Business

How to Read a Balance Sheet Like a Pro — Small Biz

Your Balance Sheet is a snapshot of everything your business owns, owes, and is worth at a single point in time. Most small business owners ignore it until the bank or an investor asks for it. This guide shows you how to read every line, calculate the seven key ratios, and use your Balance Sheet to make smarter decisions every month.

For a small business owner, the Balance Sheet answers some of the most fundamental questions about the business. Is the business solvent — can it pay its bills? Does it have enough short-term cash and assets to cover its short-term debts? How much debt has it taken on relative to its equity? Has it been building real wealth over time, or consuming it? These questions cannot be answered by looking at profit and loss alone.

Banks ask for Balance Sheets before approving business loans because they want to see whether the business has sufficient assets to secure the loan and whether it is already over-leveraged with debt. Investors ask for Balance Sheets because they want to assess the true net worth of the business before making any commitment. Even if you have no plans to raise finance, your Balance Sheet is one of the most important management tools available to you — provided you know how to read it.

The Balance Sheet is prepared at a specific date — often the last day of a financial year, quarter, or month. It covers a different dimension of financial health from the Profit and Loss statement, and both are needed for a complete picture of how the business is performing.

Assets are everything the business owns or is owed — cash, equipment, property, vehicles, stock, and money owed by customers. Liabilities are everything the business owes to others — loans, credit card balances, unpaid supplier invoices, and tax obligations. Equity (also called net worth, owners equity, or shareholders equity) is what is left over after subtracting all liabilities from all assets — it represents the owner's stake in the business.

The logic is straightforward: every asset the business has was either paid for with borrowed money (a liability) or funded by the owner's investment and accumulated profits (equity). The two sources of funding must, by definition, equal the assets they funded. If your business has £200,000 in assets, those assets were funded by some combination of debt and equity that adds up to exactly £200,000.

The Balance Sheet doesn't just tell you what your business is worth. It tells you how you got there — how much is funded by debt, how much by the owner, and whether the foundation is solid or fragile.

— ICAEW — UNDERSTANDING BUSINESS FINANCIAL STATEMENTS

Cash and bank balances are the most liquid asset of all: money sitting in your business current account or petty cash tin is immediately available. Accounts receivable (also called debtors or trade receivables) are amounts owed to your business by customers who have been invoiced but not yet paid. Inventory is the value of stock on hand — goods you have purchased or manufactured that are ready to be sold. Prepayments are expenses you have paid in advance but not yet received the benefit of — for example, a one-year insurance premium paid in January that covers you through December.

The total of your current assets is a key indicator of your business's short-term financial resilience. A business with strong current assets can weather a bad month or an unexpected cost without immediately running into problems.

It is important to note that fixed assets are not easily convertible to cash without disrupting the business. Selling a key piece of equipment to raise money might solve a short-term cash problem but could seriously damage your ability to operate. This is why lenders and analysts focus more on current assets when assessing short-term solvency.

The total of your current liabilities is critical to your short-term financial picture. If your current liabilities significantly exceed your current assets, the business may struggle to pay its bills as they fall due — a situation called illiquidity, which is one of the most common immediate causes of small business failure.

Equity has three main components. Share capital (for limited companies) or capital introduced (for sole traders and partnerships) is the money the owner(s) originally put into the business. Retained earnings (also called retained profit or accumulated reserves) are all the profits the business has generated and kept in the business over its lifetime, minus any drawings or dividends paid to the owner. Current year profit or loss is the net profit or loss for the current period that has not yet been transferred to retained earnings.

Growing equity over time is the ultimate indicator of a healthy, wealth-creating business. If equity is increasing year on year, the business is building real net worth — assets are growing faster than liabilities. If equity is declining, the business is consuming its reserves, which is unsustainable over the long term.

Negative equity — where total liabilities exceed total assets — is a serious warning sign. A business in negative equity has technically consumed all its reserves and is operating on borrowed money. While some businesses operate with negative equity for short periods during rapid growth, persistent negative equity typically indicates a business in financial difficulty.

