Credits

Should You Help Your Partner With His / Her Debt or Not?

Table of Contents

- The Debt Landscape: How Common Is Partner Debt?

- The Legal Reality: Are You Responsible for Your Partner's Debts?

- In the United Kingdom

- In the United States

- Helping vs Stepping Back: The Key Considerations

- The Emotional Dynamics of Debt in Relationships

- Practical Frameworks for Couples Navigating Partner Debt

- Framework 1: The Full Partnership Approach

- Framework 2: The Supported Independence Approach

- Framework 3: The Structured Loan Approach

- Protecting Yourself While Supporting Your Partner

- When Stepping Back Is the Right Choice

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Money is one of the most significant sources of tension in relationships. Studies consistently show that financial disagreements are among the leading predictors of relationship breakdown, and one of the most charged scenarios couples face is when one partner carries significant debt into the relationship — or accumulates it along the way.

The question of whether to help a spouse or partner clear their debts is not a simple one. It touches on love and loyalty, but also on legal liability, financial security, personal accountability, and long-term shared goals. There is no single right answer — what matters is that couples make an informed, deliberate decision rather than drifting into a situation by default.

This guide explores the financial, legal, and emotional dimensions of the question from every angle. Whether you are newly in a relationship with someone who has debt, recently married and discovering the full picture for the first time, or long-term partners navigating a debt crisis together, the framework and strategies here will help you make the decision that is right for your relationship and your financial future.

The Debt Landscape: How Common Is Partner Debt?

Debt in relationships is far more common than many people realise when they first fall in love. In the UK, the average adult holds approximately £34,000 in personal debt (excluding mortgage debt), according to figures from the Money Charity. In the United States, the average American carries around $21,800 in personal debt, with student loans, credit cards, car finance, and personal loans being the most common forms.When two people form a household, their individual debt pictures merge into a shared financial reality — even when the debt legally remains separate. A partner making large monthly debt repayments has less available income for rent, savings, joint expenses, and shared goals. Their debt effectively becomes your shared constraint, even if your name is nowhere on the paperwork.

Understanding the full scope of a partner's debt — the types, amounts, interest rates, and repayment timelines — is an essential first step before any decision about involvement can be made. Financial transparency is not a luxury in relationships; it is a necessity for making good decisions together.

The Legal Reality: Are You Responsible for Your Partner's Debts?

The most important thing to understand is what you are — and are not — legally obligated to do. The answer depends significantly on where you live, your marital status, and how accounts are structured.In the United Kingdom

In England, Wales, and Northern Ireland, you are generally not legally responsible for debts your partner incurred before the relationship or in their name alone — even if you are married. Marriage does not automatically make you liable for pre-existing individual debts. However, joint accounts and jointly taken financial products do create shared legal liability. If you are a guarantor on a loan, you are responsible. If you have a joint credit card or joint mortgage, you are equally liable.Scotland operates under the Family Law (Scotland) Act 1985, which has different provisions regarding matrimonial property, so legal advice specific to Scottish law is advisable in complex situations.

In the United States

US law varies by state. In the nine community property states — including California, Texas, and Arizona — debts incurred during a marriage may be considered joint debts regardless of whose name they are in. In common law states (the majority), spouses are generally only responsible for debts they signed for directly. Understanding which regime applies to you is critical, particularly if divorce or separation is ever a possibility.For unmarried couples in both countries, the legal position is generally cleaner: you are not responsible for your partner's individual debts unless you have co-signed or taken out joint credit. The decision to help is therefore a voluntary one, not a legal obligation.

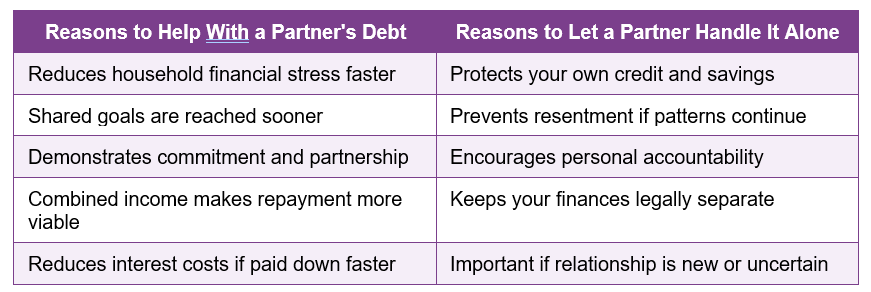

Helping vs Stepping Back: The Key Considerations

Before deciding on an approach, it helps to see both sides clearly. The table below outlines the main reasons couples choose each path:

Neither column is inherently right or wrong. The best decision depends on the nature of the debt, the length and strength of the relationship, the financial capacity of both partners, and — crucially — the attitude and behaviour of the partner who owes the money.

