Budgeting

State of Budgeting & Money Management in the US.

Table of Contents

- The Headline Numbers: Budgeting in 2026

- The Genuine Progress: What's Actually Improving

- The Persistent Problems: Where Budgeting Is Falling Short

- The Emergency Savings Gap

- Record Credit Card Debt

- Budgets That Exist on Paper but Not in Practice

- How Americans Are Actually Tracking Their Money

- Why Americans Budget: The Underlying Motivations

- What the Data Suggests About Building a Budget That Actually Works

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

More Americans have a budget in 2026 than at any point in at least the past five years — and yet, according to the same surveys reporting that progress, a clear majority of the country is still living paycheck to paycheck, financial anxiety is at a five-year high, and credit card balances have reached a record $1.23 trillion. This is the central, somewhat uncomfortable paradox at the heart of America's current relationship with money management: budgeting has never been more popular, and it has never felt less sufficient on its own.

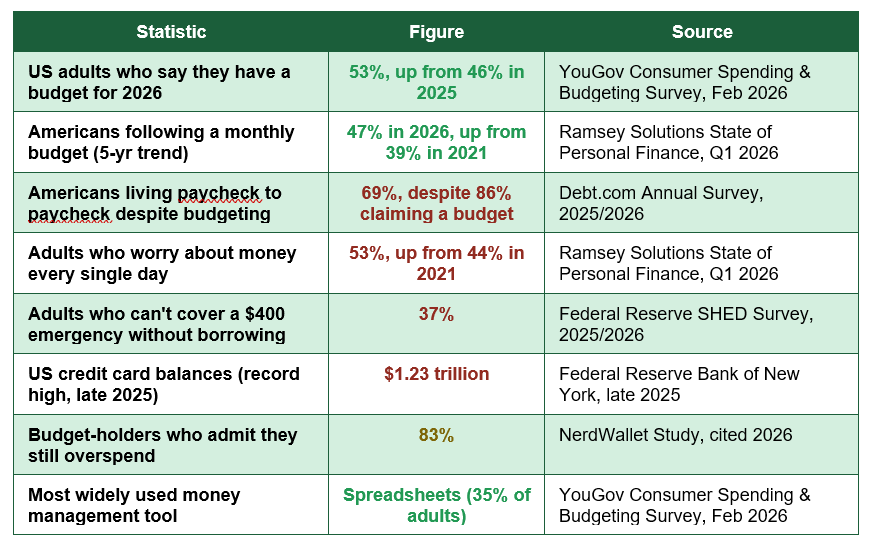

This paradox is not a contradiction in the data — it is the data's most important finding. YouGov's February 2026 survey found that 53% of US adults now have a budget for the year, up from 46% in 2025. Ramsey Solutions' five-year retrospective study found the share of Americans following a monthly budget has climbed from 39% in 2021 to 47% in 2026, with the sharpest gains concentrated among Gen Z and middle-income households. At the same time, Debt.com's annual survey found that 69% of Americans were living paycheck to paycheck heading into 2026, despite 86% of respondents claiming to have a budget in place — leading the survey's own analysts to conclude, simply, that 'the math isn't the problem.'

This guide draws together the most current, credible national survey data — from YouGov, Ramsey Solutions, the Federal Reserve, Bankrate, and Debt.com — to provide an honest, comprehensive picture of how Americans are actually managing money in 2026: who budgets and who doesn't, which tools they use, why budgets so often fail to translate into financial security, and what the generational divide in money habits reveals about where household finance is heading next.

The Headline Numbers: Budgeting in 2026

The table below brings together the most current, nationally representative statistics on budgeting and money management heading into and through 2026:

The budgeting paradox in one statistic: 86% have a budget, but 69% live paycheck to paycheck — Debt.com's analysts concluded that the issue is not arithmetic — most Americans know how to construct a budget — but consistency, follow-through, and the gap between intention and behaviour over time

Inflation remains the dominant backdrop: Bankrate's 2026 Financial Outlook Survey found that personal finance pessimism has reached its highest level in at least eight years, with 32% of Americans expecting their finances to worsen in 2026 — and of those, 78% specifically cited continued high inflation as the reason. Prices have climbed roughly 25% since 2020, while median household income has shown no statistically significant increase over the same period, a gap that sits underneath nearly every other statistic in this report.