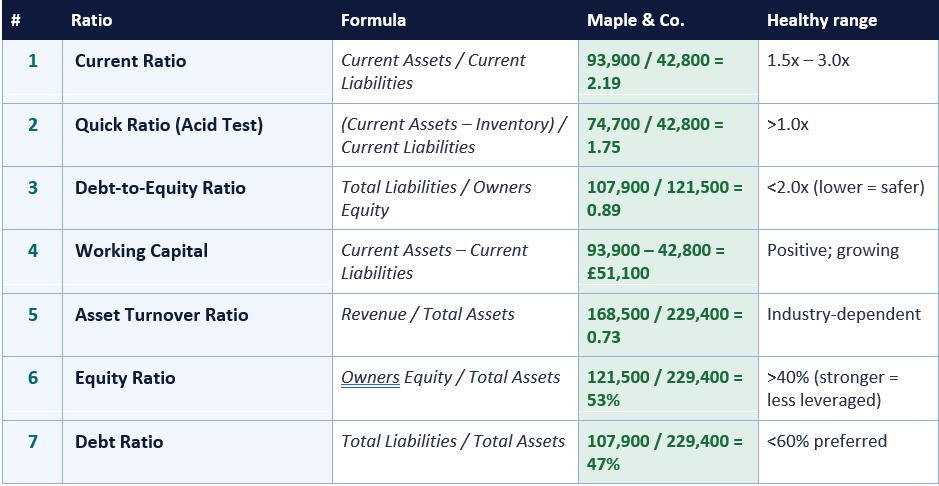

Maple & Co. is in good shape: current ratio of 2.19 means it has more than twice as many current assets as current liabilities; debt-to-equity under 1.0 means it is more equity-funded than debt-funded; working capital of over £51,000 provides a substantial buffer against unexpected costs.

Reading all three financial statements together — the P&L for profitability, the Balance Sheet for financial position and solvency, and the Cash Flow Statement for cash management — gives a complete and integrated picture of the business that no single statement can provide on its own. Most modern accounting software generates all three automatically from your bookkeeping entries.

Start by reviewing your own Balance Sheet today. Calculate the seven ratios in Section 7 and see how your business compares to the healthy benchmarks. Compare to last quarter and last year. If you spot warning signs, address them early — the earlier a financial problem is identified, the more options you have to fix it. And read your Balance Sheet alongside your P&L and Cash Flow Statement for the full picture that no single document can provide alone.

QuickBooks — Balance Sheet Explained: A Guide for Small Business Owners https://quickbooks.intuit.com/uk/blog/accounting/balance-sheet-explained/

Sage — Balance Sheet: What It Is and How to Read It https://www.sage.com/en-gb/blog/what-is-a-balance-sheet/

FreshBooks — Balance Sheet for Small Businesses: The Complete Guide https://www.freshbooks.com/hub/accounting/balance-sheet

ICAEW — Understanding Financial Statements for Business Owners https://www.icaew.com/technical/financial-reporting/information-for-business-owners

Investopedia — Balance Sheet: Explanation, Components and Examples https://www.investopedia.com/terms/b/balancesheet.asp

Investopedia — Current Ratio: Definition, Formula and Example https://www.investopedia.com/terms/c/currentratio.asp

GOV.UK — Prepare Annual Accounts for a Private Limited Company https://www.gov.uk/annual-accounts

US Small Business Administration — Financial Statements https://www.sba.gov/business-guide/manage-your-business/manage-your-finances

Wave Accounting — Free Balance Sheet Templates and Software https://www.waveapps.com/

TABLE OF CONTENTS

- What Is a Balance Sheet and Why Does It Matter?

- The Fundamental Accounting Equation: Assets = Liabilities + Equity

- Understanding Assets: What Your Business Owns

- Understanding Liabilities: What Your Business Owes

- Understanding Equity: What the Business Is Worth to Its Owner

- A Sample Balance Sheet for a Small Business

- The 7 Key Ratios Every Small Business Owner Should Calculate

- How to Spot Warning Signs in Your Balance Sheet

- How the Balance Sheet Connects to Your Other Financial Statements

- Common Balance Sheet Mistakes Small Business Owners Make

- Conclusion

- Frequently Asked Questions

- References

What Is a Balance Sheet and Why Does It Matter?

