Financial Literacy

How to Manage Money on Low Income and Get What You Want

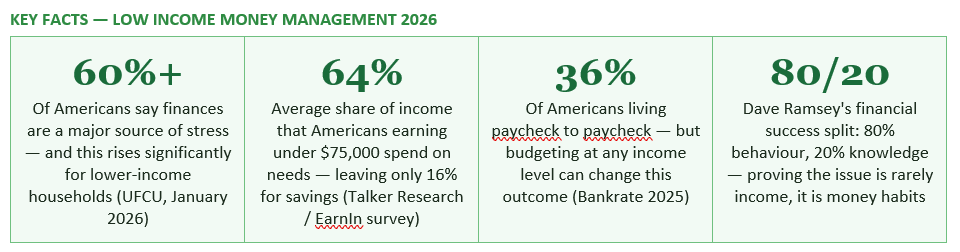

More than 60% of Americans say finances are a major source of stress, according to UFCU's January 2026 financial guidance. And a Talker Research / EarnIn survey found that Americans earning under $75,000 put an average of 64% of income toward needs — leaving just 16% for savings. But low income is not the same as no options. The difference between people who make progress financially on a modest income and those who do not is almost never income level. It is intentionality. This guide gives you the practical framework.

SmartMoneyTrek's March 2026 budgeting guide states this directly: 'The key difference is not how much they earn, but how intentionally they manage their money. Many people with modest incomes still manage to pay their bills, avoid unnecessary debt, and build small savings.' UFCU's January 2026 financial guidance reinforces it: 'A budget works at any income level — whether you earn regularly, occasionally, or not at all. A budget should be based on a person's income, not their ideal situation.'

The mindset shift that makes this possible is moving from passive to active. Passive money management means spending until the account is empty and wondering where it went. Active money management means deciding in advance where every dollar goes — before the money arrives, before the impulse buy, before the end-of-month panic. Dave Ramsey describes this as giving every dollar a job. It does not require a high income to do this. It requires the decision to do it. And that decision is the most consequential financial choice available to anyone at any income level.

Equally important is giving yourself permission to want things. Managing money on a low income is not a lifetime sentence of joyless deprivation. It is a strategy for getting what genuinely matters to you — by making deliberate choices about what matters less — rather than spending reactively and ending up with none of the things that matter most.

Budgeting on a low income is not about limiting your life; it's about maximising every single dollar you have. It's your strategic plan for stability in an unpredictable financial world.

— AZTECH TRAINING — HOW TO BUDGET WITH LOW INCOME: PRACTICAL TIPS AND STRATEGIES

Then categorise: housing, food, transport, utilities, debt payments, and all discretionary spending. UFCU recommends categorising into essentials (rent, groceries, transportation) and non-essentials (coffee runs, streaming, dining out), and estimates irregular costs by averaging annual amounts across 12 months. The spending audit is almost always revealing — and the revelation is usually the most motivating thing that happens at the start of a budget journey.

.

.

Everything outside the Four Walls — debt payments, subscriptions, savings, entertainment — is addressed only after these four categories are covered for the month. This is not irresponsibility toward creditors; it is the correct prioritisation of survival-level expenses that protect your ability to earn income and maintain stability.

The GOBankingRates / EarnIn Talker Research survey found that Americans earning under $75,000 actually spend 64% on needs, 16% on wants, and 16% on savings. Wealthvieu's May 2026 guide acknowledges this reality explicitly: 'If you earn under $35,000, needs may take 70%+ of income. Priorities shift.' The solution is to adapt the percentages rather than abandon the framework. A realistic starting split for a low-income budget might be 65% needs / 15% wants / 20% savings — or even 70% needs / 10% wants / 20% savings if necessary.

The critical point is to protect the savings percentage even when everything else must adjust. Solutions Bank's April 2026 guidance notes: 'Not everyone starts with a perfect 50/30/20 breakdown. For many people, 20% is a stretch goal rather than a starting point. Even saving 5% to 10% and automating contributions can build momentum.' On a $2,000/month take-home income, 5% savings is $100 per month. It does not feel transformative. But automated consistently, it grows to $1,200 per year — which is a car repair fund, a travel fund, or the start of an emergency buffer. The percentage matters less than the habit.

