Taxes

How to Legally Reduce Your Tax in the UK 2026/27

Every UK taxpayer has the legal right to use every allowance, relief, and exemption that Parliament has provided. Most people use only a fraction of them. This guide explains — in plain English — exactly how to reduce your tax bill legally using the reliefs available in 2026/27.

Before diving into strategies for reducing your tax bill, it is important to be clear about a distinction that is often confused: the difference between tax avoidance, tax evasion, and tax planning.

Tax evasion is illegal. It means deliberately concealing income, falsifying records, or lying to HMRC in order to pay less tax than you legally owe. It is a criminal offence that can result in prosecution, substantial fines, and imprisonment. This guide has nothing to do with tax evasion and does not discuss it further.

Tax avoidance, in its aggressive form, refers to arrangements that use the letter of the law to reduce a tax liability in ways that Parliament clearly did not intend. HMRC has extensive powers to challenge and unwind aggressive avoidance schemes, many of which have been retrospectively legislated against. This guide does not cover aggressive avoidance schemes either.

What this guide covers is tax planning — the perfectly legal, HMRC-endorsed practice of arranging your affairs to make full use of the allowances, reliefs, exemptions, and deductions that Parliament has deliberately written into tax law. Using your ISA allowance, making pension contributions, claiming the Marriage Allowance, and deducting allowable business expenses are all examples of tax planning. HMRC expects and encourages taxpayers to use these provisions. Every strategy in this guide is fully HMRC-approved and used by millions of UK taxpayers every year.

Every individual has the right to arrange their tax affairs within the law. Tax planning means using reliefs and allowances that Parliament specifically intended taxpayers to use.

— HMRC — TAX AVOIDANCE: AN INTRODUCTION

This sounds obvious, but many people miss savings here in less obvious ways. If you have a non-working or low-earning spouse or civil partner, consider whether income-producing assets — rental property, savings accounts, investment accounts — can be held in their name rather than yours, or jointly. Income shifted to a lower or non-earner uses their allowance and lower tax bands, reducing the household's overall tax bill. This is entirely legal and widely done, provided the ownership is genuine and reflects the underlying economic reality.

If your income exceeds £100,000, your personal allowance is reduced by £1 for every £2 of adjusted net income above £100,000, disappearing entirely at £125,140. This creates an effective marginal rate of 60% on income between £100,000 and £125,140 — one of the most punishing rates in the UK tax system and one that is easily avoided with proper pension planning. Pension contributions reduce your adjusted net income, and a contribution that brings your income from £110,000 back below £100,000 restores your full personal allowance, providing tax relief of up to 60p per £1 contributed in that range.

For 2026/27, you can contribute up to 100% of your UK earnings to a pension in a given year, subject to a maximum annual allowance of £60,000 (which includes both your contributions and any employer contributions). You can also carry forward unused annual allowance from the previous three tax years, potentially allowing much larger one-off contributions if your earnings support them. Anyone with a workplace pension should also ensure they are receiving the maximum employer match — this is effectively free money and should always be maximised before anything else.

* Where pension contributions restore a personal allowance that would otherwise be lost due to income exceeding £100,000.

There are four main types of ISA: a Cash ISA (straightforward tax-free savings), a Stocks and Shares ISA (tax-free investment in funds, shares, and bonds), an Innovative Finance ISA (peer-to-peer lending — higher risk), and a Lifetime ISA (designed for first-time buyers or retirement, with a 25% government bonus on contributions up to £4,000 per year for those aged 18 to 39). Married couples and civil partners each have their own £20,000 allowance, so a couple can shelter £40,000 per year from tax.

The compounding benefit of an ISA grows over time. A basic-rate taxpayer investing in a straightforward index fund inside an ISA may not notice much difference in the early years. But over ten or twenty years, the absence of income tax on dividends and capital gains tax on growth can result in meaningfully higher returns compared with identical investments held outside an ISA. For higher-rate taxpayers who pay 40% tax on dividend income and would face capital gains tax charges on large investment gains, the benefit is even more significant.

The ISA allowance is a use-it-or-lose-it annual benefit — it does not carry forward to the next tax year. Prioritising your ISA subscription each April (at the start of the new tax year) maximises the time your money spends sheltered from tax.