The Emotional Dynamics of Debt in Relationships

Debt carries a significant psychological burden. Research published in the Journal of Family and Economic Issues found that financial stress is one of the strongest predictors of relationship dissatisfaction, and that debt-related conflict tends to escalate over time when not addressed openly. The partner in debt often experiences shame, anxiety, and defensiveness, while the debt-free partner may feel frustration, fear, or a sense of unfairness.These emotional dynamics can make the money conversation extremely difficult — but they are also precisely why having it matters so much. Avoiding the topic does not make the debt disappear; it simply allows resentment and misaligned expectations to build silently.

Financial therapists increasingly recognise a pattern sometimes called financial enabling, where a partner repeatedly bails out the other from debt without addressing the underlying spending behaviours or financial habits. This may feel loving in the short term but can perpetuate a cycle of debt accumulation and dependency that ultimately harms both partners and the relationship itself.

The most productive framework is one in which both partners approach the debt as a shared problem to be solved together — not a source of blame, nor something to be completely ignored. This means honest conversation, agreed boundaries, a clear plan, and mutual accountability.

Practical Frameworks for Couples Navigating Partner Debt

Framework 1: The Full Partnership Approach

In this model, both partners treat all debt — regardless of whose name it is in — as a shared household liability to be eliminated together. Both incomes are pooled, a joint debt repayment plan is created, and extra payments are directed at high-interest debts using a method such as the avalanche (highest interest first) or snowball (smallest balance first) approach.This model is most appropriate for long-established couples or married partners with shared financial goals, strong mutual trust, and a partner who has demonstrated a genuine commitment to changing the habits that created the debt. It can dramatically accelerate debt elimination but requires complete financial transparency and careful management to avoid resentment.

Framework 2: The Supported Independence Approach

Here, the debt-free partner does not directly contribute funds but provides practical support: helping to create a repayment budget, researching balance transfer options, attending financial counselling sessions, encouraging consistent repayments, and adjusting shared household expenses to free up more of the indebted partner's income for debt repayment.This model preserves the legal and financial separation of individual debts while ensuring the indebted partner is not navigating the process alone. It is well suited to newer relationships, situations where trust is still being established, or where the debt-free partner has legitimate concerns about financial vulnerability.

Framework 3: The Structured Loan Approach

Some couples choose a middle path: the debt-free partner lends money to the indebted partner at no or low interest to pay off high-interest debt, with a written repayment agreement between them. This eliminates expensive credit card or payday loan interest and creates a structured, accountable repayment plan within the relationship.If this approach is used, a simple written agreement — even an informal one — specifying the amount, repayment schedule, and what happens in the event of separation is strongly recommended. This protects both parties and prevents the loan from becoming a source of conflict if circumstances change.

Protecting Yourself While Supporting Your Partner

If you choose to help your partner with their debt, doing so wisely means protecting your own financial position at the same time. Consider the following safeguards:- Maintain your own emergency fund — Never deplete your own savings entirely to pay another person's debt. A minimum of three months of living expenses in your own account provides essential protection.

- Keep your credit separate — Avoid taking out joint credit products specifically to consolidate your partner's debts. If the relationship ends, joint debt becomes your legal liability.

- Set clear, agreed conditions — If you are contributing money to debt repayment, agree upfront on what this means for shared finances, what the repayment plan looks like, and what happens if debt accumulates again.

- Review your partner's spending habits — Paying off debt that is immediately replaced by new spending is not a solution. Both partners need to agree on the spending behaviour changes that accompany the repayment plan.

- Consider professional advice — A fee-free debt charity such as StepChange (UK) or the National Foundation for Credit Counselling (US) can provide a neutral, expert perspective on the best repayment strategy without the emotional charge of a couple's conversation.

