Real Estate

Pay Off Your 30-Year Mortgage in 14 Years: How To

On a $300,000 mortgage at 6% over 30 years, you will pay your lender approximately $347,515 in interest alone — more than the property itself cost. But the amortisation schedule is not a fixed destiny. Strategic lump sum payments, applied directly to the principal at the right points in the mortgage term, can cut that loan in roughly half the time and save over $160,000 in interest. This guide shows exactly how the mathematics work, what the strategy looks like year by year, and how to execute it whether you are in the UK or the US.

The equivalent picture in the UK is equally stark. UKCalculator's February 2026 guide documents the average UK scenario: with an average house price of approximately £285,000 and a 20% deposit, the average mortgage is around £228,000. At 4.5% over 25 years, the total interest on that mortgage is approximately £152,000. The average UK homeowner will pay back £380,000 to own a house they borrowed £228,000 to buy.

This is not a design flaw in the mortgage product. It is the mathematics of compound interest applied to a large, long-term loan. The lender charges interest on the outstanding balance every month, and for the first many years of the loan, the outstanding balance barely moves because most of each monthly payment is consumed by interest rather than reducing the principal. Understanding this mechanism — amortisation — is the foundation of the strategy this guide explains.

On a 30-year $300,000 mortgage at 6%, your monthly payment is approximately $1,799. In month one, approximately $1,500 of that payment goes directly to the bank as interest — and only $299 reduces your actual loan balance. In month 12, the split is similar. In year five, you are still paying roughly $1,450 per month in interest and reducing the principal by only $349. By year 15, the split has equalised to roughly $950 interest and $850 principal. By year 25, most of each payment is principal. You have paid enormous sums to reach a position where your payments are finally working for you rather than for the bank.

The practical implication of this front-loading is profound and is the entire basis of the lump sum strategy: a pound or dollar of principal paid in year one is infinitely more valuable than a pound or dollar paid in year 25. When you reduce your principal in year one, you eliminate the interest that would have compounded on that amount for the remaining 29 years. When you reduce principal in year 25, you save only five years of interest on that amount. RealcostIQ's February 2026 analysis quantifies this precisely: 'A $200/month extra payment starting in Year 1 of a $320,000 loan at 7% saves approximately $89,000 in interest and pays the loan off 5.6 years early. The same $200/month starting in Year 15 saves only $28,000.'

Paying off your mortgage ahead of schedule is one of the highest-guaranteed returns available to any homeowner. Unlike stock market investments with uncertain returns, paying extra toward your mortgage principal delivers a guaranteed return equal to your interest rate — risk-free. At 7%, every $1,000 in extra principal payments saves roughly $2,400 in future interest.

— REALCOSTIQ — EARLY MORTGAGE PAYOFF CALCULATOR (FEBRUARY 2026)

Consider the effect concretely. On a $200,000, 30-year mortgage at 5% interest, Calculator.net's mortgage payoff analysis confirms that 'a one-time additional payment of $1,000 towards a $200,000, 30-year loan at 5% interest can pay off the loan four months earlier, saving $3,420 in interest.' That is a $3,420 guaranteed return on a $1,000 payment — a 3.42x guaranteed return, achieved simply by reducing the principal early. At higher interest rates, the multiplier is even more dramatic: RealcostIQ documents that 'at 7%, every $1,000 in extra principal payments saves roughly $2,400 in future interest.'

The multiplier effect works because every dollar of principal you remove from the balance in year one is a dollar that no longer generates compound interest for the lender over the remaining term. The bank was expecting to charge you interest on that dollar for 29 more years. When you pay it off now, they cannot. The earlier in the term you make lump sum payments, the longer the compounding chain you are cutting, and the larger the interest saving.

The table reveals two powerful dynamics. First, the running interest saved grows most rapidly in the early years — years 1 to 5 account for the majority of the total interest saved, because that is when the amortisation schedule is most interest-heavy. Second, the balance falls increasingly quickly in the later years because each overpayment and monthly payment represents a larger share of a smaller outstanding balance. The combination of front-loaded lump sums and consistent monthly overpayments creates a compounding acceleration effect that self-reinforces as the balance falls.

