Savings

U.S. High-Yield Savings Accounts 2026: Best Rates

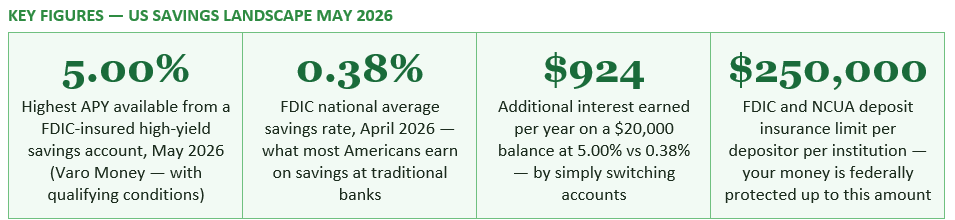

The best high-yield savings accounts in the US are paying up to 5.00% APY in May 2026 — more than 13 times the FDIC national average of 0.38%. On a $20,000 emergency fund, the difference between the average and the best is worth over $900 per year. This is the complete, up-to-date guide to the best US high-yield savings accounts, how to choose the right one, how FDIC protection works, and how to build a savings strategy that keeps your money working as hard as possible.

The rate environment changed dramatically from 2022 onwards. The Federal Reserve raised the federal funds rate from near zero in early 2022 to a peak of 5.25% to 5.50% by July 2023 in the fastest rate-tightening cycle in four decades. Although the Fed subsequently cut rates three times in late 2025, the federal funds rate remains in the 4.25% to 4.50% range as of May 2026 — still historically high. And the competitive market among online banks, fintech platforms, and credit unions has produced savings rates that substantially exceed the Fed's benchmark, with the best accounts paying 5.00% APY.

The practical significance is enormous. The FDIC reports the national average savings rate across all US institutions at 0.38% APY as of April 2026. The best high-yield savings accounts are paying more than 13 times this average. The majority of traditional bank customers — at JPMorgan Chase, Bank of America, and US Bank, which pay just 0.01% APY on their standard savings accounts — are earning essentially nothing on cash that could be generating real, meaningful returns. As US News reported, storing $1,000 in a 0.01% account earns precisely ten cents per year. The same $1,000 in a 5.00% account earns $50.

The best high-yield savings accounts are hitting rates up to 5.00% APY as of May 2026 — and that's genuinely impressive compared to the FDIC's recorded national average of 0.38%. For anyone trying to get real returns on their savings, the difference is substantial.

— FORTUNE — TOP HIGH-YIELD SAVINGS RATES MAY 2026

Calculations based on FDIC national average of 0.38% APY (April 2026) and best available HYSA rate of 5.00% APY (Varo Money, May 2026). Interest is illustrative for one year; actual earnings depend on rate changes during the period.

The table makes the cost of inertia concrete and unavoidable. A family with a $20,000 emergency fund at a traditional bank earning 0.38% is losing $924 per year compared to the best available rate — for doing nothing other than opening a different account. Over five years with no rate changes, that is $4,620 in forgone interest on the same money. The account opening process takes approximately 10 to 15 minutes. The return on that investment is extraordinarily high.

APY differs from the stated interest rate (sometimes called the nominal rate or daily periodic rate) because it accounts for compounding frequency. A savings account that pays 4.88% nominal interest compounded daily will have an APY of approximately 5.00%, because the daily compounding means each day's interest begins earning interest itself. By requiring all depository institutions to disclose APY, federal regulation ensures that you can compare accounts on a like-for-like basis regardless of how frequently they compound.

The practical rule is simple: always compare APYs, never nominal rates. A bank advertising a 4.80% rate compounded monthly is paying a lower effective yield than one advertising 4.75% compounded daily. The APY calculation already handles this difference, so using APY for all comparisons gives you the correct answer without needing to do any additional maths.

One important caveat: some accounts advertise rates that include a promotional or introductory period after which the rate drops, or rates that require meeting specific conditions (direct deposit, minimum balance, debit card usage) to earn the stated APY. Always read the small print for any account — particularly the top-paying ones — to understand what is required to earn the advertised rate and what the rate reverts to if you do not meet those requirements.

The mechanism is direct: when the Fed raises the federal funds rate, the cost of borrowing for banks increases. Banks pass this cost to borrowers (higher loan rates) and, to attract deposits, also raise savings rates. When the Fed cuts rates, savings rates typically follow downward within weeks or months.

The current rate environment is a product of the most dramatic rate cycle in modern US history. The Fed held rates near zero from March 2020 to March 2022, then raised them in eleven consecutive increases to 5.25% to 5.50% by July 2023 — the highest level since 2001. Three cuts in late 2025 brought the federal funds rate to 4.25% to 4.50%, where it remained as of May 2026. This still-elevated rate environment is what keeps HYSA rates in the 4% to 5% range. CBS News financial analyst Menard notes that 'given the uncertainty the Iran War has brought into the market, with prices peaking, rates could possibly go down from where they are today.' Savers should therefore consider locking in rates on CDs where appropriate, while maintaining flexibility in their liquid savings accounts.

The critical insight for savers is that HYSA rates are variable — they move with the federal funds rate and with individual bank competitive decisions. The 5.00% APY available today is not guaranteed to be available next month. This is why the standard advice from financial planners is to save at the highest available variable rate for liquid funds you need accessible, while using CDs to lock in rates on money you can commit for a fixed term.