HMRC estimates that around 2 million eligible couples have not claimed the Marriage Allowance. Claiming takes around five minutes at gov.uk/marriage-allowance and is free.

Pension salary sacrifice (covered in Section 3) is the most widely available and tax-efficient form of this arrangement. But a range of other employer-administered benefits can be obtained through salary sacrifice at significant tax savings.

An important caveat: salary sacrifice reduces your gross pay for National Insurance purposes, which may slightly reduce your state pension entitlement, Statutory Maternity Pay, and Statutory Sick Pay calculations. For most people the tax savings outweigh this, but it is worth checking the figures if you are close to key NI thresholds.

Several legal strategies can significantly reduce your CGT liability. First, use your annual exempt amount every year — like the ISA allowance, it cannot be carried forward, so there is no benefit to not using it. Consider realising gains each year up to the £3,000 threshold, particularly if you are holding assets with large unrealised gains that you intend to sell eventually. Second, if you have losses from other investments, realise them in the same tax year to set against gains — a loss on one holding can offset a gain on another, potentially reducing your taxable gain to zero.

Third, if you are planning to sell an investment that has appreciated significantly, consider transferring it to a spouse or civil partner before selling if they pay a lower rate of CGT or have unused annual exempt amount. Inter-spouse transfers are made at no gain or loss, preserving the original base cost, but the subsequent sale is treated as the spouse's disposal and uses their rates and allowances. This is particularly valuable where one partner is a non-taxpayer or basic-rate taxpayer and the other is a higher-rate taxpayer. Finally, where possible, hold investments within an ISA or pension wrapper, where CGT does not apply at all.

Under Gift Aid, a charity can claim 25p from HMRC for every £1 you donate, at no extra cost to you. If you are a higher-rate taxpayer, you can claim back the additional 20% tax relief yourself: a £100 Gift Aid donation effectively costs you £75 after claiming the full relief. Additional-rate taxpayers can claim a total of 25% relief, meaning a £100 donation costs £68.75.

You can also extend your basic-rate tax band by the grossed-up value of your Gift Aid donations, which can pull income out of the higher-rate band and reduce the amount of income taxed at 40%. If you are close to a tax threshold — for example, if your income is slightly above £50,270 (the higher-rate threshold) — a Gift Aid donation can reduce your effective income below that threshold and save you the 40% rate on that portion of income.

To claim higher or additional-rate Gift Aid relief, include your donations on your self-assessment return. Make sure you sign a Gift Aid declaration with each charity you donate to — without this, the relief cannot be claimed by either you or the charity. You can sign a single declaration to cover all future donations to a given charity.

The dividend allowance for 2026/27 is £500. Dividend income above this threshold is taxed at 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate) — in every case meaningfully lower than the equivalent income tax rates of 20%, 40%, and 45%. Crucially, dividends also do not attract National Insurance contributions, whereas salary is subject to both employee NI (8% up to the upper earnings limit, then 2%) and employer NI (13.8%).

The optimal structure for most owner-managed companies involves taking a small salary up to the NI primary threshold (£12,570 in 2026/27, at which point the salary becomes National Insurance-free while still being high enough to qualify for a year of state pension entitlement), and then drawing the remainder of required income as dividends. This structure saves both income tax and National Insurance on the dividend portion of income compared with taking the same sum entirely as salary. Every company's circumstances are different, however, and the optimal salary/dividend split depends on corporation tax rates, personal tax rates, IR35 status, and other factors — always take specific advice from an accountant before implementing this approach.

The single biggest mistake most UK taxpayers make is not being proactive. They pay their taxes without checking whether they are using their ISA allowance, whether they have claimed the Marriage Allowance, whether their pension contributions could be higher, or whether there are expenses they could legitimately deduct. Small changes, consistently applied year after year, compound into significant lifetime tax savings. The best time to start is always the beginning of the new tax year. The second best time is now.

