Investing

Why Savings Won't Make You Rich — But Investing Will

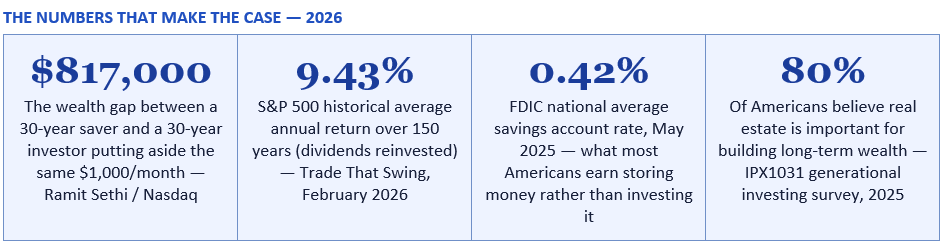

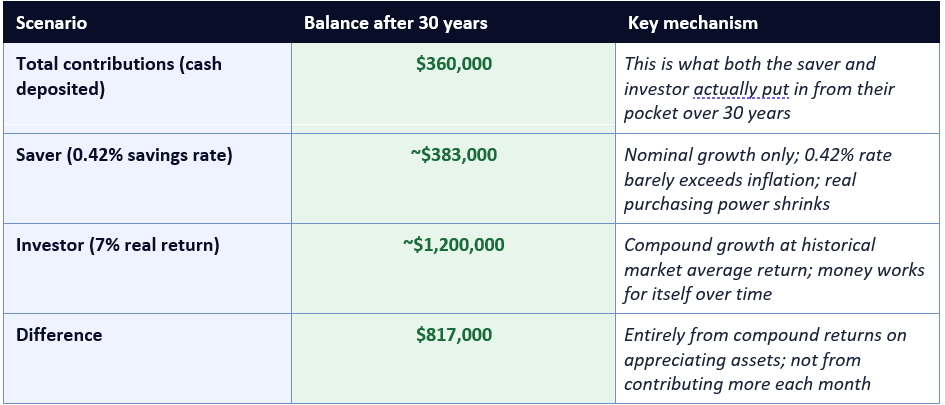

Someone who saves $1,000 per month for 30 years ends up with approximately $383,000. Someone who invests the same amount in assets that grow at the historical average ends up with approximately $1.2 million. Same discipline. Same monthly amount. Same 30 years. The $817,000 difference is not luck — it is the difference between storing money and putting money to work. Savings are the foundation. Investing in appreciating assets is how wealth is actually built.

Savings are not the enemy of wealth building — they are the necessary precondition for it. Without savings, there is no emergency fund to protect you when income stops unexpectedly. Without savings, there is no capital to deploy into investments. Without savings, every financial setback becomes a debt problem. The savings account, the high-yield savings account, the emergency fund in a money market — all of these serve a real and important purpose. The problem is not saving. The problem is confusing saving with wealth building.

Saving money and building wealth are two distinct activities with two distinct mechanisms. Saving is the act of not spending money — setting it aside in a form that is safe, accessible, and protected from loss. Its primary virtues are liquidity and capital preservation. Building wealth requires something else: putting capital into assets that generate returns over time, either through income (dividends, rent, interest) or through appreciation in value, or both. As Impact Wealth's January 2026 analysis states plainly: 'Saving money is essential, but it will not make you wealthy on its own. If your goal is to build substantial long-term wealth, investing consistently outperforms saving in nearly every measurable way.'

The practical implication is a sequencing question, not an either/or choice. Equity Bank's March 2026 guide frames it well: 'Rather than choosing one or the other, most people use a combination of both strategies. Savings protect what you cannot afford to lose, while investing helps you grow what you can set aside for the future.' The foundation — a three-to-six-month emergency fund in a high-yield savings account — comes first. Once that foundation is in place, every additional pound or dollar that goes into savings rather than investments is a missed opportunity to compound.

In concrete terms: £10,000 held in a standard savings account earning 0.42% per year for ten years grows to approximately £10,425 in nominal terms. But if inflation averages 2.5% over that period, the purchasing power of that £10,000 in today's terms is approximately £8,100 after ten years. The saver's nominal balance grew by £425. Their real wealth declined by approximately £1,900. The account statement shows growth; the actual financial position has deteriorated.

This is why the Dallas Federal Reserve defines investment so specifically: 'Investments increase by generating income (interest or dividends) or by growing (appreciating) in value. Income earned from your investments and any appreciation in the value of your investments increase your wealth.' The emphasis on appreciation in value is critical — not just nominal return, but real growth that outpaces inflation. Assets that appreciate in value over time are the mechanism through which wealth outpaces inflation and compounds toward financial independence.