Sources: Bankrate (May 12–13, 2026), NerdWallet (May 15, 2026), Fortune (May 13, 2026), CBS News, Motley Fool (May 12–13, 2026). APYs are variable and change frequently — always verify current rates at provider websites before opening an account.

A high-yield savings account is liquid — you can access your money at any time, with no penalty for withdrawal (though most accounts limit certain types of transfers to six per month). The rate is variable: it can change at any time, with or without advance notice, in response to Federal Reserve decisions and competitive market dynamics. When rates are expected to fall, HYSAs become less attractive for new money relative to locking in today's rate.

A certificate of deposit locks your money for a specified term — typically three months to five years — in exchange for a guaranteed, fixed interest rate for the full term. If you withdraw early, you pay a penalty (typically 60 to 180 days of interest, depending on the term). CDs are ideal for money you are confident you will not need during the fixed period and for periods when you expect savings rates to fall — locking in today's rate before a Fed cut.

The practical guidance for most savers in May 2026 is to keep the emergency fund (typically three to six months of living expenses) in a high-yield savings account for full liquidity, and to consider a 12-month CD for any additional savings that will not be needed for at least a year. A CD ladder — opening several CDs with staggered maturity dates (one, two, three, and four years) — provides both the rate security of fixed terms and regular liquidity as each CD matures.

Money market accounts typically come with additional features that standard savings accounts do not: a debit card for direct purchases, check-writing privileges, and in some cases ATM access. This makes them slightly more flexible than HYSAs for day-to-day access to funds. However, this flexibility comes at a cost: money market accounts typically pay slightly lower rates than the best HYSAs, and some require higher minimum balances to avoid fees or earn the advertised rate.

For most savers building an emergency fund or accumulating short-term savings, a high-yield savings account is the better choice — it offers the highest available rate with full liquidity via electronic transfer, and the slight reduction in instant accessibility (no debit card) is not a practical concern for the vast majority of emergency fund use cases. If you want the flexibility to write a check or swipe a card directly from your high-balance savings, a money market account may be worth the marginal rate trade-off. Synchrony Bank's High-Yield Savings includes an optional ATM card, giving it some of the accessibility of a money market account while retaining the savings account rate.

The Federal Deposit Insurance Corporation (FDIC) insures deposits at FDIC-member banks up to $250,000 per depositor, per insured bank, for each account ownership category. The National Credit Union Administration (NCUA) provides equivalent protection for deposits at federally insured credit unions. This means that if your bank fails — an event that has happened to hundreds of US banks over the past decade, most recently several regional banks in 2023 — the US government guarantees the return of your deposits up to $250,000 within days.

A practical four-tier framework for a US saver with $30,000 in total savings works as follows. The first tier — an emergency fund of approximately $12,000 (three months of average US household expenses) — goes into the highest-available-rate HYSA with no qualifying conditions or minimum balance requirements: Capital One 360 Performance Savings or Ally Bank at ~3.40% to 3.60% APY. This fund is always liquid, always accessible within one to three business days by electronic transfer, and earns a rate well above any traditional bank.

The second tier — approximately $8,000 earmarked for a near-term goal such as a car, home improvement, or vacation within 12 months — goes into a 12-month CD at the best available rate (approximately 4.20% in May 2026). The fixed rate is guaranteed, the term matches the goal timeline, and the slight illiquidity is acceptable because the goal has a known date.

The third tier — $8,000 committed for 24 months — goes into a 24-month CD at a slightly lower rate (typically 4.00% to 4.10%). The fourth tier — $2,000 available for the highest-rate account requiring qualifying conditions, such as Varo at 5.00% if you can meet the direct deposit requirements — earns the maximum rate on a smaller, more actively managed balance.

As each CD matures, the decision is whether to reinvest at the prevailing rate (if rates are still high or rising) or to move the proceeds into the HYSA if rates have fallen enough to make liquidity preferable. This framework never leaves emergency funds inaccessible, never misses the best available rate on committed money, and never requires complex ongoing management.

The tax is calculated at your marginal federal income tax rate — the rate that applies to your highest dollar of income. For most American households, this is 22% (taxable income $47,151 to $100,525 for single filers in 2025) or 24% ($100,526 to $191,950). On $2,000 of savings interest, a 22% federal rate means $440 in federal tax — reducing a 5.00% gross APY to approximately 3.90% after federal tax. State taxes reduce this further if you live in a state with income tax.

The practical implication is that for savers in higher tax brackets (32% to 37%), the after-tax return on a HYSA may be less competitive than alternatives including I-Bonds (US Treasury inflation-protected savings bonds, with federal tax deferred until redemption and no state tax), municipal bond funds (interest often exempt from federal and sometimes state tax), or HSAs and 401(k) plans (tax-deferred or tax-free growth on contributions). For most savers in the 22% to 24% bracket, the after-tax HYSA return still substantially exceeds the national average savings rate, making it the right default choice for the emergency fund and other liquid savings goals.

The stability-over-status framework — the growing US movement toward financial security, debt freedom, and resilience — finds one of its most direct expressions in high-yield savings. Building a fully-funded emergency fund in a 4% to 5% HYSA is not just financially prudent; it is the foundation that makes every other financial goal — debt freedom, retirement saving, investment — more achievable. Without an emergency fund, every unexpected expense sends you into debt. With one, you have the financial buffer that enables long-term wealth building. Open the account. Fund it consistently. And review the rate quarterly to ensure your money continues to work as hard as possible.

