lifestyle, and aspirational perks. The airport lounge access, the concierge service, the complimentary hotel nights. And for a specific category of frequent traveller who fully utilises every benefit, the maths can work. But for the majority of cardholders, the annual fee creates a threshold of required spend before the card becomes net positive — and many people never reach it. Research from Credit Karma notes that to offset a typical $95 annual fee through 1.5% cashback, a cardholder needs to spend over $6,333 per year just to break even, and any year they fall below that spending level, the card costs them money.

No annual fee cards eliminate this calculation entirely. There is no threshold to beat, no fee to justify, no annual review of whether you are getting your money's worth. The rewards you earn are pure gain, and the card is genuinely free to hold indefinitely — including in years when you barely use it, years when you are in debt-repayment mode and barely spending, and years when your circumstances change and a premium card would become poor value.

No annual fee credit cards offer valuable features and rewards without an upfront cost. No matter your needs, these cards won't charge you every year just to keep them open.

— CREDIT KARMA — BEST NO ANNUAL FEE CREDIT CARDS FOR MAY 2026

Annual Fee vs No Annual Fee: The Maths That Matters

The decision between a card with an annual fee and one without is a straightforward calculation — but it is one that many cardholders never actually do. The question is simply whether the net value of the fee card's additional benefits (better rewards, superior perks, higher cashback rates) exceeds the annual fee.Consider a concrete comparison. A US cardholder who spends $15,000 per year on a card earning 2% cashback with no annual fee earns $300 in rewards. A comparable card with the same 2% cashback rate but a $95 annual fee returns only $205 net. The no-fee card wins by $95 — for zero additional effort. For the fee card to justify its cost, it would need to earn rewards at a rate meaningfully above 2% on the same spending, or provide additional benefits the cardholder actually uses and values at more than $95. Many premium cards earn 3% or more in specific categories (dining, travel, grocery), which can tilt the maths toward the fee card for high spenders in those categories. But for general-purpose spending across mixed categories, the no-fee option often wins on pure cashback arithmetic.

In the UK, the comparison between the American Express Platinum Cashback Everyday (no annual fee, 0.5% to 1% cashback) and the Amex Platinum Cashback (annual fee, higher rates) shows a similar dynamic. MoneySavingExpert notes that if you spend less than £10,000 per year on the card, the no-fee Everyday version typically produces better net value. At higher spend levels, the premium card's rates pull ahead — but only for those who both spend enough and reliably pay their full balance. The Lloyds Ultra Credit Card, noted by both Which? and Good Money Guide as a strong no-fee UK option, pays 1% cashback for the first year, then 0.25% thereafter, with no fees on overseas spending or ATM withdrawals if the balance is repaid in full monthly.

The Best No Annual Fee Credit Cards in the US (2026)

