Spending

UK Discretionary Spending Cuts 2026: Recalibration Not Retreat

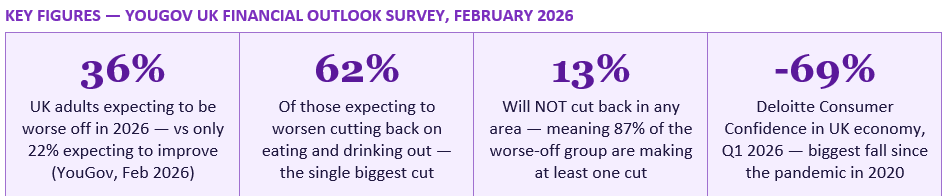

Among the 36% of UK adults who expect to be worse off in 2026, 62% plan to cut eating and drinking out, 52% fashion, 40% holidays, 39% subscriptions, and 33% even groceries. But this is not a collapse in consumer confidence — it is a deliberate, strategic recalibration. This guide unpacks every category, explains what the data really shows, and explores what it means for households, brands, and the wider economy.

The spending cut data is presented by YouGov for two distinct groups: those who expect their finances to worsen in 2026 (the 36%), and those who expect them to improve (the 22%). The contrast between these two groups is instructive — and somewhat surprising in the case of the better-off group, who are also planning significant reductions in some categories despite expecting improvement.

Among those expecting to be worse off, the scale of intended cuts is broad. Only 13% say they will not be cutting back in any area — meaning that 87% of the worse-off group are planning to reduce spending in at least one category. The cuts are concentrated in discretionary rather than essential spending, with eating out, fashion, and entertainment leading the list. But the fact that a third of this group is also planning to cut groceries suggests that for some households, essentials are also under pressure.

The data shows a UK consumer landscape shaped by divergent financial outlooks. In 2026, expectations about personal finances act as a key lens for spending decisions, influencing both everyday purchases and longer-term priorities across sectors.

— YOUGOV UK FINANCIAL OUTLOOK 2026 SURVEY, FEBRUARY 2026

Source: YouGov UK Financial Outlook Survey, 2,087 adults, 6–9 February 2026. Base: Those expecting finances to worsen in 2026.

The hospitality sector has felt this pressure acutely. RSM UK's Consumer Outlook, drawing on NIQ RSM Hospitality Business Tracker data, found that UK hospitality trading was broadly flat in 2025, with pubs outperforming the market as consumers prioritised value-led social occasions while restaurant demand remained weak as households curtailed eating out. Deloitte's Consumer Tracker for Q1 2026, based on a survey of over 3,000 UK adults conducted in March 2026, confirmed that consumer discretionary spending fell to its lowest level in three years — with the biggest single contribution from the fall in eating out and clothing spending.

The Nationwide 2026 spending research adds important nuance: even in this environment, a third of UK consumers are planning to cut eating out while a separate group are making deliberate choices about which dining experiences they preserve. The trade-down dynamic — from full-service restaurants to casual dining, from casual dining to pubs, from eating out to home cooking — is consistent with what RSM describes as consumers 'consciously cutting back on non-essentials' rather than abandoning the activity entirely.

For the 44% of the better-off group who are also cutting eating out, the motivation is different. KPMG's Consumer Pulse data suggests these households are not cutting because they cannot afford to eat out — they are cutting because they are being more intentional about which eating-out occasions represent genuine value and which are simply habit. The distinction between financially-driven and intentionally-driven cuts is important for understanding where the hospitality market is heading.

The mechanisms of the fashion cut vary by income group. For lower-income households, cuts to clothing spending typically mean buying less frequently, delaying replacement purchases, and switching to cheaper alternatives. YouGov's historical cost of living data shows that in earlier phases of the crisis, 29% of those cutting clothing were buying less frequently, 10% were switching to cheaper alternatives, and 8% had stopped clothing spending entirely. In 2026, the trade to secondhand has emerged as a significant additional mechanism.

KPMG's December 2025 Consumer Pulse found that 21% of UK consumers are likely to buy more secondhand goods in 2026 than in 2025 — rising to 31% among 18 to 24-year-olds. RSM's Consumer Outlook notes a modest improvement in clothing and fashion spending plans — 8% planning to spend more, up from 5% a year ago — suggesting a cautious re-engagement with fashion among some segments, even as the worse-off group cuts back sharply. The resale and secondhand market is one of the clear beneficiaries of the discretionary spending recalibration, with platforms including Vinted, Depop, and eBay seeing sustained strong demand.

Nationwide's January 2026 research of 1,202 customers found that travel remains the top priority for 2026 spending, with over a third planning to prioritise long trips and short breaks. Holidays, festivals, concerts, and experiences dominate the wish lists of more than four in ten consumers determined to treat themselves despite rising household bills. KPMG's Consumer Pulse found that if consumers had more discretionary budget in 2026, most (32%) would put it toward holiday costs — suggesting that holidays represent the top aspirational spend even among those who are currently cutting.