NerdWallet — Best High-Yield Savings Accounts of May 2026: Up to 4.03% (updated May 15, 2026) https://www.nerdwallet.com/banking/best/high-yield-online-savings-accounts

Fortune — Top High-Yield Savings Rates May 13, 2026: Up to 5.00% APY https://fortune.com/article/best-savings-account-rates-5-13-2026/

CBS News — Best High-Yield Savings Accounts: Top Rates and Picks May 2026 https://www.cbsnews.com/news/best-high-yield-savings-account/

US News Money — Best High-Yield Savings Accounts 2026: Top 10 Rates and Perks https://www.usnews.com/banking/high-yield-savings-accounts

The Motley Fool — Best High-Yield Savings Accounts Today May 13, 2026: Up to 5.00% APY https://www.fool.com/money/banks/articles/top-savings-account-rates-today-may-13-2026/

FDIC — National Rates and Rate Caps: Savings Accounts (April 20, 2026) https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/banklist.html

FDIC — BankFind: FDIC-Insured Institution Lookup https://banks.data.fdic.gov/

IRS — Topic No. 403: Interest Received (Taxation of Savings Interest) https://www.irs.gov/taxtopics/tc403

Consumer Financial Protection Bureau — Savings Account Basics https://www.consumerfinance.gov/consumer-tools/savings/

TABLE OF CONTENTS

- Why High-Yield Savings Accounts Matter More Than Ever

- The Rate Gap: What You Are Losing by Staying Put

- Understanding APY: The One Number That Matters

- How the Federal Reserve Affects Your Savings Rate

- The Best US High-Yield Savings Accounts: May 2026

- Account Deep-Dives: The Top Five Picks

- High-Yield Savings vs CDs: Which Is Right for You?

- HYSA vs Money Market Accounts: The Key Differences

- How FDIC and NCUA Insurance Protects Your Savings

- The Most Common Mistakes US Savers Make

- How to Build a Savings Ladder for Every Goal

- Taxes on Savings Interest: What You Need to Know

- How to Open a High-Yield Savings Account: Step-by-Step

- Conclusion

- Frequently Asked Questions

- References

Why High-Yield Savings Accounts Matter More Than Ever

For much of the period between 2008 and 2022, savings accounts in the United States paid virtually nothing. The Federal Reserve's near-zero interest rate policy — intended to stimulate economic growth following the 2008 financial crisis and again during the COVID-19 pandemic — pushed the national average savings rate below 0.10%. Americans who dutifully set money aside in their bank's savings account were watching inflation quietly erode its real value while earning interest measured in pennies per year.The rate environment changed dramatically from 2022 onwards. The Federal Reserve raised the federal funds rate from near zero in early 2022 to a peak of 5.25% to 5.50% by July 2023 in the fastest rate-tightening cycle in four decades. Although the Fed subsequently cut rates three times in late 2025, the federal funds rate remains in the 4.25% to 4.50% range as of May 2026 — still historically high. And the competitive market among online banks, fintech platforms, and credit unions has produced savings rates that substantially exceed the Fed's benchmark, with the best accounts paying 5.00% APY.

The practical significance is enormous. The FDIC reports the national average savings rate across all US institutions at 0.38% APY as of April 2026. The best high-yield savings accounts are paying more than 13 times this average. The majority of traditional bank customers — at JPMorgan Chase, Bank of America, and US Bank, which pay just 0.01% APY on their standard savings accounts — are earning essentially nothing on cash that could be generating real, meaningful returns. As US News reported, storing $1,000 in a 0.01% account earns precisely ten cents per year. The same $1,000 in a 5.00% account earns $50.

The best high-yield savings accounts are hitting rates up to 5.00% APY as of May 2026 — and that's genuinely impressive compared to the FDIC's recorded national average of 0.38%. For anyone trying to get real returns on their savings, the difference is substantial.

— FORTUNE — TOP HIGH-YIELD SAVINGS RATES MAY 2026

The Rate Gap: What You Are Losing by Staying Put

The gap between the national average and the best available rate is not a rounding error. On a meaningful savings balance, it represents hundreds or thousands of dollars per year in forgone interest — money that is simply not being earned because of the inertia of staying with a traditional bank's default savings product.Calculations based on FDIC national average of 0.38% APY (April 2026) and best available HYSA rate of 5.00% APY (Varo Money, May 2026). Interest is illustrative for one year; actual earnings depend on rate changes during the period.

The table makes the cost of inertia concrete and unavoidable. A family with a $20,000 emergency fund at a traditional bank earning 0.38% is losing $924 per year compared to the best available rate — for doing nothing other than opening a different account. Over five years with no rate changes, that is $4,620 in forgone interest on the same money. The account opening process takes approximately 10 to 15 minutes. The return on that investment is extraordinarily high.

Understanding APY: The One Number That Matters

When comparing savings accounts, one number matters above all others: the APY, or Annual Percentage Yield. APY is the standardised measure of the interest you will earn over a full year, taking into account the effect of compounding — the process by which interest earned is added to your balance and then itself earns interest.APY differs from the stated interest rate (sometimes called the nominal rate or daily periodic rate) because it accounts for compounding frequency. A savings account that pays 4.88% nominal interest compounded daily will have an APY of approximately 5.00%, because the daily compounding means each day's interest begins earning interest itself. By requiring all depository institutions to disclose APY, federal regulation ensures that you can compare accounts on a like-for-like basis regardless of how frequently they compound.