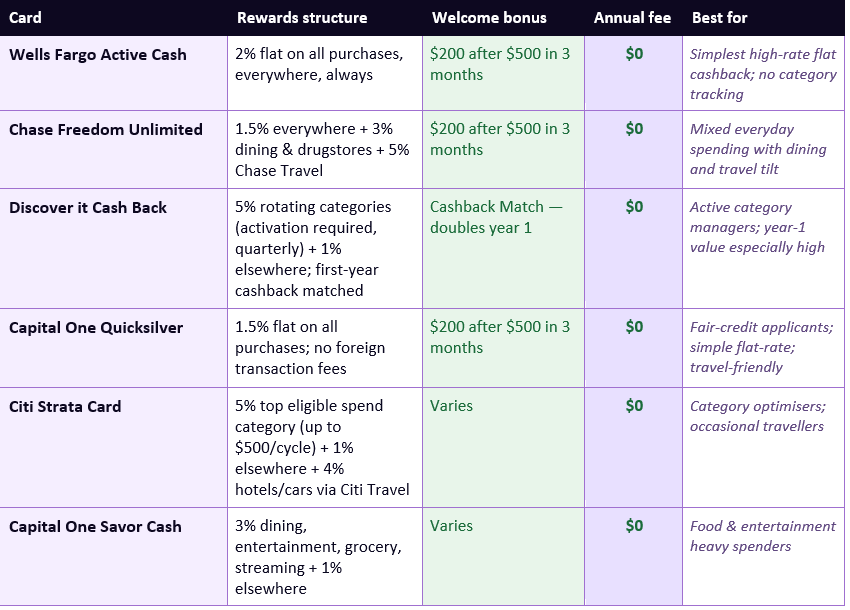

Bankrate's May 2026 best-buy analysis and Firstcard's cashback comparison identify a consistent set of top-performing no annual fee cards for US consumers. The table below covers the most widely recommended options, verified against issuer websites and current Bankrate analysis.

Sources: Bankrate (May 2026), Firstcard, Credit Karma. APRs typically 17%–27% variable — not relevant if you pay in full every month. Always check current terms at issuer website before applying.

The clear standout for pure simplicity is the Wells Fargo Active Cash at 2% flat on every purchase with no category management required. Firstcard describes it as 'beautifully simple' — earning 2 cents back on every dollar spent, no activation, no categories, no thinking. Over $20,000 of annual spending, this generates $400 in cash back at zero cost. The Chase Freedom Unlimited is the better choice for those who want the simplicity of a high base rate but also spend significantly on dining, where the 3% rate provides a meaningful boost.Discover it Cash Back is the highest-reward-potential option in year one, because Discover matches all cashback earned in the first year at the end of that year — effectively doubling the reward. On $15,000 of spending with optimised 5% category use and 1% on the remainder, year-one returns can reach $400 to $500 or more, effectively matching premium fee cards without paying any fee.

The Best No Annual Fee Credit Cards in the UK (2026)

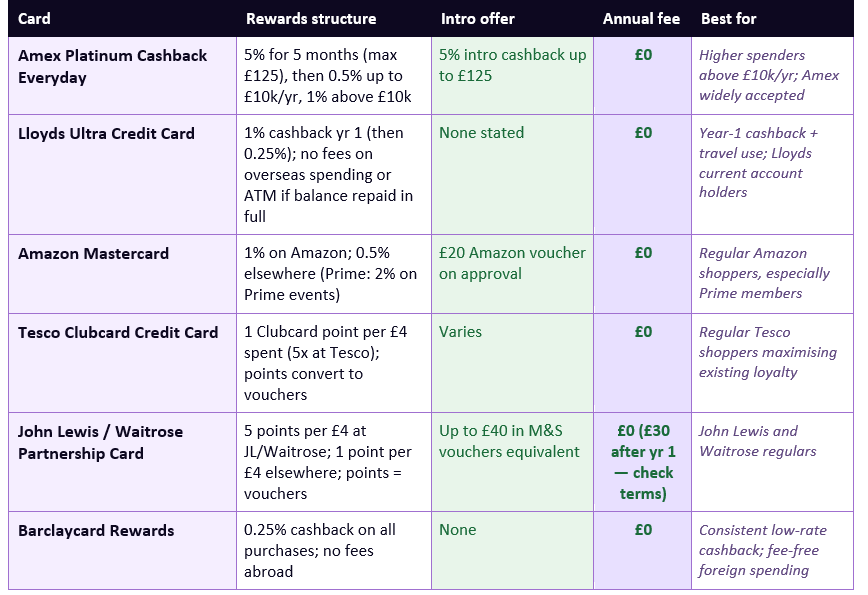

The UK no annual fee rewards landscape is narrower than the US market — partly because UK interchange fees are capped at much lower levels under regulation, reducing the pool of money available for rewards programmes. Nonetheless, several strong no-fee options exist for UK consumers.Sources: MoneySavingExpert, Which? (correct 1 May 2026), Good Money Guide, Good Money Guide. Rates and terms subject to change. Always check at provider's website before applying. American Express is not accepted by all UK merchants.