Consumer Edge's UK credit and debit card data from April 2026 provides a cautionary note: travel saw the sharpest deterioration in spending growth in the weeks following the onset of the Iran conflict in late February 2026. The combination of rising energy prices, heightened economic uncertainty, and the specific anxiety around flight costs and jet fuel prices appears to have dented travel spending intentions more acutely than the earlier February data suggested. This is a dynamic that will be worth watching through the second half of 2026.

The key insight from the holiday data is that the cut is highly income-stratified. For the financially pressed, holidays are a genuine casualty of cost of living pressures — the 40% cut figure reflects real choices to cancel or reduce travel plans. For those who are financially stable or improving, holidays are the last category to be cut and often the one being protected or even increased at the expense of other discretionary spending.

The average UK household has accumulated a significant number of streaming, software, and digital subscriptions over the past five years. Lockdown-era additions that seemed justified when the outside world was closed have persisted as ongoing monthly costs long after their original justification expired. A 2026 audit of the average UK household's subscription portfolio — Netflix, Disney Plus, Spotify, Amazon Prime, Apple Music, a gym membership, a news subscription, and one or two niche streaming services — can easily reveal £50 to £100 of monthly spending, much of which may be paid for services that are rarely or never used.

Moneybox's spending data, published in December 2025, found that monthly grocery bills had increased 14% and rent/mortgage payments 24% between 2024 and 2025. Against that backdrop, unused subscription cancellation is both financially rational and psychologically compelling — it provides an immediate, visible, controllable reduction in outgoings that the household can see on next month's bank statement. The 39% cut rate for subscriptions, even among households expecting their finances to worsen, is somewhat surprising only in that it is not higher.

The broader picture from RSM's Consumer Outlook is instructive: only 13% of consumers say their discretionary spending will be higher in 2026 than in 2025, and 57% of consumers would use a hypothetical £5,000 windfall to save or pay down debt rather than spend it. These figures confirm that the subscription cut is part of a broader defensive reorientation of household spending toward financial security rather than consumption.

Understanding how households cut grocery spending is important: it rarely means eating less. It typically means switching supermarkets (to Aldi, Lidl, or discount retailers), switching to own-brand products, reducing food waste, planning meals more carefully, buying less-expensive protein sources (lentils, eggs, tinned fish in place of meat), and reducing non-essential food items within the grocery basket (treat foods, premium beverages, convenience items). These are rational, cost-reducing strategies that maintain nutrition while reducing expenditure.

UK food price inflation in March 2026 was 3.7% year-on-year, according to ONS data — still above general CPI (3.3%) and continuing to add to cumulative food price increases of approximately 25% to 30% since 2020. The British Retail Consortium has forecast food price inflation remaining above 5% in 2026. Against this backdrop, the 33% grocery cut is better understood as a response to ongoing food price inflation rather than a new crisis — households are adjusting the composition and source of their food spending in response to sustained price pressure, not simply spending less on food in absolute terms.

The comparison with the better-off group is instructive: 14% of those expecting their finances to improve plan to spend more on groceries. This likely reflects improved diet quality, more organic or premium food choices, and less reliance on the very cheapest options that some households adopted during the crisis peak.

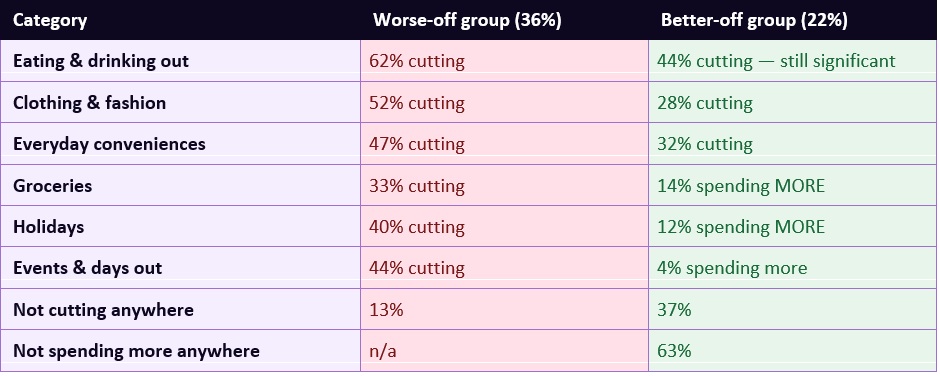

Two findings stand out. First, even among the better-off group, 44% are cutting eating and drinking out — suggesting that some of the reduction in dining out reflects a value-driven choice to cook more and dine out more selectively, not just financial necessity. Second, and perhaps most importantly, the better-off group is broadly not spending more across most categories — 63% say they will not increase spending anywhere. This points to what KPMG's Consumer Pulse describes as a 'cautious consumer landscape' in which even households with improving finances are rebuilding financial buffers and maintaining spending discipline rather than releasing pent-up consumption.

A retreat would mean households are cutting spending because they are in distress, have exhausted savings, and have no choice but to reduce consumption. The spending cuts in this scenario are forced and create negative economic feedback loops: reduced consumer spending depresses business revenues, leads to job losses, which further reduces consumer spending. The data from the height of the 2022 to 2023 cost of living crisis had elements of this — households were cutting essentials, skipping meals, and running down savings at rates that reflected genuine financial distress.