TABLE OF CONTENTS

- Tax Avoidance vs Tax Evasion: Understanding the Difference

- Use Your Personal Allowance Fully

- Pension Contributions: The Most Powerful Tax Relief Available

- ISAs: Tax-Free Savings and Investment

- Marriage Allowance and Married Couple's Allowance

- Salary Sacrifice Schemes

- Capital Gains Tax Planning

- Gift Aid: Tax Relief on Charitable Giving

- Claim All Your Allowable Expenses

- Dividends: The Tax-Efficient Way to Take Income

- Additional Tips for Specific Groups

- Conclusion

- Frequently Asked Questions

- References

Tax Avoidance vs Tax Evasion: Understanding the Difference

Before diving into strategies for reducing your tax bill, it is important to be clear about a distinction that is often confused: the difference between tax avoidance, tax evasion, and tax planning.Tax evasion is illegal. It means deliberately concealing income, falsifying records, or lying to HMRC in order to pay less tax than you legally owe. It is a criminal offence that can result in prosecution, substantial fines, and imprisonment. This guide has nothing to do with tax evasion and does not discuss it further.

Tax avoidance, in its aggressive form, refers to arrangements that use the letter of the law to reduce a tax liability in ways that Parliament clearly did not intend. HMRC has extensive powers to challenge and unwind aggressive avoidance schemes, many of which have been retrospectively legislated against. This guide does not cover aggressive avoidance schemes either.

What this guide covers is tax planning — the perfectly legal, HMRC-endorsed practice of arranging your affairs to make full use of the allowances, reliefs, exemptions, and deductions that Parliament has deliberately written into tax law. Using your ISA allowance, making pension contributions, claiming the Marriage Allowance, and deducting allowable business expenses are all examples of tax planning. HMRC expects and encourages taxpayers to use these provisions. Every strategy in this guide is fully HMRC-approved and used by millions of UK taxpayers every year.

Every individual has the right to arrange their tax affairs within the law. Tax planning means using reliefs and allowances that Parliament specifically intended taxpayers to use.

— HMRC — TAX AVOIDANCE: AN INTRODUCTION

Use Your Personal Allowance Fully

The most fundamental tax-saving opportunity for any UK taxpayer is to ensure they are using their Personal Allowance — the amount of income they can earn before paying any income tax. For 2026/27, the standard Personal Allowance is £12,570.This sounds obvious, but many people miss savings here in less obvious ways. If you have a non-working or low-earning spouse or civil partner, consider whether income-producing assets — rental property, savings accounts, investment accounts — can be held in their name rather than yours, or jointly. Income shifted to a lower or non-earner uses their allowance and lower tax bands, reducing the household's overall tax bill. This is entirely legal and widely done, provided the ownership is genuine and reflects the underlying economic reality.

If your income exceeds £100,000, your personal allowance is reduced by £1 for every £2 of adjusted net income above £100,000, disappearing entirely at £125,140. This creates an effective marginal rate of 60% on income between £100,000 and £125,140 — one of the most punishing rates in the UK tax system and one that is easily avoided with proper pension planning. Pension contributions reduce your adjusted net income, and a contribution that brings your income from £110,000 back below £100,000 restores your full personal allowance, providing tax relief of up to 60p per £1 contributed in that range.

Pension Contributions: The Most Powerful Tax Relief Available

Pension contributions are almost certainly the single most valuable tax-relief mechanism available to UK individuals. Every pound you contribute to a pension comes back with tax relief attached — and for higher and additional-rate taxpayers, that relief is extraordinarily generous.How pension tax relief works

When you contribute to a personal pension, basic-rate tax relief of 20% is added automatically by the pension provider through the relief-at-source system. This means that for every £80 you contribute, your pension actually receives £100 — a 25% return before the money has even been invested. If you are a higher-rate taxpayer (paying 40%), you can claim a further 20% through your self-assessment tax return, meaning your effective cost of a £100 pension contribution is just £60. Additional-rate taxpayers (45%) pay just £55 for every £100 that goes into their pension.For 2026/27, you can contribute up to 100% of your UK earnings to a pension in a given year, subject to a maximum annual allowance of £60,000 (which includes both your contributions and any employer contributions). You can also carry forward unused annual allowance from the previous three tax years, potentially allowing much larger one-off contributions if your earnings support them. Anyone with a workplace pension should also ensure they are receiving the maximum employer match — this is effectively free money and should always be maximised before anything else.