The American Express Platinum Cashback Everyday is the standout UK no-fee cashback card for higher spenders. Good Money Guide describes it as offering '5% cashback for the first five months (up to £125), then 0.5% on the first £10,000 spent and 1% above, with no annual fee.' The key limitation is that American Express is not accepted everywhere in the UK — many independent retailers and some chains do not accept it. For everyday use where Amex acceptance is reliable, it is the best cashback rate available at no annual cost. The Lloyds Ultra Credit Card is the best all-rounder for those who want consistent cashback with no fee and no overseas transaction charges, making it one of the most practical everyday cards for UK consumers who occasionally travel.

No Annual Fee Cards by Category: Choosing the Right One

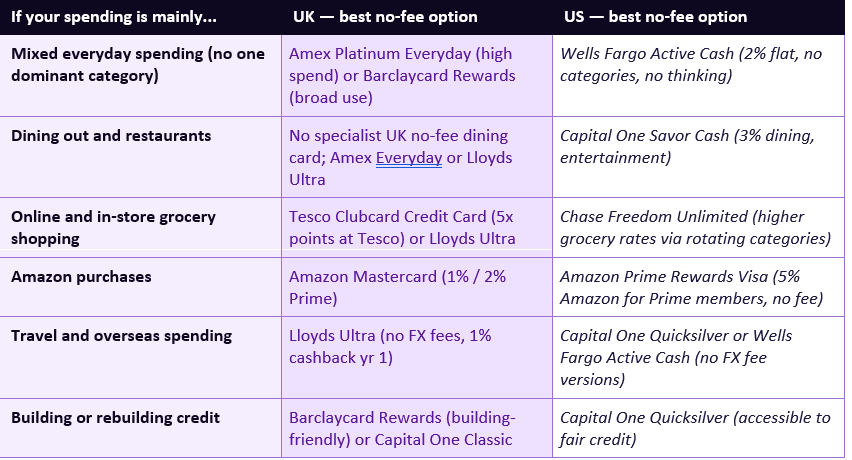

The right no annual fee card depends on how and where you spend. The following framework matches the most common UK and US spending profiles to the appropriate no-fee card type.The One Non-Negotiable Rule: Always Pay in Full

Every benefit described in this guide — every percentage point of cashback, every welcome bonus, every reward point — exists only for cardholders who pay their full statement balance every single month. This is the single most important rule in personal credit card management, and it is stated here in absolute terms because there are no exceptions to it.The average credit card APR in the US is approximately 20% to 22%. The average credit card interest rate in the UK is approximately 25% to 30% for standard purchase cards. If you carry a balance of £1,000 at 25% APR for a year, you pay approximately £250 in interest. No cashback or rewards programme at any rate currently available on a no annual fee card — including the 2% flat rate on the Wells Fargo Active Cash or the 5% first-year matching on the Discover it — comes anywhere near offsetting the cost of £250 in annual interest on a £1,000 balance. The maths is not close. Carrying a balance on a rewards card is, without exception, financially destructive regardless of the rewards rate.

The MoneySavingExpert guidance on cashback and reward cards is explicit: 'These cards are for paying like a debit card and clearing in full. Borrow or take cash and interest and fees will whack away the gain.' The stability-over-status framework applied to credit cards means using them as a payment mechanism on planned spending, treating them as a debit card psychologically, and setting up a direct debit or auto-pay for the full statement balance every month without exception. If you have any doubt about your ability to pay the full balance, a credit card is not the right tool for you at this moment — and there is no shame in that. The right tool for someone working through debt is a debt repayment plan, not a rewards card.

How No Annual Fee Cards Help Build and Protect Your Credit Score

A credit card held responsibly — used regularly for small purchases and paid in full every month — is one of the most effective tools available for building and maintaining a strong credit score. This is equally true in the UK (where Experian, Equifax, and TransUnion are the major credit reference agencies) and in the US (where FICO scores and VantageScores are the primary metrics used by lenders).The specific ways a responsibly used no annual fee card improves your credit profile are well-documented. Regular, consistent payment history — the largest single component of both FICO scores (35%) and UK credit scores — is built up over time by making on-time payments every month. Credit utilisation — the ratio of your balance to your credit limit — is improved by keeping your reported balance low relative to your limit, which means paying in full and not maxing the card. Length of credit history is extended by holding the card open over time, which is directly supported by no annual fee cards: a card that costs nothing to hold can be kept open indefinitely, which benefits the average age of your credit accounts.