The practical rule is simple: always compare APYs, never nominal rates. A bank advertising a 4.80% rate compounded monthly is paying a lower effective yield than one advertising 4.75% compounded daily. The APY calculation already handles this difference, so using APY for all comparisons gives you the correct answer without needing to do any additional maths.

One important caveat: some accounts advertise rates that include a promotional or introductory period after which the rate drops, or rates that require meeting specific conditions (direct deposit, minimum balance, debit card usage) to earn the stated APY. Always read the small print for any account — particularly the top-paying ones — to understand what is required to earn the advertised rate and what the rate reverts to if you do not meet those requirements.

How the Federal Reserve Affects Your Savings Rate

The federal funds rate — the interest rate at which banks lend to each other overnight — is set by the Federal Reserve's Federal Open Market Committee (FOMC) at meetings held approximately every six weeks. It is the benchmark rate that anchors all US interest rates, including those on savings accounts, mortgages, car loans, and credit cards.The mechanism is direct: when the Fed raises the federal funds rate, the cost of borrowing for banks increases. Banks pass this cost to borrowers (higher loan rates) and, to attract deposits, also raise savings rates. When the Fed cuts rates, savings rates typically follow downward within weeks or months.

The current rate environment is a product of the most dramatic rate cycle in modern US history. The Fed held rates near zero from March 2020 to March 2022, then raised them in eleven consecutive increases to 5.25% to 5.50% by July 2023 — the highest level since 2001. Three cuts in late 2025 brought the federal funds rate to 4.25% to 4.50%, where it remained as of May 2026. This still-elevated rate environment is what keeps HYSA rates in the 4% to 5% range. CBS News financial analyst Menard notes that 'given the uncertainty the Iran War has brought into the market, with prices peaking, rates could possibly go down from where they are today.' Savers should therefore consider locking in rates on CDs where appropriate, while maintaining flexibility in their liquid savings accounts.

The critical insight for savers is that HYSA rates are variable — they move with the federal funds rate and with individual bank competitive decisions. The 5.00% APY available today is not guaranteed to be available next month. This is why the standard advice from financial planners is to save at the highest available variable rate for liquid funds you need accessible, while using CDs to lock in rates on money you can commit for a fixed term.

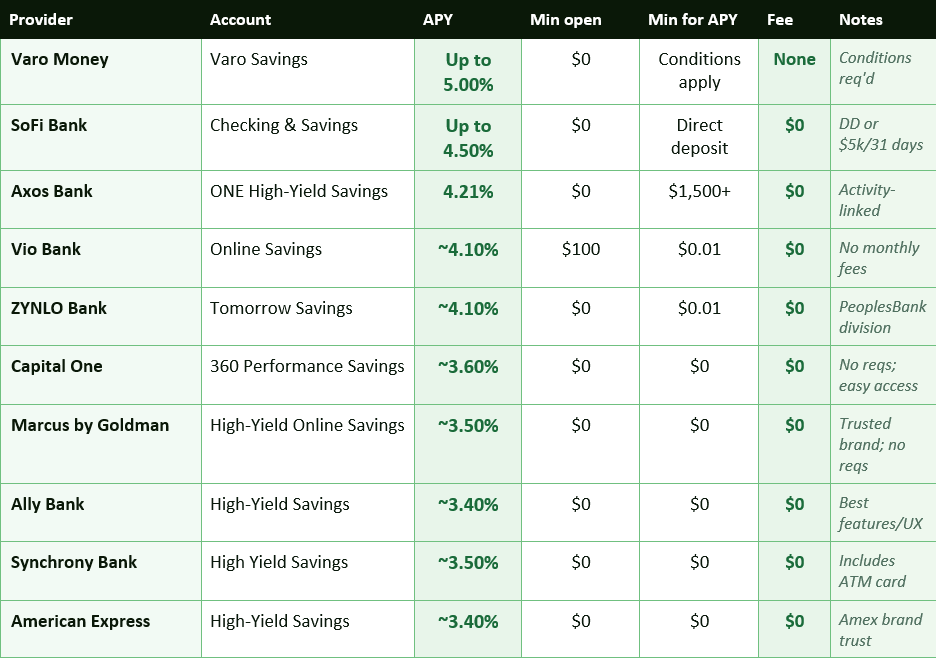

The Best US High-Yield Savings Accounts: May 2026

The following table presents the best-paying FDIC or NCUA-insured high-yield savings accounts as of mid-May 2026, based on Bankrate (updated 12–13 May 2026), NerdWallet (15 May 2026), Fortune (13 May 2026), CBS News, and Motley Fool current data.Sources: Bankrate (May 12–13, 2026), NerdWallet (May 15, 2026), Fortune (May 13, 2026), CBS News, Motley Fool (May 12–13, 2026). APYs are variable and change frequently — always verify current rates at provider websites before opening an account.