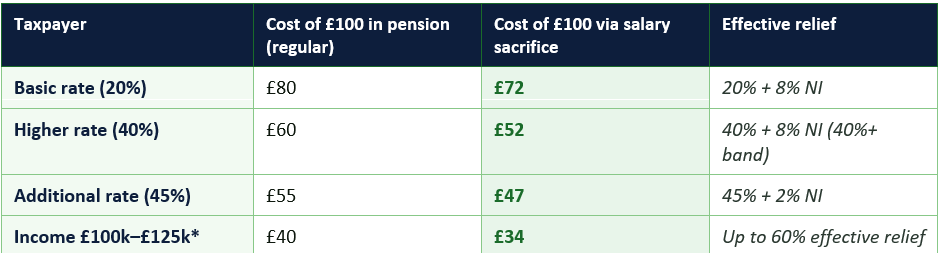

Salary sacrifice pensions: saving National Insurance too

If your employer offers a salary sacrifice pension scheme, you should strongly consider using it. Under salary sacrifice, you agree to receive a lower gross salary in exchange for higher employer pension contributions. Because the contribution is made by the employer rather than the employee, neither you nor your employer pays National Insurance on the sacrificed amount. For a basic-rate taxpayer, salary sacrifice saves both 20% income tax and 8% employee NI — a combined relief of 28% — on every pound redirected into the pension. For a higher-rate taxpayer, the combined relief rises to 48%.* Where pension contributions restore a personal allowance that would otherwise be lost due to income exceeding £100,000.

ISAs: Tax-Free Savings and Investment

An Individual Savings Account (ISA) is the simplest and most accessible tax-efficient vehicle available to UK adults. Money held inside an ISA grows completely free of income tax and capital gains tax, and there is no tax to pay when you withdraw funds. The annual ISA allowance for 2026/27 is £20,000 per person.There are four main types of ISA: a Cash ISA (straightforward tax-free savings), a Stocks and Shares ISA (tax-free investment in funds, shares, and bonds), an Innovative Finance ISA (peer-to-peer lending — higher risk), and a Lifetime ISA (designed for first-time buyers or retirement, with a 25% government bonus on contributions up to £4,000 per year for those aged 18 to 39). Married couples and civil partners each have their own £20,000 allowance, so a couple can shelter £40,000 per year from tax.

The compounding benefit of an ISA grows over time. A basic-rate taxpayer investing in a straightforward index fund inside an ISA may not notice much difference in the early years. But over ten or twenty years, the absence of income tax on dividends and capital gains tax on growth can result in meaningfully higher returns compared with identical investments held outside an ISA. For higher-rate taxpayers who pay 40% tax on dividend income and would face capital gains tax charges on large investment gains, the benefit is even more significant.

The ISA allowance is a use-it-or-lose-it annual benefit — it does not carry forward to the next tax year. Prioritising your ISA subscription each April (at the start of the new tax year) maximises the time your money spends sheltered from tax.

Marriage Allowance and Married Couple's Allowance

Two specific reliefs exist for married couples and civil partners that are frequently unclaimed, despite being straightforward to use.Marriage Allowance

The Marriage Allowance allows one partner in a married couple or civil partnership to transfer up to £1,260 of their unused personal allowance to the other. This is only available where one partner's income is below the personal allowance (£12,570 in 2026/27) and the other is a basic-rate taxpayer. The benefit is a reduction in the higher earner's tax bill of up to £252 per year (20% of £1,260). You can also backdate a claim for up to four previous tax years, potentially generating a lump-sum repayment of over £1,000.HMRC estimates that around 2 million eligible couples have not claimed the Marriage Allowance. Claiming takes around five minutes at gov.uk/marriage-allowance and is free.

Married Couple's Allowance

A separate, more generous allowance — the Married Couple's Allowance — is available where at least one partner was born before 6 April 1935. This allowance provides a direct reduction in tax of between £427 and £1,108 per year in 2026/27. If your household includes someone in this age bracket, it is well worth checking eligibility at gov.uk.Salary Sacrifice Schemes

Salary sacrifice is a formal arrangement between you and your employer in which you agree to give up part of your gross salary in exchange for a non-cash benefit of equivalent value. Because the sacrifice reduces your gross pay, you pay both income tax and National Insurance only on your lower salary — generating tax savings on top of whatever the benefit itself is worth.Pension salary sacrifice (covered in Section 3) is the most widely available and tax-efficient form of this arrangement. But a range of other employer-administered benefits can be obtained through salary sacrifice at significant tax savings.