A sinking fund is a designated savings pot for a specific, named goal. It is not an emergency fund — it is a planned expense fund. The principle is simple: instead of being blindsided by a large purchase (or putting it on a credit card), you identify it in advance, calculate how much it costs, divide that cost by the number of months you have before you need it, and set that amount aside each month.

Solutions Bank's April 2026 guide explains the mechanism: 'For non-monthly needs or annual or irregular expenses — car registration fees, school clothes, or holiday shopping — save for them using a sinking fund. Simply divide the yearly cost by twelve and set aside that smaller amount each month so you're prepared when the bill arrives.' This works for both mandatory irregular expenses (car insurance annual renewal, dentist visits, school supplies) and genuine desired purchases (a holiday, a new phone, Christmas gifts, a piece of furniture).

The power of the sinking fund on a low income is psychological as much as financial. It converts the experience of buying something you want from a moment of guilt and debt into a planned, guilt-free purchase. You saved for it. It is yours. You did not go into debt for it. And knowing that the money is being set aside each month eliminates the anxiety of the large bill appearing unexpectedly.

The practical implementation is straightforward. On payday, set up automatic transfers that fire before you have the opportunity to spend the money: a transfer to your emergency fund savings pot, a transfer to your largest sinking fund, and automatic direct debits for all essential bills on or just after the pay date. What remains in the account after these automatic movements is your spending money for the month — you cannot accidentally spend the savings because they have already moved.

This principle — pay yourself first by automating savings before spending — is one of the most consistently recommended strategies across every personal finance guide reviewed for this article. UFCU's January 2026 guide frames it as making savings non-negotiable: rather than saving whatever is left at the end of the month (which is typically nothing), automating savings at the start makes them as fixed as a rent payment. Even $25 automated on payday produces better results than $100 intended-but-not-transferred at month end.

The income-increase strategies that are most accessible for low-income households in 2026 do not require a new degree or a career change. They fall into three categories: maximising existing income, creating additional income streams, and accessing entitlements already owed.

InCharge's financial literacy guide frames the long-term relationship with budgeting correctly: 'It can change. It should change, in fact, along with changes to your financial situation. That's why it's important to continuously monitor your budget and adjust it as needed as your income grows or shrinks.' A budget is not a pass-fail test. It is a living document that reflects reality and evolves with it.

Practical motivation strategies include tracking visual progress on a specific goal — a printed chart showing the sinking fund balance growing toward a holiday or a new item you want — and celebrating the small wins that compound into large ones. Paying off a small debt, funding the first month of an emergency fund, completing the first subscription audit and seeing a lower bank total — these are real financial wins that deserve recognition. The emotional experience of financial progress, even on a small scale, is one of the strongest predictors of continued behaviour change.

Finally, the framing matters. Managing money on a low income is not a permanent punishment for being poor. It is a set of tools and habits that create more of what you want from your life — more security, less anxiety, the ability to plan ahead, and the satisfaction of getting things you want through your own deliberate effort rather than through debt that extracts a premium from your future self.

The 60% of Americans who say finances are a major source of stress are not all in that position because they earn too little. Many of them are in that position because money management on any income is a skill that is rarely taught and is difficult to learn alone. This guide is the starting point. The tools — a bank account, a spreadsheet or app, a named savings pot, a list of your actual spending — cost nothing. The decision to use them intentionally is what changes the outcome. And the outcome is not just a better bank balance. It is a life where you feel in control, where planned things happen because you planned them, and where you get what genuinely matters to you.