Account Deep-Dives: The Top Five Picks

Varo Money — Up to 5.00% APY

Varo Money offers the highest APY currently available among FDIC-insured savings accounts, at up to 5.00%. To earn the maximum rate, Varo requires qualifying conditions including receiving monthly direct deposits totalling at least $1,000 and maintaining a positive balance in both your Varo Bank Account and Varo Savings Account. Balances above a certain cap earn a lower baseline rate. Varo is a fully mobile, app-based bank — there are no branches and the product is managed entirely through the app. It is FDIC-insured through The Bancorp Bank. For savers who can meet the qualifying conditions and are comfortable with an app-only bank, the 5.00% rate represents the best FDIC-insured return on liquid savings available in the US market in May 2026.SoFi Bank — Up to 4.50% APY

SoFi won NerdWallet's annual award for best overall bank in 2026. Its Checking and Savings product combines a checking and savings account with a competitive APY. The standard rate for members with qualifying direct deposits is 3.30% APY. Members who also qualify for SoFi Plus membership or meet higher deposit thresholds can earn a boosted rate of up to 4.50% APY for a promotional period, according to Fortune's May 2026 analysis. SoFi also offers a bonus of $50 to $300 for new customers setting up eligible direct deposits. It is FDIC-insured through SoFi Bank, N.A. The combination of a strong rate, no minimum balance, no monthly fees, and multiple additional financial products (student loan refinancing, personal loans, investing) makes SoFi one of the most compelling all-in-one financial platforms for younger savers.Axos Bank ONE Bundle — 4.21% APY

CBS News identifies Axos Bank's ONE bundle as the account with the highest APY on its curated list at 4.21%. The rate is activity-linked — it requires engagement with Axos's broader product suite to earn the full rate. Axos is an established FDIC-insured online bank with a strong track record and a $1,500 minimum balance to earn the top rate. For savers already using or willing to use Axos's other products, the rate is highly competitive.Capital One 360 Performance Savings — ~3.60% APY

Capital One 360 Performance Savings is the recommendation for savers who want a strong rate without any qualifying conditions, minimum balances, or activity requirements. The same rate applies to all balances, there are no monthly fees, and Capital One has over 200 physical branch locations — an unusual feature for an online savings account that provides reassurance to savers who occasionally want in-person banking access. NerdWallet consistently rates it as one of the best accounts for straightforward, no-strings high-yield savings.Ally Bank High-Yield Savings — ~3.40% APY

Ally Bank consistently receives the highest ratings for user experience, customer service, and product features among online savings providers. The Ally High-Yield Savings account earns a competitive ~3.40% APY with no minimum balance, no monthly fees, and an industry-leading set of savings tools including 'savings buckets' (the ability to divide your account balance into separate labelled goals without opening multiple accounts), automatic savings rules, and comprehensive mobile banking. While its rate is below the very top of the market, the combination of rate, features, reliability, and customer satisfaction makes it the recommendation for savers who want the complete package rather than the maximum possible APY.High-Yield Savings vs CDs: Which Is Right for You?

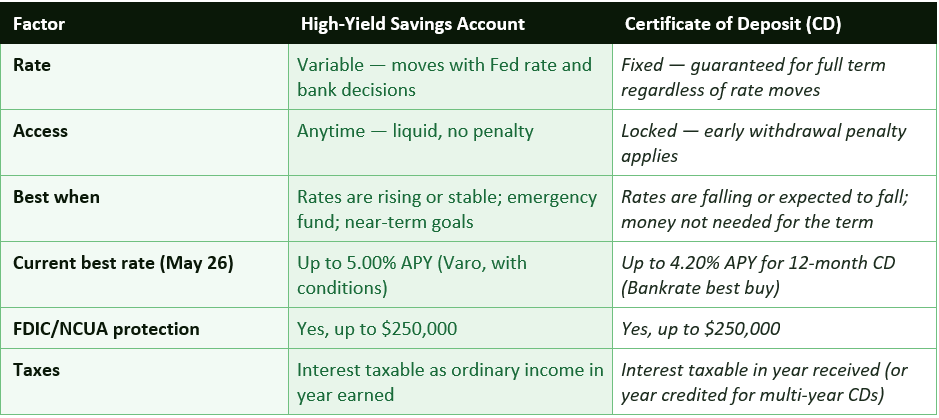

The two most common high-rate savings vehicles for US savers are high-yield savings accounts (HYSAs) and certificates of deposit (CDs). Understanding the trade-off between them is essential for optimising your savings strategy.A high-yield savings account is liquid — you can access your money at any time, with no penalty for withdrawal (though most accounts limit certain types of transfers to six per month). The rate is variable: it can change at any time, with or without advance notice, in response to Federal Reserve decisions and competitive market dynamics. When rates are expected to fall, HYSAs become less attractive for new money relative to locking in today's rate.

A certificate of deposit locks your money for a specified term — typically three months to five years — in exchange for a guaranteed, fixed interest rate for the full term. If you withdraw early, you pay a penalty (typically 60 to 180 days of interest, depending on the term). CDs are ideal for money you are confident you will not need during the fixed period and for periods when you expect savings rates to fall — locking in today's rate before a Fed cut.

The practical guidance for most savers in May 2026 is to keep the emergency fund (typically three to six months of living expenses) in a high-yield savings account for full liquidity, and to consider a 12-month CD for any additional savings that will not be needed for at least a year. A CD ladder — opening several CDs with staggered maturity dates (one, two, three, and four years) — provides both the rate security of fixed terms and regular liquidity as each CD matures.

