AI Tools

Consumers Are Turning to AI for Investment Decisions

TABLE OF CONTENTS

- How Quickly Is AI Adoption Growing Among Investors?

- Who Is Using AI Most — and for What?

- Which AI Tools Are Most Popular for Finance?

- What Are Consumers Actually Asking AI?

- What AI Gets Right — and Where It Falls Short

- The Advice Gap: Why So Many Turn to AI First

- What Regulators Are Saying

- AI as a Research Tool vs AI as an Adviser

- How to Use AI Wisely for Investment Decisions

- Conclusion

- Frequently Asked Questions

- References

How Quickly Is AI Adoption Growing Among Investors?

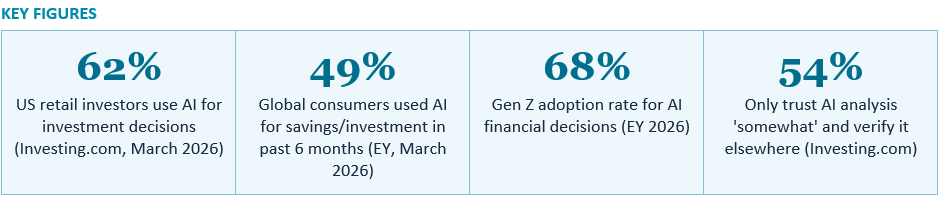

The speed at which consumers have adopted AI tools for financial decision-making has taken even the financial services industry by surprise. Just two years ago, the idea of asking a chatbot whether to put your savings into an index fund would have seemed fanciful. Today, it is something close to mainstream.The clearest picture of where things currently stand comes from two landmark surveys published in early 2026. In March 2026, Investing.com published findings from a survey of 938 American adult investors conducted the previous month. The results were striking: 62% of respondents said they had used AI tools to assist with investment decisions, and more than half said they expected to use AI even more in the future — with 38% planning to use it significantly more.

Almost simultaneously, EY released findings from its 2026 AI Sentiment Report, based on a far larger sample of 18,000 consumers across 23 countries. EY found that 49% of global consumers had used AI in the past six months to help with savings and investment decisions. Among younger demographics, adoption was even higher: 68% of Gen Z consumers and 65% of millennials had used AI for financial decisions in the same period.

A separate survey by TD Bank, released in April 2026, found that 55% of US consumers were using AI to aid their financial management decisions. And J.D. Power data found that 13% of respondents were using AI for banking and financial services on a daily basis, with 59% using it occasionally. Across multiple independent surveys, the message is consistent: AI is no longer a fringe tool for investing. It is a mainstream one.

Who Is Using AI Most — and for What?

Adoption rates vary significantly across demographic groups, and the pattern that emerges from the data is consistent across different surveys and markets. Younger, more digitally native consumers are the most enthusiastic AI adopters for financial decisions, while older consumers are more cautious — but adoption is rising across all age groups.TD Bank's 2026 survey found adoption rates of 77% among Gen Z, 72% among millennials, 49% among Gen X, and 30% among baby boomers. The J.D. Power survey found that AI chatbot usage for financial advice was particularly concentrated among consumers under 40, with ChatGPT dominating that age group, while Google Gemini was preferred among users over 40.

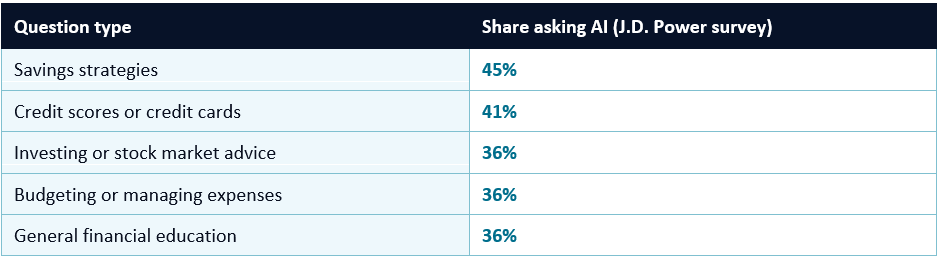

The topics consumers are turning to AI for reveal a broad and practical set of financial questions. According to J.D. Power, savings strategies were the most popular question asked to AI (45% of those who had used AI for financial purposes), followed by credit scores or credit card questions (41%), investing or stock market advice (36%), budgeting or managing expenses (36%), and general financial education (36%). Forty-nine percent of UK consumers specifically believed AI would be helpful for fraud detection, according to EY's UK-specific findings.