UFCU — Be Brave and Budget: 8 Low-Income Budgeting Tips to Take Control of Your Finance (January 2026) https://www.ufcu.org/resources/articles/detail/articles/2025/11/14/low-income-budgeting-tips

Wealthvieu — 50/30/20 Budget Rule 2026: How to Split Your Paycheck (May 2026) https://wealthvieu.com/personal-finance/budgeting-guide/50-30-20-rule/

Solutions Bank — 50/30/20 Budget Rule: Simple Math for Smarter Money (April 2026) https://www.solutions.bank/blog/post/50-30-20-budget-rule-simple-math-for-smarter-money

South State Bank — A Realistic Guide for Budgeting on a Limited Income (January 2026) https://www.southstatebank.com/personal/stories-and-insights/a-realistic-guide-for-budgeting-on-a-limited-income

AZTech Training — How to Budget with Low Income: Practical Tips and Strategies https://aztechtraining.com/articles/how-to-budget-with-low-income

InCharge — How to Budget Money on a Low Income https://www.incharge.org/financial-literacy/budgeting-saving/how-to-budget-money-on-low-income/

Albert.com — How to Budget Money on a Low Income https://albert.com/blog/how-to-budget-money-on-low-income

TABLE OF CONTENTS

- The Mindset Shift That Changes Everything

- Step 1 — Know Your Real Numbers

- Step 2 — The Four Walls: Needs That Come Before Everything Else

- Step 3 — Adapt the 50/30/20 Budget for a Low Income

- Step 4 — The Sinking Fund: How to Get What You Want Without Debt

- Step 5 — Automate the Small Stuff

- Step 6 — Cut Expenses Without Cutting Your Life

- Step 7 — Increase Your Income (Even Incrementally)

- Step 8 — Use Free Resources and Benefits You May Not Know About

- Staying Motivated: Progress Over Perfection

- Conclusion

- Frequently Asked Questions

- References

The Mindset Shift That Changes Everything

The most important thing to understand about managing money on a low income is also the most counter-intuitive: the amount you earn is not the primary variable that determines whether you make financial progress. The primary variable is how intentionally you manage what you have.SmartMoneyTrek's March 2026 budgeting guide states this directly: 'The key difference is not how much they earn, but how intentionally they manage their money. Many people with modest incomes still manage to pay their bills, avoid unnecessary debt, and build small savings.' UFCU's January 2026 financial guidance reinforces it: 'A budget works at any income level — whether you earn regularly, occasionally, or not at all. A budget should be based on a person's income, not their ideal situation.'

The mindset shift that makes this possible is moving from passive to active. Passive money management means spending until the account is empty and wondering where it went. Active money management means deciding in advance where every dollar goes — before the money arrives, before the impulse buy, before the end-of-month panic. Dave Ramsey describes this as giving every dollar a job. It does not require a high income to do this. It requires the decision to do it. And that decision is the most consequential financial choice available to anyone at any income level.

Equally important is giving yourself permission to want things. Managing money on a low income is not a lifetime sentence of joyless deprivation. It is a strategy for getting what genuinely matters to you — by making deliberate choices about what matters less — rather than spending reactively and ending up with none of the things that matter most.

Budgeting on a low income is not about limiting your life; it's about maximising every single dollar you have. It's your strategic plan for stability in an unpredictable financial world.

— AZTECH TRAINING — HOW TO BUDGET WITH LOW INCOME: PRACTICAL TIPS AND STRATEGIES

Step 1 — Know Your Real Numbers

Before you can make a plan, you need accurate information. Most people have a vague sense of their income and a very vague sense of their spending. Active money management requires specificity.Know your actual take-home income

Your real income for budgeting purposes is your net pay — the money that hits your bank account after tax, National Insurance (UK), Social Security, and any other deductions. Gross salary is largely irrelevant for day-to-day budgeting. If your income varies — because you work irregular hours, do gig work, freelance, or have seasonal income — South State Bank's January 2026 budgeting guide advises: 'If you have an irregular income, use your lowest monthly take-home pay to start.' This creates a floor — a minimum income figure you can plan around — so you are never caught short in a slower month. UFCU's guidance echoes this: 'If your income fluctuates, consider budgeting based on your lowest recent month. This creates a safety buffer for slower months.'Know where your money is actually going

The gap between where people think their money goes and where it actually goes is almost always significant. The practical action is a 30-day spending audit: for one month, record every single outgoing — every direct debit, every card transaction, every cash withdrawal. Use your bank's transaction history, your credit card statements, and your payment apps.Then categorise: housing, food, transport, utilities, debt payments, and all discretionary spending. UFCU recommends categorising into essentials (rent, groceries, transportation) and non-essentials (coffee runs, streaming, dining out), and estimates irregular costs by averaging annual amounts across 12 months. The spending audit is almost always revealing — and the revelation is usually the most motivating thing that happens at the start of a budget journey.