The difference comes down to one fundamental principle: money that sits idle loses purchasing power over time, while money that works for you has the potential to grow exponentially.

— IMPACT WEALTH — WHY IS INVESTING A MORE POWERFUL TOOL TO BUILD LONG-TERM WEALTH THAN SAVING? (JANUARY 2026)

The saver deposits $1,000 per month into a standard savings account earning the FDIC national average of 0.42% per year (May 2025 FDIC data). After 30 years, they have accumulated approximately $383,000. This is genuinely good — $383,000 is a significant sum, earned through consistent discipline over three decades. But it represents only 7% more than the $360,000 they contributed in cash over 30 years. The savings account added almost nothing beyond the deposits themselves.

The investor commits the same $1,000 per month for 30 years but invests it in assets generating the historical average real return of 7% per year (after inflation). After 30 years, they have approximately $1.2 million. The investor has $817,000 more than the saver — for the same monthly commitment, the same time period, and the same discipline. The difference is entirely attributable to the power of compound returns on appreciating assets.

Source: Ramit Sethi / Nasdaq analysis; FDIC national average savings rate, May 2025. Based on $1,000/month contributions over 30 years. Historical investment return of 7% real (after inflation) is the long-run S&P 500 inflation-adjusted average per Trade That Swing (February 2026) and Optionality (March 2026). Past performance does not guarantee future results.

Appreciating assets share certain characteristics. They produce something of value — either directly (a property provides shelter, a business produces goods or services) or by entitling the holder to a share of something that does. They benefit from scarcity — their supply is constrained relative to demand over time (quality real estate in growing cities, shares in genuinely growing businesses). And they compound — the returns they generate can be reinvested to generate further returns, creating the exponential growth trajectory that makes long-term investing so powerful.

Depreciating assets — cars, most electronics, most physical consumer goods — lose value over time because they wear out, become obsolete, or face competitive alternatives that reduce their relative desirability. The key insight from IPX1031's 2025 survey is instructive: 80% of Americans understand at some level that real estate is important for building long-term wealth, while 58% believe the stock market provides better returns. Both intuitions are right. The most effective wealth-building portfolios typically include both.

The mechanism is compound growth — the most powerful force in personal finance. At 7% real return per year, money doubles approximately every ten years. $10,000 invested at age 25 becomes approximately $40,000 by age 45 and $160,000 by age 65 — in real purchasing-power terms, with no additional contributions. The same $10,000 in a savings account at 0.42% grows to approximately $11,300 after 30 years in nominal terms, losing real value throughout.

The Motley Fool's projection makes the compounding argument concrete: at a 10.3% annualised total return (the S&P 500's nominal lifetime average since 1957), a single $10,000 investment grows to over $189,000 over 30 years. Jay Zigmont, CFP and founder of Childfree Trust, recommends: 'Long-term, passive investing is truly sustainable. For my clients, I tend to recommend a three-fund portfolio including the entire US stock market, international stock market, and bonds.' Robert R. Johnson, CFA and professor of finance at Creighton University, adds: 'I would recommend simply dollar cost averaging into a mutual fund or ETF that tracks a well-known index like the S&P 500. Consistency and patience are the virtues associated with accumulating wealth over the long run.'

Index funds carry two principal costs — one visible, one invisible. The visible cost is fees: the best S&P 500 index funds carry expense ratios of 0.03% to 0.15% per year, meaning they consume virtually nothing of your returns. The invisible cost is volatility: Optionality's March 2026 analysis notes that a 10% correction occurs roughly every 1.8 years, bear markets occur about every 5.4 years, and the average bear market lasts 13 months. Volatility is not a reason to avoid stocks; it is the price you pay for the higher long-term returns. The investors who earn the most from index funds are those who continue contributing through corrections and hold through bear markets rather than selling at the bottom.

A 25-year inflation-adjusted analysis by Penrose Team and Wealthformula comparing real estate investment against S&P 500 index fund investment (2000 to 2025) found that the real estate investor (who purchased a median-priced home in Phoenix with a 20% down payment and held it as a rental) achieved a real IRR of approximately 5% per year and grew their initial equity roughly 4.5 times in real terms over 25 years. The S&P 500 investor achieved a 7.7% compound annual growth rate nominal and a 254% total real return. Both strategies built wealth significantly — the mechanisms and effort involved were dramatically different.