Common salary sacrifice benefits and their tax advantages

- Workplace pension: Save both income tax (20–45%) and employee NI (2–8%) on redirected salary — the most valuable salary sacrifice option for most employees.

- Cycle to Work scheme: Purchase a bicycle and cycling equipment up to £3,000 (higher limits with some employers) tax-free, saving 32–47% on the cost compared with buying outright.

- Electric vehicle salary sacrifice: Lease a fully electric car through your employer at significantly reduced cost because Benefit-in-Kind tax rates on EVs are just 3% in 2026/27 — making this one of the most generous employer benefits currently available.

- Childcare vouchers (legacy scheme): No longer open to new entrants since October 2018, but if you joined before that date you may still be in a grandfathered scheme that saves up to £933 per year in tax and NI.

- Annual travel pass / season ticket loans: Some employers offer season ticket loans through salary sacrifice that allow you to spread the cost of an annual travel pass pre-tax.

An important caveat: salary sacrifice reduces your gross pay for National Insurance purposes, which may slightly reduce your state pension entitlement, Statutory Maternity Pay, and Statutory Sick Pay calculations. For most people the tax savings outweigh this, but it is worth checking the figures if you are close to key NI thresholds.

Capital Gains Tax Planning

Capital Gains Tax (CGT) is charged on the profit you make when you sell certain assets — including shares, property (other than your main home), and other investments — that have increased in value. For 2026/27, the annual CGT exemption is £3,000, meaning you pay no CGT on the first £3,000 of gains in any tax year. Beyond that, gains are taxed at 18% or 24% on residential property (for basic and higher-rate taxpayers respectively) and at 18% or 24% on other assets from 30 October 2024.Several legal strategies can significantly reduce your CGT liability. First, use your annual exempt amount every year — like the ISA allowance, it cannot be carried forward, so there is no benefit to not using it. Consider realising gains each year up to the £3,000 threshold, particularly if you are holding assets with large unrealised gains that you intend to sell eventually. Second, if you have losses from other investments, realise them in the same tax year to set against gains — a loss on one holding can offset a gain on another, potentially reducing your taxable gain to zero.

Third, if you are planning to sell an investment that has appreciated significantly, consider transferring it to a spouse or civil partner before selling if they pay a lower rate of CGT or have unused annual exempt amount. Inter-spouse transfers are made at no gain or loss, preserving the original base cost, but the subsequent sale is treated as the spouse's disposal and uses their rates and allowances. This is particularly valuable where one partner is a non-taxpayer or basic-rate taxpayer and the other is a higher-rate taxpayer. Finally, where possible, hold investments within an ISA or pension wrapper, where CGT does not apply at all.

Gift Aid: Tax Relief on Charitable Giving

If you make donations to registered charities in the UK, Gift Aid allows the charity to claim back basic-rate tax on your donation — and if you are a higher or additional-rate taxpayer, you can claim further relief through your self-assessment return.Under Gift Aid, a charity can claim 25p from HMRC for every £1 you donate, at no extra cost to you. If you are a higher-rate taxpayer, you can claim back the additional 20% tax relief yourself: a £100 Gift Aid donation effectively costs you £75 after claiming the full relief. Additional-rate taxpayers can claim a total of 25% relief, meaning a £100 donation costs £68.75.

You can also extend your basic-rate tax band by the grossed-up value of your Gift Aid donations, which can pull income out of the higher-rate band and reduce the amount of income taxed at 40%. If you are close to a tax threshold — for example, if your income is slightly above £50,270 (the higher-rate threshold) — a Gift Aid donation can reduce your effective income below that threshold and save you the 40% rate on that portion of income.

To claim higher or additional-rate Gift Aid relief, include your donations on your self-assessment return. Make sure you sign a Gift Aid declaration with each charity you donate to — without this, the relief cannot be claimed by either you or the charity. You can sign a single declaration to cover all future donations to a given charity.