First: always designate the payment as a principal reduction payment. In US mortgage terminology, this is typically labelled 'principal only payment,' 'additional principal,' or 'prepayment toward principal.' In the UK, instructing the lender to 'reduce the capital balance' (as opposed to 'reduce future payments') ensures the benefit is applied immediately to the balance and that your interest calculation for the following month is based on the lower balance.

Second: in the UK, if your mortgage has an offset facility — where savings held in a linked account are offset against the mortgage balance for interest calculation purposes — depositing lump sums into the offset account rather than making a formal capital repayment can provide equivalent interest savings with the added benefit of retaining access to the funds if needed. This is a useful tool for homeowners who want the financial benefit of early repayment without permanently committing liquid funds.

Third: after any significant lump sum payment, request a new mortgage statement or recalculate your amortisation schedule to confirm the payment has been correctly applied and to update your projected payoff date. Errors in payment application are rare but not unheard of, and confirming the correct application provides both peace of mind and accurate data for your annual review.

TotalMortgage's extra payment analysis explains why this works: 'A bi-weekly schedule accelerates your payoff because it creates 13 full payments a year instead of the standard 12. By making half your standard payment every two weeks, you naturally add one extra principal payment annually, which significantly reduces total interest and shortens your loan term.' This one additional payment per year, applied to a 30-year mortgage from the start, typically reduces the total term by three to four years and saves tens of thousands of dollars in interest — without requiring any additional cash outlay beyond the thirteenth monthly payment.

Combined with the annual lump sum strategy, bi-weekly payments provide the consistent baseline acceleration that compounds alongside each lump sum, further compressing the payoff timeline. The combination of bi-weekly payments (one extra monthly payment per year) and $10,000 annual lump sums on a $300,000 mortgage at 6% takes the 30-year loan to approximately 14 years — the target payoff timeframe this guide is built around.

Casaplorer's mortgage analysis addresses this directly: 'Lump-sum payment: Instead of adding to your monthly payments, you may want to pay one large lump-sum towards your principal balance. This can help you save more on interest than if you paid the same amount as accelerated payments.' The reason is timing: a lump sum deployed in January eliminates an entire year's worth of interest on that amount from the moment it is applied. If you spread the same amount across 12 monthly overpayments, the first payment eliminates 12 months of future interest but the last payment in December eliminates only zero months of future interest within that calendar year. On average, monthly overpayments of the same total amount save slightly less interest than a front-loaded lump sum.

The practical answer is to use both in combination. Annual lump sums (from bonuses, refunds, or windfalls) provide the large step-changes that most dramatically compress the amortisation schedule. Monthly overpayments — even modest ones of $100 to $200 — provide consistent baseline acceleration that adds up significantly over time. AARP's April 2026 mortgage analysis confirms: '$100 more a month starting in the fifth year of that loan saves $34,184 in interest.' US Bank's calculator example shows that '$200 extra per month on a $405,000 loan at 6.625% can save $115,823 in interest over the full term.' Neither approach alone delivers the 14-year payoff target as effectively as the combination of both.

The strategy requires no special financial sophistication — only an understanding of how amortisation works, a commitment to redirecting periodic windfalls (bonuses, tax refunds, salary increases) to the mortgage before they are absorbed by spending, and the discipline to instruct your lender to apply all payments to the capital balance. Use a mortgage payoff calculator to model your exact numbers. Confirm your lender's overpayment rules. Apply every lump sum as early in the year as possible. And review your progress annually. The compound acceleration of falling principal on a falling balance means the final years of the mortgage pay off faster than any of the early ones — and the homeowner who arrives there debt-free a decade and a half ahead of schedule has earned both financial freedom and a sum in saved interest that rivals any investment they could have made.

UKCalculator — How to Pay Off Your Mortgage Early: UK Guide (February 2026) https://ukcalculator.com/how-to-pay-off-mortgage-early.html

WoodHall Mortgages — Pay Off Mortgage Early: Pros, Cons and Strategies (November 2025) https://woodhallmortgages.co.uk/pay-off-your-mortgage-early-pros-cons-strategies/

AARP — See How Much You Could Save By Paying Off Your Mortgage Early (April 2026) https://www.aarp.org/money/personal-finance/mortgage-payoff-calculator/

US Bank — Amortization Calculator: Extra Payment Calculator (2026) https://www.usbank.com/home-loans/mortgage/mortgage-calculators/amortization-calculator.html