Real estate's unique advantage is leverage. A mortgage allows you to control a $400,000 asset with an $80,000 down payment — meaning that if the property appreciates by 5%, your $400,000 asset gains $20,000 in value, representing a 25% return on your $80,000 equity. This leverage effect amplifies returns significantly compared with unleveraged stock market investing at equivalent initial capital, though it also amplifies losses in a declining market. Sam Dogen, founder of Financial Samurai, advises: 'No single asset, including real estate, should exceed 50% of one's overall net worth. Homeowners should aim for their homes to represent 25% to 30% of net worth by retirement, diversifying investments into stocks, bonds, and other assets.'

In a standard taxable brokerage account, dividends and capital gains are taxed every year, reducing the amount available to reinvest and compound. In a tax-advantaged account like a 401(k) or Roth IRA, gains compound untaxed (or tax-free in a Roth) until withdrawal, allowing the full return to reinvest and compound year after year. Over 30 years, the difference in after-tax wealth between a taxable and tax-advantaged account holding identical investments can be substantial — often 20% to 30% more wealth at retirement from the same contributions.

Vanguard's How America Saves 2025 report, cited by AOL, found that most workers are letting professionals or automated funds manage their 401(k)s, and nearly half are putting a bigger share of their paycheck toward retirement than previously. The 401(k) contribution limit in 2025 is $23,500 per year (plus $7,500 catch-up for those 50 and over). A Roth IRA allows $7,000 per year ($8,000 for 50+), with the unique advantage that qualified withdrawals in retirement are completely tax-free. For most UK investors, the Stocks and Shares ISA (£20,000 annual allowance in 2026/27 — though under-65s should note this is the last year before the allowance is reduced to £12,000 from April 2027) is the primary tax-efficient investment vehicle.

The long-run performance of REITs is well-documented: Optionality's March 2026 analysis cites US aggregate REITs returning 7.8% annualised over the long term — comparable to the S&P 500's real return and significantly above bonds (3.5%) or cash (1.8%). REITs provide the inflation-hedging characteristics of real estate (rents tend to rise with inflation, and property values generally appreciate over time) combined with the liquidity of a publicly traded stock — you can buy or sell a REIT position in seconds, unlike a physical property which may take months to transact.

For investors who want real estate exposure in their portfolio but lack the capital or appetite for direct property ownership, REITs represent the most accessible route. In the UK, Property REITs can be held within a Stocks and Shares ISA, combining real estate returns with full tax exemption on dividends and capital gains. In the US, REITs held within a 401(k) or IRA provide the same tax-advantaged compounding on their income-heavy distributions.

'The market might crash.' It will. It does, regularly. Optionality documents that bear markets occur every 5.4 years on average. The question is not whether a crash will happen, but what you do when it does. Every S&P 500 bear market in history has eventually been followed by a full recovery and new highs. Investors who held through 2008 to 2009 and 2020 were fully recovered within months to a couple of years and went on to compound substantial wealth. The risk is not the crash — it is the behavioural response to the crash.

'What if I pick the wrong investment?' This is the primary argument for index funds rather than individual stock selection. An S&P 500 index fund owns a small piece of approximately 500 of the largest US companies — meaning no individual company failure can destroy your investment. When one company struggles, others succeed. The index as a whole has never permanently lost value over any 20-year period in its history. This diversification, available to any investor for a 0.03% annual fee, eliminates the single-stock risk that makes stock-picking so dangerous for non-professionals.

The practical framework is simple: build a genuine emergency fund in a high-yield savings account, maximise contributions to tax-advantaged investment accounts, invest consistently in low-cost broad market index funds and real estate exposure appropriate to your circumstances, and stay invested through volatility rather than responding to fear. The historical record of appreciating asset returns over the long run is not a guarantee — but it is the strongest evidence available about what produces wealth, and it points consistently in the same direction. The time to start is now, at whatever amount is possible. Compound interest rewards those who start early and stay consistent above all other strategies.

References

Trade That Swing — Historical Average Stock Market Returns: S&P 500 150-Year Average (February 2026) https://tradethatswing.com/average-historical-stock-market-returns-for-sp-500-5-year-up-to-150-year-averages/

Optionality — S&P 500 Statistics 2026: Historical Returns, Average Performance and Data (March 2026) https://www.optionalityhq.com/statistics/sp500-statistics

Impact Wealth — Why Is Investing a More Powerful Tool to Build Long-Term Wealth Than Saving? (January 2026) https://impactwealth.org/why-is-investing-a-more-powerful-tool-to-build-long-term-wealth-than-saving/

Equity Bank — Saving vs. Investing: When to Build Wealth (March 2026) https://www.equitybank.com/articles/saving-vs-investing-when-its-time-to-start-building-wealth/

Bankrate — Saving vs. Investing: Key Differences, How to Choose (February 2026) https://www.bankrate.com/investing/saving-vs-investing/