The Genuine Progress: What's Actually Improving

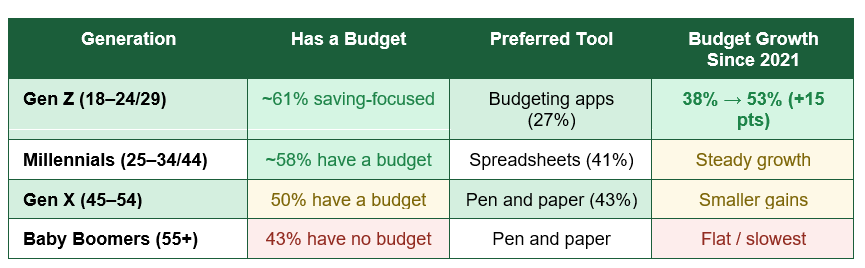

Despite the genuine challenges documented throughout this report, it would be inaccurate to characterise 2026 purely as a story of financial deterioration. Ramsey Solutions' five-year retrospective study, marking the program's milestone anniversary, identified several areas of real, measurable improvement in how Americans manage money compared to 2021.The share of Americans who say 'debt is a normal part of life' has fallen from 59% in 2021 to 51% in 2026 — a meaningful shift in attitude that has coincided with behavioural change: debit card usage has risen from 35% to 41% over the same period, while credit card reliance has edged down from 42% to 39%, with Gen Z showing the sharpest decline of any generation, from 27% to just 20%. Sixty percent of US adults say they are better off financially today than they were five years ago, and a notably optimistic 74% believe they will be better off financially five years from now, even amid the near-term pessimism captured in other surveys.

Encouragingly, the budgeting gains are not evenly distributed by chance — they are concentrated precisely where financial education and habit-formation efforts have focused most intensely. Gen Z's budgeting rate has nearly doubled, from 38% to 53% over five years, and middle-income households have seen a comparable jump from 37% to 49%, suggesting that targeted financial literacy efforts and the proliferation of budgeting apps designed for younger, digitally native users are having a measurable, durable effect.

The Persistent Problems: Where Budgeting Is Falling Short

Set against this genuine progress, several data points reveal where budgeting, as commonly practised, continues to fall short of producing real financial security for a majority of Americans.The Emergency Savings Gap

According to the Federal Reserve's Survey of Household Economics and Decisionmaking (SHED), 73% of US adults describe themselves as 'doing okay financially' — yet 37% say they could not cover an unexpected $400 expense without borrowing money or selling something. This gap between self-reported financial adequacy and actual emergency preparedness is one of the most consistently cited warning signs in household finance research, suggesting that many Americans' sense of financial stability is more fragile, and more dependent on nothing going wrong, than they themselves perceive.Record Credit Card Debt

US credit card balances reached a record $1.23 trillion by late 2025, according to the Federal Reserve Bank of New York's household debt tracking — a figure that underscores how, even amid rising budget adoption, a meaningful share of household spending is still being financed through revolving, high-interest debt rather than covered by current income and savings.Budgets That Exist on Paper but Not in Practice

Perhaps the most telling statistic in this entire report comes from NerdWallet's research finding that 83% of Americans who report having a budget admit they still overspend relative to it. This single figure captures the core limitation of budgeting as it is most commonly practised in 2026: constructing a budget has become widespread and increasingly accessible, but the harder work of sustaining adherence to it, month after month, against the backdrop of real financial stress, remains the much larger unsolved challenge.Financial stress is rising despite budgeting gains: 53% worry about money daily, up from 44% in 2021 — even as more Americans construct formal budgets than ever before, the share reporting daily financial worry has climbed nine percentage points over the same five-year period (Ramsey Solutions, Q1 2026)

How Americans Are Actually Tracking Their Money

One of the more counterintuitive findings in YouGov's 2026 survey is that, despite the proliferation of sophisticated budgeting apps and AI-powered financial tools, the single most widely used money management method among US adults remains the humble spreadsheet, used by 35% of all respondents — including 47% of 18-24 year-olds and 41% of 35-44 year-olds, two age groups one might assume would gravitate most naturally toward app-based solutions.WalletHub's complementary research breaks this pattern down further by generation: while 27% of young adults (18-29) say they prefer dedicated budgeting apps, the preference shifts notably with age, with 39% of those 30-44 favouring spreadsheets and 43% of those 45-59 sticking with traditional pen-and-paper tracking. This suggests the budgeting tool landscape in 2026 is genuinely generationally fragmented rather than converging on a single dominant digital solution, even as fintech investment in budgeting and money management apps continues to grow.

