Spending

UK Consumer Behaviour Trends: The Full Data

Table of Contents

- The Headline Numbers: UK Consumer Sentiment in 2026

- Where UK Consumers Are Cutting Back

- The Trust Collapse: Brand Loyalty and Shrinkflation Fatigue

- Rising Saving Ratio Amid Falling Confidence

- Where UK Spending Is Holding Up — or Even Growing

- What This Means: Practical Takeaways

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

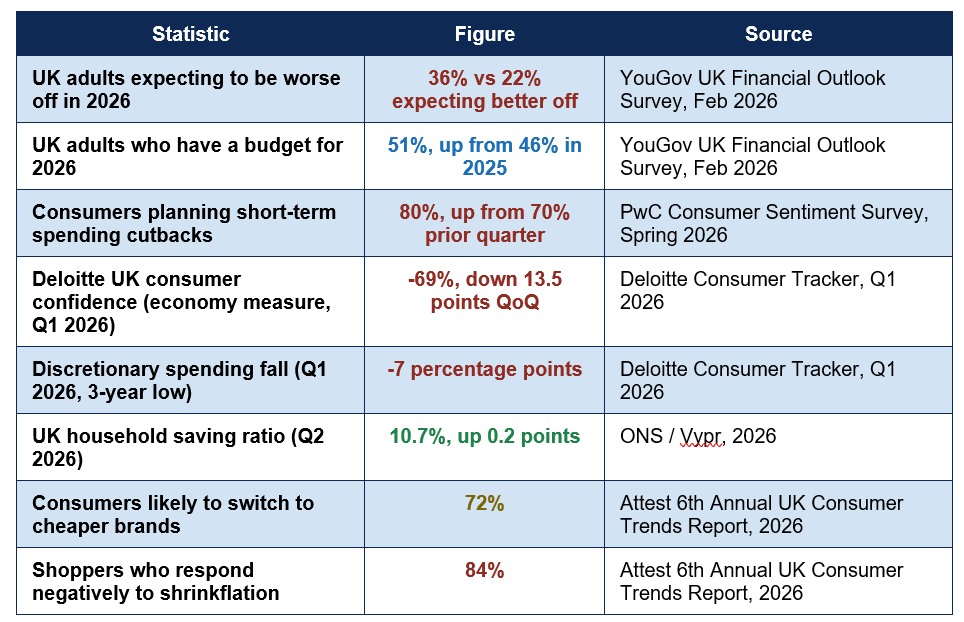

UK consumer confidence has fallen to its lowest level in four years, discretionary spending has dropped to a three-year low, and 80% of consumers say they are planning short-term spending cutbacks — yet, paradoxically, the UK household saving ratio has actually risen, and nearly four in five households report that their overall spending has increased year-on-year. This is the genuinely complex picture emerging from the most current UK consumer research in 2026: a population that is spending more in absolute terms, while feeling, planning, and behaving more cautiously than at almost any point since the depths of the pandemic.

Several converging pressures explain this mood. Deloitte's Q1 2026 Consumer Tracker found that renewed geopolitical instability, particularly the escalation of conflict in the Middle East, has driven energy costs higher and pushed consumer confidence down 13.5 percentage points in a single quarter, the sharpest decline since the end of 2024. PwC's Spring 2026 Consumer Sentiment Survey similarly found that nine out of ten UK consumers now name the cost of living as their single biggest concern, with almost three-quarters saying this concern will directly shape their spending and saving decisions over the coming year.

This guide draws together the most current, credible UK consumer research — from YouGov, Deloitte, PwC, Barclays, RSM, and Attest — to map exactly how British consumer behaviour is shifting in 2026: who is budgeting and why, where spending cutbacks are concentrated, how trust and brand loyalty are evolving, and which sectors are bucking the broader cautious trend. The result is a comprehensive, data-grounded picture of a UK consumer landscape defined by careful, deliberate spending rather than either confident growth or outright retreat.

The Headline Numbers: UK Consumer Sentiment in 2026

The table below brings together the most current UK survey data on consumer confidence, budgeting, and spending behaviour:

Deloitte confidence index, Q1 2026: -69%, lowest since Q4 2022 — the sharpest quarterly fall since the depths of the pandemic in Q2 2020, driven primarily by renewed energy cost pressure and broader geopolitical uncertainty (Deloitte Consumer Tracker, Q1 2026)

The spending-confidence paradox explained: Vypr's research found that while 79% of UK households report increased year-on-year spending, more than four in five (81%) remain worried about rising living costs. The explanation lies in inflation: even as nominal spending rises, much of that increase simply reflects higher prices for the same goods and services, rather than households genuinely having more discretionary purchasing power. Real wages have struggled to keep pace, meaning higher spending and lower confidence are entirely compatible rather than contradictory.