IPX1031 — Wealth-Building in 2025: Generational Investing Statistics (January 2026) https://www.ipx1031.com/investing-statistics-by-generation/

Wealthformula — Real Estate vs. S&P 500: Historical Returns, Risk and Cost Comparison https://www.wealthformula.com/blog/real-estate-vs-sp-500-historical-returns-risk-and-cost-comparison/

TABLE OF CONTENTS

- Savings: Essential Foundation, Not a Wealth Engine

- The Inflation Problem: Why Cash Savings Lose Value Over Time

- The Mathematical Case: What 30 Years of Saving vs Investing Produces

- What Makes an Asset 'Appreciating'?

- Asset Class 1: Stock Market Index Funds

- Asset Class 2: Real Estate

- Asset Class 3: Retirement Accounts — The Tax-Advantaged Compounder

- Asset Class 4: REITs — Real Estate Without the Landlord Work

- Building a Simple, Practical Investment Strategy

- Common Objections — and Honest Answers

- Conclusion

- Frequently Asked Questions

- References

Savings: Essential Foundation, Not a Wealth Engine

Savings are not the enemy of wealth building — they are the necessary precondition for it. Without savings, there is no emergency fund to protect you when income stops unexpectedly. Without savings, there is no capital to deploy into investments. Without savings, every financial setback becomes a debt problem. The savings account, the high-yield savings account, the emergency fund in a money market — all of these serve a real and important purpose. The problem is not saving. The problem is confusing saving with wealth building.Saving money and building wealth are two distinct activities with two distinct mechanisms. Saving is the act of not spending money — setting it aside in a form that is safe, accessible, and protected from loss. Its primary virtues are liquidity and capital preservation. Building wealth requires something else: putting capital into assets that generate returns over time, either through income (dividends, rent, interest) or through appreciation in value, or both. As Impact Wealth's January 2026 analysis states plainly: 'Saving money is essential, but it will not make you wealthy on its own. If your goal is to build substantial long-term wealth, investing consistently outperforms saving in nearly every measurable way.'

The practical implication is a sequencing question, not an either/or choice. Equity Bank's March 2026 guide frames it well: 'Rather than choosing one or the other, most people use a combination of both strategies. Savings protect what you cannot afford to lose, while investing helps you grow what you can set aside for the future.' The foundation — a three-to-six-month emergency fund in a high-yield savings account — comes first. Once that foundation is in place, every additional pound or dollar that goes into savings rather than investments is a missed opportunity to compound.

The Inflation Problem: Why Cash Savings Lose Value Over Time

The most important economic argument for investing over saving is one that is rarely visible until you do the maths. Inflation — the gradual rise in the general price level — erodes the purchasing power of cash savings continuously, every year, without pause. A sum of money sitting in a savings account that earns 0.42% APY (the FDIC national average, May 2025) in a 2.5% to 3% inflation environment is not just not growing — it is shrinking in real terms.In concrete terms: £10,000 held in a standard savings account earning 0.42% per year for ten years grows to approximately £10,425 in nominal terms. But if inflation averages 2.5% over that period, the purchasing power of that £10,000 in today's terms is approximately £8,100 after ten years. The saver's nominal balance grew by £425. Their real wealth declined by approximately £1,900. The account statement shows growth; the actual financial position has deteriorated.

This is why the Dallas Federal Reserve defines investment so specifically: 'Investments increase by generating income (interest or dividends) or by growing (appreciating) in value. Income earned from your investments and any appreciation in the value of your investments increase your wealth.' The emphasis on appreciation in value is critical — not just nominal return, but real growth that outpaces inflation. Assets that appreciate in value over time are the mechanism through which wealth outpaces inflation and compounds toward financial independence.

The difference comes down to one fundamental principle: money that sits idle loses purchasing power over time, while money that works for you has the potential to grow exponentially.

— IMPACT WEALTH — WHY IS INVESTING A MORE POWERFUL TOOL TO BUILD LONG-TERM WEALTH THAN SAVING? (JANUARY 2026)

The Mathematical Case: What 30 Years of Saving vs Investing Produces

The most compelling argument for investing over pure saving is not theoretical — it is arithmetical. Ramit Sethi's widely cited analysis, reported by Nasdaq, calculates the outcome of two people who each set aside $1,000 per month for 30 years with different approaches.The saver deposits $1,000 per month into a standard savings account earning the FDIC national average of 0.42% per year (May 2025 FDIC data). After 30 years, they have accumulated approximately $383,000. This is genuinely good — $383,000 is a significant sum, earned through consistent discipline over three decades. But it represents only 7% more than the $360,000 they contributed in cash over 30 years. The savings account added almost nothing beyond the deposits themselves.