Why Americans Budget: The Underlying Motivations

Understanding why people budget reveals as much about the current financial climate as the budgeting rates themselves. YouGov's research found that the dominant motivation, cited by 66% of those with a budget, is simply ensuring enough money is available for essentials — food, rent, and bills — a figure that rises to 70% among women and 69% among both 25-34 and 45-54 year-olds, indicating that budgeting in 2026 is, for a clear majority of practitioners, fundamentally a tool of necessity rather than aspiration.Beyond covering essentials, 49% budget specifically to increase general savings (rising to 61% among both 18-24 and 25-34 year-olds), 38% budget specifically to stop overspending, 35% use a budget to manage debt, and 29% are saving toward a specific defined goal such as a house deposit or a holiday. This hierarchy of motivations — survival first, debt management and overspending control second, aspirational saving last — provides a clear, data-grounded picture of where most American households currently sit on the spectrum from financial precarity to financial planning.

The optimism-pessimism split by age: YouGov found that younger adults remain considerably more optimistic about their 2026 financial outlook than older generations — 45% of 18-24 year-olds and 48% of 25-34 year-olds expect their finances to improve in 2026, compared to just 29-30% among those 35 and older. Adults 55 and over are the most likely of any age group to expect their finances to worsen (32%), a pattern likely connected to fixed or near-fixed retirement income colliding with persistent inflation in essential costs.

What the Data Suggests About Building a Budget That Actually Works

Drawing on the patterns identified across this body of 2026 research, several practical principles emerge for households looking to close the gap between having a budget and actually benefiting from one:- Treat budget adherence, not budget creation, as the real challenge: With 83% of budget-holders admitting to overspending, the evidence strongly suggests that the planning stage is not where most households need the most support — building in regular, low-friction review habits matters more than constructing an initially perfect budget.

- Build emergency savings before optimising every spending category: With 37% of Americans unable to cover a $400 emergency without borrowing, prioritising even a modest, automatically funded emergency reserve addresses the single most common point of budget failure: an unplanned expense derailing an otherwise sound plan.

- Choose a tracking method you will actually maintain, not the most sophisticated one available: The continued dominance of spreadsheets across nearly every age group, despite the availability of advanced budgeting apps, suggests that consistency of use matters far more than the technical sophistication of the tool itself.

- Address high-interest debt as a parallel priority, not an afterthought: With US credit card balances at a record $1.23 trillion, a budget that does not explicitly account for accelerated repayment of high-interest revolving debt is unlikely to produce meaningful financial improvement, regardless of how well other categories are managed.

- Recognise that values-based budgeting tends to outperform restriction-based budgeting: Financial guidance increasingly emphasises identifying genuine spending priorities and redirecting money away from low-value categories, rather than imposing blanket restrictions — an approach consistent with why purely willpower-based budgets, per NerdWallet's findings, fail so consistently.

Conclusion

The state of budgeting and money management in the United States in 2026 is genuinely a story of two simultaneous, equally true trends: more Americans are budgeting than at any point in recent memory, with real, measurable gains concentrated among younger and middle-income households, and yet the gap between having a budget and achieving financial security remains stubbornly wide for a clear majority of the population. Sixty-nine percent living paycheck to paycheck despite an 86% budgeting rate, record credit card debt, and a 37% emergency-fund shortfall all point to the same underlying conclusion: the limiting factor in American household finance in 2026 is not financial literacy or planning ability in the abstract, but the much harder combination of consistent execution, adequate income relative to costs, and resilience against the unplanned expenses that derail even well-constructed plans.The generational data offers a genuinely hopeful thread within this otherwise mixed picture. Gen Z's budgeting rate has nearly doubled in five years, debt is increasingly viewed as something to be managed rather than accepted as inevitable, and a clear majority of Americans believe their financial situation will improve over the coming five years even amid near-term pessimism. Whether that optimism is realised will depend less on whether more households adopt a budget — that battle is increasingly being won — and more on whether the structural gap between costs and incomes narrows enough for budgeting discipline to actually translate into the financial security it is meant to produce.