HYSA vs Money Market Accounts: The Key Differences

Money market accounts (MMAs) are often confused with high-yield savings accounts because they share similar characteristics: both are FDIC-insured deposit accounts, both typically pay higher rates than traditional savings accounts, and both are offered by online banks. The key differences are practical ones.Money market accounts typically come with additional features that standard savings accounts do not: a debit card for direct purchases, check-writing privileges, and in some cases ATM access. This makes them slightly more flexible than HYSAs for day-to-day access to funds. However, this flexibility comes at a cost: money market accounts typically pay slightly lower rates than the best HYSAs, and some require higher minimum balances to avoid fees or earn the advertised rate.

For most savers building an emergency fund or accumulating short-term savings, a high-yield savings account is the better choice — it offers the highest available rate with full liquidity via electronic transfer, and the slight reduction in instant accessibility (no debit card) is not a practical concern for the vast majority of emergency fund use cases. If you want the flexibility to write a check or swipe a card directly from your high-balance savings, a money market account may be worth the marginal rate trade-off. Synchrony Bank's High-Yield Savings includes an optional ATM card, giving it some of the accessibility of a money market account while retaining the savings account rate.

How FDIC and NCUA Insurance Protects Your Savings

Federal deposit insurance is the single most important consumer protection in American banking. Understanding how it works ensures you never inadvertently leave savings unprotected.The Federal Deposit Insurance Corporation (FDIC) insures deposits at FDIC-member banks up to $250,000 per depositor, per insured bank, for each account ownership category. The National Credit Union Administration (NCUA) provides equivalent protection for deposits at federally insured credit unions. This means that if your bank fails — an event that has happened to hundreds of US banks over the past decade, most recently several regional banks in 2023 — the US government guarantees the return of your deposits up to $250,000 within days.

FDIC insurance — key rules for savers with larger balances

- The $250,000 limit applies per depositor, per institution, per account ownership category. A single depositor can hold more than $250,000 at FDIC-insured banks — but must spread it across multiple institutions or ownership categories to maintain full protection. At the same institution, a single depositor can hold up to $250,000 in individual accounts and up to $250,000 in joint accounts (for a combined $500,000 for a couple) with full FDIC protection.

- Joint accounts are protected separately from individual accounts. A couple with $250,000 each in individual accounts at the same bank, plus a $500,000 joint account, has $1,000,000 in FDIC-protected deposits at that bank (individual limits apply per owner, joint limit applies per co-owner).

- All deposits at the same FDIC-insured institution are combined for coverage purposes. If you have a checking account, a savings account, and a CD at the same bank, all three are added together for your $250,000 individual account limit.

- Fintech platforms and cash management accounts: Some fintech companies (including SoFi and Varo) offer FDIC insurance through partner banks. This protection is genuine and legally sound, but verify the specific FDIC partner bank and check that you are not also holding deposits at that partner bank directly (which would count toward the same $250,000 limit).

- Not FDID-insured: Money market mutual funds (which are different from money market deposit accounts), US Treasury securities, and brokerage accounts are not FDIC-insured — though T-bills have the full faith and credit of the US government as a separate guarantee.

The Most Common Mistakes US Savers Make

Six savings mistakes that cost Americans hundreds per year

- Leaving money in a big bank's 0.01% savings account: JPMorgan Chase, Bank of America, and US Bank all pay 0.01% APY on their standard savings accounts. On $10,000, that earns $1 per year. Moving to a 4.00%+ HYSA at an online bank earns $400 per year on the same money. The account opening takes 15 minutes. There is no rational argument for leaving money in a 0.01% account when 4.00%+ alternatives are one application away.

- Confusing a promotional rate with the ongoing rate: Some HYSAs advertise headline rates that include a bonus for a limited period (3 to 12 months) after which the rate drops significantly. Always check the ongoing rate — the rate after any promotional period expires — before making a decision. If the ongoing rate is materially lower than the headline, factor that into your comparison.

- Not meeting qualifying conditions for top-rate accounts: Accounts paying 5.00% APY often require specific actions — a minimum direct deposit amount, a debit card purchase threshold, or a minimum balance in a linked checking account. If you open an account at the top rate but fail to meet the qualifying conditions, you earn the much lower fallback rate and may not notice for months. Read the requirements before opening and set up the qualifying activity immediately.

- Failing to ladder CDs in a falling-rate environment: If the Federal Reserve is expected to cut rates further in 2026, the right strategy is to lock in today's rates on CDs for any money you will not need. Staying in a variable-rate HYSA when rates are declining means your earnings fall with every Fed cut. A simple CD ladder (12-month, 24-month, and 36-month CDs opened simultaneously) captures today's rates on the longer-term tranches.

- Underestimating the tax on savings interest: Interest earned in a HYSA is ordinary income — taxable at your marginal federal rate in the year it is earned, even if you do not withdraw it. On $5,000 of interest at a 22% federal rate, the tax is $1,100. This does not make HYSAs a bad choice, but it means the after-tax return matters: a 5.00% APY at a 22% tax rate produces a 3.90% after-tax return. High earners (32% to 37% brackets) should compare HYSA after-tax returns against tax-advantaged alternatives (I-bonds, municipal bonds) for non-emergency funds.

- Not checking rates frequently enough: HYSA rates are variable and competitive. The best-rate provider in January may not be the best-rate provider in May. A quarterly rate review — comparing your current account's APY to the current Bankrate or NerdWallet best-buy table — takes five minutes and has caught meaningful rate changes. There is no penalty for switching HYSA providers, and many savers switch once or twice a year to stay at or near the top rate.