Which AI Tools Are Most Popular for Finance?

Across both the Investing.com and J.D. Power surveys, one name dominated: ChatGPT. Among US retail investors using AI tools for investment research, ChatGPT was the most widely used, with 54% of Investing.com respondents saying they had used it for investing-related research. The ABA Banking Journal study found ChatGPT was particularly dominant among users under 40. A parallel Lloyds Banking Group study of 5,000 UK consumers corroborated this finding, identifying ChatGPT as the most popular tool, with Google's Gemini second.Other tools mentioned in surveys included Microsoft Copilot, Meta AI, Apple Siri, and Amazon Alexa, though all registered in single-digit percentages compared with ChatGPT's lead. Among those using general-purpose chatbots, the shift toward AI-specific financial platforms is also accelerating. Platforms like BridgeWise provide AI-powered research on more than 50,000 assets and represent a growing category of tools specifically designed for investment analysis, in contrast to general-purpose chatbots repurposed for financial questions.

The growth in dedicated AI investment platforms is significant because they are engineered with financial data as their primary input, rather than relying on general training data that may be outdated or incomplete. These platforms typically pull live market data, earnings reports, and analyst notes into their analysis — addressing one of the most frequently cited limitations of general-purpose chatbots, which are trained on static datasets with a knowledge cutoff date and cannot access real-time market prices.

What Are Consumers Actually Asking AI?

Understanding what questions people are asking AI — and what they actually do with the answers — helps clarify both the genuine value of these tools and their limitations. LendingTree researchers tested 20 personal finance prompts across ChatGPT, Google Gemini, and Claude Sonnet in August 2025, providing one of the most detailed independent evaluations of AI financial guidance published to date.The researchers found that AI chatbots were often technically correct but did not always paint a realistic picture of an individual's financial situation. When asked about retirement planning for a 50-year-old couple with only $100,000 saved, ChatGPT recommended saving more than $30,000 annually to catch up over 17 years — without asking about the couple's income or the reasons behind the savings shortfall. That is an unrealistic goal for many households, but the AI presented it as the solution without the caveats a human adviser would typically include.

Numerical accuracy was another concern. LendingTree found that ChatGPT presented 2024 IRA and 401(k) contribution limits as if they were the 2025 figures, citing $23,000 for 401(k) contributions when the actual 2025 limit had risen to $23,500. LLMs, the researchers noted, are language prediction models — they handle text better than numbers, and can produce plausible-sounding figures that are slightly incorrect. This is a particular risk in financial contexts where specific numbers — tax thresholds, contribution limits, interest rates — are critical to decision quality.

Chatbots are often technically correct but don't always paint a realistic picture. They tend to be overly optimistic when key details are missing.

— LENDINGTREE RESEARCH TEAM, AUGUST 2025

What AI Gets Right — and Where It Falls Short

AI tools for investing have genuine strengths that explain their rapid adoption, alongside serious limitations that explain why regulators and financial professionals remain cautious. Understanding both sides is essential for anyone using these tools.Where AI adds real value

The speed and breadth of AI's information processing is genuinely impressive and genuinely useful. Nearly 40% of Investing.com survey respondents said the key advantage of AI was its ability to analyse market data faster than they could themselves. AI can rapidly summarise earnings reports, cross-reference analyst ratings, compare historical performance data, and explain complex financial concepts in plain language — tasks that would take a human researcher hours to complete manually.AI also excels at emotional neutrality. Fifteen percent of Investing.com respondents specifically said AI helped reduce emotional decision-making and improve discipline in their investment strategies. This is consistent with the research on behavioural finance: human investors are prone to panic-selling during market downturns and chasing returns during bull markets. An AI that simply presents data and analysis without the emotional charge of a news broadcast or a panicking friend can, in theory, help investors make more rational decisions.

For financial education — explaining what a bond is, how dollar-cost averaging works, the difference between a Roth and a traditional IRA — AI chatbots perform reliably well. The 36% of J.D. Power respondents using AI for general financial education are likely using it in a way that is both safe and genuinely helpful.