A recalibration, by contrast, describes households that are consciously adjusting the composition of their spending in response to changed price levels and financial priorities — not because they are in distress, but because they are being more intentional about where their money goes. The evidence for the recalibration framing in 2026 is significant. RSM's finding that 57% of consumers would use a £5,000 windfall to save or pay down debt rather than spend it suggests financial prudence, not crisis. KPMG's data showing 25% of consumers are planning a holiday spend in Q1 2026 suggests protected experiential spending. The growth of secondhand purchasing (21% of consumers, rising to 31% of Gen Z) is not a distressed behaviour — it is a value-driven choice that many consumers will maintain even if finances improve.

The YouGov data itself supports the recalibration framing. The 51% of UK adults who now have a budget — up from 38% in 2023 — are not all in financial distress. Many are simply applying more deliberate management to their money than they did before the cost of living crisis began. The 41% budgeting to stop overspending, and the 43% looking to increase general savings, reflect households that have developed new financial habits that they intend to maintain.

Consumer Edge's UK credit and debit card spending data from April 2026 adds a real-time dimension: the onset of the Iran conflict in late February 2026 triggered an immediate broad-based slowdown in discretionary spending growth, with travel seeing the sharpest deterioration. This real-time behavioural shift, visible in actual card transaction data rather than just survey intentions, confirms that the intended spending cuts in the YouGov data are already materialising in practice.

The YouGov survey data, read alongside RSM, KPMG, and Nationwide research, points to three dominant reallocation priorities.

The framing of 'recalibration, not retreat' is borne out by the data. Households are protecting experiences, rebuilding savings, shifting to secondhand and value-led purchasing, and cutting habitual or low-value spending rather than retreating from the economy entirely. The 13% who are not cutting anything — and the 22% expecting to improve — are the growth segment that consumer businesses are competing for. But even that group is, in 63% of cases, not planning to increase spending anywhere. The era of effortless consumer growth, if it ever truly existed, has not returned to the UK in 2026.

Deloitte — The Deloitte Consumer Tracker Q1 2026 (March 2026) https://www.deloitte.com/uk/en/Industries/consumer/research/consumer-tracker.html

KPMG UK — Cautious Consumer Landscape Continues into 2026 (December 2025) https://kpmg.com/uk/en/media/press-releases/2025/12/cautious-consumer-landscape-continues.html

RSM UK — Consumer Outlook 2026 https://www.rsmuk.com/insights/consumer-outlook

Nationwide — 2026 Spending Trends: Consumers Splash Out on Holidays and Wellness (January 2026) https://www.nationwide.co.uk/media/news/2026-spending-trends-consumers-splash-out-on-holidays-concerts-and-wellness-but-rising-costs-put-big-purchases-on-ice

Consumer Edge — UK Consumers Already Pulling Back on Discretionary Spend (April 2026) https://www.consumeredge.com/resources/insights/data-suggests-uk-consumers-are-already-pulling-back-on-discretionary-spend/

Chad.co.uk / Moneybox — Brits to Slash Spending in 2026, Axing Takeaways and Subscriptions (December 2025) https://www.chad.co.uk/read-this/brits-to-slash-spending-in-2026-axing-takeaways-subscriptions-and-nights-out-5453529

House of Commons Library — High Cost of Living: Impact on Households (January 2026) https://researchbriefings.files.parliament.uk/documents/CBP-10100/CBP-10100.pdf

MoneyHelper — Free Budgeting Tools and Guidance https://www.moneyhelper.org.uk

Turn2Us — Benefits Entitlement Calculator https://www.turn2us.org.uk

TABLE OF CONTENTS

- The Data: Who Is Cutting and How Much?

- The Full Spending Cuts Breakdown

- Category Deep-Dive 1: Eating and Drinking Out

- Category Deep-Dive 2: Clothing and Fashion

- Category Deep-Dive 3: Holidays and Travel

- Category Deep-Dive 4: Subscriptions

- Category Deep-Dive 5: Groceries — The Reluctant Cut

- What the Better-Off Group Is Doing Differently

- Recalibration vs Retreat: Why the Framing Matters

- The Broader Context: Deloitte, KPMG, and RSM Data

- What Is Being Prioritised Instead

- What This Means for Households, Brands, and the Economy

- Conclusion

- Frequently Asked Questions

- References

The Data: Who Is Cutting and How Much?

The YouGov UK Financial Outlook survey, conducted with 2,087 nationally representative UK adults between 6 and 9 February 2026, provides the most granular publicly available picture of how UK households plan to adjust their spending in 2026. The headline finding is that 36% of UK adults expect their financial situation to worsen in 2026, compared with only 22% who expect it to improve — an overall cautious outlook that has translated into concrete plans to cut discretionary spending across multiple categories.The spending cut data is presented by YouGov for two distinct groups: those who expect their finances to worsen in 2026 (the 36%), and those who expect them to improve (the 22%). The contrast between these two groups is instructive — and somewhat surprising in the case of the better-off group, who are also planning significant reductions in some categories despite expecting improvement.