When Stepping Back Is the Right Choice

There are circumstances in which stepping back from a partner's debt — even with the best intentions — is the wiser decision. These include:- The debt is the result of gambling, addiction, or compulsive spending behaviours that have not been addressed. Without treating the underlying issue, debt repayment assistance simply enables continuation of harmful patterns.

- Your partner is not transparent about the full extent of their debts, resists discussing finances, or minimises the seriousness of the situation.

- Helping would require you to take on debt yourself, deplete your retirement savings, or compromise your own financial security.

- The relationship is relatively new and insufficient time has passed to assess whether the financial patterns and values are compatible for a long-term partnership.

- Your partner shows no initiative to address the debt themselves and expects you to solve the problem without personal effort or accountability.

Stepping back in these circumstances is not a failure of love or commitment. It is a recognition that financial health — like emotional health — requires individual agency and responsibility, and that no relationship thrives when one partner is rescuing the other indefinitely.

Conclusion

The question of whether to help your spouse or partner with their debts does not have a universal answer. It is shaped by the legal framework you live within, the nature and origin of the debt, the strength and maturity of the relationship, and the attitudes and behaviours of both partners toward money.What every couple can benefit from, regardless of which path they choose, is an honest, informed, and compassionate conversation about money. Debt is not a moral failing — it is a financial condition that can be addressed with the right plan, the right support, and the right attitude. The couples who navigate it most successfully are those who treat it as a shared challenge rather than a source of blame, and who make deliberate, agreed decisions rather than letting the situation drift.

Whether you choose full partnership, structured support, or respectful independence, the most important thing is that both of you are in the conversation — with clarity, honesty, and a plan.

Frequently Asked Questions (FAQ)

Am I legally responsible for my partner's debts if we are married?

In most of England, Wales, and Northern Ireland, you are not automatically responsible for debts your spouse held before marriage or in their name alone. However, joint accounts, co-signed loans, and — in community property US states — debts incurred during the marriage may create shared legal liability. Always seek specific legal advice if you are uncertain about your position.What should I do if my partner is hiding debt from me?

Financial deception is a serious issue in relationships. If you suspect undisclosed debt, you can request a full credit report conversation, suggest joint sessions with a financial counsellor, or access a free credit check service. Undisclosed debt is not just a financial problem — it is a trust issue that deserves open, honest conversation. If a partner consistently refuses transparency, professional relationship or financial counselling may be beneficial.Should we merge finances if one of us has significant debt?

There is no obligation to merge finances, and many couples find that maintaining some financial independence while managing a joint household budget works well. The decision to merge finances should be based on mutual trust, shared values, and transparent financial disclosure — not on the assumption that love resolves all money complications automatically.How do we create a debt repayment plan together?

Start by listing all debts with their balances, interest rates, and minimum payments. Then calculate the total monthly surplus available after all household expenses. Direct extra repayment funds at the highest-interest debt first (avalanche method) to minimise total interest paid, or the smallest balance first (snowball method) for psychological wins. Free tools are available through services like StepChange in the UK and the NFCC in the US.Can relationship conflict over debt be resolved?

Yes — many couples successfully navigate significant debt challenges and emerge with stronger financial habits and deeper trust. The key factors are openness, a willingness to take responsibility, a concrete plan, and patience. Couples who find it difficult to discuss money without conflict often benefit from working with a financial counsellor or therapist who specialises in financial relationships.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. StepChange Debt Charity (UK) — Free Debt Advice

https://www.stepchange.org/

2. National Foundation for Credit Counselling (US) — Debt Help

https://www.nfcc.org/

3. The Money Charity (UK) — Money Statistics Report

https://themoneycharity.org.uk/money-statistics/

4. Citizens Advice (UK) — Debt and Your Partner

https://www.citizensadvice.org.uk/debt-and-money/

5. Consumer Financial Protection Bureau (US) — Managing Debt

https://www.consumerfinance.gov/consumer-tools/debt-collection/

6. Journal of Family and Economic Issues — Financial Stress and Relationship Quality

https://link.springer.com/journal/10834

7. Money Advice Service (UK) — Talking to Your Partner About Money

https://www.moneyhelper.org.uk/en/family-and-care/talk-money/talking-to-your-partner-about-money

8. Investopedia — How Debt Affects Relationships

https://www.investopedia.com/financial-edge/0210/how-debt-can-destroy-a-budding-relationship.aspx

0 Comments Comments