Business

How to Raise from VC, Family Office & Angel in 2026

They all write cheques. But an angel investor, a family office, and a venture capital firm are three fundamentally different animals — with different incentive structures, different decision-making timelines, different things they need from you, and entirely different approaches to the relationship after they invest. Treating them the same way in your fundraising process is one of the most common and most costly mistakes founders make. I spent years working in a VC company, but now as entrepreneur, here's my take. This guide gives you the distinct playbook for each.

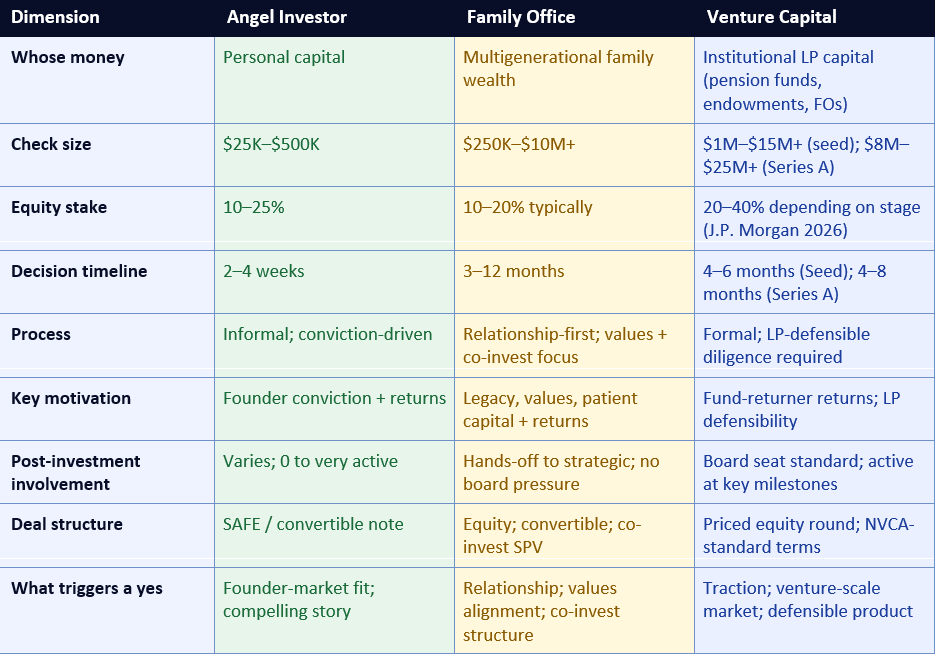

The fundamental difference between an angel investor, a family office, and a venture capital firm is not check size or sector preference — it is whose money they are deploying and what obligations that creates. This single structural distinction explains nearly everything about how each type behaves, decides, and operates as a post-investment partner.

An angel investor is a wealthy individual writing a cheque from their own bank account. They answer to no one. Zyner.io's March 2026 analysis articulates the implication precisely: 'Angels invest on conviction, and conviction is personal. They can move on gut feel, back a pre-revenue founder with a compelling story, and write a check by the end of the week.' Because it is their own money, an angel's decision to invest is genuinely an expression of their personal view — of the founder, the market, and whether they believe this specific company will succeed. The process is fast, the relationship is personal, and the post-investment involvement ranges from zero to heavily engaged depending on the individual.

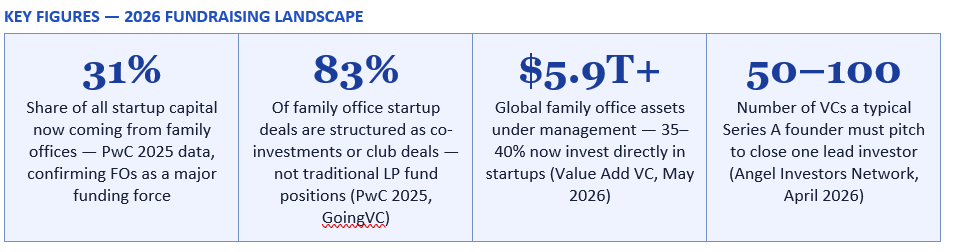

A family office manages the wealth of one family (single-family office, or SFO) or multiple families (multi-family office, or MFO) across generations. Family offices manage $5.9 trillion or more in global assets, and according to Value Add VC's May 2026 analysis, 35 to 40% now invest directly in startups. They are playing with genuinely long time horizons — multigenerational wealth management that is not subject to a fund's ten-year lifecycle or LP redemption pressure. This makes their capital uniquely patient but their decision-making uniquely cautious.

A venture capital firm raises a fund from outside investors called limited partners — pension funds, university endowments, family offices, and high-net-worth individuals. The VC's general partners then deploy that capital into startups over a three to five-year investment period and attempt to return the fund (and ideally many multiples of it) to LPs over a ten-year lifecycle. Because VCs are fiduciaries — legally obligated to act in their LPs' interests — every investment decision must be justifiable to a partnership that includes conservative institutional investors. As Zyner.io explains: 'When a VC passes, it's often not about you. It's about what they can defend to their LPs.'

Family offices manage $5.9T+ globally and 35–40% now invest directly in startups. They move slower than VCs, care about relationships over return optics, and can be the most patient — and valuable — capital on your cap table.

— VALUE ADD VC — FAMILY OFFICE INVESTING IN STARTUPS: HOW THEY THINK AND WHAT THEY WANT (MAY 2026)

These are not variations of the same question. They require fundamentally different answers, different supporting evidence, and different emotional registers in the pitch. A deck built to demonstrate venture-scale market opportunity (necessary for a VC) will feel impersonal and mercenary to a family office evaluating values alignment. A personal story about conviction and founder-market fit (compelling for an angel) will feel insufficiently rigorous to a VC who needs to defend the investment to institutional LPs. The following sections give the distinct playbook for each type.

Beyond capital, the best angels bring operator experience — they have built or scaled companies themselves and can offer pragmatic guidance on the specific challenges you face. A well-chosen angel in your sector can provide introductions to customers, early hires, and follow-on investors that are worth many times the capital they invested. Visible.vc's December 2025 guide notes that 'angels typically invest early and offer flexible terms' — the terms on angel rounds, typically structured as SAFE notes or convertible notes with minimal investor protections, are materially simpler and more founder-friendly than institutional investment agreements.

