Credits

Pay Off Credit Card Debt Before Investing: Here's Why

Table of Contents

- Introduction

- The Scale of the Credit Card Debt Crisis: Key Statistics

- The Mathematics: Why Debt Repayment Always Wins Against High-Interest Debt

- Chart: Credit Card Debt vs. Investing — The Numbers Do Not Lie

- The Hidden Cost of Minimum Payments: A Wealth Destruction Machine

- The Psychological Dimension: Stress, Behaviour, and Financial Decision-Making

- The Practical Framework: How to Sequence Debt Repayment and Investing

- Step 1: Build a Starter Emergency Fund First

- Step 2: Capture Any Employer 401(k) Match

- Step 3: Eliminate All High-Interest Debt Using the Avalanche or Snowball Method

- Step 4: Build a Full Emergency Fund

- Step 5: Begin Structured, Consistent Investing

- When Investing Alongside Debt Repayment Can Make Sense

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Introduction

One of the most common and consequential financial dilemmas facing working adults today is deceptively simple to state and surprisingly difficult to navigate: should I pay off my credit card debt, or start investing first? In an era of rising interest rates, stock market enthusiasm, and social media financial gurus promoting investment returns, the question feels more pressing than ever.The answer, for the vast majority of people carrying high-interest credit card debt, is unambiguous: pay off the debt first. Not because investing is unimportant — it is essential to long-term wealth building — but because the mathematics of high-interest debt creates a guaranteed negative return that no investment strategy can reliably overcome. Understanding why this is true, backed by current statistics and real numbers, is one of the most valuable financial insights you can acquire.

This blog post makes the case clearly and comprehensively. It examines the current scale of the credit card debt crisis in the US and UK, demonstrates through actual numbers why carrying credit card debt while investing is mathematically self-defeating, explores the psychological dimensions of the decision, and provides a practical, step-by-step framework for eliminating debt and then building an investment portfolio that compounds wealth over time. By the end, the reasoning will be not just intellectually clear but actionable — which is ultimately what financial education should always produce.

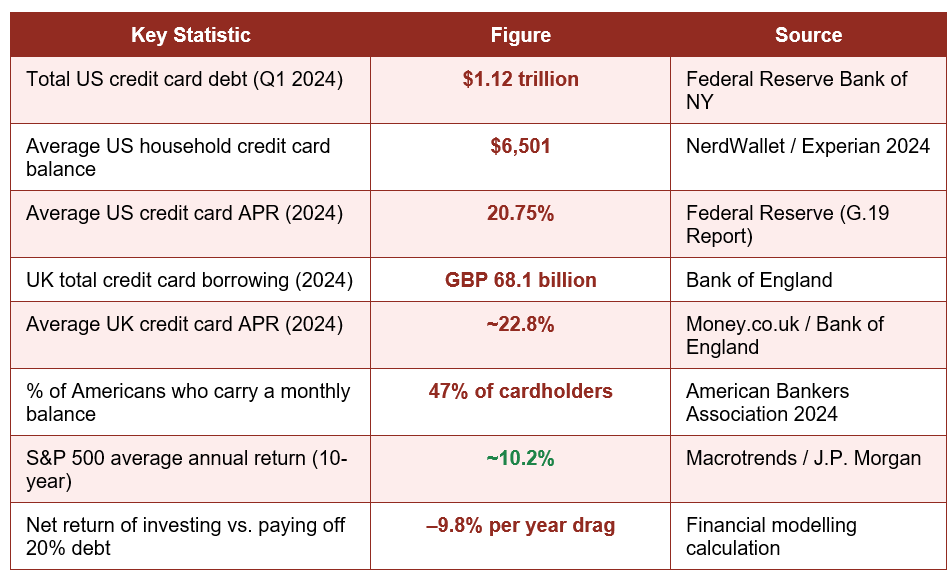

The Scale of the Credit Card Debt Crisis: Key Statistics

Before examining the debt-versus-investing question, it is worth understanding the scale of the problem that credit card debt represents. The numbers are staggering — and they illuminate why this question matters for tens of millions of households.