MoneySavingExpert — Should I Overpay My Mortgage? (March 2026 update) https://www.moneysavingexpert.com/mortgages/mortgages-vs-savings/

Casaplorer — Early Mortgage Payoff Calculator (2026) https://casaplorer.com/early-mortgage-payoff-calculator

TotalMortgage — Extra Payment Mortgage Calculator: Making Additional Home Loan Payments https://www.totalmortgage.com/mortgage-calculators/extra-payment

Ramsey Solutions — Mortgage Payoff Calculator https://www.ramseysolutions.com/real-estate/mortgage-payoff-calculator

TABLE OF CONTENTS

- Why Your Mortgage Costs More Than You Think

- How Amortisation Front-Loads Your Interest Payments

- The Lump Sum Principle: Why Early Payments Are So Powerful

- The 14-Year Payoff Illustrated: A Worked Example

- Building Your Lump Sum Sources — Where the Money Comes From

- The Step-by-Step Execution Strategy

- Early Repayment Charges: UK and US Rules

- How to Instruct Your Lender Correctly

- The Bi-Weekly Payment Bonus

- Lump Sums vs Monthly Overpayments: Which Is Better?

- Conclusion

- Frequently Asked Questions

- References

1. Why Your Mortgage Costs More Than You Think

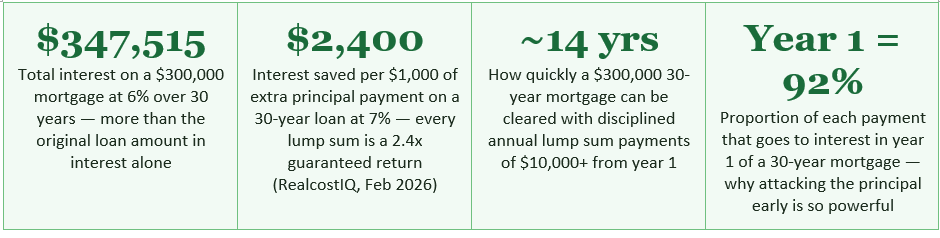

When you sign a 30-year mortgage for $300,000 at 6% interest, you are not simply agreeing to repay $300,000. You are agreeing to repay $300,000 in principal plus every penny of interest that accumulates over the 30-year term. On those numbers, AARP's April 2026 mortgage calculator confirms the total interest paid over a standard 30-year life is approximately $347,515 — meaning the bank receives more in interest than the original amount you borrowed. The true cost of the loan is $647,515, not $300,000.The equivalent picture in the UK is equally stark. UKCalculator's February 2026 guide documents the average UK scenario: with an average house price of approximately £285,000 and a 20% deposit, the average mortgage is around £228,000. At 4.5% over 25 years, the total interest on that mortgage is approximately £152,000. The average UK homeowner will pay back £380,000 to own a house they borrowed £228,000 to buy.

This is not a design flaw in the mortgage product. It is the mathematics of compound interest applied to a large, long-term loan. The lender charges interest on the outstanding balance every month, and for the first many years of the loan, the outstanding balance barely moves because most of each monthly payment is consumed by interest rather than reducing the principal. Understanding this mechanism — amortisation — is the foundation of the strategy this guide explains.

2. How Amortisation Front-Loads Your Interest Payments

Amortisation is the process by which a loan is repaid through regular equal payments, structured so that the proportions of interest and principal within each payment shift over the life of the loan. In the early years, almost every payment goes to interest. In the final years, almost every payment goes to principal. This front-loading of interest is the key insight behind the lump sum strategy.On a 30-year $300,000 mortgage at 6%, your monthly payment is approximately $1,799. In month one, approximately $1,500 of that payment goes directly to the bank as interest — and only $299 reduces your actual loan balance. In month 12, the split is similar. In year five, you are still paying roughly $1,450 per month in interest and reducing the principal by only $349. By year 15, the split has equalised to roughly $950 interest and $850 principal. By year 25, most of each payment is principal. You have paid enormous sums to reach a position where your payments are finally working for you rather than for the bank.

The practical implication of this front-loading is profound and is the entire basis of the lump sum strategy: a pound or dollar of principal paid in year one is infinitely more valuable than a pound or dollar paid in year 25. When you reduce your principal in year one, you eliminate the interest that would have compounded on that amount for the remaining 29 years. When you reduce principal in year 25, you save only five years of interest on that amount. RealcostIQ's February 2026 analysis quantifies this precisely: 'A $200/month extra payment starting in Year 1 of a $320,000 loan at 7% saves approximately $89,000 in interest and pays the loan off 5.6 years early. The same $200/month starting in Year 15 saves only $28,000.'