Angel syndicates and special purpose vehicles (SPVs) are an important mechanism that Zyner.io's March 2026 analysis highlights: 'Angel syndicates and SPVs let individual angels pool their checks and invest as a single entity. This means you get the capital of many angels but only add one line to your cap table.' If you are raising from a network of smaller angels, exploring whether they would co-invest through a syndicate reduces cap table complexity and administrative overhead significantly.

The key structural fact is patient capital. Family offices are not subject to a fund's ten-year lifecycle, LP redemption rights, or quarterly reporting pressure. According to Simple's April 2026 family office investment guide, family offices 'are structured for generational longevity, free from public quarterly reporting. With patient capital, family offices often lead in accessing unique investment opportunities.' This means a family office can hold a position for fifteen years without pressure to exit — genuinely different from any institutional fund. Ocorian's 2025 survey, cited by Qubit Capital's January 2026 analysis, found 66% of family offices expect to increase their risk appetite over the next year, and 76% are doing more sophisticated deals than before.

Family offices are also deeply relationship-gated. Value Add VC's analysis notes that 'warm intros from trusted co-investors convert at 10–15x the rate of cold outreach. Family office deal flow is almost entirely relationship-gated.' The best route to a family office is through a trusted intermediary — a co-investor already in the round, a mutual advisor, or a relationship built over months of genuine interaction before you need capital.

The fiduciary obligation to LPs means every investment must be defensible in a formal partnership meeting. A VC partner who wants to invest in your company must convince the rest of the partnership. This is why VCs pass on companies that subjectively seem promising: the partner might believe in you personally, but if they cannot construct a convincing case for why this company could return the fund, the partnership will not approve the investment. VCs require a large addressable market, a defensible product, a strong founding team, and evidence of traction — not just a good story, but proof that the story is starting to come true.

The VC process typically moves through four stages: initial outreach and first meeting (where the VC is assessing fit and initial conviction), partner meetings (where the founding team meets the broader partnership), deep due diligence (financial model review, customer reference calls, technical review, competitive analysis), and term sheet and close. For a Seed round, this process may take two to four months; for a Series A, four to six months or longer. Seedblink's practical guide confirms: 'Raising from VCs can take more time than raising from angel investors. There are more meetings, more due diligence, and more legal steps.'

Delaware C-Corporation incorporation is a practical prerequisite. StartupOwl's February 2026 guide notes that 'you must be a Delaware C-Corporation. VCs cannot invest in most LLCs because their fund structure includes tax-exempt and foreign limited partners who cannot hold pass-through interests.' If you are not yet a Delaware C-Corp and are approaching institutional VCs, incorporation is the first action to take.

Sources: Zyner.io March 2026, Value Add VC May 2026, Angel Investors Network April 2026, J.P. Morgan 2026 analysis via angelinvestorsnetwork.com, StartupOwl February 2026, Seedblink.

Angel investors are the natural starting point for pre-revenue or very early revenue companies. They tolerate the highest uncertainty and the lightest due diligence, and they invest based on conviction about the founder rather than requiring proof of product-market fit. The typical angel check of $25,000 to $250,000 funds the company through its first meaningful milestones — initial product development, first customers, early revenue. Visible.vc's December 2025 guide advises: 'Angel investors are better to pitch to when your company is extremely early stage. When starting the company look to close friends, family, and professionals that can make a small investment.'

Family offices become the right target once you have traction but are not yet ready for a formal institutional VC round — typically after demonstrating initial product-market fit but before the metrics required for a Series A are fully established. They are also ideal as participants in a round where a VC is leading: the 83% co-invest statistic from PwC's 2025 data means family offices are structurally predisposed to fill rounds alongside a credible institutional lead rather than to lead rounds themselves. If you have a lead VC committed, a family office co-invest tranche can fill the round quickly.

Venture capital is best approached when you have the traction and metrics required to make a VC-defensible case: typically $500K to $1M ARR for SaaS Series A, meaningful growth rates that demonstrate product-market fit, and a clear go-to-market motion that can be scaled with capital. The angel rounds build the traction; the family office round can bridge or fill the institutional round; the VC round funds the scale.

For angels, lead with personal narrative. Why you? Why now? What personal insight or experience makes you the person to build this? Founders who tell a compelling, specific, credible story about their founder-market fit create the personal conviction that drives angel decisions. The market can be large, the product compelling, but the angel is fundamentally betting on the person. Close with a clear, simple ask: 'We are raising $500K on a SAFE at a $3M cap. We have $150K committed from two angels and we are looking for three to four more.'

For family offices, lead with shared values and then build to the opportunity. Do not open with your growth metrics — open with the mission and the legacy the family office will be participating in. Then demonstrate that you have done your research on their values and investment history, and explain specifically why this company is aligned with what they care about. Only then transition to the commercial opportunity. Value Add VC is explicit: 'Emotional motivations' and 'desire for involvement' are core decision factors. Present the co-invest structure clearly, with a liquidity narrative that respects their need for a thoughtful exit plan.

For VCs, open with a crisp insight that explains why the market is about to change and why your company is positioned to capture the resulting opportunity. VCs hear hundreds of pitches; the ones that are remembered articulate a counterintuitive insight — a belief about the world that most people do not yet hold but that will be obviously true in five years. Everything else in the pitch — traction, team, product — is evidence for that insight. Close with your ask and a clear articulation of what the capital will accomplish: specific milestones, timeline, and the metrics you expect to achieve.

Angel due diligence is typically light and focused on the founder. Expect a background conversation about your career, some reference calls with people you have worked with, and perhaps a review of your financials and key metrics. Angels rarely hire third-party diligence firms or conduct formal legal review before the seed stage. The most important preparation is ensuring the founders who know you best can give compelling, specific endorsements — not generic praise, but specific stories about how you performed under pressure or solved a difficult problem.

Family office due diligence is more thorough and includes an element that few founders anticipate: personal background checks. Flowlie's April 2025 guide notes that family offices conduct 'thorough diligence including founder background checks' because they are deploying personal generational wealth and the trust element is paramount. They will also review your cap table carefully — any messiness (former co-founders without clean separation agreements, unclear IP ownership, angel investors with unusual rights) will slow or stop the process. Ensure your legal house is in order before approaching family offices.