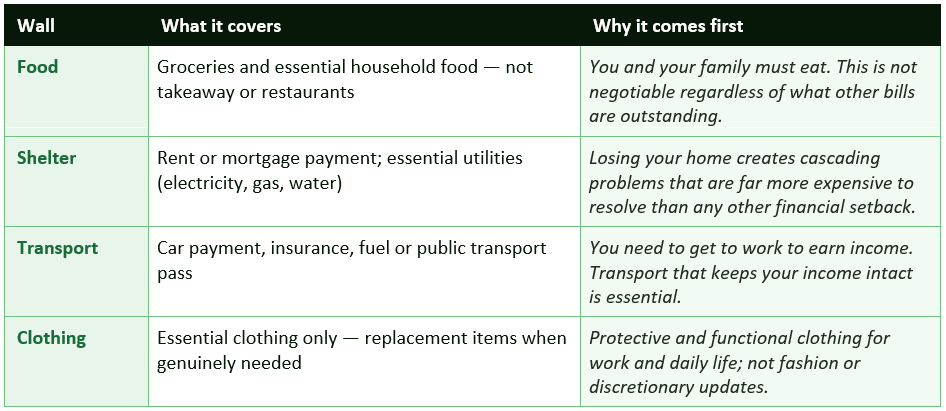

Step 2 — The Four Walls: Needs That Come Before Everything Else

Before any budget framework is applied, one principle must be established: certain expenses must be paid first, regardless of anything else. Dave Ramsey's Four Walls concept — widely cited in financial guidance including the Headway/Makeheadway March 2025 guide — defines the non-negotiable foundation of any low-income budget..Everything outside the Four Walls — debt payments, subscriptions, savings, entertainment — is addressed only after these four categories are covered for the month. This is not irresponsibility toward creditors; it is the correct prioritisation of survival-level expenses that protect your ability to earn income and maintain stability.

Step 3 — Adapt the 50/30/20 Budget for a Low Income

The 50/30/20 budget rule — allocate 50% of after-tax income to needs, 30% to wants, and 20% to savings — is a useful framework but was designed for median or above-median incomes. For low-income households, the standard split often does not work as published, because needs frequently consume more than 50% of a low income.The GOBankingRates / EarnIn Talker Research survey found that Americans earning under $75,000 actually spend 64% on needs, 16% on wants, and 16% on savings. Wealthvieu's May 2026 guide acknowledges this reality explicitly: 'If you earn under $35,000, needs may take 70%+ of income. Priorities shift.' The solution is to adapt the percentages rather than abandon the framework. A realistic starting split for a low-income budget might be 65% needs / 15% wants / 20% savings — or even 70% needs / 10% wants / 20% savings if necessary.

The critical point is to protect the savings percentage even when everything else must adjust. Solutions Bank's April 2026 guidance notes: 'Not everyone starts with a perfect 50/30/20 breakdown. For many people, 20% is a stretch goal rather than a starting point. Even saving 5% to 10% and automating contributions can build momentum.' On a $2,000/month take-home income, 5% savings is $100 per month. It does not feel transformative. But automated consistently, it grows to $1,200 per year — which is a car repair fund, a travel fund, or the start of an emergency buffer. The percentage matters less than the habit.

Step 4 — The Sinking Fund: How to Get What You Want Without Debt

The sinking fund is the specific mechanism that allows people on low incomes to get what they actually want — not by magic or by finding money they do not have, but by deciding in advance what they want and saving for it systematically in small increments.A sinking fund is a designated savings pot for a specific, named goal. It is not an emergency fund — it is a planned expense fund. The principle is simple: instead of being blindsided by a large purchase (or putting it on a credit card), you identify it in advance, calculate how much it costs, divide that cost by the number of months you have before you need it, and set that amount aside each month.