A Balance Sheet — also called a Statement of Financial Position — is a snapshot of your business's financial health at a single point in time. While your Profit and Loss statement shows what happened over a period (how much you earned and spent in the last month or year), the Balance Sheet shows where you stand right now: what the business owns, what it owes, and what is left over for the owner.For a small business owner, the Balance Sheet answers some of the most fundamental questions about the business. Is the business solvent — can it pay its bills? Does it have enough short-term cash and assets to cover its short-term debts? How much debt has it taken on relative to its equity? Has it been building real wealth over time, or consuming it? These questions cannot be answered by looking at profit and loss alone.

Banks ask for Balance Sheets before approving business loans because they want to see whether the business has sufficient assets to secure the loan and whether it is already over-leveraged with debt. Investors ask for Balance Sheets because they want to assess the true net worth of the business before making any commitment. Even if you have no plans to raise finance, your Balance Sheet is one of the most important management tools available to you — provided you know how to read it.

The Balance Sheet is prepared at a specific date — often the last day of a financial year, quarter, or month. It covers a different dimension of financial health from the Profit and Loss statement, and both are needed for a complete picture of how the business is performing.

The Fundamental Accounting Equation: Assets = Liabilities + Equity

Every Balance Sheet, for every business of every size in every country, is built on a single equation:Assets = Liabilities + Owners Equity

This equation must always balance — which is why the document is called a Balance Sheet. If the two sides do not balance, there is an error in the accounting. Understanding what this equation actually means in plain English is the key to reading any Balance Sheet with confidence.Assets are everything the business owns or is owed — cash, equipment, property, vehicles, stock, and money owed by customers. Liabilities are everything the business owes to others — loans, credit card balances, unpaid supplier invoices, and tax obligations. Equity (also called net worth, owners equity, or shareholders equity) is what is left over after subtracting all liabilities from all assets — it represents the owner's stake in the business.

The logic is straightforward: every asset the business has was either paid for with borrowed money (a liability) or funded by the owner's investment and accumulated profits (equity). The two sources of funding must, by definition, equal the assets they funded. If your business has £200,000 in assets, those assets were funded by some combination of debt and equity that adds up to exactly £200,000.

The Balance Sheet doesn't just tell you what your business is worth. It tells you how you got there — how much is funded by debt, how much by the owner, and whether the foundation is solid or fragile.

— ICAEW — UNDERSTANDING BUSINESS FINANCIAL STATEMENTS

Understanding Assets: What Your Business Owns

The asset section of the Balance Sheet is divided into two main categories: current assets and fixed assets (also called non-current assets). The distinction between them is based on how quickly they can be converted into cash.Current Assets

Current assets are assets that are expected to be converted into cash, consumed, or sold within the next twelve months. They are listed in order of liquidity — how quickly they can be turned into cash — starting with the most liquid.Cash and bank balances are the most liquid asset of all: money sitting in your business current account or petty cash tin is immediately available. Accounts receivable (also called debtors or trade receivables) are amounts owed to your business by customers who have been invoiced but not yet paid. Inventory is the value of stock on hand — goods you have purchased or manufactured that are ready to be sold. Prepayments are expenses you have paid in advance but not yet received the benefit of — for example, a one-year insurance premium paid in January that covers you through December.

The total of your current assets is a key indicator of your business's short-term financial resilience. A business with strong current assets can weather a bad month or an unexpected cost without immediately running into problems.

Fixed Assets (Non-Current Assets)

Fixed assets are assets the business owns and uses over a longer period — typically more than twelve months. They include tangible assets such as equipment, machinery, vehicles, computers, and property, and intangible assets such as patents, trademarks, and goodwill. Fixed assets appear on the Balance Sheet at their net book value — their original purchase cost minus accumulated depreciation. Depreciation is the accounting treatment that spreads the cost of a fixed asset over its useful life rather than expensing it all at once.It is important to note that fixed assets are not easily convertible to cash without disrupting the business. Selling a key piece of equipment to raise money might solve a short-term cash problem but could seriously damage your ability to operate. This is why lenders and analysts focus more on current assets when assessing short-term solvency.

Understanding Liabilities: What Your Business Owes

Liabilities represent all the financial obligations your business has to external parties — money you owe, rather than money you own. Like assets, liabilities are divided into current liabilities (due within twelve months) and long-term liabilities (due in more than twelve months).Current Liabilities

Current liabilities are obligations that must be settled within the next twelve months. These include accounts payable (money owed to suppliers for goods or services received but not yet paid for), short-term bank overdrafts, the current portion of any long-term loans (the amount due to be repaid in the next twelve months), VAT or sales tax owed to the tax authority, PAYE and National Insurance owed on payroll, and accruals — expenses that have been incurred but not yet invoiced, such as an accountant's fee for work done in March that has not yet been billed.The total of your current liabilities is critical to your short-term financial picture. If your current liabilities significantly exceed your current assets, the business may struggle to pay its bills as they fall due — a situation called illiquidity, which is one of the most common immediate causes of small business failure.