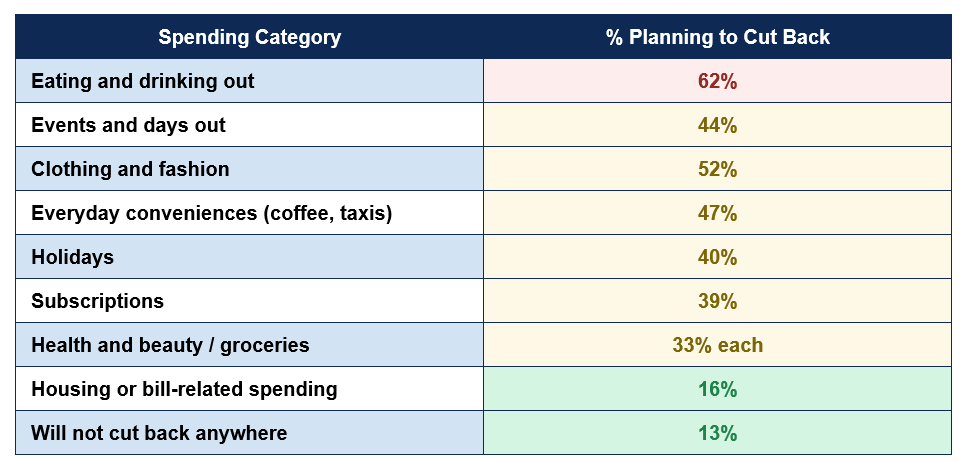

Where UK Consumers Are Cutting Back

YouGov's February 2026 survey provides a detailed breakdown of exactly where consumers who expect their finances to worsen plan to make cuts, offering a precise map of which spending categories are considered discretionary and dispensable versus which are protected as close to essential:

The pattern is consistent and economically logical: eating and drinking out is, by a clear margin, the first and most common area of cutback, reflecting its position as one of the most easily deferred discretionary expenses. Clothing, everyday conveniences such as takeaway coffee and taxis, and holidays follow closely behind. By contrast, housing and bill-related spending sits at the bottom of the cutback list, reflecting both its largely fixed, contractual nature and its status as a genuine necessity that few households have meaningful flexibility to reduce in the short term.

Notably, even among the smaller group of consumers who expect their financial situation to improve in 2026, cutback intentions remain present, if more muted: 44% still plan to reduce spending on eating and drinking out, and 32% on everyday conveniences. This suggests that cautious spending habits in 2026 have become somewhat decoupled from individual financial outlook, reflecting a broader, more entrenched cultural shift toward deliberate spending rather than a behaviour confined only to those under direct financial pressure.

The Trust Collapse: Brand Loyalty and Shrinkflation Fatigue

Perhaps the most significant structural shift identified in Attest's sixth annual UK Consumer Trends report is the extent to which trust, rather than price alone, has become the deciding factor in UK purchasing decisions. The research found that 72% of UK consumers are now likely to switch to cheaper brands, while 84% of shoppers respond negatively to shrinkflation — the practice of reducing product size or quantity while maintaining or increasing price — and 71% say they leave or lose trust in a retailer entirely after experiencing an unexpected bank charge or fee.This trust erosion extends into subscription services specifically: 55% of UK consumers report having been auto-renewed into a subscription without clear consent, a pattern increasingly described in consumer research as 'subscription bloat' and contributing to broader scepticism toward recurring payment models across streaming, software, and retail membership schemes. Attest's analysis concludes that even small, isolated breaches of consumer trust can now trigger outright brand abandonment in a way that may not have been true even a few years ago, reflecting both heightened price sensitivity and a generally lower tolerance for perceived unfairness during a period of sustained cost pressure.