Paying off your mortgage ahead of schedule is one of the highest-guaranteed returns available to any homeowner. Unlike stock market investments with uncertain returns, paying extra toward your mortgage principal delivers a guaranteed return equal to your interest rate — risk-free. At 7%, every $1,000 in extra principal payments saves roughly $2,400 in future interest.

— REALCOSTIQ — EARLY MORTGAGE PAYOFF CALCULATOR (FEBRUARY 2026)

The Lump Sum Principle: Why Early Payments Are So Powerful

A lump sum payment is a single, substantial payment made directly against your mortgage principal — separate from your regular monthly payment. Unlike a regular monthly overpayment, which provides a modest incremental benefit, a meaningful lump sum creates an immediate step-change in your outstanding balance, fundamentally reshaping the amortisation schedule for all remaining years.Consider the effect concretely. On a $200,000, 30-year mortgage at 5% interest, Calculator.net's mortgage payoff analysis confirms that 'a one-time additional payment of $1,000 towards a $200,000, 30-year loan at 5% interest can pay off the loan four months earlier, saving $3,420 in interest.' That is a $3,420 guaranteed return on a $1,000 payment — a 3.42x guaranteed return, achieved simply by reducing the principal early. At higher interest rates, the multiplier is even more dramatic: RealcostIQ documents that 'at 7%, every $1,000 in extra principal payments saves roughly $2,400 in future interest.'

The multiplier effect works because every dollar of principal you remove from the balance in year one is a dollar that no longer generates compound interest for the lender over the remaining term. The bank was expecting to charge you interest on that dollar for 29 more years. When you pay it off now, they cannot. The earlier in the term you make lump sum payments, the longer the compounding chain you are cutting, and the larger the interest saving.

The 14-Year Payoff Illustrated: A Worked Example

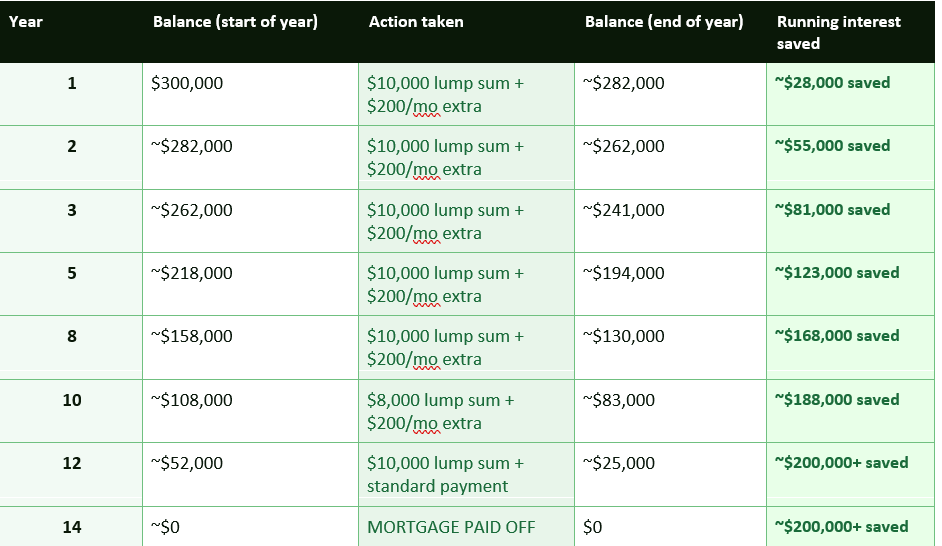

The following worked example demonstrates how a $300,000 mortgage at 6% over 30 years can be cleared in approximately 14 years using a realistic lump sum strategy combined with modest monthly overpayments. The figures use standard amortisation mathematics and are intended to illustrate the principle — your exact numbers will depend on your mortgage balance, rate, and overpayment capacity.

Illustrative figures based on standard amortisation calculations. Assumes $10,000 annual lump sum applied in month 1 of each year plus $200/month extra. Actual outcomes depend on interest rate, exact balance, lump sum timing, and lender terms. Use a mortgage payoff calculator (see references) to model your exact scenario.