Where AI falls short

AI struggles significantly with personalisation. It does not know your full financial picture — your income, debts, tax situation, risk tolerance, dependants, or long-term goals — unless you explicitly tell it, and even then it cannot hold that context across multiple sessions. A professional financial adviser builds a relationship and a deep understanding of your situation over time. A chatbot starts fresh every time.AI also cannot access real-time market prices, interest rates, or regulatory updates unless it has a live internet connection. Even the best AI tools have knowledge cutoff dates and may present outdated figures as current. For a field where the difference between last year's tax rules and this year's can be material to a financial decision, this is a serious limitation.

Perhaps most importantly, AI-generated financial analysis can be confidently wrong. The phenomenon known as hallucination — where AI produces plausible-sounding but factually incorrect information — is a known risk with all current language models. For lesser-known companies or niche financial products, the risk of hallucination is higher. As BridgeWise CEO Gaby Diamant noted in a 2025 interview with Euronews: if you ask about a company that is not well-known, the AI will try to please you with an answer that may not be grounded in fact.

The Advice Gap: Why So Many Turn to AI First

To understand why consumers are turning to AI for investment advice, it is important to understand the problem AI is filling: a profound shortage of affordable, accessible human financial advice.In the UK, the proportion of human financial advisers accepting clients with less than £50,000 in investable assets has halved over the past six years — from 52% to just 25%, according to Schroders data. At the same time, the proportion of advisers serving only clients with £200,000 or more has nearly trebled, from 11% to 30%. The result is that millions of people with meaningful savings but below the informal wealth threshold for professional advice are effectively shut out of the human advisory market.

In the US, the picture is similar. While a robo-adviser can manage a simple portfolio for a management fee of 0.25% to 0.50%, personalised financial planning from a human certified financial planner (CFP) typically costs between $150 and $300 per hour, or requires a minimum investable asset level to qualify for ongoing advice. For younger investors, first-time investors, and lower-to-middle income households, the cost of human advice is simply prohibitive.

This advice gap explains not just the growth of AI adoption but also its demographic distribution. Gen Z and millennials — who are less likely to have sufficient assets for premium human advice and more comfortable with digital tools — are the most enthusiastic AI adopters. AI is not replacing professional advice for the people who can afford it. It is filling a vacuum for the millions who cannot.

What Regulators Are Saying

Regulators in both the US and UK have responded to the rapid adoption of AI investment tools with a combination of genuine interest, active investigation, and clear consumer warnings about the limitations and risks involved.The UK's Financial Conduct Authority (FCA) opened a formal review of AI's retail-market implications in January 2026, examining how AI could evolve for retail investors, regulators, firms, and markets. The FCA's position on general-purpose AI tools is unambiguous: ChatGPT, Gemini, Claude, and similar tools are not regulated financial services products. Advice generated by these tools is not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If you lose money acting on ChatGPT's investment guidance, you have no regulatory recourse.

The FCA has also noted that it is developing a new regulatory category called 'targeted support' — ready-made, scenario-based suggestions for common financial situations like managing surplus savings or planning for retirement income — which would sit between generic information and full personalised advice, at a lower cost. FCA Deputy Chief Executive Sarah Pritchard has described this framework as potentially 'game-changing' for access to financial guidance.

In the US, the Securities and Exchange Commission (SEC) has been active in monitoring how AI is being used by retail brokers and investment advisers, and has cautioned that any AI tool providing personalised investment recommendations may cross the line into regulated investment advisory activity. A 2025 study published in Nature noted that while AI's ability to process unstructured financial data — reports, news, user queries — is impressive, the risk of biased or inaccurate inputs producing misleading outputs (hallucination) remains a central regulatory concern.

Regulatory position at a glance

- UK FCA: General-purpose AI tools like ChatGPT are NOT regulated. Advice from them is NOT covered by the Financial Ombudsman Service or FSCS.

- UK FCA: A new 'targeted support' regulatory category is being developed to fill the gap between generic information and full personalised advice.

- US SEC: AI tools providing personalised investment recommendations may constitute regulated investment advisory activity.

- EU MiFID II: Direct investment advice is a regulated activity. No publicly available AI tool is currently authorised to provide it under EU rules.

- General regulator advice: Always verify AI-generated financial guidance against trusted, regulated sources before acting on it.