Consumers who lose trust after an unexpected bank charge: 71% — a single unexpected fee is now enough to drive a majority of UK consumers to abandon a brand or provider entirely, illustrating how thin the margin for error has become in a cost-conscious consumer environment (Attest, 2026)

Rising Saving Ratio Amid Falling Confidence

ONS data shows the UK household saving ratio increased to 10.7% in the second quarter of the year being tracked, a 0.2 percentage point rise, even as broader confidence measures from Deloitte and PwC trended downward over a similar period. This apparent contradiction is, in fact, a textbook precautionary savings response: facing the prospect of larger utility bills and the possibility of future tax rises, UK households are choosing to set money aside specifically as a buffer, even while simultaneously reporting deep pessimism about their overall financial trajectory.This dynamic is creating genuinely new opportunities in UK retail and financial services. Vypr's research highlights that some major retailers, including Currys, are exploring embedded savings accounts tied to existing customer loyalty schemes — explicitly positioning the brand as a financial partner rather than purely a point of sale. The logic is straightforward: in an environment where 81% of households remain cost-conscious despite increased spending, brands that visibly help customers save, rather than simply encouraging more spending, may build a more durable form of loyalty than traditional promotional discounting alone can achieve.

RSM's research adds an important nuance to the saving story: precautionary behaviour tends to lag the initial economic shock before intensifying. Drawing on the pattern observed after the 2022 energy crisis triggered by Russia's invasion of Ukraine, RSM notes that consumer confidence took nearly two years to recover, with the deepest pullback in discretionary spending typically arriving well after the initial shock rather than immediately. This suggests the full consumer behaviour impact of 2026's renewed geopolitical and energy pressures may still be unfolding.

Where UK Spending Is Holding Up — or Even Growing

Despite the broadly cautious backdrop, Barclays' transaction-level spending data for the period to late May 2026 reveals several categories showing genuine, sustained growth, painting a more nuanced picture than blanket consumer retrenchment.- Digital content and subscriptions: Rose 12.8% year-on-year, the strongest growth since August 2021, driven by popular streaming content and major sporting events — suggesting that even cost-conscious consumers continue prioritising home entertainment value relative to its cost.

- Fuel spending: Increased 11.9% year-on-year, the category's largest uplift since 2022, reflecting rising pump prices passing directly through to consumer spending on an essential, largely inelastic category.

- Staycations and domestic travel: One in five UK consumers report planning a staycation this year, citing convenience, lower costs, and a preference for UK-based trips, contributing to hotel and domestic accommodation spending outperforming international travel, which fell for a third consecutive month amid a more cautious, wait-and-see approach to overseas trips.

- Seasonal and weather-driven categories: Warmer May weather and an early bank holiday boosted spending on food and drink specialists, up 4% year-on-year, as households hosted barbecues and outdoor gatherings — illustrating that even within an overall cautious spending environment, short-term, weather- and event-driven discretionary spending can still see meaningful growth.

What This Means: Practical Takeaways

For businesses operating in the UK consumer market, and for consumers themselves navigating this environment, several practical patterns emerge from the 2026 data:- Value communication matters more than price alone: With 72% of consumers willing to switch to cheaper alternatives but trust functioning as the ultimate deciding factor, businesses that communicate genuine value and maintain transparent pricing are better positioned than those competing on price cuts alone.

- Transparency failures carry outsized consequences: The finding that 71% of consumers lose trust after just one unexpected charge underscores how little room for error exists; clear, upfront pricing and proactive communication about any fees or charges has become a competitive necessity rather than a nice-to-have.

- Essential spending categories remain the most resilient: Housing, bills, and core grocery spending consistently show the least appetite for cutbacks across every survey reviewed, meaning businesses in genuinely essential categories face more stable demand than those in clearly discretionary ones.

- Households should expect a lagged, extended period of caution: RSM's historical analysis of the 2022 energy shock suggests the full consumer behaviour response to 2026's pressures may continue unfolding for a year or more, meaning both businesses and individual financial planning should account for an extended period of consumer caution rather than expecting a rapid rebound.

- Precautionary saving and spending are not mutually exclusive: The rising saving ratio alongside increased overall spending shows households are not simply retrenching uniformly; many are simultaneously building a financial buffer while continuing to spend on what they value most, a pattern individuals can replicate in their own budgeting by deliberately protecting both an emergency fund and spending on genuine priorities.

Conclusion

UK consumer behaviour in 2026 defies easy categorisation as either a confident recovery or a straightforward downturn. The data instead reveals a population engaged in careful, deliberate calibration: confidence has fallen to its lowest level since the end of 2022, 80% of consumers are planning spending cutbacks, and nine in ten name the cost of living as their primary concern — yet overall spending continues to rise, the household saving ratio is climbing, and specific categories like digital subscriptions, fuel, and domestic travel are showing genuine growth even amid the broader caution.The thread connecting these seemingly contradictory data points is trust and value, more than price or confidence in isolation. With 72% of consumers ready to switch to cheaper brands and 84% reacting negatively to practices like shrinkflation, UK consumers in 2026 are not simply spending less — they are spending more selectively, more cautiously, and with considerably less tolerance for perceived unfairness or hidden costs than in previous years. Renewed geopolitical instability and energy cost pressure, layered onto several years of already-elevated living costs, have pushed this selective, trust-driven approach to spending from a niche behaviour into the clear mainstream.