The table reveals two powerful dynamics. First, the running interest saved grows most rapidly in the early years — years 1 to 5 account for the majority of the total interest saved, because that is when the amortisation schedule is most interest-heavy. Second, the balance falls increasingly quickly in the later years because each overpayment and monthly payment represents a larger share of a smaller outstanding balance. The combination of front-loaded lump sums and consistent monthly overpayments creates a compounding acceleration effect that self-reinforces as the balance falls.

Building Your Lump Sum Sources — Where the Money Comes From

The strategy requires a source of periodic lump sum funds to deploy against the mortgage principal. The most reliable sources are those that arrive on a predictable schedule — making it possible to plan each year's mortgage attack in advance.Eight reliable sources of lump sum mortgage overpayments

- Annual work bonus: For employees who receive an annual or quarterly bonus, committing a defined percentage (50% or more) of each bonus directly to the mortgage as a lump sum is the most powerful consistent source of overpayment capital. This works best when the decision is automatic — set up before the bonus arrives, so the money is applied before lifestyle spending absorbs it.

- Tax refunds: In the US, the average federal tax refund is approximately $3,000. In the UK, HMRC tax rebates for overpaid income tax, Marriage Allowance claims, or employment expense reimbursements can provide lump sums of several hundred to several thousand pounds. Directing tax refunds to mortgage principal rather than discretionary spending is a zero-sacrifice overpayment.

- Salary increments and pay rises: When income increases — a promotion, a new role, a market-rate pay review — the temptation is to expand lifestyle spending proportionally. Instead, committing part or all of the net salary increase to an increased monthly overpayment and an additional annual lump sum maintains current living standards while dramatically accelerating the mortgage payoff.

- Inheritance or windfall payments: A substantial inheritance or unexpected windfall represents the most powerful single lump sum opportunity. WoodHall Mortgages' November 2025 guide documents a case study where a £25,000 lump sum on a standard residential mortgage saved approximately £42,000 in interest versus staying on the standard variable rate with the original term.

- Annual savings sweeps: At the end of each calendar year, reviewing your savings accounts and applying any accumulated savings above your emergency fund threshold (three to six months of expenses) as a mortgage lump sum converts low-yield cash savings into a guaranteed return equal to your mortgage rate.

- Rental income or investment income: Homeowners who have income from a second property, side business, or investment portfolio can designate a defined portion of that income as an annual mortgage contribution, creating a systematic link between income-producing activity and mortgage reduction.

- Sale of assets: Selling a second car, selling items of value no longer needed, or liquidating underperforming investments can generate one-off lump sums for mortgage reduction.

- Overtime, freelance, or second income: Income from additional work — overtime pay, freelance projects, consulting work — that exceeds normal income requirements can be channelled directly to the mortgage, effectively using additional work hours to buy future financial freedom.

The Step-by-Step Execution Strategy

The lump sum mortgage payoff strategy has five execution steps that remain consistent regardless of the mortgage size, rate, or country.Step 1 — Know your exact numbers

Before making any overpayment, understand your current mortgage balance, your current interest rate, your remaining term, your lender's overpayment allowance (typically 10% of the outstanding balance per year in the UK, no limit for most US mortgages), and whether you are in an early repayment charge period. Call your lender or log in to your online mortgage account to retrieve your exact balance and the annual overpayment limit.Step 2 — Calculate your target trajectory

Use a mortgage payoff calculator (links provided in References) to model your specific scenario. Input your actual balance, rate, and term. Then model different lump sum amounts to understand how quickly each level of overpayment would clear the mortgage. For a 30-year mortgage, clearing it in 14 to 16 years typically requires annual lump sums of $8,000 to $12,000 alongside modest monthly overpayments — though this varies significantly with mortgage size and interest rate. The Ramsey Solutions calculator documents that adding $300 per month to a standard mortgage 'saves just over $64,000 in interest and pays off the home over 11 years sooner.' Combined with annual lump sums, the timeline compresses further.Step 3 — Instruct your lender correctly