VC due diligence is the most comprehensive. Expect customer reference calls (VCs typically call three to five customers directly without the founder present), a technical review if you are a deep tech company, competitive analysis, legal review of incorporation documents and IP assignments, and cap table validation. Prepare a clean, complete data room in advance: cap table model, financial model with assumptions visible, key customer contracts, employment agreements with key team members, and IP assignment documentation. A well-prepared data room dramatically accelerates the VC diligence process and signals organisational maturity.

The key principle is to track each investor's process separately and be honest about where each stands. VCs require competitive tension from other VCs to move quickly — you can mention family office interest, but VCs calibrate primarily against other institutional investors. Family offices are influenced by the credibility of the lead VC — 'we have [credible VC firm] committed as lead' is a powerful signal that substantially accelerates family office interest. Angels are influenced by the quality of other angels already in the round.

Use a simple CRM or spreadsheet to track each investor's stage: initial conversation, follow-up materials sent, second meeting, due diligence, term sheet. Update it weekly. The volume of a serious fundraise — managing 20 to 40 active investor conversations simultaneously — makes tracking essential. An investor who does not hear from you for three weeks during a live fundraise will assume the process has concluded or that their interest has been superseded.

Angels typically want very little formal engagement — a brief monthly or quarterly email update is sufficient for most. The best angels are available when you need them (for introductions, for a phone call when you face a difficult decision) but do not require ongoing reporting. Treat them as a network asset: reach out when they can specifically help, and keep them informed of major milestones. An angel who feels kept in the loop and occasionally useful becomes a strong advocate in their own network.

Family offices vary considerably. Value Add VC describes their post-investment stance: 'They don't want to run the company or manage the founder. Information rights, observer seat if any, and quarterly updates. That's the deal.' The SFO case can be different — a family whose wealth came from your sector may seek active mentorship and strategic involvement. Flowlie's April 2025 guide notes: 'SFOs where the family built businesses in your sector often provide active mentorship, strategic guidance, industry introductions, and customer connections.' Clarify the expected post-investment relationship before closing.

VCs are the most formally involved. Board seats are standard at Series A and above. VCs typically expect monthly or quarterly management reports, proactive communication about major decisions and strategic pivots, and engagement with their portfolio network. The most valuable post-VC relationships are those where the founder proactively uses the investor's network — asking for specific introductions, requesting strategic feedback on specific decisions, and giving the investor enough context to be genuinely helpful rather than just monitoring.

The most successful founders in 2026 treat these three investor types as complementary parts of a capital strategy rather than competing alternatives. They use angel capital to build early traction, family office capital to fill rounds and provide patient long-term anchors, and VC capital to fund the scaling phase. They approach each type with the right materials, the right narrative emphasis, and the right expectations about timeline and process. They build relationships with family offices months before they need the capital. They get the angels in the round who open the doors to Series A VCs. And they never mistake the fact that all three write cheques for the idea that all three write them the same way.

Angel Investors Network — Angel Investor vs Venture Capitalist: 2026 Guide (April 2026) https://angelinvestorsnetwork.com/venture-capital/angel-investor-vs-venture-capitalist-2026-guide

Value Add VC — Family Office Investing in Startups: How They Think and What They Want (May 2026) https://valueaddvc.com/blog/family-offices-investing-in-startups-how-they-think-and-what-they-want

GoingVC — Winning Family Offices in 2025: The VC Fundraising Playbook (August 2025) https://www.goingvc.com/post/winning-family-offices-in-2025-the-vc-fundraising-playbook

Qubit Capital — How to Win Family Office Funding: Key Strategies for Startups (January 2026) https://qubit.capital/blog/family-office-investments-startup-funding-guide

Qubit Capital — Family Office Startup Funding: Case Studies and Investment Strategies https://qubit.capital/blog/family-office-case-studies

Flowlie — Navigating the World of Family Office Structures for Startup Funding (April 2025) https://www.flowlie.com/blog/navigating-the-world-of-family-office-structures-for-startup-funding/

StartupOwl — Venture Capital Funding: How VC Works, Who Qualifies and How to Get a Meeting (February 2026) https://startupowl.com/fund/venture-capital-funding

Seedblink — Raising from VCs: A Practical Guide for Startup Founders https://seedblink.com/blog/raising-from-vcs-a-practical-guide-for-startup-founders

TABLE OF CONTENTS

- The Three Investor Types: A Structural Overview

- Why the Same Pitch Does Not Work for All Three

- Part 1: How to Raise from an Angel Investor

- Part 2: How to Raise from a Family Office

- Part 3: How to Raise from a Venture Capital Firm

- The Master Comparison: All Three Side-by-Side

- The Right Sequencing: Who to Approach and When

- Building Your Investor List: Targeting the Right People

- What Goes Into Your Fundraising Materials

- The Pitch: What Each Investor Type Wants to Hear

- Due Diligence: What to Expect from Each Investor

- Managing Multiple Investor Types Simultaneously

- Post-Investment: What Each Relationship Looks Like

- Common Mistakes Founders Make with Each Investor Type

- Conclusion

- Frequently Asked Questions

- References

The Three Investor Types: A Structural Overview

The fundamental difference between an angel investor, a family office, and a venture capital firm is not check size or sector preference — it is whose money they are deploying and what obligations that creates. This single structural distinction explains nearly everything about how each type behaves, decides, and operates as a post-investment partner.An angel investor is a wealthy individual writing a cheque from their own bank account. They answer to no one. Zyner.io's March 2026 analysis articulates the implication precisely: 'Angels invest on conviction, and conviction is personal. They can move on gut feel, back a pre-revenue founder with a compelling story, and write a check by the end of the week.' Because it is their own money, an angel's decision to invest is genuinely an expression of their personal view — of the founder, the market, and whether they believe this specific company will succeed. The process is fast, the relationship is personal, and the post-investment involvement ranges from zero to heavily engaged depending on the individual.

A family office manages the wealth of one family (single-family office, or SFO) or multiple families (multi-family office, or MFO) across generations. Family offices manage $5.9 trillion or more in global assets, and according to Value Add VC's May 2026 analysis, 35 to 40% now invest directly in startups. They are playing with genuinely long time horizons — multigenerational wealth management that is not subject to a fund's ten-year lifecycle or LP redemption pressure. This makes their capital uniquely patient but their decision-making uniquely cautious.