These statistics reveal two crucial realities. First, credit card debt in both the US and UK is carried at extraordinarily high interest rates — averaging over 20% APR — that vastly exceed any realistic investment return available to retail investors. Second, nearly half of all credit cardholders in the US are paying interest on a monthly balance, meaning the compounding cost of that debt is working against them continuously. The interaction of high-rate debt and slow debt repayment is one of the most effective wealth-destruction mechanisms in personal finance.

At 20.75% APR, a $6,501 average US credit card balance costs approximately $1,349 in interest in the first year alone — whether or not the cardholder makes a single investment.

The Mathematics: Why Debt Repayment Always Wins Against High-Interest Debt

The core argument for paying off credit card debt before investing rests on an arithmetically irrefutable foundation: the guaranteed return of eliminating a 20% APR debt exceeds the expected return of any diversified, appropriately-risk-managed investment portfolio.Consider the comparison through a concrete scenario. You have $5,000 available. Option A is to invest it in an S&P 500 index fund, which has historically returned approximately 10.2% per year. Option B is to use it to pay off $5,000 of credit card debt at 20% APR. Over five years:

- Option A (Invest): $5,000 at 10.2% annual return grows to approximately $8,157 — a gain of $3,157.

- Option B (Pay Off Debt): The $5,000 debt at 20% APR, if paid via minimum payments, would have cost you $3,289 in interest over five years. Paying it off eliminates this guaranteed loss — an effective guaranteed return of 20%.

- Net advantage of Option B over Option A: approximately $6,446 over five years — more than doubling the outcome of investing.

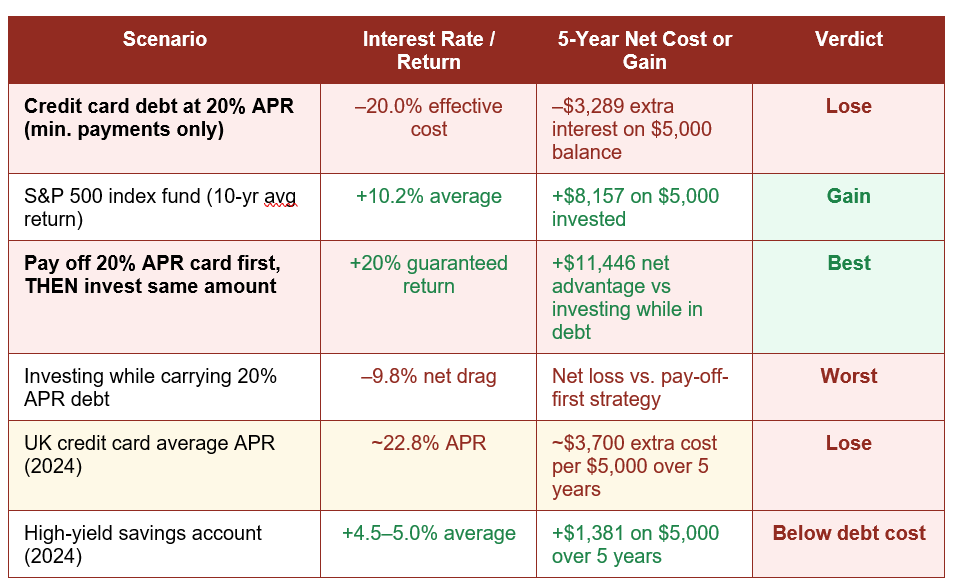

The chart below illustrates this comparison across multiple scenarios, including the additional drag created by attempting to invest while carrying high-rate debt simultaneously:

Chart: Credit Card Debt vs. Investing — The Numbers Do Not Lie

Key insight: Paying off a 20% APR credit card delivers a guaranteed 20% return — risk-free. The S&P 500's best 10-year average return is approximately 10.2%. There is no legal, ethical investment vehicle accessible to retail investors that reliably outperforms the guaranteed return of eliminating 20%+ interest-rate debt.