This is the most critical operational step, and it is frequently misunderstood. When you make an overpayment, you must instruct your lender to apply the payment to the capital balance, not to defer future payments. As Casaplorer's mortgage guide states: 'When making additional payments, make sure to specify to your lender that the payments should be applied to your loan principal. Otherwise, the lender may apply the payments to future interest payments and you will not save on the interest cost from your principal balance.' UKCalculator's February 2026 guide reinforces this: 'Ask your lender to apply overpayments to reduce the capital balance (not defer future payments). Most do this automatically, but it is worth confirming in writing.'Step 4 — Deploy lump sums as early in each year as possible

Within each year, the earlier in the year you apply your lump sum, the more months of interest you eliminate. A lump sum applied in January saves 12 months of interest on that amount within the same year. The same lump sum applied in December saves approximately one month of interest within that year. For maximum impact, time lump sums to coincide with the earliest available opportunity — immediately upon receipt of a bonus, immediately when a tax refund arrives, or at the start of each mortgage year.Step 5 — Review and recalibrate annually

Once per year, pull your updated mortgage statement, recalculate your remaining term given the overpayments you have made, and adjust your lump sum target for the next year. As your balance falls, the annual interest charge decreases, and the same lump sum achieves an even larger proportional reduction in both balance and time. This annual review also provides the motivational reinforcement of seeing the tangible progress — a balance that has fallen faster than the standard schedule, and a projected payoff date that has moved meaningfully earlier.Early Repayment Charges: UK and US Rules

The most important risk to check before implementing the lump sum strategy is the early repayment charge (ERC) — a fee charged by some lenders when you overpay beyond certain limits during a fixed-rate period.UK: the 10% annual allowance rule

In the UK, most fixed-rate mortgage products allow overpayments of up to 10% of the outstanding mortgage balance per year without triggering an ERC. MoneySavingExpert confirms: 'Many UK deals allow up to 10% per year without an ERC, but check your lender.' On a £200,000 balance, 10% means £20,000 of penalty-free overpayment per year — sufficient for most lump sum strategies. Some lenders are more generous: tracker mortgages and standard variable rate (SVR) mortgages typically allow unlimited overpayments. Always check your specific mortgage offer document or call your lender before making a lump sum payment, particularly if you are within a fixed-rate period.US: mostly penalty-free but check your loan documents

Most US mortgages, particularly those purchased by Fannie Mae or Freddie Mac, do not carry prepayment penalties. TotalMortgage's extra payment calculator notes: 'In most cases, you can pay off your mortgage early without any penalties.' However, some portfolio loans, adjustable-rate mortgages, and private lender products do include prepayment penalties — typically 1% to 5% of the amount prepaid, applicable in the first three to five years of the loan. Ramsey Solutions advises: 'A prepayment penalty is a fee that can be charged if your mortgage is paid down or paid off early. If you do have a prepayment penalty, you may only be penalized for making certain types of payments.' Check your loan documents or call your servicer before making a large lump sum payment if you are within the first five years of the loan.How to Instruct Your Lender Correctly

The mechanical execution of a lump sum overpayment is straightforward once you understand the rules, but three operational details matter.First: always designate the payment as a principal reduction payment. In US mortgage terminology, this is typically labelled 'principal only payment,' 'additional principal,' or 'prepayment toward principal.' In the UK, instructing the lender to 'reduce the capital balance' (as opposed to 'reduce future payments') ensures the benefit is applied immediately to the balance and that your interest calculation for the following month is based on the lower balance.

Second: in the UK, if your mortgage has an offset facility — where savings held in a linked account are offset against the mortgage balance for interest calculation purposes — depositing lump sums into the offset account rather than making a formal capital repayment can provide equivalent interest savings with the added benefit of retaining access to the funds if needed. This is a useful tool for homeowners who want the financial benefit of early repayment without permanently committing liquid funds.

Third: after any significant lump sum payment, request a new mortgage statement or recalculate your amortisation schedule to confirm the payment has been correctly applied and to update your projected payoff date. Errors in payment application are rare but not unheard of, and confirming the correct application provides both peace of mind and accurate data for your annual review.

The Bi-Weekly Payment Bonus

Alongside lump sum payments, the bi-weekly payment strategy provides a structural, automatic boost to your repayment rate that requires no willpower or cash-flow planning once it is set up. Instead of making one monthly mortgage payment, you make half your monthly payment every two weeks. Because there are 52 weeks in a year, this produces 26 half-payments — or 13 full monthly payments — rather than the standard 12.TotalMortgage's extra payment analysis explains why this works: 'A bi-weekly schedule accelerates your payoff because it creates 13 full payments a year instead of the standard 12. By making half your standard payment every two weeks, you naturally add one extra principal payment annually, which significantly reduces total interest and shortens your loan term.' This one additional payment per year, applied to a 30-year mortgage from the start, typically reduces the total term by three to four years and saves tens of thousands of dollars in interest — without requiring any additional cash outlay beyond the thirteenth monthly payment.