No annual fee cards are particularly valuable for credit building because the absence of a fee removes the cost of holding them during periods when you are actively reducing spending. A premium card with a £95 annual fee creates pressure to spend enough to justify it; a no-fee card creates no such pressure, allowing you to hold it for credit profile benefits even if you use it rarely.

Welcome Bonuses and Introductory Offers: Getting the Most from Day One

Many no annual fee cards offer a welcome bonus for new cardholders who meet a minimum spend within the first 60 to 90 days. In the US, the most common structure is $200 cash back after spending $500 in the first three months — a 40% effective return on those first $500 of spending. The Wells Fargo Active Cash, Chase Freedom Unlimited, and Capital One Quicksilver all offer this structure. In the UK, the Amex Platinum Cashback Everyday offers 5% cashback for the first five months up to a maximum of £125.Welcome bonuses on no-fee cards should be treated as a windfall on spending you were already planning to do — not as a reason to spend more than your budget allows. The $500 minimum spend threshold is comfortably reached by most cardholders simply by using the new card for groceries, utilities, petrol, and other planned monthly expenses. There is no need to manufacture spending to hit a bonus threshold that was going to be reached in normal use anyway.

The Discover it Cash Back first-year cashback matching offer deserves particular attention. Discover automatically matches all cashback earned in the first year — with no cap and no minimum. This means any cashback you earn, whether from the 5% rotating categories or the 1% base rate, is doubled at the end of year one. On $15,000 of annual spending with reasonable category utilisation, this can produce $350 to $500 of first-year rewards — competitive with any no-fee card on the market. After year one, the matching ends and the card reverts to its standard rates.

Foreign Transaction Fees: What to Check Before You Travel

One of the most overlooked costs on credit cards is the foreign transaction fee — typically 2% to 3% of each international purchase — charged by many cards when you use them abroad or make purchases in a foreign currency. For frequent travellers, this fee can significantly erode the value of a rewards programme and render an otherwise attractive card poor value for travel use.Several no annual fee cards explicitly eliminate foreign transaction fees, making them excellent travel companions with no additional cost. In the US, the Wells Fargo Active Cash, Capital One Quicksilver, and Discover it Cash Back all charge no foreign transaction fee. In the UK, the Lloyds Ultra Credit Card charges no fees on overseas spending or ATM withdrawals when the balance is repaid in full monthly — making it one of the best UK travel cards among no-fee options, as Good Money Guide confirms: it offers 'fee-free spending abroad, which you can earn cashback on too.'

Before taking any credit card abroad, check two things: whether it charges foreign transaction fees (3% on a £2,000 holiday adds £60 in unnecessary costs), and whether your card network (Visa, Mastercard, or Amex) is widely accepted at your destination. American Express has lower acceptance than Visa or Mastercard in many international markets, including parts of Europe and Asia. A no-fee Visa or Mastercard with no FX fees — such as the Barclaycard Rewards (Visa) or the Lloyds Ultra (Mastercard) in the UK — provides the widest acceptance with no additional travel cost.

Balance Transfer No-Fee Cards: A Debt-Free Tool

A balance transfer credit card allows you to move existing credit card debt from a high-interest card to a new card with a lower or zero introductory interest rate, giving you a window to pay down the debt without ongoing interest accumulation. In the UK, many 0% balance transfer cards charge a balance transfer fee of 2% to 3.5% — but several cards offer a 0% transfer period with no transfer fee, making them a genuinely cost-free debt management tool.Uswitch notes that '0% balance transfer cards with no fee can have shorter 0% periods' than their fee-charging counterparts, which is the trade-off. If you have a smaller balance that can be paid off within a shorter 0% period, a no-transfer-fee card is objectively better value — you pay no fee and clear the debt during the interest-free window. For larger balances that require a longer runway to pay off, the 3% transfer fee on a card with a longer 0% period may represent better value overall, since the fee is one-time but the interest saving accumulates over the extended period.