Among those expecting to be worse off, the scale of intended cuts is broad. Only 13% say they will not be cutting back in any area — meaning that 87% of the worse-off group are planning to reduce spending in at least one category. The cuts are concentrated in discretionary rather than essential spending, with eating out, fashion, and entertainment leading the list. But the fact that a third of this group is also planning to cut groceries suggests that for some households, essentials are also under pressure.

The data shows a UK consumer landscape shaped by divergent financial outlooks. In 2026, expectations about personal finances act as a key lens for spending decisions, influencing both everyday purchases and longer-term priorities across sectors.

— YOUGOV UK FINANCIAL OUTLOOK 2026 SURVEY, FEBRUARY 2026

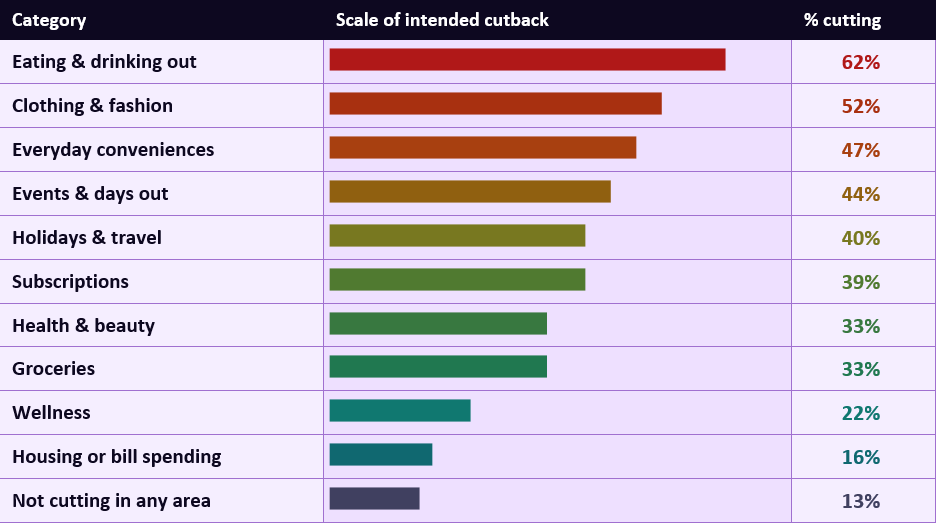

The Full Spending Cuts Breakdown

The table below shows the full spending cuts data from YouGov's February 2026 survey, for households expecting to be worse off. The bar chart visualises relative scale across all categories.Source: YouGov UK Financial Outlook Survey, 2,087 adults, 6–9 February 2026. Base: Those expecting finances to worsen in 2026.

Category Deep-Dive 1: Eating and Drinking Out

At 62%, eating and drinking out is the single most common intended spending cut among UK households expecting to be worse off in 2026. This finding is consistent across every piece of consumer research published in early 2026 and reflects a structural shift in dining-out behaviour that has been building since the start of the cost of living crisis.The hospitality sector has felt this pressure acutely. RSM UK's Consumer Outlook, drawing on NIQ RSM Hospitality Business Tracker data, found that UK hospitality trading was broadly flat in 2025, with pubs outperforming the market as consumers prioritised value-led social occasions while restaurant demand remained weak as households curtailed eating out. Deloitte's Consumer Tracker for Q1 2026, based on a survey of over 3,000 UK adults conducted in March 2026, confirmed that consumer discretionary spending fell to its lowest level in three years — with the biggest single contribution from the fall in eating out and clothing spending.

The Nationwide 2026 spending research adds important nuance: even in this environment, a third of UK consumers are planning to cut eating out while a separate group are making deliberate choices about which dining experiences they preserve. The trade-down dynamic — from full-service restaurants to casual dining, from casual dining to pubs, from eating out to home cooking — is consistent with what RSM describes as consumers 'consciously cutting back on non-essentials' rather than abandoning the activity entirely.

For the 44% of the better-off group who are also cutting eating out, the motivation is different. KPMG's Consumer Pulse data suggests these households are not cutting because they cannot afford to eat out — they are cutting because they are being more intentional about which eating-out occasions represent genuine value and which are simply habit. The distinction between financially-driven and intentionally-driven cuts is important for understanding where the hospitality market is heading.

Category Deep-Dive 2: Clothing and Fashion

Clothing and fashion at 52% among the worse-off group is the second largest intended cut — and represents a continuation of a trend that has been reshaping the UK clothing market for several years. Deloitte's Q1 2026 Consumer Tracker identified clothing and footwear as one of the two categories with the sharpest decline in discretionary spending, down 11 percentage points on Q4 2025 and 10 percentage points year-on-year.The mechanisms of the fashion cut vary by income group. For lower-income households, cuts to clothing spending typically mean buying less frequently, delaying replacement purchases, and switching to cheaper alternatives. YouGov's historical cost of living data shows that in earlier phases of the crisis, 29% of those cutting clothing were buying less frequently, 10% were switching to cheaper alternatives, and 8% had stopped clothing spending entirely. In 2026, the trade to secondhand has emerged as a significant additional mechanism.