How to Build a Savings Ladder for Every Goal

A savings ladder allocates different pools of savings to different accounts based on when you need the money, maximising the return on each tranche without ever locking away funds you might need urgently.A practical four-tier framework for a US saver with $30,000 in total savings works as follows. The first tier — an emergency fund of approximately $12,000 (three months of average US household expenses) — goes into the highest-available-rate HYSA with no qualifying conditions or minimum balance requirements: Capital One 360 Performance Savings or Ally Bank at ~3.40% to 3.60% APY. This fund is always liquid, always accessible within one to three business days by electronic transfer, and earns a rate well above any traditional bank.

The second tier — approximately $8,000 earmarked for a near-term goal such as a car, home improvement, or vacation within 12 months — goes into a 12-month CD at the best available rate (approximately 4.20% in May 2026). The fixed rate is guaranteed, the term matches the goal timeline, and the slight illiquidity is acceptable because the goal has a known date.

The third tier — $8,000 committed for 24 months — goes into a 24-month CD at a slightly lower rate (typically 4.00% to 4.10%). The fourth tier — $2,000 available for the highest-rate account requiring qualifying conditions, such as Varo at 5.00% if you can meet the direct deposit requirements — earns the maximum rate on a smaller, more actively managed balance.

As each CD matures, the decision is whether to reinvest at the prevailing rate (if rates are still high or rising) or to move the proceeds into the HYSA if rates have fallen enough to make liquidity preferable. This framework never leaves emergency funds inaccessible, never misses the best available rate on committed money, and never requires complex ongoing management.

Taxes on Savings Interest: What You Need to Know

All interest earned in a US high-yield savings account is taxable as ordinary income in the year it is credited to your account — regardless of whether you withdraw it. Your bank will send you a Form 1099-INT at the beginning of the following year reporting all interest you earned during the calendar year. You are required to report this on your federal tax return (and most state returns, depending on your state's tax treatment of savings interest).The tax is calculated at your marginal federal income tax rate — the rate that applies to your highest dollar of income. For most American households, this is 22% (taxable income $47,151 to $100,525 for single filers in 2025) or 24% ($100,526 to $191,950). On $2,000 of savings interest, a 22% federal rate means $440 in federal tax — reducing a 5.00% gross APY to approximately 3.90% after federal tax. State taxes reduce this further if you live in a state with income tax.

The practical implication is that for savers in higher tax brackets (32% to 37%), the after-tax return on a HYSA may be less competitive than alternatives including I-Bonds (US Treasury inflation-protected savings bonds, with federal tax deferred until redemption and no state tax), municipal bond funds (interest often exempt from federal and sometimes state tax), or HSAs and 401(k) plans (tax-deferred or tax-free growth on contributions). For most savers in the 22% to 24% bracket, the after-tax HYSA return still substantially exceeds the national average savings rate, making it the right default choice for the emergency fund and other liquid savings goals.

How to Open a High-Yield Savings Account: Step-by-Step

- Compare current rates at Bankrate.com or NerdWallet.com — both update their HYSA best-buy tables daily. Identify two or three accounts that meet your criteria: minimum deposit you can meet, qualifying conditions you can satisfy, and no monthly fees. Note both the top rate and the ongoing rate after any promotional period.

- Check FDIC or NCUA insurance — confirm any account you are considering is covered. Look for the FDIC member seal on the bank's website, or search the FDIC's BankFind database at banks.data.fdic.gov. All accounts in this guide are FDIC or NCUA insured.

- Gather your documents — you will need a Social Security Number or Individual Taxpayer Identification Number, a valid government-issued ID (driver's licence or passport), your home address, and the routing and account numbers for your existing bank account (to fund the new account via electronic transfer).

- Apply online — all the accounts in this guide can be opened entirely online in 10 to 15 minutes. Navigate directly to the bank's own website, not through a comparison site, to ensure you are opening the correct account. Complete the application, verify your identity, and review the account terms before submitting.

- Fund the account — initiate an electronic transfer from your existing checking or savings account. Most HYSAs begin earning the full APY from the date the funds are deposited. Allow one to three business days for the transfer to complete.

- Set up qualifying conditions immediately — if your account requires a direct deposit or minimum monthly activity to earn the top rate, configure this before your first full month. Change your payroll direct deposit to the new account (or set up a qualifying transfer from an existing account if the bank accepts that as a qualifying deposit).

- Set a rate review reminder — calendar a reminder for 90 days from account opening to compare your current APY to the live Bankrate or NerdWallet best-buy table. HYSA rates change frequently; a regular review ensures you do not fall behind the best available rate.

CONCLUSION

The best high-yield savings accounts in the US are paying up to 5.00% APY in May 2026 — more than thirteen times the FDIC national average of 0.38%. On a $20,000 emergency fund, the difference is nearly $1,000 per year in additional interest earned on money that should already be working hard. The accounts are FDIC-insured, the application takes 15 minutes, there are no fees, and there is no risk of losing principal.The stability-over-status framework — the growing US movement toward financial security, debt freedom, and resilience — finds one of its most direct expressions in high-yield savings. Building a fully-funded emergency fund in a 4% to 5% HYSA is not just financially prudent; it is the foundation that makes every other financial goal — debt freedom, retirement saving, investment — more achievable. Without an emergency fund, every unexpected expense sends you into debt. With one, you have the financial buffer that enables long-term wealth building. Open the account. Fund it consistently. And review the rate quarterly to ensure your money continues to work as hard as possible.