Critics of the debt-first approach sometimes argue that historical stock market returns can exceed credit card rates during periods of extraordinary market performance. This is occasionally true in the short term — but it requires accepting stock market risk to compete with a guaranteed cost. The relevant comparison is not peak returns versus APR; it is risk-adjusted expected returns versus guaranteed cost. On that basis, paying off high-interest debt wins every time.The Hidden Cost of Minimum Payments: A Wealth Destruction Machine

One of the most insidious features of credit card debt is the minimum payment structure, which is designed to maximise the interest paid by the cardholder while creating the illusion of responsible management. Making only the minimum payment on a credit card balance is one of the most expensive financial behaviours a person can engage in.

This is the mathematical reality that minimum payments obscure. The credit card statement shows a modest, manageable monthly number. The total cost over the repayment timeline reveals the true price: paying back more than twice the original debt in total. Every month that minimum payments are chosen over aggressive repayment extends this timeline and compounds the total interest cost.

For context, if the same $6,501 were invested in an S&P 500 index fund for 19 years at an average 10.2% annual return, it would grow to approximately $41,200. But this mathematical victory is hollow if the $6,501 card balance is simultaneously costing $9,400 in interest over the same period. The net position of investing while making minimum payments on credit card debt is dramatically negative compared to eliminating the debt first.

The Psychological Dimension: Stress, Behaviour, and Financial Decision-Making

The case for paying off debt first is not purely mathematical. Behavioural finance research consistently demonstrates that financial stress impairs decision-making in ways that create additional financial harm — and credit card debt is one of the most potent sources of financial stress in modern life.A 2023 study published in the journal Psychological Science found that financial anxiety — defined as persistent worry about debt and financial obligations — reduces cognitive bandwidth in ways that impair planning, impulse control, and long-term financial decision-making. In practical terms, people carrying significant credit card debt make worse financial decisions than the same individuals would make when debt-free, creating a vicious cycle in which debt causes stress, stress causes poor decisions, and poor decisions perpetuate debt.

There is also the matter of financial momentum. Research from behavioural economists including Dr. Wendy De La Rosa at the Wharton School shows that the psychological experience of paying off debt — particularly the milestone of closing an account or reaching a zero balance — generates positive motivation and financial confidence that correlates with better long-term financial behaviours. This is the core insight behind the debt snowball method: the psychological benefit of early wins is a real, measurable factor in debt repayment success.

Carrying credit card debt while investing can also create a false sense of financial progress. A brokerage account showing gains provides visible, positive feedback — even as the interest clock on credit card debt silently erodes more wealth than the portfolio is creating. This cognitive mismatch is one reason many financially intelligent people make the mistake of investing while in high-interest debt.

The Practical Framework: How to Sequence Debt Repayment and Investing

Understanding why debt repayment should come first is necessary but not sufficient. The equally important question is how to do it — and in what precise sequence to transition from debt elimination to wealth building. The following framework is the most widely endorsed sequence in professional financial planning:Step 1: Build a Starter Emergency Fund First

Before making extra debt payments, build a minimum emergency fund of $500 to $1,000 (or one month of essential expenses). This prevents a single unexpected expense from forcing you to add new credit card charges while paying off existing ones — which is the most common cause of debt repayment failure.Step 2: Capture Any Employer 401(k) Match

If your employer offers a 401(k) match — for example, matching 100% of contributions up to 4% of your salary — contribute enough to capture the full match before making extra debt payments. An employer match is a guaranteed 100% return on contribution, which exceeds even the highest credit card APR. This is the one exception to the debt-first rule. In the UK, the equivalent consideration applies to auto-enrolled pension contributions where employer matching is available.Step 3: Eliminate All High-Interest Debt Using the Avalanche or Snowball Method

Direct all available surplus income — after essential expenses, minimum debt payments, and the 401(k) match contribution — toward aggressive credit card debt repayment. Choose your method:- Avalanche method (mathematically optimal): Pay the minimum on all cards and direct all extra payments to the card with the highest APR first. Once it is paid off, redirect that payment to the next highest APR card. This minimises total interest paid.