The balance transfer no-fee card is a tool for debt elimination, not a reason to accumulate new debt. The stability-over-status framework applied here is clear: use the 0% window to pay down existing debt as fast as possible, making consistent monthly payments that fully clear the transferred balance before the interest-free period ends. Missing this deadline and allowing the balance to roll into standard APR territory eliminates all the benefit of the transfer.

What No Annual Fee Cards Cannot Do Well

Intellectual honesty requires acknowledging what no annual fee cards do less well than premium cards, and where the annual fee is genuinely worth paying for certain users.Travel benefits and airport lounge access are the clearest area where premium fee cards outperform no-fee alternatives. A card paying a $550 annual fee but including Priority Pass lounge access, comprehensive travel insurance, trip delay reimbursement, and hotel status can generate well over $1,000 in annual value for a frequent business traveller who uses all the benefits. No no-fee card provides this level of travel infrastructure. Similarly, the best dining rewards (often 4% to 5% at restaurants) and grocery rewards (4% to 6%) are typically found on fee cards rather than no-fee alternatives.

Sign-up bonuses are generally more generous on fee cards: 60,000 to 100,000 points offers on premium travel cards regularly represent $600 to $1,500 in value, compared with $200 to $300 on most no-fee cards. For cardholders who churn bonuses systematically — applying for a card, earning the bonus, and then potentially downgrading or cancelling — fee cards offer more attractive one-time value, though this strategy requires discipline and a good understanding of credit score implications.

The conclusion is not that premium cards are never worth it — it is that most everyday, non-travelling spenders who are focused on financial stability rather than rewards optimisation get better overall value from a no annual fee card that costs them nothing and earns them something. The absence of a fee means the card is never a liability, never requires a break-even calculation, and never tempts you to overspend to justify an annual charge.

How to Use a No Annual Fee Card as Part of a Financial Strategy

A no annual fee credit card used correctly is one component of a broader financial strategy — not a destination in itself. Here is how it fits with the other elements of the stability-over-status financial framework.The five-step framework for using a no-fee card as a financial tool

- Use the card only for planned spending: Before using a credit card for any purchase, ask whether you have already budgeted for this expenditure. Credit cards should replace cash or debit card spending on planned items — groceries, utilities, fuel, subscriptions — never enable spending beyond your means. The budgeting frameworks in our companion budgeting article apply equally whether you pay by cash, debit, or credit card.

- Set up automatic full balance repayment: Set up a direct debit (UK) or AutoPay (US) to pay the full statement balance automatically on the due date every month. This eliminates any risk of forgetting to pay, never allows interest to accrue, and requires no ongoing mental management of payment timing.

- Direct cashback or rewards into savings or debt repayment: Every time cashback is credited to your account, redirect it explicitly — to your emergency fund, your debt repayment pot, or your high-yield savings account. Cashback that is simply absorbed into general spending produces no net financial benefit. Cashback that is systematically redirected to savings compounds over time.

- Keep the card open long-term: A no-fee card held open for years — even if rarely used — contributes positively to your credit history length and the average age of your accounts. Closing a card unnecessarily reduces your credit history length and can temporarily lower your credit score. A card that costs nothing to hold should be kept open unless there is a specific reason to close it.

- Review your reward rate annually: Card issuers change their rewards programmes, add fees, or reduce rates over time. Once per year, check that your card's rewards rate is still competitive with the best available no-fee alternatives. If a better no-fee card exists for your spending pattern, consider switching — and use the eligibility checker on MoneySuperMarket (UK) or Credit Karma (US) to check approval likelihood before applying.

Red Flags: How Credit Cards Lure You Into Debt

Credit card companies are highly sophisticated marketers, and their products are designed to make spending feel frictionless and rewarding. Understanding their tactics is essential for using them safely.Six credit card traps — and how to avoid them

- Minimum payment psychology: The statement always shows you the minimum payment required — often just 1% to 2% of the balance plus interest. Paying only the minimum on a £2,000 balance at 25% APR takes over 30 years to clear and costs more in interest than the original spending. Always pay the full statement balance, never the minimum.