For businesses and individual consumers alike, the practical lesson from this year's data is the same: in an environment this finely balanced between continued spending and genuine caution, transparency, demonstrated value, and protection against unwelcome financial surprises matter more than at almost any point in recent UK consumer history. Those who understand and respond to this trust-first, value-conscious mindset — rather than assuming either confident growth or blanket retrenchment — are best placed to navigate what RSM's own research suggests could be an extended period of careful, watchful UK consumer behaviour.

Frequently Asked Questions (FAQ)

Why has UK consumer confidence fallen so sharply in 2026?

Deloitte's Q1 2026 Consumer Tracker attributes the 13.5 percentage point quarterly fall in its confidence index primarily to the impact of renewed geopolitical events, particularly escalating conflict in the Middle East, which pushed energy costs higher just as households were already managing slowing wage growth and a deteriorating job market. PwC's complementary research found that nine in ten consumers now cite the cost of living as their primary concern, with these worries intensifying further in the wake of the same geopolitical developments.If consumers are cutting back, why is overall UK spending still increasing?

This apparent contradiction is explained largely by inflation and category-specific dynamics rather than genuine across-the-board growth in discretionary purchasing power. Vypr's research found 79% of households report increased year-on-year spending, but much of this reflects higher prices for the same goods rather than greater real spending capacity. At the same time, specific categories like fuel (up due to higher pump prices) and digital subscriptions (up due to strong content demand) are growing even as broadly discretionary categories like eating out, fashion, and holidays see widespread planned cutbacks.What is 'shrinkflation' and why does it matter so much to UK consumers right now?

Shrinkflation refers to the practice of reducing a product's size, weight, or quantity while keeping the price the same or increasing it, effectively raising the per-unit price without an explicit headline price increase. Attest's 2026 research found 84% of UK shoppers respond negatively to this practice, reflecting heightened sensitivity to perceived unfairness during a sustained cost-of-living squeeze; consumers who feel misled by reduced product sizes are increasingly likely to switch brands entirely rather than simply accept the change.How long is this period of cautious UK consumer spending likely to last?

RSM's analysis of the 2022 energy crisis, triggered by Russia's invasion of Ukraine, found that UK consumer confidence took nearly two years to fully recover, with the deepest pullback in discretionary spending typically emerging well after the initial economic shock rather than immediately. Applying this historical pattern to the renewed pressures of 2026 suggests the current period of consumer caution may continue for an extended period, potentially well into 2027, rather than resolving quickly.Which spending categories are most protected from UK consumer cutbacks?

Housing and bill-related spending consistently rank lowest among categories UK consumers plan to cut, at just 16% according to YouGov's 2026 research, reflecting both the largely fixed, contractual nature of these costs and their status as genuine necessities. Core grocery spending and health-related spending also show comparatively more resilience than clearly discretionary categories such as eating out, fashion, and non-essential travel, which consistently top the list of planned cutbacks across nearly every survey reviewed in this report.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. YouGov — UK Financial Outlook 2026: Consumer Spending Trends, Budgeting Habits and Financial Expectations

https://yougov.com/en-gb/articles/54168-uk-financial-outlook-2026-consumer-spending-trends-budgeting-habits-and-financial-expectations

2. Deloitte — The Deloitte Consumer Tracker, Q1 2026

https://www.deloitte.com/uk/en/Industries/consumer/research/consumer-tracker.html

3. PwC UK — Consumer Sentiment Survey, Spring 2026

https://www.pwc.co.uk/industries/retail-consumer/insights/consumer-sentiment-survey.html

4. Barclays Corporate — UK Consumer Spend Report

https://www.barclayscorporate.com/insights/industry-expertise/uk-consumer-spending-report/

5. RSM UK — Consumer Outlook 2026

https://www.rsmuk.com/insights/consumer-outlook

6. Attest — 2026 UK Consumer Trends Report

https://www.askattest.com/our-research/2026-uk-consumer-trends-report

7. Office for National Statistics — UK Consumer Trends Statistics

https://www.gov.uk/government/statistics/announcements/consumer-trends-uk-october-to-december-2026

8. Vypr — UK Consumer Spending Trends 2026: Essential Insights for Brands

https://vyprclients.com/future-of-uk-consumer-spending/

0 Comments Comments