A venture capital firm raises a fund from outside investors called limited partners — pension funds, university endowments, family offices, and high-net-worth individuals. The VC's general partners then deploy that capital into startups over a three to five-year investment period and attempt to return the fund (and ideally many multiples of it) to LPs over a ten-year lifecycle. Because VCs are fiduciaries — legally obligated to act in their LPs' interests — every investment decision must be justifiable to a partnership that includes conservative institutional investors. As Zyner.io explains: 'When a VC passes, it's often not about you. It's about what they can defend to their LPs.'

Family offices manage $5.9T+ globally and 35–40% now invest directly in startups. They move slower than VCs, care about relationships over return optics, and can be the most patient — and valuable — capital on your cap table.

— VALUE ADD VC — FAMILY OFFICE INVESTING IN STARTUPS: HOW THEY THINK AND WHAT THEY WANT (MAY 2026)

Why the Same Pitch Does Not Work for All Three

Most first-time founders make the mistake of preparing one pitch deck, one financial model, and one narrative — and using them with every type of investor. This approach fails for a simple reason: each investor type is evaluating a different question. The angel asks: 'Do I believe in this founder and this idea?' The family office asks: 'Does this fit our values, legacy, and capital allocation strategy, and can we co-invest alongside a trusted lead?' The VC asks: 'Is this the kind of company that can return our entire fund?'These are not variations of the same question. They require fundamentally different answers, different supporting evidence, and different emotional registers in the pitch. A deck built to demonstrate venture-scale market opportunity (necessary for a VC) will feel impersonal and mercenary to a family office evaluating values alignment. A personal story about conviction and founder-market fit (compelling for an angel) will feel insufficiently rigorous to a VC who needs to defend the investment to institutional LPs. The following sections give the distinct playbook for each type.

Part 1: How to Raise from an Angel Investor

What angels are and what they bring

Angel investors are individuals who invest personal capital — typically $25,000 to $500,000 per deal according to StartupOwl's February 2026 guide — at the earliest stages of a company's life. The defining feature is that they are writing from personal conviction rather than institutional obligation. This creates the fastest possible decision process (two to four weeks from first conversation to wire, according to the Angel Investors Network's April 2026 analysis) but also the most varied investment criteria, since every angel has different expertise, networks, and conviction triggers.Beyond capital, the best angels bring operator experience — they have built or scaled companies themselves and can offer pragmatic guidance on the specific challenges you face. A well-chosen angel in your sector can provide introductions to customers, early hires, and follow-on investors that are worth many times the capital they invested. Visible.vc's December 2025 guide notes that 'angels typically invest early and offer flexible terms' — the terms on angel rounds, typically structured as SAFE notes or convertible notes with minimal investor protections, are materially simpler and more founder-friendly than institutional investment agreements.

The angel fundraising process

Angel fundraising is relationship-first and network-driven. Cold outreach to angels has a very low conversion rate; warm introductions from mutual connections convert at dramatically higher rates. The typical angel process is: initial meeting or call (60 to 90 minutes, covering founder, product, market, and why now), followed by one or two follow-up conversations, reference checks on the founder, and a decision. The due diligence is typically light — angels are making a conviction bet on the founder more than a rigorous assessment of financial projections.Angel syndicates and special purpose vehicles (SPVs) are an important mechanism that Zyner.io's March 2026 analysis highlights: 'Angel syndicates and SPVs let individual angels pool their checks and invest as a single entity. This means you get the capital of many angels but only add one line to your cap table.' If you are raising from a network of smaller angels, exploring whether they would co-invest through a syndicate reduces cap table complexity and administrative overhead significantly.

The angel investor fundraising playbook — what works in 2026

- Lead with founder story and conviction: Angels back people before products. Explain why you specifically are the right person to build this company. What in your background gives you an unfair advantage? What personal insight led to this idea? Angels who cannot remember your story after the meeting will not invest.

- Target angels with relevant domain experience: An angel who has built a company in your sector understands your challenges, has relevant contacts, and can evaluate your claims credibly. A domain-expert angel who writes a smaller cheque is often more valuable than a generalist angel who writes a larger one.

- Keep the round simple: SAFEs (Simple Agreements for Future Equity) are the standard instrument for angel rounds. They are fast, cheap, and require no valuation negotiation at the angel stage. Y Combinator's SAFE documents are the industry standard — any experienced angel will recognise them and can sign quickly.

- Create a light but real social proof loop: Close your first angel quickly, even if it is a smaller cheque, and use their endorsement in subsequent conversations. Angels are influenced by the quality of other angels who have already committed — a credible early investor signals that someone with relevant knowledge has already done due diligence.

- Respect the timeline but create soft urgency: Unlike VCs, angels do not have deployment pressure. But a round with a clear closing date — 'we are closing in six weeks' — creates enough urgency to prevent indefinite deferral. Follow up consistently without being pushy.

Part 2: How to Raise from a Family Office

What family offices are and what makes them different

Family offices are the most misunderstood investor category in startup fundraising. PwC's 2025 data, cited by GoingVC's analysis, shows family offices account for approximately 31% of all capital invested into startups — making them a major force in the market. Yet most founders underinvest in understanding how they operate. According to Value Add VC's May 2026 analysis: 'Family offices manage $5.9T+ globally and 35–40% now invest directly in startups. They move slower than VCs, care about relationships over returns optics, and can be the most patient — and valuable — capital on your cap table.'The key structural fact is patient capital. Family offices are not subject to a fund's ten-year lifecycle, LP redemption rights, or quarterly reporting pressure. According to Simple's April 2026 family office investment guide, family offices 'are structured for generational longevity, free from public quarterly reporting. With patient capital, family offices often lead in accessing unique investment opportunities.' This means a family office can hold a position for fifteen years without pressure to exit — genuinely different from any institutional fund. Ocorian's 2025 survey, cited by Qubit Capital's January 2026 analysis, found 66% of family offices expect to increase their risk appetite over the next year, and 76% are doing more sophisticated deals than before.

How family offices actually invest in startups in 2026

PwC's 2025 data reveals a critical structural point: 83% of family office startup deals are now structured as co-investments or club deals rather than traditional LP fund positions. Value Add VC explains the preference: 'Co-investments give families something traditional LP positions don't: more ownership, more transparency, and more control.' This means your family office pitch should not be structured as a pitch to a passive fund investor — it should be structured as an invitation to co-invest directly alongside a lead VC, with visibility into the specific company, its metrics, and its management team.Family offices are also deeply relationship-gated. Value Add VC's analysis notes that 'warm intros from trusted co-investors convert at 10–15x the rate of cold outreach. Family office deal flow is almost entirely relationship-gated.' The best route to a family office is through a trusted intermediary — a co-investor already in the round, a mutual advisor, or a relationship built over months of genuine interaction before you need capital.