KPMG's December 2025 Consumer Pulse found that 21% of UK consumers are likely to buy more secondhand goods in 2026 than in 2025 — rising to 31% among 18 to 24-year-olds. RSM's Consumer Outlook notes a modest improvement in clothing and fashion spending plans — 8% planning to spend more, up from 5% a year ago — suggesting a cautious re-engagement with fashion among some segments, even as the worse-off group cuts back sharply. The resale and secondhand market is one of the clear beneficiaries of the discretionary spending recalibration, with platforms including Vinted, Depop, and eBay seeing sustained strong demand.

Category Deep-Dive 3: Holidays and Travel

The holiday spending picture is among the most nuanced in the data — and reveals a sharp divergence between income groups that is absent in most other categories. Among the worse-off group, 40% plan to cut holidays. But consumer research from multiple sources consistently shows that holidays remain the top protected or even increased spending category among those who can afford it.Nationwide's January 2026 research of 1,202 customers found that travel remains the top priority for 2026 spending, with over a third planning to prioritise long trips and short breaks. Holidays, festivals, concerts, and experiences dominate the wish lists of more than four in ten consumers determined to treat themselves despite rising household bills. KPMG's Consumer Pulse found that if consumers had more discretionary budget in 2026, most (32%) would put it toward holiday costs — suggesting that holidays represent the top aspirational spend even among those who are currently cutting.

Consumer Edge's UK credit and debit card data from April 2026 provides a cautionary note: travel saw the sharpest deterioration in spending growth in the weeks following the onset of the Iran conflict in late February 2026. The combination of rising energy prices, heightened economic uncertainty, and the specific anxiety around flight costs and jet fuel prices appears to have dented travel spending intentions more acutely than the earlier February data suggested. This is a dynamic that will be worth watching through the second half of 2026.

The key insight from the holiday data is that the cut is highly income-stratified. For the financially pressed, holidays are a genuine casualty of cost of living pressures — the 40% cut figure reflects real choices to cancel or reduce travel plans. For those who are financially stable or improving, holidays are the last category to be cut and often the one being protected or even increased at the expense of other discretionary spending.

Category Deep-Dive 4: Subscriptions

The 39% of the worse-off group planning to cut subscriptions represents one of the most actionable data points in the entire YouGov survey — because subscription cutting is the most within-reach, immediate, and financially rational response to financial pressure available to most UK households.The average UK household has accumulated a significant number of streaming, software, and digital subscriptions over the past five years. Lockdown-era additions that seemed justified when the outside world was closed have persisted as ongoing monthly costs long after their original justification expired. A 2026 audit of the average UK household's subscription portfolio — Netflix, Disney Plus, Spotify, Amazon Prime, Apple Music, a gym membership, a news subscription, and one or two niche streaming services — can easily reveal £50 to £100 of monthly spending, much of which may be paid for services that are rarely or never used.

Moneybox's spending data, published in December 2025, found that monthly grocery bills had increased 14% and rent/mortgage payments 24% between 2024 and 2025. Against that backdrop, unused subscription cancellation is both financially rational and psychologically compelling — it provides an immediate, visible, controllable reduction in outgoings that the household can see on next month's bank statement. The 39% cut rate for subscriptions, even among households expecting their finances to worsen, is somewhat surprising only in that it is not higher.

The broader picture from RSM's Consumer Outlook is instructive: only 13% of consumers say their discretionary spending will be higher in 2026 than in 2025, and 57% of consumers would use a hypothetical £5,000 windfall to save or pay down debt rather than spend it. These figures confirm that the subscription cut is part of a broader defensive reorientation of household spending toward financial security rather than consumption.

Category Deep-Dive 5: Groceries — The Reluctant Cut

The 33% of worse-off households planning to cut grocery spending is the most significant figure in the entire dataset — because groceries are not a discretionary category. They are an essential. When households start cutting food spending, it typically signals that the financial pressure has moved beyond discretionary tightening and into essential cost management.Understanding how households cut grocery spending is important: it rarely means eating less. It typically means switching supermarkets (to Aldi, Lidl, or discount retailers), switching to own-brand products, reducing food waste, planning meals more carefully, buying less-expensive protein sources (lentils, eggs, tinned fish in place of meat), and reducing non-essential food items within the grocery basket (treat foods, premium beverages, convenience items). These are rational, cost-reducing strategies that maintain nutrition while reducing expenditure.

UK food price inflation in March 2026 was 3.7% year-on-year, according to ONS data — still above general CPI (3.3%) and continuing to add to cumulative food price increases of approximately 25% to 30% since 2020. The British Retail Consortium has forecast food price inflation remaining above 5% in 2026. Against this backdrop, the 33% grocery cut is better understood as a response to ongoing food price inflation rather than a new crisis — households are adjusting the composition and source of their food spending in response to sustained price pressure, not simply spending less on food in absolute terms.

The comparison with the better-off group is instructive: 14% of those expecting their finances to improve plan to spend more on groceries. This likely reflects improved diet quality, more organic or premium food choices, and less reliance on the very cheapest options that some households adopted during the crisis peak.