Frequently Asked Questions

What is the best high-yield savings account rate in the US right now?

As of mid-May 2026, the highest advertised APY from a FDIC-insured savings account is up to 5.00% from Varo Money, which requires qualifying monthly direct deposits and a positive balance in linked accounts. Among accounts with no qualifying conditions, Capital One 360 Performance Savings and Ally Bank High-Yield Savings are paying approximately 3.40% to 3.60% APY, while SoFi offers up to 4.50% APY for direct deposit members. The FDIC national average for all US savings accounts is 0.38% APY (April 2026). Always check current rates at Bankrate.com or NerdWallet.com before opening an account, as rates change frequently.Are high-yield savings accounts safe?

Yes, provided the account is FDIC-insured (bank) or NCUA-insured (credit union). All accounts in this guide carry FDIC or NCUA insurance, which protects deposits up to $250,000 per depositor per insured institution. This means that even if the bank fails, the US government guarantees the return of your deposits up to $250,000. The FDIC has never failed to make depositors whole on an insured amount since its founding in 1933. Unlike the stock market, a HYSA balance does not fluctuate — the only risk to your principal is if the bank fails and your balance exceeds the $250,000 insurance limit at that institution.Why do online banks offer higher savings rates than traditional banks?

Online banks have fundamentally lower operating costs than traditional banks because they do not maintain branch networks, ATM fleets, or the large staffing levels required for in-person banking. A traditional bank with thousands of physical branches and tens of thousands of employees has enormous fixed costs to cover before it can pass any interest rate benefit to depositors. An online bank with no branches and a technology-driven model can operate on much lower margins and therefore offer dramatically higher deposit rates. Additionally, online banks often operate in a more competitive market where APY is the primary marketing tool — they compete for deposits almost entirely on rate, which drives rates upward. This structural difference is why JPMorgan Chase (0.01%) and Varo Money (5.00%) exist in the same market simultaneously.How do savings account rates change with Federal Reserve decisions?

The Federal Reserve sets the federal funds rate — the benchmark rate that anchors all US interest rates. When the Fed raises its rate (as it did eleven times from 2022 to 2023), banks typically raise savings rates to attract deposits and cover higher borrowing costs. When the Fed cuts rates (as it did three times in late 2025), savings rates typically follow downward within weeks. The federal funds rate was in the 4.25% to 4.50% range as of May 2026, which is why HYSA rates remain in the 3.40% to 5.00% range. If the Fed makes further cuts in 2026 — as some analysts expect given global economic uncertainty — HYSA rates may fall. Savers should consider opening CDs for money they can commit for a fixed term, to lock in today's rates before any future cuts.Do I have to pay tax on high-yield savings account interest?

Yes. Interest earned in a US high-yield savings account is taxable as ordinary income in the year it is earned, at your marginal federal income tax rate. Your bank will send you a Form 1099-INT in January of the following year reporting the interest you earned. You must report this on your federal and, in most states, state tax return. On $2,000 of interest at a 22% federal rate, the tax is approximately $440, reducing a 5.00% gross APY to approximately 3.90% after federal tax. You owe tax on the interest whether or not you withdraw it from the account. For savers in higher tax brackets, tax-advantaged alternatives (I-Bonds, municipal bonds) may be worth comparing for non-emergency, long-term savings.What is the difference between APY and interest rate?

APY (Annual Percentage Yield) is the annualised effective return on your savings, taking into account how often interest is compounded (added to your balance). The nominal interest rate is the simple rate before compounding is applied. A savings account paying 4.88% nominal interest compounded daily will have an APY of approximately 5.00%, because each day's interest begins earning interest itself. Federal law requires banks to disclose APY, making it the standardised comparison figure. Always compare APY figures when choosing between savings accounts — they account for compounding frequency and allow a true apples-to-apples comparison between accounts that pay interest daily, monthly, or quarterly.References

Bankrate — Best High-Yield Savings Accounts of May 2026: Up to 4.21% (updated May 12–13, 2026) https://www.bankrate.com/banking/savings/best-high-yield-interests-savings-accounts/NerdWallet — Best High-Yield Savings Accounts of May 2026: Up to 4.03% (updated May 15, 2026) https://www.nerdwallet.com/banking/best/high-yield-online-savings-accounts

Fortune — Top High-Yield Savings Rates May 13, 2026: Up to 5.00% APY https://fortune.com/article/best-savings-account-rates-5-13-2026/

CBS News — Best High-Yield Savings Accounts: Top Rates and Picks May 2026 https://www.cbsnews.com/news/best-high-yield-savings-account/

US News Money — Best High-Yield Savings Accounts 2026: Top 10 Rates and Perks https://www.usnews.com/banking/high-yield-savings-accounts

The Motley Fool — Best High-Yield Savings Accounts Today May 13, 2026: Up to 5.00% APY https://www.fool.com/money/banks/articles/top-savings-account-rates-today-may-13-2026/

FDIC — National Rates and Rate Caps: Savings Accounts (April 20, 2026) https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/banklist.html

FDIC — BankFind: FDIC-Insured Institution Lookup https://banks.data.fdic.gov/

IRS — Topic No. 403: Interest Received (Taxation of Savings Interest) https://www.irs.gov/taxtopics/tc403

Consumer Financial Protection Bureau — Savings Account Basics https://www.consumerfinance.gov/consumer-tools/savings/

0 Comments Comments