- Snowball method (psychologically powerful): Pay the minimum on all cards and direct all extra payments to the card with the lowest balance first. Early wins build momentum and maintain motivation, which research shows improves completion rates — particularly for those who have struggled with debt repayment in the past.

.

Step 4: Build a Full Emergency Fund

Once high-interest debt is eliminated, expand your emergency fund to three to six months of total living expenses in a high-yield savings account. This removes the financial vulnerability that causes many debt-free people to reaccumulate credit card balances during periods of unexpected expense.Step 5: Begin Structured, Consistent Investing

Now — and only now — redirect the full surplus income previously used for debt repayment into an investment portfolio. The payment you were making against your credit card balance becomes your monthly investment contribution. Because your baseline expenses and lifestyle have not changed, this transition requires no additional income — simply a redirection of existing cash flow from a negative-return obligation to a positive-return asset.For most individual investors, a globally diversified portfolio of low-cost index funds — held in tax-advantaged accounts such as a 401(k), IRA, or ISA — provides the optimal combination of expected return, tax efficiency, and simplicity. Automate contributions monthly to remove the temptation of timing the market or deferring investment decisions.

When Investing Alongside Debt Repayment Can Make Sense

While the general rule is unambiguous for high-interest credit card debt, there are specific circumstances where investing concurrently with debt repayment is financially rational:- Low-interest debt (below 6-7% APR): Personal loans, car finance, or student loans at rates well below historical market returns present a genuine trade-off. At 4% APR, investing in the stock market has a positive expected return net of the debt cost, and many financial advisors recommend a split approach — aggressive debt repayment and modest investing simultaneously.

- Employer pension matching (as described above): Always capture the full employer match regardless of debt, as this provides an immediate guaranteed return exceeding any debt rate.

- Time-limited investment opportunities: An employee stock purchase plan (ESPP) offering shares at a 15% discount, or a defined-contribution pension scheme with limited enrollment windows, may justify temporary parallel investment even with existing debt.

The key principle is that the higher the interest rate on your debt, the more decisively you should prioritise debt repayment over investing. Credit card APRs in the 18-25% range are so significantly above expected investment returns that no rational case for simultaneous investing can be made on purely financial grounds.

Conclusion

The debate between paying off credit card debt and investing is not genuinely close — at least not at the interest rates that credit cards currently charge. With average APRs exceeding 20% in the US and UK, credit card debt represents a guaranteed negative return that no investment vehicle can reliably beat on a risk-adjusted basis. The mathematics, the statistics, and the collective wisdom of financial planners all point in the same direction: eliminate high-interest debt first, then invest aggressively and consistently.The framework is straightforward: capture any employer pension match, build a starter emergency fund, then direct every available dollar or pound at credit card debt using the avalanche method. Once debt is eliminated, expand your emergency fund and redirect the full debt repayment amount into a diversified investment portfolio. The investment compounding that begins on a debt-free foundation is categorically more powerful than the fractional gains possible while simultaneously paying 20% APR.

The most important insight is not which option is mathematically superior — that is clear. The most important insight is that the transition from indebted to invested is a one-time sequence that, once completed, creates a permanently better financial trajectory. Every month of delay in beginning that sequence costs money in interest that could have been working for you in a portfolio. Start the debt payoff plan this month, not next. The difference between starting today and starting in six months, compounded over a lifetime, is more significant than most people imagine.