What the Better-Off Group Is Doing Differently

One of the most revealing aspects of the YouGov data is the comparison between the worse-off group (36% of adults) and the better-off group (22%). Even the better-off group is not entirely increasing spending — 63% say they will not be spending more in any area — but the pattern of their cuts and increases tells a very different story.Two findings stand out. First, even among the better-off group, 44% are cutting eating and drinking out — suggesting that some of the reduction in dining out reflects a value-driven choice to cook more and dine out more selectively, not just financial necessity. Second, and perhaps most importantly, the better-off group is broadly not spending more across most categories — 63% say they will not increase spending anywhere. This points to what KPMG's Consumer Pulse describes as a 'cautious consumer landscape' in which even households with improving finances are rebuilding financial buffers and maintaining spending discipline rather than releasing pent-up consumption.

Recalibration vs Retreat: Why the Framing Matters

The distinction between 'recalibration' and 'retreat' is not semantic. It carries fundamentally different implications for how the UK consumer landscape will evolve through 2026 and beyond.A retreat would mean households are cutting spending because they are in distress, have exhausted savings, and have no choice but to reduce consumption. The spending cuts in this scenario are forced and create negative economic feedback loops: reduced consumer spending depresses business revenues, leads to job losses, which further reduces consumer spending. The data from the height of the 2022 to 2023 cost of living crisis had elements of this — households were cutting essentials, skipping meals, and running down savings at rates that reflected genuine financial distress.

A recalibration, by contrast, describes households that are consciously adjusting the composition of their spending in response to changed price levels and financial priorities — not because they are in distress, but because they are being more intentional about where their money goes. The evidence for the recalibration framing in 2026 is significant. RSM's finding that 57% of consumers would use a £5,000 windfall to save or pay down debt rather than spend it suggests financial prudence, not crisis. KPMG's data showing 25% of consumers are planning a holiday spend in Q1 2026 suggests protected experiential spending. The growth of secondhand purchasing (21% of consumers, rising to 31% of Gen Z) is not a distressed behaviour — it is a value-driven choice that many consumers will maintain even if finances improve.

The YouGov data itself supports the recalibration framing. The 51% of UK adults who now have a budget — up from 38% in 2023 — are not all in financial distress. Many are simply applying more deliberate management to their money than they did before the cost of living crisis began. The 41% budgeting to stop overspending, and the 43% looking to increase general savings, reflect households that have developed new financial habits that they intend to maintain.

The Broader Context: Deloitte, KPMG, and RSM Data

The YouGov survey data is consistent with and complemented by several other major consumer confidence and spending datasets published in early 2026.Deloitte Consumer Tracker Q1 2026

Deloitte's Consumer Tracker, based on a survey of over 3,000 UK adults conducted between 12 and 17 March 2026, found that consumer discretionary spending fell to its lowest level in three years in Q1 2026 — its lowest level since Q1 2023, which was just months after UK inflation reached its 11.1% peak. Confidence in the UK economy fell 13.5 percentage points to -69%, representing the biggest single-quarter fall since Q4 2024 and returning to levels last seen in Q4 2022. The fall was driven by a broad-based decline across all non-essential categories, led by clothing and footwear (down 11 percentage points on Q4 2025) and alcoholic beverages (down 15 percentage points). Deloitte's commentary noted that 'this drop represents the biggest fall since Q2 2020 when the UK was in the midst of a global pandemic.'KPMG Consumer Pulse Q4 2025 / Q1 2026

KPMG UK's Consumer Pulse survey of 3,000 UK consumers, published in December 2025, found that 49% of those thinking the economy is worsening say they are cutting discretionary spend, and only 13% say their discretionary spending will be higher in 2026 than 2025. Forty-two per cent plan no big-ticket spending in Q1 2026. KPMG's head of consumer retail Linda Ellett described 'a landscape of consumers adjusting to higher household essential outgoings and spending caution due to perception of a worsening economy' as likely to continue into 2026.RSM UK Consumer Outlook 2026

RSM's Consumer Outlook, drawing on 2,000 consumer survey respondents plus real-time performance data from RSM's proprietary industry trackers, found that 52% of adults feel financially comfortable (unchanged from a year ago) but the share feeling financially squeezed has risen to 18%, up from 14%. Gen X leads the squeezed group at 26% financially stretched, consistent with the Aegon data showing Gen X as the least financially optimistic generation. RSM characterises the outlook as 'selective demand, uneven recovery and a focus on value and experience.'Consumer Edge's UK credit and debit card spending data from April 2026 adds a real-time dimension: the onset of the Iran conflict in late February 2026 triggered an immediate broad-based slowdown in discretionary spending growth, with travel seeing the sharpest deterioration. This real-time behavioural shift, visible in actual card transaction data rather than just survey intentions, confirms that the intended spending cuts in the YouGov data are already materialising in practice.

What Is Being Prioritised Instead

The spending cuts data tells only half the story. Equally important is what UK households are doing with the money they are not spending on eating out, fashion, and holidays.The YouGov survey data, read alongside RSM, KPMG, and Nationwide research, points to three dominant reallocation priorities.