Solutions Bank's April 2026 guide explains the mechanism: 'For non-monthly needs or annual or irregular expenses — car registration fees, school clothes, or holiday shopping — save for them using a sinking fund. Simply divide the yearly cost by twelve and set aside that smaller amount each month so you're prepared when the bill arrives.' This works for both mandatory irregular expenses (car insurance annual renewal, dentist visits, school supplies) and genuine desired purchases (a holiday, a new phone, Christmas gifts, a piece of furniture).

The power of the sinking fund on a low income is psychological as much as financial. It converts the experience of buying something you want from a moment of guilt and debt into a planned, guilt-free purchase. You saved for it. It is yours. You did not go into debt for it. And knowing that the money is being set aside each month eliminates the anxiety of the large bill appearing unexpectedly.

Practical sinking fund examples — what to save for and how much

- Annual car insurance (UK/US): If your annual policy costs $1,200 and renews in 12 months, set aside $100 per month into a named pot. When renewal arrives, you pay in cash rather than spreading into expensive monthly instalments (which typically cost 20–30% more per year than annual payment).

- Christmas and gifts: Average UK household spends £500–£800 on Christmas. Divide by 12 = £42–£67 per month, starting in January. By December you have the full amount saved and spend nothing you did not plan.

- New phone or electronics: A $600 phone in 12 months requires $50 per month set aside in a specific named savings pot. In 12 months it is yours, without credit, without interest, without a monthly payment plan.

- Holiday or break: A £400 short break in 8 months requires £50 per month. This is achievable on almost any income as a deliberate savings decision — and it is the specific mechanism that makes 'treating yourself' financially sustainable rather than destructive.

- Emergency fund (the master sinking fund): SmartMoneyTrek's March 2026 guide and the CFPB both identify building an emergency fund as the most stabilising financial action for low-income households. Start with a target of $500 to $1,000 — a micro emergency fund that prevents small crises from becoming debt emergencies. Save $25 to $50 per month until it is funded.

Step 5 — Automate the Small Stuff

The single most effective behavioural trick in personal finance is automation — making savings and bill payments happen without any active decision required. Every time a financial decision requires willpower in the moment, there is a chance that willpower fails. When the decision is automated, it happens regardless of mood, tiredness, competing temptations, or a bad week.The practical implementation is straightforward. On payday, set up automatic transfers that fire before you have the opportunity to spend the money: a transfer to your emergency fund savings pot, a transfer to your largest sinking fund, and automatic direct debits for all essential bills on or just after the pay date. What remains in the account after these automatic movements is your spending money for the month — you cannot accidentally spend the savings because they have already moved.

This principle — pay yourself first by automating savings before spending — is one of the most consistently recommended strategies across every personal finance guide reviewed for this article. UFCU's January 2026 guide frames it as making savings non-negotiable: rather than saving whatever is left at the end of the month (which is typically nothing), automating savings at the start makes them as fixed as a rent payment. Even $25 automated on payday produces better results than $100 intended-but-not-transferred at month end.

Step 6 — Cut Expenses Without Cutting Your Life

The aim of an expense audit is not to eliminate everything enjoyable — it is to identify spending that is not actually producing value for you and redirect it to things that do. Most people, when they review spending carefully, find a combination of forgotten subscriptions, habitual purchases that bring no real satisfaction, and more expensive versions of things they could get cheaper without any quality reduction.Practical expense cuts that most households can make without feeling deprived

- Subscription audit — cancel and save: The average UK household spends £55–£90 per month on digital subscriptions; the average US household spends $219 per month (C+R Research 2022 data — the number has grown since). Most people have at least one subscription they have not used in the past month and at least one where a cheaper tier would be sufficient. Cancel unused subscriptions immediately. Downgrade streaming from premium to standard where the difference is unnoticeable.