- 0% purchase period expiry: Many cards offer an introductory 0% APR on purchases for 12 to 18 months. After the period ends, the standard APR (often 20%+ in the US, 25%+ in the UK) applies to any remaining balance. If you use a 0% purchase period, ensure the balance is fully cleared before it expires — set a calendar reminder.

- Reward-chasing overspending: The prospect of earning 3% on dining or 5% on groceries can subtly encourage spending in those categories beyond what you would otherwise spend. Rewards are only net-positive if the underlying spending was already budgeted. Spending £50 more on dining to earn £1.50 in cashback is a net loss of £48.50.

- Cash advance fees: Using a credit card to withdraw cash triggers immediate interest at a higher rate (typically 27%+ APR in the UK, with no interest-free period), plus a cash advance fee of 2% to 3%. Never use a credit card for cash withdrawals. Ever. The Lloyds Ultra card is an exception for abroad ATM use if the balance is repaid in full monthly, but this should be treated as a specific travel tool, not a general rule.

- Balance transfer fee misalignment: If you use a balance transfer card to consolidate debt, ensure the transfer fee (if any) plus the timeline for repayment produces a better outcome than your current interest rate. A 3% transfer fee on a £5,000 balance costs £150 upfront — but saves significantly on interest if you can clear the balance within the 0% period.

- Credit limit increases: Card issuers regularly offer unsolicited credit limit increases. A higher limit can improve your credit utilisation ratio (positive for credit scores) but also represents a larger potential debt if spending increases proportionally. Never treat a credit limit increase as additional spending power — treat it as additional headroom that you should not use.

CONCLUSION

The best credit card for most people is not the one with the most impressive marketing, the most aspirational branding, or the highest headline rewards rate. It is the one that costs nothing to hold, earns you a reliable return on spending you were already going to do, and never creates a financial obligation that works against you. In 2026, no annual fee credit cards in both the UK and US are better than they have ever been — 2% flat cashback with no fee in the US, 1% with no overseas fees in the UK, and introductory bonuses that can reach $300 to $500 in year one without paying a penny.The stability-over-status philosophy applied to credit cards is simple: use the card as a tool that works for you, not against you. Pay the full balance every month, automatically. Direct the cashback into savings or debt repayment rather than absorbing it back into consumption. Hold the card open for credit history benefits. Review its competitiveness annually. And never — under any circumstances — allow the pursuit of rewards to justify spending beyond your budget. A no-fee card used correctly is genuinely free money on spending you were going to do anyway. A credit card used incorrectly is one of the most expensive forms of consumer debt available. The difference between the two is entirely within your control.

Frequently Asked Questions

What is the best no annual fee cashback credit card in the US in 2026?

For flat-rate simplicity, the Wells Fargo Active Cash card is widely rated the best in 2026, earning 2% cashback on all purchases with no categories to manage, no annual fee, and a $200 welcome bonus after $500 of spending in the first three months. For those willing to manage categories, the Discover it Cash Back earns 5% on rotating quarterly categories (up to the quarterly maximum after activation) plus 1% on everything else, with all first-year cashback doubled by Discover at year end. For mixed spending with a dining tilt, the Chase Freedom Unlimited (1.5% base + 3% dining/drugstores + 5% Chase Travel) is among the strongest no-fee options, according to Bankrate's May 2026 analysis.What is the best no annual fee cashback credit card in the UK in 2026?

For higher spenders who use Amex regularly, the American Express Platinum Cashback Everyday offers the best ongoing cashback with no annual fee — 5% for the first five months (up to £125), then 0.5% on spending up to £10,000 per year and 1% above that threshold. Good Money Guide confirms there is no annual fee and it earns 1% on spend above £10,000 annually. For all-around flexibility with no fees abroad, the Lloyds Ultra Credit Card (1% cashback in year one, then 0.25%, no overseas fees, no ATM fees if balance repaid in full) is identified by both Which? and Good Money Guide as a strong no-fee all-rounder. Note that Amex is not accepted by all UK merchants.Is it worth getting a no annual fee card if I already have a premium fee card?