Long-Term Liabilities

Long-term liabilities are obligations due in more than twelve months — most commonly medium and long-term bank loans, director loans that are not expected to be repaid within the year, hire purchase agreements, and finance leases. Long-term debt is not inherently bad: using borrowed money to fund growth can be a sensible business strategy if the return on that investment exceeds the cost of the debt. But excessive long-term debt increases financial risk, particularly for businesses with variable or seasonal revenue.Understanding Equity: What the Business Is Worth to Its Owner

Owners equity — sometimes called shareholders equity, net assets, or simply equity — is the residual interest in the business after all liabilities have been deducted from all assets. It represents the net worth of the business from the owner's perspective.Equity has three main components. Share capital (for limited companies) or capital introduced (for sole traders and partnerships) is the money the owner(s) originally put into the business. Retained earnings (also called retained profit or accumulated reserves) are all the profits the business has generated and kept in the business over its lifetime, minus any drawings or dividends paid to the owner. Current year profit or loss is the net profit or loss for the current period that has not yet been transferred to retained earnings.

Growing equity over time is the ultimate indicator of a healthy, wealth-creating business. If equity is increasing year on year, the business is building real net worth — assets are growing faster than liabilities. If equity is declining, the business is consuming its reserves, which is unsustainable over the long term.

Negative equity — where total liabilities exceed total assets — is a serious warning sign. A business in negative equity has technically consumed all its reserves and is operating on borrowed money. While some businesses operate with negative equity for short periods during rapid growth, persistent negative equity typically indicates a business in financial difficulty.

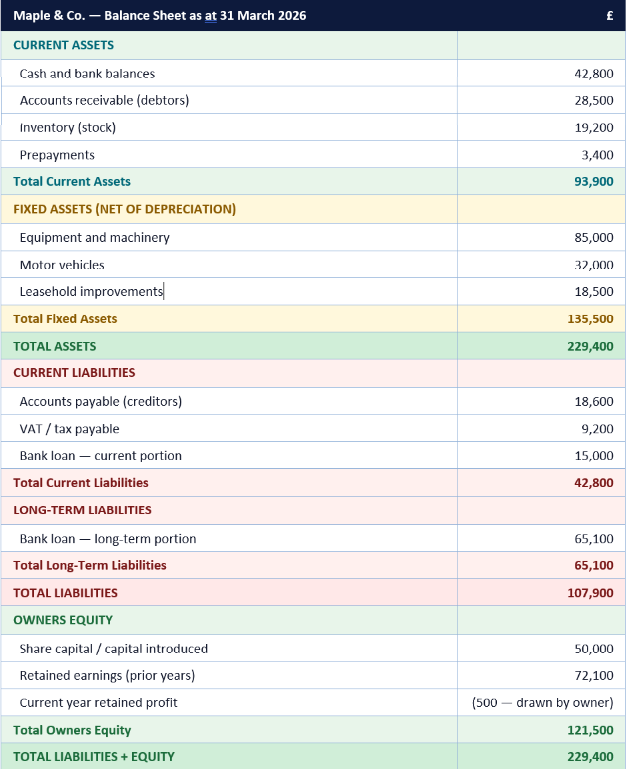

A Sample Balance Sheet for a Small Business

The following is a sample Balance Sheet for a fictional small business, Maple & Co., as at 31 March 2026. The same business appeared in our P&L guide. Use this as a reference as you work through the ratios in the next section.The 7 Key Ratios Every Small Business Owner Should Calculate

Once you understand the structure of the Balance Sheet, these seven ratios transform raw numbers into actionable intelligence about your business's financial health.Maple & Co. is in good shape: current ratio of 2.19 means it has more than twice as many current assets as current liabilities; debt-to-equity under 1.0 means it is more equity-funded than debt-funded; working capital of over £51,000 provides a substantial buffer against unexpected costs.