AI as a Research Tool vs AI as an Adviser

The most important distinction for consumers to understand is the difference between using AI as a research tool and relying on it as a financial adviser. These are fundamentally different activities with very different risk profiles — and the evidence suggests that consumers who keep them separate get much more from AI without exposing themselves to the risks that regulators are most concerned about.As a research tool, AI is powerful and generally reliable. It can explain how different asset classes work, compare the historical performance of fund types, summarise news about a sector, help you understand a financial product's terms, or calculate how much you would need to save monthly to reach a retirement goal at a given return assumption. None of these activities involve personalised advice — they are information and calculations that anyone can verify.

As an adviser — providing specific recommendations about what you personally should buy, sell, or hold based on your individual financial situation — AI is operating in a domain it is not yet equipped for and is not regulated to provide. It does not know your tax situation, your liabilities, your dependants, your risk tolerance, or your full investment history. It may present general guidance as personalised advice without the caveats that would protect a less financially informed investor.

The 54% of Investing.com survey respondents who said they trust AI analysis only somewhat and typically verify it using other sources are approaching these tools in exactly the right way. They are using AI as one input among several, not as the final authority. The 23% who say they trust AI mostly or completely are the group that regulators and financial professionals are most concerned about.

How to Use AI Wisely for Investment Decisions

Based on the current evidence, the research evaluations, and the regulatory guidance, here is how to get the genuine benefits of AI for financial planning while protecting yourself from the risks.A sensible framework for using AI in your investing

- Use AI for education and explanation: Asking AI to explain what an ETF is, how compound interest works, or what dollar-cost averaging means is low-risk and high-value. AI excels at making financial concepts accessible.

- Use AI for research support, not final decisions: Let AI summarise a company's earnings, compare fund fee structures, or outline the pros and cons of different account types. Then verify the specifics with the fund provider, the company's own filings, or a regulated source.

- Always verify specific figures independently: Contribution limits, tax thresholds, interest rates, and regulatory rules change regularly. Always cross-check any specific numbers AI gives you with official sources (IRS.gov, FCA.org.uk, SEC.gov).

- Do not share personal financial details with public AI tools: Telling ChatGPT your full savings balance, income, and National Insurance number to get personalised advice creates a data privacy risk and still will not produce regulated advice.

- Treat AI recommendations as a starting point, not an endpoint: Use AI to identify questions to ask, topics to research, and options to explore — then verify and decide with independent sources or a regulated professional.

- Know when to use a human: For major financial decisions — significant lump-sum investments, retirement planning, estate planning, tax optimisation — the cost of professional advice is usually justified. Many robo-advisers offer a hybrid model with access to human advisers for complex questions.

CONCLUSION

The shift toward AI in consumer financial decision-making is not a fad. With 62% of US retail investors and 49% of global consumers already using AI for savings and investment decisions, and with adoption rates climbing fastest among the youngest and most digitally fluent generations, artificial intelligence has become a structural part of how millions of people engage with their own finances.The most important message from the evidence is nuanced: AI is a genuinely powerful tool for financial research, education, and analysis — and a risky substitute for personalised, regulated financial advice. Consumers who use AI as one informed input among several, who verify the specifics they are given, and who understand the limits of what a general-purpose chatbot can reliably provide, are well-positioned to benefit from these tools. Those who treat AI as a trusted financial adviser with the full picture of their situation are taking on a risk that regulators have been explicit about: there is no safety net when things go wrong.

Frequently Asked Questions

How many consumers are using AI for investment decisions?

According to an Investing.com survey of 938 US adult investors conducted in March 2026, 62% had used AI tools to assist with investment decisions. A larger EY survey of 18,000 consumers across 23 countries, released the same month, found that 49% of global consumers had used AI for savings and investment decisions in the past six months. A TD Bank survey found 55% of US consumers using AI for financial management decisions.What is the most popular AI tool for investment advice?

ChatGPT is the most widely used AI tool for financial decisions across multiple surveys. The Investing.com survey found 54% of AI-using investors had used ChatGPT for investment research. The J.D. Power survey found it dominant among consumers under 40. A Lloyds Banking Group study of 5,000 UK consumers also identified ChatGPT as the top tool, with Google Gemini second. Microsoft Copilot, Meta AI, Apple Siri, and Amazon Alexa were all used but at much lower rates.Is AI investment advice regulated?