- Grocery bills — the biggest controllable expense: Meal planning for the week before shopping, writing a specific list, and shopping to the list consistently reduces grocery bills by 20–30% for most households. Switching from branded to own-brand equivalents on everyday items (pasta, rice, tinned goods, cleaning products) cuts grocery bills by 15–20% on those items with no quality impact. Cooking in bulk and using a slow cooker reduces food costs and decision fatigue simultaneously.

- Energy and utilities: Switching to a cheaper energy tariff at renewal, reducing standby consumption, and adjusting heating patterns can reduce energy bills by £200–£400 per year (UK) or $200–$400 per year (US). In the UK, check eligibility for the Warm Home Discount (£150) and Cold Weather Payment schemes.

- Phone and broadband: The biggest savings available to most households are through switching contracts rather than reducing usage. Switching mobile to a SIM-only deal typically saves £15–£30 per month versus a handset contract. Comparing broadband providers at renewal rather than auto-renewing typically saves £10–£20 per month.

- Transport: Combining trips, using public transport for some journeys, carpooling, and buying rail or bus season tickets where they represent a saving over daily fares all reduce transport costs without reducing the journeys made. In the UK, a 16–25, 26–30, or family railcard reduces rail fares by a third for an annual fee of £30–£35.

Step 7 — Increase Your Income (Even Incrementally)

Budgeting more carefully at the same income level has limits. When essential expenses consume 64% to 70% of a low income, there is a ceiling on how much further optimisation can achieve. The other side of the equation — income — must also be actively worked on.The income-increase strategies that are most accessible for low-income households in 2026 do not require a new degree or a career change. They fall into three categories: maximising existing income, creating additional income streams, and accessing entitlements already owed.

Maximise existing income

The most immediate action is to check whether you are being paid correctly and whether you are capturing all available income from your current employer. Are you eligible for overtime? Have you asked for a pay review in the last 12 months? Are you enrolled in your employer's pension scheme and receiving the employer match (which is effectively a pay increase of 3% to 5% on matched contributions)? Many low-income workers are eligible for the employer pension match and are not enrolled — missing out on money that is legally theirs.Side income on your schedule

The Albert.com low-income budget guide notes: 'Make a low-income budget work by looking for ways to increase income wherever you can.' In 2026, the most accessible side income options for people with existing jobs include selling unused items (once-off but immediate), doing occasional tasks on platforms like TaskRabbit or local community groups, renting storage space, pet-sitting or dog walking, and tutoring in any subject you have competence in. The goal is not a second full-time job — it is an additional £50 to £200 per month that can be specifically directed to a sinking fund or savings goal.The 52-week savings challenge

For those starting from zero savings and needing a structured motivation tool, the 52-week challenge (saving £1/$1 in week one, £2/$2 in week two, escalating to £52/$52 in week 52) builds to £1,378/$1,378 saved by year-end. Makeheadway's March 2025 guide identifies it as an effective momentum-builder for households with no current savings habit.Step 8 — Use Free Resources and Benefits You May Not Know About

One of the most common and most costly money management mistakes for low-income households is not claiming benefits, entitlements, and free resources that are specifically designed for people in their situation. Billions of pounds and dollars in unclaimed benefits go unused every year because eligible households are unaware of them, assume they will not qualify, or find the application process too complex.Staying Motivated: Progress Over Perfection

The most common reason low-income budgeting plans fail is not lack of strategy — it is loss of motivation after the first imperfect month. A budget that had three overspends in month one and was abandoned is infinitely worse than a budget that had three overspends and was revised and continued.InCharge's financial literacy guide frames the long-term relationship with budgeting correctly: 'It can change. It should change, in fact, along with changes to your financial situation. That's why it's important to continuously monitor your budget and adjust it as needed as your income grows or shrinks.' A budget is not a pass-fail test. It is a living document that reflects reality and evolves with it.