The investor commits the same $1,000 per month for 30 years but invests it in assets generating the historical average real return of 7% per year (after inflation). After 30 years, they have approximately $1.2 million. The investor has $817,000 more than the saver — for the same monthly commitment, the same time period, and the same discipline. The difference is entirely attributable to the power of compound returns on appreciating assets.

Source: Ramit Sethi / Nasdaq analysis; FDIC national average savings rate, May 2025. Based on $1,000/month contributions over 30 years. Historical investment return of 7% real (after inflation) is the long-run S&P 500 inflation-adjusted average per Trade That Swing (February 2026) and Optionality (March 2026). Past performance does not guarantee future results.

What Makes an Asset 'Appreciating'?

An appreciating asset is one whose value increases over time — not because of inflation making everything nominally more expensive, but because of genuine underlying value creation: a business generating more revenue, a property serving a growing population with constrained housing supply, a commodity with industrial demand that outpaces supply. The difference between an appreciating asset and a depreciating one is whether the underlying economics drive value upward or downward over the long runAppreciating assets share certain characteristics. They produce something of value — either directly (a property provides shelter, a business produces goods or services) or by entitling the holder to a share of something that does. They benefit from scarcity — their supply is constrained relative to demand over time (quality real estate in growing cities, shares in genuinely growing businesses). And they compound — the returns they generate can be reinvested to generate further returns, creating the exponential growth trajectory that makes long-term investing so powerful.

Depreciating assets — cars, most electronics, most physical consumer goods — lose value over time because they wear out, become obsolete, or face competitive alternatives that reduce their relative desirability. The key insight from IPX1031's 2025 survey is instructive: 80% of Americans understand at some level that real estate is important for building long-term wealth, while 58% believe the stock market provides better returns. Both intuitions are right. The most effective wealth-building portfolios typically include both.

Asset Class 1: Stock Market Index Funds

Broad stock market index funds — particularly those tracking the S&P 500 or a total market index — are the most accessible, lowest-cost, and historically most consistent vehicle for long-term wealth building available to ordinary investors. The S&P 500's historical average annual return is 9.43% over 150 years with dividends reinvested, according to Trade That Swing's February 2026 analysis. Adjusted for inflation, the real return is approximately 7% per year (Optionality, March 2026). Optionality notes that a 10.2% average nominal annual return 'still represents one of the strongest long-term wealth-building vehicles available to investors.'The mechanism is compound growth — the most powerful force in personal finance. At 7% real return per year, money doubles approximately every ten years. $10,000 invested at age 25 becomes approximately $40,000 by age 45 and $160,000 by age 65 — in real purchasing-power terms, with no additional contributions. The same $10,000 in a savings account at 0.42% grows to approximately $11,300 after 30 years in nominal terms, losing real value throughout.

The Motley Fool's projection makes the compounding argument concrete: at a 10.3% annualised total return (the S&P 500's nominal lifetime average since 1957), a single $10,000 investment grows to over $189,000 over 30 years. Jay Zigmont, CFP and founder of Childfree Trust, recommends: 'Long-term, passive investing is truly sustainable. For my clients, I tend to recommend a three-fund portfolio including the entire US stock market, international stock market, and bonds.' Robert R. Johnson, CFA and professor of finance at Creighton University, adds: 'I would recommend simply dollar cost averaging into a mutual fund or ETF that tracks a well-known index like the S&P 500. Consistency and patience are the virtues associated with accumulating wealth over the long run.'

Index funds carry two principal costs — one visible, one invisible. The visible cost is fees: the best S&P 500 index funds carry expense ratios of 0.03% to 0.15% per year, meaning they consume virtually nothing of your returns. The invisible cost is volatility: Optionality's March 2026 analysis notes that a 10% correction occurs roughly every 1.8 years, bear markets occur about every 5.4 years, and the average bear market lasts 13 months. Volatility is not a reason to avoid stocks; it is the price you pay for the higher long-term returns. The investors who earn the most from index funds are those who continue contributing through corrections and hold through bear markets rather than selling at the bottom.

Asset Class 2: Real Estate

Real estate is the other great appreciating asset class and has made more millionaires than any other category of investment in history. IPX1031's 2025 survey finds that 80% of Americans believe owning real estate is important for long-term wealth building — a view that is consistently validated by the data, though with important nuances.A 25-year inflation-adjusted analysis by Penrose Team and Wealthformula comparing real estate investment against S&P 500 index fund investment (2000 to 2025) found that the real estate investor (who purchased a median-priced home in Phoenix with a 20% down payment and held it as a rental) achieved a real IRR of approximately 5% per year and grew their initial equity roughly 4.5 times in real terms over 25 years. The S&P 500 investor achieved a 7.7% compound annual growth rate nominal and a 254% total real return. Both strategies built wealth significantly — the mechanisms and effort involved were dramatically different.