The family office fundraising process

The single most important thing to understand about family office timing is that it is not VC timing. Value Add VC states directly: 'The single biggest mistake founders make with family offices is expecting VC timing. They don't have the same deployment pressure. A Goldman Sachs survey found that 46% of family offices planned to increase VC and PE allocations in 2024 — but increase means over 12–24 months, not the next 90 days.' Flowlie's April 2025 guide confirms: 'Family offices generally move slower than they initially suggest due to the personal nature of their capital and thorough diligence including founder background checks. Build extra buffer time into your fundraising timeline when pursuing family office capital.'The family office fundraising playbook — what works in 2026

- Lead with values and legacy alignment, not just returns: Qubit Capital's January 2026 guide identifies 'emotional motivations' as central to family office decision-making: 'Many family offices invest in sectors that resonate with personal values, legacy, social impact, or innovation.' Research the family's background and their current portfolio before pitching. If they built their wealth in real estate, understand how your company connects to that legacy. If they are impact-focused, demonstrate your sustainability or social metrics.

- Structure your ask around co-investment, not fund LP commitments: Pitch a direct equity stake in your company alongside your lead VC, via an SPV if necessary. Present it as 'we have a lead VC committed and we are offering a co-invest tranche to select family offices who want direct exposure.' This matches how 83% of family office startup deals are actually structured.

- Have a genuine liquidity narrative: Unlike angels who write small conviction cheques, family offices managing generational wealth need to understand the exit path. Value Add VC is explicit: 'Liquidity talk is mandatory. FOs don't need cash tomorrow, but they demand a plan — secondaries, NAV credit, early DPI. Hope is not a strategy.' Prepare a clear, honest liquidity discussion: not a promise of a specific exit, but a thoughtful narrative about paths to liquidity.

- Keep your fundraising ask clean and appropriately sized: Value Add VC notes that 'family offices hate sloppy fundraising. If you're raising $10M but only need $6M to hit the next milestone, they want the $6M story.' Precision in your ask signals maturity and respect for their capital. Ticket sizes typically range from $250,000 to $10M+ depending on the family office's scale and your stage.

- Build the relationship before you need the money: Family offices invest in founders they know and trust over time. One of the most effective strategies is to establish a connection with a family office twelve to eighteen months before you need their capital — through shared events, introductions from mutual contacts, and genuine value exchange (sharing insight, making introductions) before asking for anything.

Part 3: How to Raise from a Venture Capital Firm

How VCs are structured and what drives their decisions

Understanding how a VC firm is structured is the starting point for understanding how to raise from one. A VC firm raises a fund from limited partners — institutions and wealthy individuals who commit capital for a ten-year period in exchange for a share of returns. The general partners of the firm deploy that capital into startups over the first three to five years, attempt to generate returns through exits (IPOs or acquisitions) in the following years, and return capital to LPs. This ten-year clock, combined with the power law return requirement (a single investment needs to be able to return the entire fund), shapes every VC decision.The fiduciary obligation to LPs means every investment must be defensible in a formal partnership meeting. A VC partner who wants to invest in your company must convince the rest of the partnership. This is why VCs pass on companies that subjectively seem promising: the partner might believe in you personally, but if they cannot construct a convincing case for why this company could return the fund, the partnership will not approve the investment. VCs require a large addressable market, a defensible product, a strong founding team, and evidence of traction — not just a good story, but proof that the story is starting to come true.

The VC fundraising process

The Angel Investors Network's April 2026 analysis is explicit about the reality of Series A fundraising: 'Raising Series A requires four to six months of full-time fundraising, detailed financial models projecting five-year growth, and tolerance for rejection — most founders pitch 50–100 VCs to close one lead investor.' This is not an exaggeration. VC fundraising is a volume process at the outset — you need to engage a large number of investors simultaneously to generate the competitive tension that produces a term sheet.The VC process typically moves through four stages: initial outreach and first meeting (where the VC is assessing fit and initial conviction), partner meetings (where the founding team meets the broader partnership), deep due diligence (financial model review, customer reference calls, technical review, competitive analysis), and term sheet and close. For a Seed round, this process may take two to four months; for a Series A, four to six months or longer. Seedblink's practical guide confirms: 'Raising from VCs can take more time than raising from angel investors. There are more meetings, more due diligence, and more legal steps.'

Delaware C-Corporation incorporation is a practical prerequisite. StartupOwl's February 2026 guide notes that 'you must be a Delaware C-Corporation. VCs cannot invest in most LLCs because their fund structure includes tax-exempt and foreign limited partners who cannot hold pass-through interests.' If you are not yet a Delaware C-Corp and are approaching institutional VCs, incorporation is the first action to take.

The VC fundraising playbook — what works in 2026

- Demonstrate venture-scale opportunity clearly: VCs are looking for companies that could return their entire fund. That typically requires a market large enough that capturing a small share of it creates a very large business. Your deck must answer the market size question with credible data, not optimistic bottom-up speculation. A genuine $50B+ total addressable market with a credible path to $10M+ ARR is the minimum threshold for most Series A VCs.

- Get warm introductions from founders in the VC's portfolio: Cold outreach to VCs has an extremely low meeting-to-call conversion rate. A warm introduction from a portfolio founder — someone the VC has already backed and trusts — is the highest-quality signal that your time is worth theirs. Build these relationships before you start the formal process.

- Run a parallel process with a tight timeline: Contact all target VCs within a two-week window and set a clear fundraising timeline. VC fundraising timelines that stretch indefinitely allow investors to defer without deciding. A stated close date creates the urgency that brings decisions forward and generates competitive tension.

- Prepare institutional-grade materials: VCs have reviewed thousands of pitch decks. Yours needs to be crisp, clearly structured, and tell a compelling story in the standard format: problem, solution, market, product, traction, team, ask. Your financial model needs to show five-year projections with clearly stated assumptions that can be scrutinised and stress-tested. Use frameworks like NVCA model documents for term sheet discussions.