Frequently Asked Questions (FAQ)

What if my credit card APR is lower than average — say 12%? Should I still pay it off first?

At 12% APR, the argument for debt-first is less absolute but still generally valid. The S&P 500's long-run average return of approximately 10.2% means that after taxes on investment gains, the net return from investing is likely below the guaranteed 12% return of debt elimination. Most financial advisors apply a threshold of around 6-7% APR as the point below which investing alongside debt becomes genuinely competitive. Above that threshold — which includes all standard credit cards — debt payoff first is the superior strategy.Is the avalanche or snowball method better for paying off credit card debt?

Mathematically, the avalanche method (highest APR first) is always superior — it minimises total interest paid across all debts. However, research by behavioural economists shows that the snowball method (smallest balance first) produces higher completion rates among people who have previously struggled with debt repayment, because the psychological reward of eliminating entire debts provides motivation that sustains long-term behaviour. The best method is the one you will actually complete. If you have strong financial discipline, use the avalanche. If you need motivational momentum, use the snowball.Should I close my credit card accounts after paying them off?

Generally, no. Closing credit card accounts reduces your total available credit, which increases your credit utilisation ratio and can lower your credit score. Keeping paid-off accounts open with a zero balance — and ideally making a small, automatic monthly purchase that is paid in full each month — maintains your credit history and available credit limit, both of which support a strong credit score. The exception is a card with a high annual fee that provides no ongoing value, which is worth closing if the fee outweighs any credit score impact.What is the fastest way to pay off credit card debt?

The fastest approaches, in order of typical impact, are: first, a balance transfer to a 0% APR promotional card (available with good credit) that allows all payments to attack principal rather than interest; second, a debt consolidation loan at a lower rate than your current cards; third, aggressively increasing your monthly payment above the minimum using the avalanche method; and fourth, generating additional income through a side job or asset sale to make lump-sum payments. Combining a balance transfer (to eliminate interest) with aggressive extra payments (to accelerate principal reduction) is often the most powerful combination available to someone with good credit.What is the right order of financial priorities?

The widely endorsed sequence recommended by financial planners is: (1) build a starter emergency fund of $500 to $1,000; (2) contribute enough to your employer's pension or 401(k) to capture the full employer match; (3) pay off all high-interest debt (above 6-7% APR) as aggressively as possible; (4) build a full emergency fund of three to six months of expenses; (5) maximise ISA / IRA contributions in tax-advantaged accounts; (6) maximise all other available retirement account contributions; (7) invest any remaining surplus in a taxable brokerage account. This sequence optimises guaranteed returns, tax efficiency, and risk management simultaneously.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Federal Reserve Bank of New York — Household Debt and Credit Report Q1 2024

https://www.newyorkfed.org/microeconomics/hhdc

2. Federal Reserve — Consumer Credit G.19 Report (Average Credit Card APR)

https://www.federalreserve.gov/releases/g19/current/

3. Bank of England — Consumer Credit Statistics (UK)

https://www.bankofengland.co.uk/statistics/money-and-credit

4. NerdWallet — Average Credit Card Interest Rates 2024

https://www.nerdwallet.com/blog/average-credit-card-interest-rate/

5. Investopedia — Debt Avalanche vs Debt Snowball: Which Is Better?

https://www.investopedia.com/articles/personal-finance/080716/debt-avalanche-vs-debt-snowball-which-best-you.asp

6. J.P. Morgan Asset Management — Long-Term Capital Market Assumptions

https://am.jpmorgan.com/us/en/asset-management/adv/insights/portfolio-insights/ltcma/

7. Consumer Financial Protection Bureau (CFPB) — Understanding Credit Card Interest

https://www.consumerfinance.gov/consumer-tools/credit-cards/

8. MoneySavingExpert (UK) — Balance Transfer Credit Cards Guide

https://www.moneysavingexpert.com/credit-cards/balance-transfer-credit-cards/

0 Comments Comments