Practical motivation strategies include tracking visual progress on a specific goal — a printed chart showing the sinking fund balance growing toward a holiday or a new item you want — and celebrating the small wins that compound into large ones. Paying off a small debt, funding the first month of an emergency fund, completing the first subscription audit and seeing a lower bank total — these are real financial wins that deserve recognition. The emotional experience of financial progress, even on a small scale, is one of the strongest predictors of continued behaviour change.

Finally, the framing matters. Managing money on a low income is not a permanent punishment for being poor. It is a set of tools and habits that create more of what you want from your life — more security, less anxiety, the ability to plan ahead, and the satisfaction of getting things you want through your own deliberate effort rather than through debt that extracts a premium from your future self.

CONCLUSION

Managing money on a low income is harder than managing money on a high income. That is simply true, and any guide that pretends otherwise is doing its readers a disservice. But it is not impossible, and the core mechanics that make it work are available to anyone at any income level. Know your real numbers. Cover the Four Walls first. Adapt the budget framework to fit your actual income rather than a theoretical ideal. Use sinking funds to get what you want without debt. Automate savings before spending starts. Cut the spending that is not serving you. Increase income wherever you can, even by small amounts. And claim every benefit and resource you are entitled to.The 60% of Americans who say finances are a major source of stress are not all in that position because they earn too little. Many of them are in that position because money management on any income is a skill that is rarely taught and is difficult to learn alone. This guide is the starting point. The tools — a bank account, a spreadsheet or app, a named savings pot, a list of your actual spending — cost nothing. The decision to use them intentionally is what changes the outcome. And the outcome is not just a better bank balance. It is a life where you feel in control, where planned things happen because you planned them, and where you get what genuinely matters to you.

Frequently Asked Questions

Is it really possible to save money on a low income?

Yes — though the practical reality is that it requires more intentionality than saving on a higher income, because there is less margin for error. SmartMoneyTrek's March 2026 guide confirms: 'Even with limited income, the right budgeting strategy can help you cover essential expenses, reduce unnecessary spending, and gradually build savings. Even small financial improvements can make a meaningful difference over time.' The key principle is to start with whatever small amount is possible rather than waiting until circumstances improve. $25 per month automated into savings is $300 per year — enough to create a meaningful emergency buffer within 3 to 4 months. The habit and the buffer are both more important than the amount. Solutions Bank's April 2026 guide recommends starting with 5% to 10% if 20% is not achievable, with a focus on automation rather than willpower.What is the Four Walls budget method and how does it help on low income?

The Four Walls method, popularised by Dave Ramsey, establishes a hierarchy of spending priorities for tight budgets. The four walls are: food (groceries and essential household food), shelter (rent or mortgage and essential utilities), transport (getting to work and meeting essential commitments), and basic clothing. These four categories are paid first in every month, before any other expense — including debt payments. The rationale is that losing any of the four walls creates problems far more expensive than any missed payment. On a low income, the Four Walls method provides clarity about what must be protected every month, making it easier to make difficult decisions about other spending when money is tight. Everything outside the Four Walls is addressed in priority order after these are covered.What is a sinking fund and how do I use one on a tight budget?

A sinking fund is a named savings pot dedicated to a specific planned expense. Instead of being surprised by large irregular costs — annual insurance, Christmas, a holiday, a car repair, a new phone — you calculate the cost, divide it by the number of months available, and set that amount aside each month into a clearly labelled pot. On a tight budget, sinking funds allow you to plan for and achieve desired purchases without using credit or debt. Even £10 to $10 per month directed to a specific sinking fund produces a meaningful result over time: £120/$120 per year toward a goal that matters to you. The psychological effect is equally important — knowing the money is accumulating eliminates anxiety about the approaching bill and removes the guilt from the eventual purchase, because you saved for it deliberately.How do I budget when my income is irregular?

Both UFCU's January 2026 guide and South State Bank's January 2026 guide recommend the same approach for irregular income: build your budget around your lowest recent monthly income rather than an average or your best month. This creates a floor that is reliably achievable in even slow months, with any income above the floor available to boost savings or sinking funds. AZTech Training's budgeting guide advises listing all income sources including gig work, freelance, and side income as separate line items, recognising that 'irregular income budgeting means accounting for all cash flow, no matter how small or infrequent.' In months where income exceeds the budgeted floor, allocate the surplus in a defined order: top up emergency fund first, then sinking funds, then optionally accelerate a specific goal.What free tools and resources are available for low-income budgeting?