- Understand the partner's thesis before the meeting: Every VC partner has an investment thesis — the types of companies they believe will produce venture returns in their specific fund size and timeline. Research the partner's recent investments, their published writing, and their stated thesis before your first meeting. A pitch that explicitly connects your company to their stated thesis is far more compelling than a generic market narrative.

The Master Comparison: All Three Side-by-Side

Sources: Zyner.io March 2026, Value Add VC May 2026, Angel Investors Network April 2026, J.P. Morgan 2026 analysis via angelinvestorsnetwork.com, StartupOwl February 2026, Seedblink.

The Right Sequencing: Who to Approach and When

The order in which you approach these three investor types matters significantly — both because each type is best suited to a different stage of company development, and because the relationships you build with earlier-stage investors become the warm introductions that open doors with later-stage ones.Angel investors are the natural starting point for pre-revenue or very early revenue companies. They tolerate the highest uncertainty and the lightest due diligence, and they invest based on conviction about the founder rather than requiring proof of product-market fit. The typical angel check of $25,000 to $250,000 funds the company through its first meaningful milestones — initial product development, first customers, early revenue. Visible.vc's December 2025 guide advises: 'Angel investors are better to pitch to when your company is extremely early stage. When starting the company look to close friends, family, and professionals that can make a small investment.'

Family offices become the right target once you have traction but are not yet ready for a formal institutional VC round — typically after demonstrating initial product-market fit but before the metrics required for a Series A are fully established. They are also ideal as participants in a round where a VC is leading: the 83% co-invest statistic from PwC's 2025 data means family offices are structurally predisposed to fill rounds alongside a credible institutional lead rather than to lead rounds themselves. If you have a lead VC committed, a family office co-invest tranche can fill the round quickly.

Venture capital is best approached when you have the traction and metrics required to make a VC-defensible case: typically $500K to $1M ARR for SaaS Series A, meaningful growth rates that demonstrate product-market fit, and a clear go-to-market motion that can be scaled with capital. The angel rounds build the traction; the family office round can bridge or fill the institutional round; the VC round funds the scale.

Building Your Investor List: Targeting the Right People

The quality of your investor list is more important than its length. A highly targeted list of 30 investors who are genuinely relevant to your stage, sector, and geography will outperform a spray-and-pray list of 200 names.For angels

Target angels who have built businesses in your sector, invested in similar companies (check AngelList, Crunchbase, and publicly available portfolios), and are geographically accessible for the early relationship-building that drives angel conviction. Operator angels — founders who have already built and exited a company in your space — are the highest-quality targets. Warm introductions from other portfolio founders or mutual advisors are the most effective sourcing mechanism.For family offices

Family offices are difficult to find because many operate without a public internet presence. The best sourcing approaches are: events designed for family office deal flow (family office associations, private wealth conferences), co-investor introductions from VCs who regularly work with family offices, placement agents or advisors who specialise in family office access, and relationship-building over time through thoughtful content and genuine mutual value exchange. VC Lab's April 2026 guide notes that for fund managers seeking family office LPs, 'smaller family offices that have a track record of backing emerging managers' are the most accessible entry points.For VCs

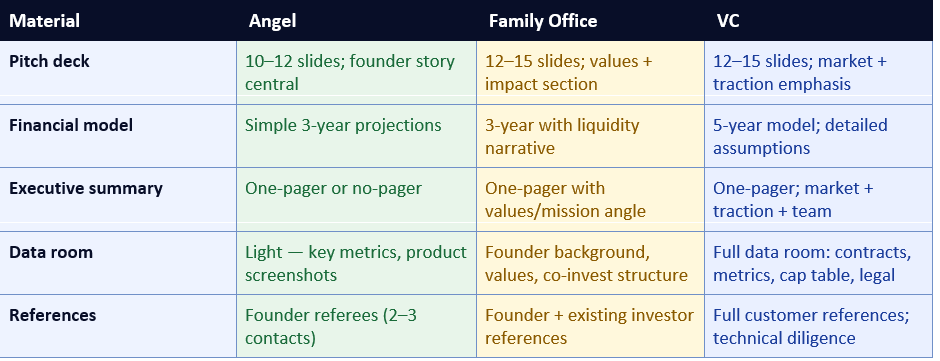

Research specific partners, not just firms. A VC firm is not a monolith — different partners have different theses, different portfolio focuses, and different conviction areas. Use AngelList Venture, Crunchbase, and individual VC websites to understand which partner at each firm is most aligned with your sector and stage. Read their recent published writing — blog posts, Twitter/X threads, podcast appearances — to understand their current investment thesis and the frameworks they use to evaluate companies.What Goes Into Your Fundraising Materials

Each investor type has different expectations for the depth and format of fundraising materials — and calibrating appropriately signals your understanding of how each type operates.The Pitch: What Each Investor Type Wants to Hear

A pitch is a story, and different audiences need different stories to be moved to action. The structural content of a pitch may be similar across investor types — problem, solution, market, traction, team, ask — but the emphasis, tone, and supporting detail should shift significantly.For angels, lead with personal narrative. Why you? Why now? What personal insight or experience makes you the person to build this? Founders who tell a compelling, specific, credible story about their founder-market fit create the personal conviction that drives angel decisions. The market can be large, the product compelling, but the angel is fundamentally betting on the person. Close with a clear, simple ask: 'We are raising $500K on a SAFE at a $3M cap. We have $150K committed from two angels and we are looking for three to four more.'

For family offices, lead with shared values and then build to the opportunity. Do not open with your growth metrics — open with the mission and the legacy the family office will be participating in. Then demonstrate that you have done your research on their values and investment history, and explain specifically why this company is aligned with what they care about. Only then transition to the commercial opportunity. Value Add VC is explicit: 'Emotional motivations' and 'desire for involvement' are core decision factors. Present the co-invest structure clearly, with a liquidity narrative that respects their need for a thoughtful exit plan.

For VCs, open with a crisp insight that explains why the market is about to change and why your company is positioned to capture the resulting opportunity. VCs hear hundreds of pitches; the ones that are remembered articulate a counterintuitive insight — a belief about the world that most people do not yet hold but that will be obviously true in five years. Everything else in the pitch — traction, team, product — is evidence for that insight. Close with your ask and a clear articulation of what the capital will accomplish: specific milestones, timeline, and the metrics you expect to achieve.