Real estate's unique advantage is leverage. A mortgage allows you to control a $400,000 asset with an $80,000 down payment — meaning that if the property appreciates by 5%, your $400,000 asset gains $20,000 in value, representing a 25% return on your $80,000 equity. This leverage effect amplifies returns significantly compared with unleveraged stock market investing at equivalent initial capital, though it also amplifies losses in a declining market. Sam Dogen, founder of Financial Samurai, advises: 'No single asset, including real estate, should exceed 50% of one's overall net worth. Homeowners should aim for their homes to represent 25% to 30% of net worth by retirement, diversifying investments into stocks, bonds, and other assets.'

Asset Class 3: Retirement Accounts — The Tax-Advantaged Compounder

Retirement accounts — 401(k)s and IRAs in the US, pensions and ISAs in the UK — are not themselves asset classes, but they are the most tax-efficient vehicle for holding appreciating assets. The compounding advantage of a 401(k) or ISA over a standard brokerage account is substantial and often underappreciated.In a standard taxable brokerage account, dividends and capital gains are taxed every year, reducing the amount available to reinvest and compound. In a tax-advantaged account like a 401(k) or Roth IRA, gains compound untaxed (or tax-free in a Roth) until withdrawal, allowing the full return to reinvest and compound year after year. Over 30 years, the difference in after-tax wealth between a taxable and tax-advantaged account holding identical investments can be substantial — often 20% to 30% more wealth at retirement from the same contributions.

Vanguard's How America Saves 2025 report, cited by AOL, found that most workers are letting professionals or automated funds manage their 401(k)s, and nearly half are putting a bigger share of their paycheck toward retirement than previously. The 401(k) contribution limit in 2025 is $23,500 per year (plus $7,500 catch-up for those 50 and over). A Roth IRA allows $7,000 per year ($8,000 for 50+), with the unique advantage that qualified withdrawals in retirement are completely tax-free. For most UK investors, the Stocks and Shares ISA (£20,000 annual allowance in 2026/27 — though under-65s should note this is the last year before the allowance is reduced to £12,000 from April 2027) is the primary tax-efficient investment vehicle.

Asset Class 4: REITs — Real Estate Without the Landlord Work

Real Estate Investment Trusts (REITs) allow investors to access the appreciation and income characteristics of real estate without purchasing physical property, managing tenants, or dealing with maintenance and void periods. REITs are publicly traded companies that own income-producing real estate — office buildings, residential properties, retail centres, industrial warehouses, data centres — and are required by law to distribute at least 90% of their taxable income as dividends to shareholders.The long-run performance of REITs is well-documented: Optionality's March 2026 analysis cites US aggregate REITs returning 7.8% annualised over the long term — comparable to the S&P 500's real return and significantly above bonds (3.5%) or cash (1.8%). REITs provide the inflation-hedging characteristics of real estate (rents tend to rise with inflation, and property values generally appreciate over time) combined with the liquidity of a publicly traded stock — you can buy or sell a REIT position in seconds, unlike a physical property which may take months to transact.

For investors who want real estate exposure in their portfolio but lack the capital or appetite for direct property ownership, REITs represent the most accessible route. In the UK, Property REITs can be held within a Stocks and Shares ISA, combining real estate returns with full tax exemption on dividends and capital gains. In the US, REITs held within a 401(k) or IRA provide the same tax-advantaged compounding on their income-heavy distributions.

Building a Simple, Practical Investment Strategy

The good news about wealth-building through appreciating assets is that it does not require sophisticated financial knowledge, daily market monitoring, or complex strategies. The evidence consistently shows that simple, consistent, low-cost approaches outperform active management over the long run. The following framework applies whether you are starting with £50 per month or £5,000.A practical five-step wealth-building framework for 2026

- Step 1 — Build the foundation first: Before investing a single pound or dollar in appreciating assets, establish a three-to-six-month emergency fund in a high-yield savings account. This is the financial moat that prevents a job loss, car repair, or medical bill from forcing you to sell investments at the worst possible time. In the UK, current best easy-access rates are up to 4.84% APY (Chip, May 2026). In the US, rates up to 5.00% APY are available from Varo Money. This fund is not an investment — it is protection for your investments.