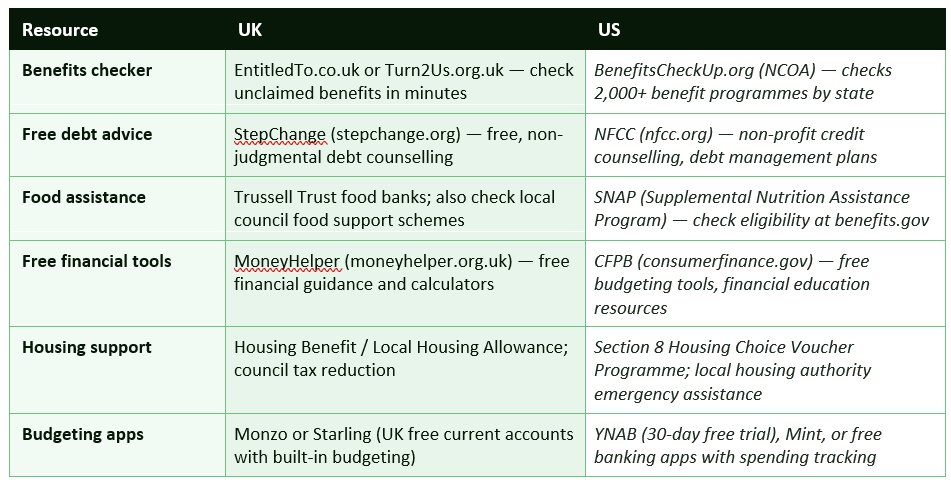

Several high-quality free tools are available for both UK and US budgeting. In the UK: MoneyHelper (moneyhelper.org.uk) provides free financial guidance, calculators, and debt advice; StepChange (stepchange.org) offers free professional debt counselling; and EntitledTo or Turn2Us allow you to check unclaimed benefits in minutes. In the US: the Consumer Financial Protection Bureau (consumerfinance.gov) provides free budgeting tools and financial education resources; the NFCC (nfcc.org) offers non-profit credit counselling; and BenefitsCheckUp.org checks eligibility for 2,000+ benefit programmes by state. For budgeting apps: Monzo and Starling (UK) are free current accounts with built-in spending categorisation and budgeting features; YNAB offers a 30-day free trial and is widely rated as the best app for budget management on tight incomes. Many local credit unions also offer free financial consultations.References

SmartMoneyTrek — How to Budget on a Low Income: 10 Practical Strategies That Actually Work (March 2026) https://smartmoneytrek.com/how-to-budget-on-a-low-incomeUFCU — Be Brave and Budget: 8 Low-Income Budgeting Tips to Take Control of Your Finance (January 2026) https://www.ufcu.org/resources/articles/detail/articles/2025/11/14/low-income-budgeting-tips

Wealthvieu — 50/30/20 Budget Rule 2026: How to Split Your Paycheck (May 2026) https://wealthvieu.com/personal-finance/budgeting-guide/50-30-20-rule/

Solutions Bank — 50/30/20 Budget Rule: Simple Math for Smarter Money (April 2026) https://www.solutions.bank/blog/post/50-30-20-budget-rule-simple-math-for-smarter-money

South State Bank — A Realistic Guide for Budgeting on a Limited Income (January 2026) https://www.southstatebank.com/personal/stories-and-insights/a-realistic-guide-for-budgeting-on-a-limited-income

AZTech Training — How to Budget with Low Income: Practical Tips and Strategies https://aztechtraining.com/articles/how-to-budget-with-low-income

InCharge — How to Budget Money on a Low Income https://www.incharge.org/financial-literacy/budgeting-saving/how-to-budget-money-on-low-income/

Albert.com — How to Budget Money on a Low Income https://albert.com/blog/how-to-budget-money-on-low-income

0 Comments Comments