Due Diligence: What to Expect from Each Investor

Due diligence processes vary significantly in depth, duration, and focus across investor types. Calibrating your preparation accordingly reduces friction and signals professionalism.Angel due diligence is typically light and focused on the founder. Expect a background conversation about your career, some reference calls with people you have worked with, and perhaps a review of your financials and key metrics. Angels rarely hire third-party diligence firms or conduct formal legal review before the seed stage. The most important preparation is ensuring the founders who know you best can give compelling, specific endorsements — not generic praise, but specific stories about how you performed under pressure or solved a difficult problem.

Family office due diligence is more thorough and includes an element that few founders anticipate: personal background checks. Flowlie's April 2025 guide notes that family offices conduct 'thorough diligence including founder background checks' because they are deploying personal generational wealth and the trust element is paramount. They will also review your cap table carefully — any messiness (former co-founders without clean separation agreements, unclear IP ownership, angel investors with unusual rights) will slow or stop the process. Ensure your legal house is in order before approaching family offices.

VC due diligence is the most comprehensive. Expect customer reference calls (VCs typically call three to five customers directly without the founder present), a technical review if you are a deep tech company, competitive analysis, legal review of incorporation documents and IP assignments, and cap table validation. Prepare a clean, complete data room in advance: cap table model, financial model with assumptions visible, key customer contracts, employment agreements with key team members, and IP assignment documentation. A well-prepared data room dramatically accelerates the VC diligence process and signals organisational maturity.

Managing Multiple Investor Types Simultaneously

Most successful fundraises involve all three investor types in the same round or in close sequence — angels building early momentum, a family office filling the round alongside a VC lead, or a VC leading with family offices participating in the co-invest tranche. Managing all three simultaneously requires process discipline.The key principle is to track each investor's process separately and be honest about where each stands. VCs require competitive tension from other VCs to move quickly — you can mention family office interest, but VCs calibrate primarily against other institutional investors. Family offices are influenced by the credibility of the lead VC — 'we have [credible VC firm] committed as lead' is a powerful signal that substantially accelerates family office interest. Angels are influenced by the quality of other angels already in the round.

Use a simple CRM or spreadsheet to track each investor's stage: initial conversation, follow-up materials sent, second meeting, due diligence, term sheet. Update it weekly. The volume of a serious fundraise — managing 20 to 40 active investor conversations simultaneously — makes tracking essential. An investor who does not hear from you for three weeks during a live fundraise will assume the process has concluded or that their interest has been superseded.

Post-Investment: What Each Relationship Looks Like

The relationship after investment varies considerably by investor type, and understanding the post-close expectations of each type helps founders manage them effectively.Angels typically want very little formal engagement — a brief monthly or quarterly email update is sufficient for most. The best angels are available when you need them (for introductions, for a phone call when you face a difficult decision) but do not require ongoing reporting. Treat them as a network asset: reach out when they can specifically help, and keep them informed of major milestones. An angel who feels kept in the loop and occasionally useful becomes a strong advocate in their own network.

Family offices vary considerably. Value Add VC describes their post-investment stance: 'They don't want to run the company or manage the founder. Information rights, observer seat if any, and quarterly updates. That's the deal.' The SFO case can be different — a family whose wealth came from your sector may seek active mentorship and strategic involvement. Flowlie's April 2025 guide notes: 'SFOs where the family built businesses in your sector often provide active mentorship, strategic guidance, industry introductions, and customer connections.' Clarify the expected post-investment relationship before closing.

VCs are the most formally involved. Board seats are standard at Series A and above. VCs typically expect monthly or quarterly management reports, proactive communication about major decisions and strategic pivots, and engagement with their portfolio network. The most valuable post-VC relationships are those where the founder proactively uses the investor's network — asking for specific introductions, requesting strategic feedback on specific decisions, and giving the investor enough context to be genuinely helpful rather than just monitoring.

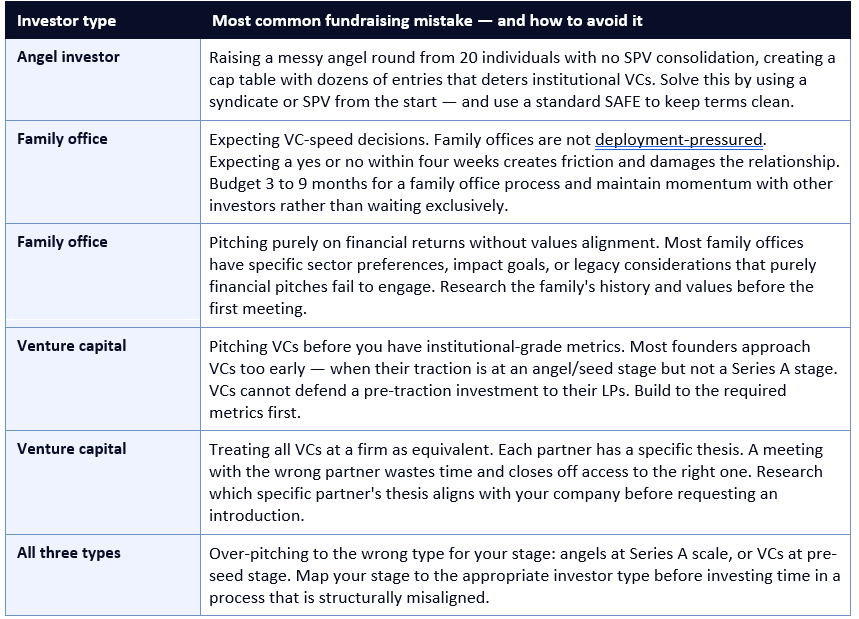

Common Mistakes Founders Make with Each Investor Type

CONCLUSION

An angel investor, a family office, and a venture capital firm are not interchangeable sources of capital — they are structurally different institutions with different incentives, different decision processes, and different post-investment relationships. Treating them the same way in your fundraising process is a mistake that costs time, relationships, and, most importantly, terms. Angels back founders on conviction and move in weeks. Family offices deploy patient generational capital in months — and they are behind 31% of all startup capital, predominantly through co-investments. VCs make LP-defensible bets on venture-scale opportunity and take four to six months to close.The most successful founders in 2026 treat these three investor types as complementary parts of a capital strategy rather than competing alternatives. They use angel capital to build early traction, family office capital to fill rounds and provide patient long-term anchors, and VC capital to fund the scaling phase. They approach each type with the right materials, the right narrative emphasis, and the right expectations about timeline and process. They build relationships with family offices months before they need the capital. They get the angels in the round who open the doors to Series A VCs. And they never mistake the fact that all three write cheques for the idea that all three write them the same way.