No. General-purpose AI tools like ChatGPT, Gemini, and Claude are not regulated financial services products. The UK's FCA has explicitly stated that advice from these tools is not covered by the Financial Ombudsman Service or Financial Services Compensation Scheme. In the US, the SEC has indicated that AI tools providing personalised investment recommendations may constitute regulated investment advisory activity, but no publicly available chatbot is currently authorised to provide such advice. If you act on AI-generated investment advice and lose money, you have no regulatory recourse.Why are so many young people turning to AI for financial advice?

Primarily because affordable human financial advice is increasingly difficult to access. In the UK, the proportion of financial advisers accepting clients with less than £50,000 has halved over six years. In the US, hourly planning fees from CFPs run to $150 to $300. For younger, lower-wealth investors who are digitally comfortable, AI fills a vacuum left by advisers who no longer serve their asset level. Gen Z adoption of AI for financial decisions reached 68% globally in EY's 2026 survey and 77% in TD Bank's US survey.Can you trust AI for investment advice?

For financial education, research support, and explanation of concepts — yes, with appropriate verification. For personalised investment recommendations specific to your financial situation — no, for several reasons: AI does not know your full financial picture, it can present outdated figures confidently, it is prone to hallucination on niche topics, and it provides no regulatory protection. The Investing.com survey found 54% of investors only trust AI analysis somewhat and verify it elsewhere. That is the right approach.What does AI do well in financial planning?

AI performs well at explaining financial concepts, summarising complex documents, comparing options at a high level, calculating illustrative projections, and answering general knowledge questions about how financial products work. Nearly 40% of Investing.com respondents said AI helps them analyse market data faster, and 15% said it helps reduce emotional decision-making. These are genuine advantages for investors who use AI as a research tool rather than a decision-maker.What is the FCA doing about AI in investing?

The UK Financial Conduct Authority opened a formal review of AI's implications for retail investors in January 2026, examining how AI might evolve for consumers, firms, and regulators. It has issued clear warnings that general-purpose AI tools are not regulated and provide no consumer protection. It is also developing a new 'targeted support' regulatory category — scenario-based financial guidance sitting between generic information and full personalised advice — which the FCA's deputy CEO has described as potentially 'game-changing' for access to financial help.References

Investing.com — Nearly Two-Thirds of Retail Investors Now Use AI to Inform Investment Decisions (April 2026) https://www.investorideas.com/news/2026/technology/04061-ai-retail-investing-survey.asp, EY — Nearly Half of Global Consumers Now Use AI to Guide Savings and Investment Decisions (March 2026) https://www.ey.com/en_gl/newsroom/2026/04/nearly-half-of-global-consumers-now-use-ai-to-guide-savings-and-investment-decisions, ABA Banking Journal — Bank Surveys Find Consumers Increasingly Turning to AI for Financial Advice (April 2026) https://bankingjournal.aba.com/2026/04/bank-surveys-find-consumers-increasingly-turning-to-ai-for-financial-advice/, ResultSense — Consumers Using AI for Financial Advice: EY Survey and FCA Warning (April 2026) https://www.resultsense.com/news/2026-04-24-consumers-ai-financial-advice-fca, ResultSense — 40% of Britons Use AI Chatbots for Financial Advice (February 2026) https://www.resultsense.com/news/2026-02-17-priced-out-britons-turn-to-ai-for-financial-advice, LendingTree — AI Chatbot Users: Survey on AI Influence on Financial Decisions (September 2025) https://www.lendingtree.com/credit-cards/study/ai-chatbot-users/, Euronews — Personal Finance and AI: Should You Trust ChatGPT's Investment Advice? (October 2025) https://www.euronews.com/business/2025/10/30/personal-finance-and-ai-should-you-trust-chatgpts-investment-advice, ABA Banking Journal — Survey: Consumers Increasingly Turn to AI for Financial Advice (September 2025) https://bankingjournal.aba.com/2025/09/survey-consumers-increasingly-turn-to-ai-for-financial-advice/, Traders Magazine — Nearly Two-Thirds of Retail Investors Use AI to Inform Investment Decisions https://www.tradersmagazine.com/xtra/nearly-two-thirds-of-retail-investors-use-ai-to-inform-investment-decisions/FCA — Consumer Information: AI Tools and Financial Decisions https://www.fca.org.uk/consumers

0 Comments Comments