- Step 2 — Maximise tax-advantaged accounts first: Invest through your 401(k) to at least the employer match (if available — this is effectively a 50–100% immediate return), then through a Roth IRA or Traditional IRA (US), or a Stocks and Shares ISA (UK). The tax efficiency of these vehicles means you capture more of the underlying asset's return. Contributions to these accounts should take priority over taxable investment accounts for most investors.

- Step 3 — Choose simple, low-cost index funds: For most investors, a three-fund portfolio (global equity index fund, domestic equity index fund, and bond index fund) captures the returns of the global economy at minimal cost. Funds tracking the FTSE All-World, S&P 500, or MSCI World with expense ratios below 0.15% are appropriate building blocks. Dollar-cost averaging — investing a fixed amount on a fixed schedule regardless of market conditions — is the most effective method for building positions without the risk of poor timing.

- Step 4 — Add real estate exposure appropriately: For those with capital for a deposit, owner-occupied property builds equity through mortgage repayment while providing real estate appreciation. For those without the capital or appetite for direct ownership, REITs provide equivalent exposure within an ISA or retirement account. Sam Dogen's guidance applies: keep real estate at 25–30% of net worth at retirement, not the entire portfolio.

- Step 5 — Stay invested through volatility: The primary reason investors earn less than the historical market average is that they sell during corrections and miss the recovery. Optionality's March 2026 data shows the average bear market lasts 13 months and recovers fully within 27 months. Investors who remain invested through bear markets earn the long-run return. Investors who sell during them crystallise losses and miss the recovery. The single most valuable investing skill is the ability to hold through short-term pain for long-term gain.

Common Objections — and Honest Answers

'I don't have enough money to invest.' The most widely used starting position for stock market index investing is now £1 or $1 — literally the price of a coffee. Apps like Freetrade, InvestEngine, and Trading 212 in the UK, and Fidelity, Vanguard, and Charles Schwab in the US, allow fractional share purchases with no minimum investment requirement. The habit of investing is more important than the amount at first. Starting with £50 per month at 25 and increasing contributions over time produces far better outcomes than waiting until you have a 'significant' amount to invest.'The market might crash.' It will. It does, regularly. Optionality documents that bear markets occur every 5.4 years on average. The question is not whether a crash will happen, but what you do when it does. Every S&P 500 bear market in history has eventually been followed by a full recovery and new highs. Investors who held through 2008 to 2009 and 2020 were fully recovered within months to a couple of years and went on to compound substantial wealth. The risk is not the crash — it is the behavioural response to the crash.

'What if I pick the wrong investment?' This is the primary argument for index funds rather than individual stock selection. An S&P 500 index fund owns a small piece of approximately 500 of the largest US companies — meaning no individual company failure can destroy your investment. When one company struggles, others succeed. The index as a whole has never permanently lost value over any 20-year period in its history. This diversification, available to any investor for a 0.03% annual fee, eliminates the single-stock risk that makes stock-picking so dangerous for non-professionals.

CONCLUSION

Savings matter. They protect you, give you options, and provide the capital that makes investing possible. But savings alone — sitting in accounts that earn 0.42% while inflation runs at 2.5% or more — are a slow path to financial stagnation, not wealth. The $817,000 difference between the 30-year saver and the 30-year investor, investing the same monthly amount, is not the product of financial genius or exceptional luck. It is the product of compound returns on appreciating assets, accumulated over time.The practical framework is simple: build a genuine emergency fund in a high-yield savings account, maximise contributions to tax-advantaged investment accounts, invest consistently in low-cost broad market index funds and real estate exposure appropriate to your circumstances, and stay invested through volatility rather than responding to fear. The historical record of appreciating asset returns over the long run is not a guarantee — but it is the strongest evidence available about what produces wealth, and it points consistently in the same direction. The time to start is now, at whatever amount is possible. Compound interest rewards those who start early and stay consistent above all other strategies.

Frequently Asked Questions

Why won't savings make me rich?

Savings accounts, even high-yield ones, earn rates that rarely exceed inflation by more than one to two percentage points. The FDIC national average savings rate in the US was 0.42% in May 2025, well below any reasonable inflation estimate. In a 2.5% inflation environment, a 0.42% savings account is losing approximately 2% of its real purchasing power every year. Even the best high-yield savings accounts in 2026 — paying 4.84% in the UK and up to 5.00% in the US — produce after-tax returns in the 3% to 4% range for most holders. This is useful for protecting capital and outpacing inflation marginally, but it produces nothing close to the compounding wealth that stock market index funds, real estate, and other appreciating assets deliver at 7% to 10%+ over the long run. Ramit Sethi's analysis, reported by Nasdaq, quantifies this: someone saving $1,000 per month for 30 years ends up with $383,000; an investor doing the same ends up with $1.2 million.What assets appreciate in value over time?