Frequently Asked Questions

What is the main difference between raising from an angel investor and a VC?

The fundamental structural difference is whose money each deploys. An angel invests their own personal capital with no obligations to outside investors — they can decide in two to four weeks based on personal conviction and back a pre-revenue founder on gut feel. A VC deploys capital raised from institutional LPs (pension funds, endowments, family offices) and is a fiduciary with legal obligations to those investors. Every VC investment must be defensible in a partnership meeting to colleagues who will scrutinise the deal against their fund's return requirements. This is why VCs run four to six-month due diligence processes and pass on companies they personally like if the venture-scale return case is not clear. Angels invest on conviction; VCs invest on defensible conviction. Both are legitimate criteria — they just require very different companies, very different materials, and very different pitches.How is raising from a family office different from raising from a VC?

The key differences are timing, motivation, and deal structure. Family offices deploy patient, multigenerational capital with no fund lifecycle pressure — they can hold positions for 15 years without an exit requirement, making them genuinely different from a VC's 10-year fund. Timing is slower: expect 3 to 12 months for a family office decision versus 4 to 6 months for a VC. Motivation is broader: family offices care about values alignment, legacy, sector resonance, and impact alongside financial returns — a purely financial pitch misses the most important decision criteria. Deal structure is different: 83% of family office startup deals are co-investments or club deals (PwC 2025 data), not traditional LP fund positions, meaning your best approach is to invite a family office to invest directly alongside your lead VC via an SPV. Cold outreach to family offices almost never works — warm intros from trusted co-investors convert at 10–15x the rate.When should a startup approach each type of investor?

Stage alignment is the most important factor. Angel investors are best approached at pre-revenue or very early revenue stages — they tolerate maximum uncertainty and invest based on founder conviction rather than metrics. Family offices typically invest after initial traction is demonstrated but before the metrics needed for a formal Series A are fully established; they are also excellent participants in institutional rounds as co-investors alongside a lead VC. Venture capital is best approached when you have the metrics required to build an LP-defensible investment thesis: for most SaaS Series A rounds, this means $500K to $1M ARR, strong month-over-month growth rates, clear unit economics, and a repeatable go-to-market motion. The Angel Investors Network's April 2026 guide notes that founders typically pitch 50 to 100 VCs to close one lead — building the traction that makes that process more efficient before starting it is the highest-return preparation.How do I find family office investors for my startup?

Family offices are the hardest investor type to find because many operate without public internet presence. The most effective sourcing approaches in 2026 are: (1) introductions from VCs who regularly work with family offices as LPs or co-investors — ask your existing investors if they have family office relationships they would be willing to facilitate; (2) family office-specific events and associations (FOA, UHNW Alliance, family office conferences); (3) placement agents or advisors who specialise in family office access; (4) LinkedIn outreach to family office investment officers who have a public profile — a higher-quality approach than generic cold outreach to a family office email address; (5) building the relationship 12 to 18 months before you need capital through genuine value exchange, shared events, and mutual contact development. Value Add VC notes that warm intros convert at 10–15x the rate of cold outreach for family offices specifically.What documentation do I need before approaching a VC?

Before approaching institutional VCs, you should have: Delaware C-Corporation incorporation (required by most VCs due to LP structure constraints); a clean cap table with all equity properly documented (SAFEs, options, angel notes all properly reflected); IP assignment agreements from all founders and key employees; a pitch deck (12 to 15 slides); a five-year financial model with clearly stated assumptions; a data room accessible via Notion, DocSend, or Google Drive containing key metrics, customer contracts (anonymised), incorporation documents, and cap table model; and customer references (three to five customers willing to speak to VCs directly). The quality of your data room signals organisational maturity to VCs — a well-prepared data room can accelerate the due diligence phase by two to four weeks. Ensure you are registered as a Delaware C-Corp before contacting institutional investors.How do I manage raising from multiple investor types simultaneously?

Use a simple CRM or tracking spreadsheet to manage each investor's process independently. Track: investor name, type (angel/FO/VC), stage of conversation, last contact date, next action, and notes on their specific interests and concerns. Update it at least weekly. The key principle for managing multiple types simultaneously is to understand how each type influences the others: VC competitive tension is primarily created by other VCs; family office confidence is significantly boosted by a credible VC lead committing; angels are influenced by the quality of other angels already committed. Use this influence structure to sequence conversations productively — get an early angel committed who can be named to family offices, then use family office co-invest interest as supplementary signal to VCs that strong non-institutional investors have already done diligence. Never misrepresent the status of any investor's commitment — the startup ecosystem is small and misrepresentation is discovered.References

Zyner.io — Angel Investors vs. Venture Capitalists: Key Differences Explained 2026 (March 2026) https://zyner.io/blog/vc-vs-angel-investorAngel Investors Network — Angel Investor vs Venture Capitalist: 2026 Guide (April 2026) https://angelinvestorsnetwork.com/venture-capital/angel-investor-vs-venture-capitalist-2026-guide

Value Add VC — Family Office Investing in Startups: How They Think and What They Want (May 2026) https://valueaddvc.com/blog/family-offices-investing-in-startups-how-they-think-and-what-they-want

GoingVC — Winning Family Offices in 2025: The VC Fundraising Playbook (August 2025) https://www.goingvc.com/post/winning-family-offices-in-2025-the-vc-fundraising-playbook

Qubit Capital — How to Win Family Office Funding: Key Strategies for Startups (January 2026) https://qubit.capital/blog/family-office-investments-startup-funding-guide

Qubit Capital — Family Office Startup Funding: Case Studies and Investment Strategies https://qubit.capital/blog/family-office-case-studies

Flowlie — Navigating the World of Family Office Structures for Startup Funding (April 2025) https://www.flowlie.com/blog/navigating-the-world-of-family-office-structures-for-startup-funding/

StartupOwl — Venture Capital Funding: How VC Works, Who Qualifies and How to Get a Meeting (February 2026) https://startupowl.com/fund/venture-capital-funding

Seedblink — Raising from VCs: A Practical Guide for Startup Founders https://seedblink.com/blog/raising-from-vcs-a-practical-guide-for-startup-founders

0 Comments Comments