Saving and financial resilience

RSM's finding that 57% of consumers would use a £5,000 windfall to save or pay down debt rather than spend it captures the dominant financial mood. Emergency savings ranked second in the Aegon Financial Priorities survey at 34%, reflecting a strong desire to rebuild financial buffers depleted during the cost of living crisis. KPMG found that willingness to dip into savings to fund spending is limited, with only 8% planning to draw down savings to manage costs. The combined picture is of a consumer population that is prioritising rebuilding financial resilience over maintaining consumption levels — a rational response to several years of financial insecurity.Experiences over goods

The one category that consistently emerges as protected or increased even among financially cautious households is experiences — particularly holidays, concerts, festivals, and wellness activities. Nationwide's research found that 41% of consumers are determined to treat themselves this year and that holiday budget is ring-fenced even as other spending falls. Deloitte's commentary notes that 'spending on travel remains the exception' to the broader discretionary spending decline. RSM identifies health and beauty as a category seeing a growing share planning to spend more, driven particularly by Gen Z. The experiences-over-goods shift, which predates the cost of living crisis in some respects, has been accelerated by it.Value-led purchasing

KPMG's Consumer Pulse found that 21% of consumers will use AI tools to track prices in 2026, and a fifth will buy more secondhand goods. The shift toward value-driven purchasing — using comparison tools, buying secondhand, switching to own-brand and discount retailers, planning meals to reduce waste — is not a temporary emergency measure. It is a set of behaviours that households are consciously adopting and many will maintain even when finances improve.What This Means for Households, Brands, and the Economy

For households

The data is clear: the households most likely to navigate 2026 successfully are those that approach spending cuts strategically rather than reactively. A deliberate recalibration — identifying which discretionary spending delivers genuine value and satisfaction and which has become habit, cutting the latter, protecting the former — is more financially sustainable and psychologically healthier than undifferentiated austerity. The 51% of UK adults now budgeting are, in large part, already doing this.Practical implications for households managing discretionary spending in 2026

- Audit your subscriptions now: The 39% of worse-off households cutting subscriptions are responding to one of the fastest, most controllable sources of saving. Check every direct debit and standing order — an annual subscription audit typically reveals £30–£80 of monthly spending that can be painlessly reduced.

- Trade down in eating out, not out of it entirely: Cutting restaurants in favour of pubs, pubs in favour of home cooking, or full restaurant meals in favour of breakfast or lunch visits instead of dinner, preserves the social and experiential value of eating out at meaningfully lower cost.

- Protect genuinely high-value experiences: The consistent message from consumer research is that experiences — holidays, concerts, festivals — generate more satisfaction and lasting value than equivalent goods spending. If you are making cuts, goods and convenience spending are better candidates than experiences that you will value for much longer.

- Use the subscription-cancellation habit to build a savings habit: Every subscription you cancel creates a direct debit slot and a monthly cash flow that can be redirected to savings. Set up an automatic transfer to a savings account on the same day as the cancelled direct debit to convert the saving into a productive habit.

- Buy secondhand for fashion and high-value goods: 21% of UK consumers plan to buy more secondhand in 2026. Vinted, eBay, and Facebook Marketplace offer excellent quality at 40–80% below retail prices for clothing, electronics, and household goods. For fashion in particular, secondhand is increasingly the first choice rather than a fallback.

For brands and consumer businesses

The shift from consumption-led to value-led spending creates specific winners and losers. Value-led retailers (Aldi, Lidl, discount fashion), secondhand platforms (Vinted, Depop), and experience businesses with clear value propositions (budget travel, pubs, festivals at accessible price points) are better positioned than premium or convenience-led businesses whose pricing is under pressure from household recalibration. KPMG's Linda Ellett's observation that 'competition among consumer businesses for the remaining share of available consumer spend will be fierce' captures the strategic challenge accurately.For the economy

The Deloitte finding that discretionary spending has fallen to its lowest level since Q1 2023 — and the sharp fall in consumer confidence in the UK economy to -69% — suggests that the hoped-for consumer recovery has been delayed rather than cancelled. The Iran conflict's impact on energy prices in early 2026 has reset the inflation trajectory upward and reinjected uncertainty into household financial planning. The structural recalibration of consumer spending habits — more saving, more secondhand, more intentional purchasing — represents a lasting change in UK consumer behaviour that will shape the retail and hospitality markets for years to come.CONCLUSION

The YouGov data on UK discretionary spending cuts for 2026 describes a consumer population that is managing its money with more deliberation, more discipline, and more intentionality than at any point in recent memory. The 62% cutting eating out, the 52% cutting fashion, the 39% cutting subscriptions, and even the 33% cutting groceries are not signs of a consumer collapse — they are signs of a systematic repriorisation of spending that has been forced by five years of cost of living pressure and is now becoming embedded in household financial behaviour.The framing of 'recalibration, not retreat' is borne out by the data. Households are protecting experiences, rebuilding savings, shifting to secondhand and value-led purchasing, and cutting habitual or low-value spending rather than retreating from the economy entirely. The 13% who are not cutting anything — and the 22% expecting to improve — are the growth segment that consumer businesses are competing for. But even that group is, in 63% of cases, not planning to increase spending anywhere. The era of effortless consumer growth, if it ever truly existed, has not returned to the UK in 2026.

Frequently Asked Questions

What is the source of the spending cuts data?