Claim All Your Allowable Expenses

Many employed and self-employed people fail to claim all the expenses they are entitled to deduct from their taxable income. The rules differ depending on whether you are employed or self-employed, but in both cases there is likely to be more you can claim than you currently do.Employed workers

As an employee, you can claim a deduction for expenses you have incurred wholly, exclusively, and necessarily in the performance of your duties — and which your employer has not reimbursed. Common allowable expenses include professional subscriptions to bodies approved by HMRC, the cost of tools and equipment used in work, mileage above the employer-reimbursed amount (at HMRC's approved 45p per mile for the first 10,000 miles, then 25p per mile), and the cost of a home office if you work from home under a formal arrangement. HMRC also offers a simplified flat-rate allowance for working from home of £6 per week without needing to keep detailed records.Self-employed and sole traders

Self-employed people can deduct a much broader range of expenses from their business income, reducing their taxable profit. Allowable expenses include office costs, travel and vehicle costs (using actual costs or HMRC's simplified mileage rates), staff costs, raw materials and stock, marketing and advertising, professional fees (accountant, solicitor), relevant training courses, and a proportion of household bills if working from home. Use HMRC's online guidance on allowable expenses for self-employed people or speak to an accountant to make sure you are claiming everything you are entitled to.Dividends: The Tax-Efficient Way to Take Income

For company directors and business owners who have control over how they extract profits from their business, dividends remain a significantly more tax-efficient way to take income than salary — despite reductions in the dividend allowance in recent years.The dividend allowance for 2026/27 is £500. Dividend income above this threshold is taxed at 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate) — in every case meaningfully lower than the equivalent income tax rates of 20%, 40%, and 45%. Crucially, dividends also do not attract National Insurance contributions, whereas salary is subject to both employee NI (8% up to the upper earnings limit, then 2%) and employer NI (13.8%).

The optimal structure for most owner-managed companies involves taking a small salary up to the NI primary threshold (£12,570 in 2026/27, at which point the salary becomes National Insurance-free while still being high enough to qualify for a year of state pension entitlement), and then drawing the remainder of required income as dividends. This structure saves both income tax and National Insurance on the dividend portion of income compared with taking the same sum entirely as salary. Every company's circumstances are different, however, and the optimal salary/dividend split depends on corporation tax rates, personal tax rates, IR35 status, and other factors — always take specific advice from an accountant before implementing this approach.

Additional Tips for Specific Groups

Several additional legal tax-reduction opportunities are available to specific groups of taxpayers.Additional reliefs by taxpayer type

- Landlords: Ensure you are claiming all allowable expenses — mortgage interest (as a 20% tax credit), maintenance and repairs, letting agent fees, insurance, and professional fees. Consider whether incorporation of the rental portfolio would be beneficial given your specific circumstances.

- Investors: Use your £20,000 ISA allowance every year and your £3,000 CGT annual exempt amount. Bed-and-ISA (selling investments and re-buying them inside an ISA) can crystallise gains within the annual exempt amount and shelter future growth tax-free.

- High earners above £100k: Pension contributions that reduce your adjusted net income back to or below £100,000 restore your full personal allowance and generate effective tax relief of up to 60% — this is one of the most valuable opportunities in the UK tax system.

- Parents: The £2,000-per-child government top-up through Tax-Free Childcare (for every £8 deposited, the government adds £2) is a 25% return on money you would spend on childcare anyway. If your income is approaching £100,000, consider pension contributions to stay below the High Income Child Benefit Charge threshold.

- Pensioners: The State Pension is taxable income but is paid gross. Ensure that your tax code correctly reflects your non-savings income and that you are using all available allowances. Pension Credit and Attendance Allowance are tax-free and should be claimed if eligible.

- Entrepreneurs: Business Asset Disposal Relief (formerly Entrepreneurs' Relief) reduces CGT on qualifying business disposals to 10% on the first £1 million of lifetime qualifying gains. Enterprise Investment Scheme (EIS) investments attract 30% income tax relief and CGT deferral/exemption — though these carry significant investment risk.

CONCLUSION

The UK tax system contains a substantial number of reliefs, allowances, and exemptions that Parliament has deliberately created to encourage savings, investment, charitable giving, homeownership, retirement planning, and entrepreneurship. Every strategy in this guide is fully legal, actively supported by HMRC, and used by millions of UK taxpayers every year.The single biggest mistake most UK taxpayers make is not being proactive. They pay their taxes without checking whether they are using their ISA allowance, whether they have claimed the Marriage Allowance, whether their pension contributions could be higher, or whether there are expenses they could legitimately deduct. Small changes, consistently applied year after year, compound into significant lifetime tax savings. The best time to start is always the beginning of the new tax year. The second best time is now.

0 Comments Comments