How to Spot Warning Signs in Your Balance Sheet

Once you can read a Balance Sheet, you can also use it to spot financial problems before they become crises. These are the warning signs that should prompt immediate investigation.Balance Sheet red flags every small business owner should know

- Current ratio below 1.0: Your current liabilities exceed your current assets. This means the business may not be able to pay its short-term debts as they fall due — a sign of potential insolvency risk.

- Rapidly growing accounts receivable: If debtors are growing faster than revenue, customers are taking longer to pay. This creates a cash flow squeeze and may indicate collection problems. Calculate your debtor days: (Accounts Receivable / Revenue) x 365.

- Inventory growing faster than sales: Suggests goods are not selling as fast as expected. Unsold inventory ties up cash and may eventually need to be written down, hitting profitability.

- Declining or negative equity: If equity falls quarter after quarter, the business is consuming its reserves. Negative equity means liabilities exceed assets — a very serious warning sign.

- High debt-to-equity ratio (above 2.0): The business is heavily financed by debt. High leverage amplifies both gains and losses and increases financial fragility, particularly in downturns.

- Short-term debt funding long-term assets: If long-term fixed assets are largely funded by short-term borrowing, this maturity mismatch creates refinancing risk. Long-term assets should generally be funded by long-term debt or equity.

- Large related-party loans in liabilities: Director loans or loans to/from associated companies that have grown significantly may indicate the business is propping up cash flow through non-commercial borrowing.

How the Balance Sheet Connects to Your Other Financial Statements

The Balance Sheet does not exist in isolation. It is the cumulative financial record of the business — every transaction that has ever been recorded flows into it in some way. Understanding how it connects to the Profit and Loss statement and the Cash Flow statement is the key to reading all three fluently.The link with the Profit and Loss statement

The net profit or loss from your P&L flows directly into your Balance Sheet through retained earnings. If your business made a net profit of £29,500 in the first quarter of 2026 (as in our Maple & Co. example), that profit adds £29,500 to retained earnings in the equity section of the Balance Sheet. The Balance Sheet is, in a sense, the accumulated history of every P&L your business has ever produced.The link with the Cash Flow statement

Changes in the current asset and current liability sections of the Balance Sheet between two dates directly drive the working capital section of the Cash Flow Statement. If accounts receivable grew from £20,000 to £28,500 between Balance Sheets, that £8,500 increase represents cash that has been earned (shown on the P&L) but not yet collected — a use of cash on the Cash Flow Statement. Understanding these linkages allows you to reconcile why a profitable business can still run short of cash.Reading all three financial statements together — the P&L for profitability, the Balance Sheet for financial position and solvency, and the Cash Flow Statement for cash management — gives a complete and integrated picture of the business that no single statement can provide on its own. Most modern accounting software generates all three automatically from your bookkeeping entries.

Common Balance Sheet Mistakes Small Business Owners Make

Even business owners who review their Balance Sheet regularly often make the same recurring mistakes in how they interpret and use it.Common mistakes to avoid when reading your Balance Sheet

- Only reviewing it once a year: The Balance Sheet is most useful when compared across periods. Quarterly reviews allow you to spot trends early — is working capital improving or declining? Is debt growing faster than equity?

- Ignoring the notes to the accounts: In formal accounts, the Balance Sheet is accompanied by notes that explain significant items. Loan terms, contingent liabilities, and asset valuation policies all matter and are typically explained in the notes.

- Confusing book value with market value: Fixed assets appear at historical cost minus depreciation — not at what they could be sold for today. A piece of equipment fully depreciated to zero on the Balance Sheet may still be worth significant money in the real world, and vice versa.

- Not reconciling accounts receivable: A large debtors figure looks good on paper, but if significant portions are old and unlikely to be collected, the true value is lower. Review your aged debtors report alongside the Balance Sheet figure.

- Treating directors' loans as permanent equity: A large director loan in the liabilities section is a real debt, even if there is no immediate intention to repay it. It affects all solvency ratios and needs to be managed like any other liability.

- Not comparing to the prior year: A single Balance Sheet tells you where you stand. Comparing to the same date in the previous year tells you whether the business is moving in the right direction.