The assets with the strongest long-run appreciation records are: (1) Broad stock market index funds tracking the S&P 500 or a total market index — 9.43% average annual return over 150 years with dividends reinvested, 7% real (Trade That Swing, February 2026); (2) Real estate — both owner-occupied (building equity through mortgage repayment and price appreciation) and rental property (income plus appreciation, leveraged through a mortgage); (3) REITs (Real Estate Investment Trusts) — 7.8% annualised long-term return, accessible through any brokerage account (Optionality, March 2026); (4) Gold — 8.1% annualised long-term return, primarily as an inflation and volatility hedge rather than a primary wealth-building vehicle. US aggregate bonds returned 3.5% annualised, making them appropriate for capital preservation and portfolio stabilisation but not primary wealth building.What is compound interest and why does it matter for wealth building?

Compound interest — or more broadly, compound returns — is the process by which investment returns are added to the principal and then themselves begin generating returns. In other words, your returns earn returns. The effect is not linear but exponential over time. At 7% real annual return: $10,000 becomes $19,672 after 10 years, $38,697 after 20 years, and $76,123 after 30 years — without any additional contributions. The Motley Fool quantifies the S&P 500 version: at a 10.3% nominal annualised return, $10,000 grows to over $189,000 over 30 years. The key conditions for compound returns to work powerfully are time (starting earlier dramatically amplifies the outcome), consistency (reinvesting returns rather than withdrawing them), and low costs (high fees eat the returns that would otherwise compound).When should I save and when should I invest?

Save until your emergency fund is established (three to six months of essential living expenses in a high-yield savings account). During this phase, any surplus after meeting your emergency fund target should still be invested, not held in additional savings. Invest consistently and continuously once the emergency fund is in place, prioritising: (1) employer-matched 401(k) or workplace pension contributions first (the match is an instant 50–100% return); (2) tax-advantaged accounts (Roth IRA, ISA) up to annual limits; (3) additional taxable investment accounts for any surplus. Continue saving only for specific near-term goals with a defined timeline of less than three to five years — house deposit, car purchase, holiday fund — using high-yield savings for those. Everything else with a timeline longer than five years belongs in appreciating assets, not savings accounts. Equity Bank's March 2026 guidance summarises it well: 'Savings protect what you cannot afford to lose, while investing helps you grow what you can set aside for the future.'How much should I invest each month to build meaningful wealth?

Any consistent amount invested over time produces meaningful wealth through compounding. Investing $200 per month from age 25 at 7% real return produces approximately $482,000 by age 65. Investing $500 per month produces approximately $1.2 million. Investing $1,000 per month produces approximately $2.4 million. The most powerful lever is starting age, not monthly amount — every decade of earlier starting effectively doubles the final outcome at the same monthly contribution. The practical starting point is to invest at least enough to capture any employer match on a workplace pension or 401(k) (which represents a guaranteed immediate return of 50% to 100% on those contributions), and then to increase investment contributions by 1% of income each year until you are investing 15% to 20% of gross income. Dollar-cost averaging — investing a fixed amount on a fixed monthly schedule — removes the need to time the market and captures both high and low prices over time.References

Trade That Swing — Historical Average Stock Market Returns: S&P 500 150-Year Average (February 2026) https://tradethatswing.com/average-historical-stock-market-returns-for-sp-500-5-year-up-to-150-year-averages/

Optionality — S&P 500 Statistics 2026: Historical Returns, Average Performance and Data (March 2026) https://www.optionalityhq.com/statistics/sp500-statistics

Impact Wealth — Why Is Investing a More Powerful Tool to Build Long-Term Wealth Than Saving? (January 2026) https://impactwealth.org/why-is-investing-a-more-powerful-tool-to-build-long-term-wealth-than-saving/

Equity Bank — Saving vs. Investing: When to Build Wealth (March 2026) https://www.equitybank.com/articles/saving-vs-investing-when-its-time-to-start-building-wealth/

Bankrate — Saving vs. Investing: Key Differences, How to Choose (February 2026) https://www.bankrate.com/investing/saving-vs-investing/

IPX1031 — Wealth-Building in 2025: Generational Investing Statistics (January 2026) https://www.ipx1031.com/investing-statistics-by-generation/

Wealthformula — Real Estate vs. S&P 500: Historical Returns, Risk and Cost Comparison https://www.wealthformula.com/blog/real-estate-vs-sp-500-historical-returns-risk-and-cost-comparison/

0 Comments Comments