Yes, in several scenarios. First, as a backup card accepted by merchants who do not take American Express or your primary card network. Second, as a dedicated travel card if your primary card charges foreign transaction fees. Third, to maintain a second credit account for credit history diversification — holding two well-managed cards typically benefits credit scores more than one. Fourth, as a household spend card if your spending does not reach the threshold where a premium card's fee is justified, while using a no-fee card maximises net rewards without any break-even calculation required.Can I get a no annual fee credit card with bad credit?

Yes, though the options are more limited and the rewards rates are generally lower. Capital One's range includes no annual fee cards accessible to fair-credit and even some poor-credit applicants in the US. In the UK, Barclaycard Initial and Capital One Classic are no-fee credit-building cards with low credit limits designed for those with limited or poor credit histories. The primary goal for these applicants should be building credit through responsible use and on-time payments — the modest rewards are secondary. Secured credit cards (where you provide a deposit as collateral) are also available with no annual fees and serve as a credit-building tool.How do I avoid paying interest on a cashback credit card?

Set up automatic full balance repayment — a direct debit (UK) or AutoPay (US) for the full statement balance, scheduled to pay on the due date every month. This is the single most important action for safe credit card use. As long as the full balance is paid by the statement due date every month, no interest is ever charged on purchase transactions. Set up the auto-payment immediately after receiving your card, before making any purchases. Never reduce the auto-pay amount to the minimum payment — always set it to the full balance. Keep a buffer in your current account to ensure the direct debit always clears.What is the difference between cashback and rewards points on no annual fee cards?

Cashback cards pay you a direct percentage of spending in cash — typically as a statement credit, bank deposit, or cheque. The value is always transparent: 2% means 2 pence or 2 cents back per pound or dollar spent, with no conversion required. Rewards points are less transparent: their value depends on how you redeem them, and the same points programme can yield 0.5p per point or 1.5p per point depending on redemption method. Cashback cards are generally better for most people because the value is simple, guaranteed, and requires no active management. Points programmes can deliver higher value for those willing to research and optimise redemptions — particularly for flights and hotel stays — but also carry the risk of points devaluation, expiry, or complexity that reduces effective returns for casual users.References

Bankrate — Best No Annual Fee Credit Cards for May 2026 https://www.bankrate.com/credit-cards/rewards/best-no-annual-fee-cards/MoneySavingExpert — Best Cashback and Reward Credit Cards (updated May 2026) https://www.moneysavingexpert.com/credit-cards/best-credit-card-rewards/

Which? — Best Cashback and Reward Credit Cards 2026 (correct 1 May 2026) https://www.which.co.uk/money/credit-cards-and-loans/credit-cards/best-credit-card-deals/best-cash-back-credit-cards-akfnR0Q4GK6X

Good Money Guide — Best Rewards Credit Cards Compared UK 2026 https://goodmoneyguide.com/banking/credit-cards/reward-credit-cards/

MoneySuperMarket — Best No Annual Fee Credit Cards UK May 2026 https://www.moneysupermarket.com/credit-cards/no-annual-fee/

Uswitch — Compare No Annual Fee Credit Cards UK May 2026 https://www.uswitch.com/credit-cards/no-annual-fee-credit-card/

Credit Karma — Best No Annual Fee Credit Cards for May 2026 https://www.creditkarma.com/credit-cards/no-annual-fee

Firstcard — Best Cash Back Credit Cards With No Annual Fee 2026 https://www.firstcard.app/learn/highest-cash-back-credit-card-no-annual-fee

StepChange — Free UK Debt Advice (if credit card debt has become unmanageable) https://www.stepchange.org

Consumer Financial Protection Bureau — Credit Card Basics for US Consumers https://www.consumerfinance.gov/consumer-tools/credit-cards/

0 Comments Comments