CONCLUSION

The Balance Sheet is not just a document for the bank or your accountant. It is one of the most powerful management tools available to a small business owner — a real-time scorecard of your business's financial strength, solvency, and accumulated wealth. Once you can read it fluently, you can answer the questions that matter most: can the business pay its bills? Is it building or consuming net worth? Is the level of debt sustainable? Is working capital trending in the right direction?Start by reviewing your own Balance Sheet today. Calculate the seven ratios in Section 7 and see how your business compares to the healthy benchmarks. Compare to last quarter and last year. If you spot warning signs, address them early — the earlier a financial problem is identified, the more options you have to fix it. And read your Balance Sheet alongside your P&L and Cash Flow Statement for the full picture that no single document can provide alone.

Frequently Asked Questions

What is the difference between a Balance Sheet and a Profit and Loss statement?

A Balance Sheet is a snapshot of your business's financial position at a single point in time — what it owns (assets), what it owes (liabilities), and what it is worth to the owner (equity). A Profit and Loss statement shows financial performance over a period of time — revenue earned, costs incurred, and profit or loss generated. Together they give a complete picture: the P&L shows what happened; the Balance Sheet shows where you stand as a result.What does it mean if my current ratio is below 1.0?

A current ratio below 1.0 means your current liabilities (amounts due within twelve months) exceed your current assets (assets convertible to cash within twelve months). This indicates the business may not be able to meet its short-term financial obligations as they fall due. It does not necessarily mean insolvency is imminent — the business may have reliable credit facilities or cash flow — but it is a serious warning sign that requires attention.What is owners equity and how is it calculated?

Owners equity represents the net worth of the business from the owner's perspective. It is calculated as Total Assets minus Total Liabilities. It is made up of money originally invested in the business (share capital or capital introduced) plus all profits retained in the business over time (retained earnings), minus any drawings or dividends paid out to the owner. Growing equity over time indicates a business that is building real, lasting financial value.How often should a small business review its Balance Sheet?

Quarterly is the minimum for most small businesses, though monthly is better for businesses carrying significant debt, operating with thin working capital, or growing rapidly. The Balance Sheet is most useful when compared across multiple periods — tracking the trend of key ratios quarter by quarter reveals whether the business's financial position is strengthening or deteriorating, allowing early corrective action.What is working capital and why does it matter?

Working capital is Current Assets minus Current Liabilities. It represents the short-term financial buffer available to the business — the money available after all short-term obligations have been met. Positive and growing working capital is a sign of financial resilience. Declining or negative working capital is a warning sign, often indicating that the business is struggling to manage its short-term cash obligations. Working capital management — chasing debtors, managing stock levels, and negotiating supplier payment terms — is one of the most important operational finance tasks for any small business owner.What accounting software produces a Balance Sheet automatically?

Most modern small business accounting platforms generate a Balance Sheet automatically from your bookkeeping entries, including Xero, QuickBooks Online, Sage, and FreeAgent (UK); QuickBooks Online, FreshBooks, and Wave (US and international). You should be able to generate a Balance Sheet as at any date, and most platforms allow you to compare side by side with a prior period. If you are not yet using cloud accounting software, the automatic generation of the three core financial statements is one of the most compelling reasons to make the switch.References and Further Reading

Xero — What Is a Balance Sheet? https://www.xero.com/uk/guides/balance-sheet/QuickBooks — Balance Sheet Explained: A Guide for Small Business Owners https://quickbooks.intuit.com/uk/blog/accounting/balance-sheet-explained/

Sage — Balance Sheet: What It Is and How to Read It https://www.sage.com/en-gb/blog/what-is-a-balance-sheet/

FreshBooks — Balance Sheet for Small Businesses: The Complete Guide https://www.freshbooks.com/hub/accounting/balance-sheet

ICAEW — Understanding Financial Statements for Business Owners https://www.icaew.com/technical/financial-reporting/information-for-business-owners

Investopedia — Balance Sheet: Explanation, Components and Examples https://www.investopedia.com/terms/b/balancesheet.asp

Investopedia — Current Ratio: Definition, Formula and Example https://www.investopedia.com/terms/c/currentratio.asp

GOV.UK — Prepare Annual Accounts for a Private Limited Company https://www.gov.uk/annual-accounts

US Small Business Administration — Financial Statements https://www.sba.gov/business-guide/manage-your-business/manage-your-finances

Wave Accounting — Free Balance Sheet Templates and Software https://www.waveapps.com/

0 Comments Comments