The primary data source is YouGov's UK Financial Outlook 2026 survey, conducted online with 2,087 nationally representative UK adults between 6 and 9 February 2026. Data was weighted by age, gender, education, region, and social grade to be representative of all adults in Great Britain aged 16 and over. The survey asked respondents who expected their finances to worsen, improve, or stay the same in 2026 to identify which spending categories they planned to cut or increase. The full article is published at yougov.com.Why is eating out the biggest spending cut at 62%?

Eating out is the most common cut because it combines the highest flexibility (it is entirely optional), the clearest emotional driver (it feels indulgent when money is tight), and the most visible cost-saving mechanism (cooking at home is an immediately accessible alternative). It also reflects a structural shift in UK hospitality: as average restaurant meal prices have risen significantly since 2020 due to food price inflation, minimum wage increases, and energy costs, the price-to-value calculation for eating out has deteriorated for many households. Deloitte's Q1 2026 Consumer Tracker confirmed that restaurant demand remained weak while pub trading outperformed — consistent with households trading down to more affordable social eating occasions.Why are even households expecting to be better off cutting some spending?

YouGov's data shows that 44% of the better-off group are also cutting eating and drinking out, and 28% are cutting fashion. This reflects two separate phenomena. First, some of the 'better-off' group's improvement is modest — they may be slightly less financially pressured than before, but not comfortable enough to return to pre-crisis spending patterns. Second, and more importantly, there appears to be a genuine attitudinal shift among all income groups toward more intentional spending — the recalibration dynamic described throughout this article. KPMG's finding that 57% of all consumers would use a £5,000 windfall to save or pay down debt rather than spend it captures this across income levels.What spending is being protected or increased?

Across multiple datasets, the consistently protected or increased spending category is experiences — particularly holidays (Nationwide found travel is the top priority for 2026 spending among those who can afford it), concerts and festivals, and wellness activities. RSM found health and beauty seeing growing planned spend, particularly among Gen Z. KPMG found that among those planning to spend, 25% plan to spend on holidays in Q1 2026 and that holidays are the top aspiration if discretionary budget increases. The experiences-over-goods shift, already a pre-pandemic trend, has been reinforced by the cost of living crisis.Is this a crisis or just normal adjustment?

The data supports the recalibration framing rather than the crisis framing for most households. A genuine crisis would be characterised by cutting essentials out of necessity, depleting all savings, and accumulating unsustainable debt — all of which were more prevalent during the 2022 to 2023 inflation peak. The 2026 pattern — cutting discretionary spending while protecting experiences, building emergency savings, and buying secondhand — is characteristic of financially aware households making deliberate trade-offs rather than desperate ones. However, for the households in the most financially pressured segment — those cutting groceries, housing costs, and health and beauty — the crisis framing remains appropriate.What should I do if I am in the 36% expecting to be worse off?

Start with an audit rather than a panic. Write down all your fixed monthly outgoings and compare them to the spending categories in the YouGov data. The most immediately actionable savings are subscriptions (cancel unused ones), eating out (reduce frequency rather than eliminate entirely), and supermarket switching or own-brand switching for groceries. For the medium term, check your full benefit entitlement at turn2us.org.uk, review all bills for switching opportunities, and seek free budgeting advice from MoneyHelper at moneyhelper.org.uk. The 51% of UK adults now budgeting have found that the process itself — of understanding where money goes — typically identifies savings that were not previously visible.References

YouGov — UK Financial Outlook 2026: Consumer Spending Trends, Budgeting Habits and Financial Expectations (February 2026) https://yougov.com/en-gb/articles/54168-uk-financial-outlook-2026-consumer-spending-trends-budgeting-habits-and-financial-expectationsDeloitte — The Deloitte Consumer Tracker Q1 2026 (March 2026) https://www.deloitte.com/uk/en/Industries/consumer/research/consumer-tracker.html

KPMG UK — Cautious Consumer Landscape Continues into 2026 (December 2025) https://kpmg.com/uk/en/media/press-releases/2025/12/cautious-consumer-landscape-continues.html

RSM UK — Consumer Outlook 2026 https://www.rsmuk.com/insights/consumer-outlook

Nationwide — 2026 Spending Trends: Consumers Splash Out on Holidays and Wellness (January 2026) https://www.nationwide.co.uk/media/news/2026-spending-trends-consumers-splash-out-on-holidays-concerts-and-wellness-but-rising-costs-put-big-purchases-on-ice

Consumer Edge — UK Consumers Already Pulling Back on Discretionary Spend (April 2026) https://www.consumeredge.com/resources/insights/data-suggests-uk-consumers-are-already-pulling-back-on-discretionary-spend/

Chad.co.uk / Moneybox — Brits to Slash Spending in 2026, Axing Takeaways and Subscriptions (December 2025) https://www.chad.co.uk/read-this/brits-to-slash-spending-in-2026-axing-takeaways-subscriptions-and-nights-out-5453529

House of Commons Library — High Cost of Living: Impact on Households (January 2026) https://researchbriefings.files.parliament.uk/documents/CBP-10100/CBP-10100.pdf

MoneyHelper — Free Budgeting Tools and Guidance https://www.moneyhelper.org.uk

Turn2Us — Benefits Entitlement Calculator https://www.turn2us.org.uk

0 Comments Comments