Combined with the annual lump sum strategy, bi-weekly payments provide the consistent baseline acceleration that compounds alongside each lump sum, further compressing the payoff timeline. The combination of bi-weekly payments (one extra monthly payment per year) and $10,000 annual lump sums on a $300,000 mortgage at 6% takes the 30-year loan to approximately 14 years — the target payoff timeframe this guide is built around.

Lump Sums vs Monthly Overpayments: Which Is Better?

Both lump sum payments and regular monthly overpayments reduce the principal and save interest — the question is which approach produces better results for the same amount of money deployed.Casaplorer's mortgage analysis addresses this directly: 'Lump-sum payment: Instead of adding to your monthly payments, you may want to pay one large lump-sum towards your principal balance. This can help you save more on interest than if you paid the same amount as accelerated payments.' The reason is timing: a lump sum deployed in January eliminates an entire year's worth of interest on that amount from the moment it is applied. If you spread the same amount across 12 monthly overpayments, the first payment eliminates 12 months of future interest but the last payment in December eliminates only zero months of future interest within that calendar year. On average, monthly overpayments of the same total amount save slightly less interest than a front-loaded lump sum.

The practical answer is to use both in combination. Annual lump sums (from bonuses, refunds, or windfalls) provide the large step-changes that most dramatically compress the amortisation schedule. Monthly overpayments — even modest ones of $100 to $200 — provide consistent baseline acceleration that adds up significantly over time. AARP's April 2026 mortgage analysis confirms: '$100 more a month starting in the fifth year of that loan saves $34,184 in interest.' US Bank's calculator example shows that '$200 extra per month on a $405,000 loan at 6.625% can save $115,823 in interest over the full term.' Neither approach alone delivers the 14-year payoff target as effectively as the combination of both.

CONCLUSION

A 30-year mortgage does not have to take 30 years. The amortisation schedule is not a fixed destiny — it is a mathematical model that responds directly and powerfully to every pound or dollar of principal you remove from it, especially early in the term. At 7%, every $1,000 of early principal reduction saves approximately $2,400 in future interest — a guaranteed, risk-free return that no savings account or low-risk investment can match. Strategic annual lump sum payments of $8,000 to $12,000, combined with modest monthly overpayments and bi-weekly payment scheduling, can compress a 30-year mortgage to approximately 14 years and save over $160,000 in interest on a $300,000 loan.The strategy requires no special financial sophistication — only an understanding of how amortisation works, a commitment to redirecting periodic windfalls (bonuses, tax refunds, salary increases) to the mortgage before they are absorbed by spending, and the discipline to instruct your lender to apply all payments to the capital balance. Use a mortgage payoff calculator to model your exact numbers. Confirm your lender's overpayment rules. Apply every lump sum as early in the year as possible. And review your progress annually. The compound acceleration of falling principal on a falling balance means the final years of the mortgage pay off faster than any of the early ones — and the homeowner who arrives there debt-free a decade and a half ahead of schedule has earned both financial freedom and a sum in saved interest that rivals any investment they could have made.

Frequently Asked Questions

How do lump sum mortgage payments reduce the total interest I pay?

Every mortgage balance is subject to interest calculated on the outstanding principal. When you make a lump sum payment directly to the principal, you reduce the balance permanently from that point forward. All future interest charges are calculated on the new, lower balance rather than the original higher one. Because mortgage amortisation front-loads interest (in year one of a 30-year mortgage, roughly 92% of each payment is interest), reducing the principal in the early years eliminates the longest possible chain of compound interest. RealcostIQ's February 2026 analysis quantifies this: at 7%, every $1,000 of extra principal payment saves approximately $2,400 in future interest. The saving multiplier is highest in year one and decreases as you progress through the term.What is the 10% overpayment allowance in the UK and how does it work?