For individual households navigating this landscape, the clearest lesson from the 2026 data is to treat budgeting not as a one-time exercise of writing down numbers, but as an ongoing practice of review, adjustment, and emergency-fund building that is resilient to the inevitable months when the plan and reality diverge. The Americans showing the most genuine progress in this year's data are not necessarily those with the most sophisticated spreadsheets or apps, but those who have built the habit of consistent engagement with their own numbers, month after month, regardless of which tool sits in front of them.

Frequently Asked Questions (FAQ)

Why do so many Americans have a budget but still live paycheck to paycheck?

This gap, identified clearly in Debt.com's 2025/2026 survey (86% with a budget versus 69% living paycheck to paycheck), reflects a distinction between budget creation and budget adherence. NerdWallet's research found that 83% of people with a budget admit to overspending relative to it, suggesting the core challenge for most households is not a lack of financial planning knowledge but the harder, ongoing work of sticking to a plan consistently, particularly against a backdrop of inflation that has outpaced wage growth for many households since 2020.What's the most popular budgeting tool in the US in 2026?

Spreadsheets remain the single most widely used money management tool overall, used by 35% of US adults according to YouGov's 2026 survey, including a notable 47% of 18-24 year-olds. Preferences do vary by age: WalletHub's research found that younger adults (18-29) are more likely to favour dedicated budgeting apps (27%), while those 45-59 are more likely to use traditional pen-and-paper tracking (43%), indicating a genuinely fragmented tool landscape rather than a single dominant method across all generations.Has budgeting actually improved Americans' financial situations over the past five years?

The evidence is mixed but leans cautiously positive on several dimensions. Ramsey Solutions' five-year retrospective found that 60% of Americans say they are better off financially than five years ago, debt is increasingly viewed as avoidable rather than inevitable (down from 59% to 51% agreeing 'debt is a normal part of life'), and credit card reliance has declined modestly while debit card usage has risen. At the same time, daily financial worry has increased over the same period, and emergency savings adequacy remains a persistent weak point, suggesting genuine but incomplete progress rather than a uniformly positive trend.Which generation is making the most progress with budgeting?

Gen Z shows the most dramatic improvement in the available data, with budgeting rates rising from 38% to 53% over the five years tracked by Ramsey Solutions' research, alongside the sharpest decline in credit card reliance of any generation (27% to 20%) and the highest rate of optimism about their 2026 financial outlook (45-48% expecting improvement, per YouGov). Middle-income households have also shown comparably strong gains, with budgeting rates rising from 37% to 49% over the same period.What is the single biggest financial vulnerability revealed by 2026 survey data?

The inability to absorb an unexpected expense stands out as the most consistently cited vulnerability across multiple independent surveys. The Federal Reserve's SHED survey found 37% of US adults could not cover a $400 emergency expense without borrowing or selling something, even though 73% describe themselves as generally 'doing okay financially' — a gap that suggests many households' sense of financial stability depends heavily on nothing unexpected occurring, rather than reflecting genuine resilience against financial shocks.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. YouGov — US Consumer Spending and Budgeting Trends in 2026

https://yougov.com/en-us/articles/54197-us-consumer-spending-and-budgeting-trends-in-2026

2. Ramsey Solutions — The State of Personal Finance in America, Q1 2026

https://www.ramseysolutions.com/budgeting/state-of-personal-finance

3. Federal Reserve — Survey of Household Economics and Decisionmaking (SHED)

https://www.federalreserve.gov/consumerscommunities/shed.htm

4. Federal Reserve Bank of New York — Household Debt and Credit Report

https://www.newyorkfed.org/microeconomics/hhdc

5. Bankrate — 2026 Financial Outlook Survey

https://www.bankrate.com/banking/financial-outlook-survey/

6. WalletHub — Budgeting Statistics for 2026

https://wallethub.com/edu/budgeting-statistics/146387

7. National Endowment for Financial Education (NEFE) — Consumer Polls and Research

https://www.nefe.org/research/polls/default.aspx

8. Debt.com — Annual Money Survey

https://www.debt.com/research/

0 Comments Comments