Most UK fixed-rate and tracker mortgage products include a penalty-free overpayment allowance — typically 10% of the outstanding mortgage balance per year. This means that on a £200,000 balance, you can make up to £20,000 in lump sum overpayments per year without incurring an Early Repayment Charge (ERC). ERCs typically range from 1% to 5% of the amount overpaid above the allowance. The allowance resets each year (the specific date depends on your mortgage product — usually the anniversary of your fixed rate). Always check your specific mortgage offer document or call your lender before making a lump sum payment. Standard Variable Rate (SVR) and most tracker mortgages allow unlimited overpayments without ERC. MoneySavingExpert confirms the general 10% rule and recommends checking your lender's specific terms before every significant overpayment.Does it matter when in the year I make a lump sum payment?

Yes — significantly. The earlier in the year you apply a lump sum, the more months of interest you eliminate within that calendar year and in all subsequent years. A lump sum applied in January reduces the balance for 12 months before the year-end; the same sum applied in December reduces the balance for approximately one month before year-end. The difference in total interest saved over the life of the loan between a January and a December lump sum of the same amount can be several hundred to several thousand dollars, depending on the mortgage size and rate. For maximum benefit, plan to apply lump sums at the earliest possible date — ideally the day a bonus is received, a tax refund arrives, or a windfall clears. Never hold the money for months before applying it.Is it better to overpay my mortgage or invest the money?

This is the central personal finance debate for homeowners with surplus cash, and the honest answer is: it depends on your mortgage interest rate and your expected investment return. Overpaying your mortgage delivers a guaranteed, risk-free return exactly equal to your mortgage interest rate. At 6%, every £1,000 of overpayment saves £1,000 worth of 6% guaranteed interest — equivalent to a 6% risk-free return on that money. If your expected after-tax investment return is higher than your mortgage rate (which historically it has been over long periods for equity investors), investing may produce better financial outcomes. If it is lower or comparable, mortgage overpayment is preferable. WoodHall Mortgages' November 2025 guide frames this well: for many homeowners, the combination is optimal — overpay the mortgage to within the penalty-free allowance and invest any remaining surplus. The right balance depends on your mortgage rate, investment options, risk tolerance, and time horizon.Do US mortgages have prepayment penalties?

Most US mortgages do not have prepayment penalties, particularly those purchased by Fannie Mae or Freddie Mac (which covers the majority of conforming conventional loans). TotalMortgage confirms: 'In most cases, you can pay off your mortgage early without any penalties.' However, some portfolio loans (held by the originating lender rather than sold to the secondary market), certain adjustable-rate mortgages, and private lender products do include prepayment penalties — typically 1% to 5% of the prepaid amount, applying in the first three to five years of the loan. FHA loans have no prepayment penalty. VA loans have no prepayment penalty. Check your loan note (the document you signed at closing) or call your mortgage servicer to confirm whether your specific loan includes a prepayment penalty before making a large lump sum payment.References

RealcostIQ — Early Mortgage Payoff Calculator: Save Thousands Paying Extra (February 2026) https://realcostiq.com/early-mortgage-payoff-calculator/UKCalculator — How to Pay Off Your Mortgage Early: UK Guide (February 2026) https://ukcalculator.com/how-to-pay-off-mortgage-early.html

WoodHall Mortgages — Pay Off Mortgage Early: Pros, Cons and Strategies (November 2025) https://woodhallmortgages.co.uk/pay-off-your-mortgage-early-pros-cons-strategies/

AARP — See How Much You Could Save By Paying Off Your Mortgage Early (April 2026) https://www.aarp.org/money/personal-finance/mortgage-payoff-calculator/

US Bank — Amortization Calculator: Extra Payment Calculator (2026) https://www.usbank.com/home-loans/mortgage/mortgage-calculators/amortization-calculator.html

MoneySavingExpert — Should I Overpay My Mortgage? (March 2026 update) https://www.moneysavingexpert.com/mortgages/mortgages-vs-savings/

Casaplorer — Early Mortgage Payoff Calculator (2026) https://casaplorer.com/early-mortgage-payoff-calculator

TotalMortgage — Extra Payment Mortgage Calculator: Making Additional Home Loan Payments https://www.totalmortgage.com/mortgage-calculators/extra-payment

Ramsey Solutions — Mortgage Payoff Calculator https://www.ramseysolutions.com/real-estate/mortgage-payoff-calculator

0 Comments Comments