Finance

How UK Political Instability Affects Your Personal Finance

Table of Contents

- Fourteen Years, Six Prime Ministers: The Timeline

- Case Study: The September 2022 Mini-Budget and Its Direct Hit on Household Finances

- How Political Instability Transmits Into Different Parts of Your Finances

- Mortgages and Borrowing Costs

- The Pound and Imported Inflation

- Pension Funds and Retirement Savings

- Business Investment and Employment

- Foreign Investment and Long-Term Growth

- Practical Steps to Protect Your Finances From Political and Market Volatility

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

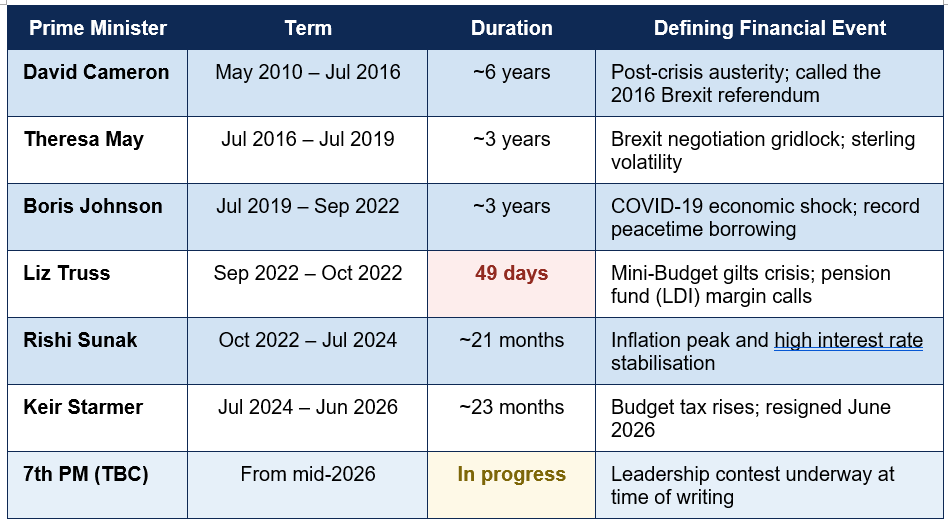

Between May 2010 and June 2026, the United Kingdom had six different Prime Ministers, with a seventh leadership transition underway following Keir Starmer's resignation announcement on 22 June 2026. That works out to an average premiership of roughly two years and four months over more than fourteen years — a level of leadership turnover that is genuinely unusual among major developed economies, and one that has coincided with some of the most volatile episodes in recent UK financial market history.

This is not simply a matter of political trivia. Financial markets, mortgage pricing, pension fund stability, and currency values all respond, often quickly and sometimes severely, to perceived political risk and policy uncertainty. The clearest illustration remains the September 2022 'mini-Budget' crisis under Liz Truss, Britain's shortest-serving Prime Minister at just 49 days in office, which triggered a sudden spike in government borrowing costs, forced the Bank of England into an emergency GBP 65 billion bond-buying intervention, and pushed more than 1,600 mortgage products out of the market within days.

This guide examines, with real data, how the UK's pattern of frequent leadership change has connected to tangible financial outcomes for ordinary households and savers — mortgage costs, pension stability, currency-driven inflation, and investment confidence — and, more importantly, what individuals can practically do to protect their own finances against this kind of recurring political and market volatility, regardless of which government is in office at any given time.

Fourteen Years, Six Prime Ministers: The Timeline

The scale of the turnover becomes clear when laid out in full. The table below tracks every UK premiership from May 2010 through the resignation of Keir Starmer in June 2026:

Average premiership length, 2010–2026: ~2 years 4 months — across six full or substantially complete premierships in just over fourteen years, compared to an average of closer to 4-5 years per Prime Minister across the preceding half-century (House of Commons Library research briefing, June 2026)

- Why this matters for markets, not just politics: Financial markets price in policy stability and predictability as part of how they assess risk on UK government debt (gilts), the pound, and UK equities. Frequent, often abrupt changes in economic leadership and policy direction — rather than any single ideology — tend to increase the risk premium investors demand to hold UK assets, a dynamic that shows up directly in borrowing costs for the government and, by extension, for mortgage holders and businesses.

Case Study: The September 2022 Mini-Budget and Its Direct Hit on Household Finances

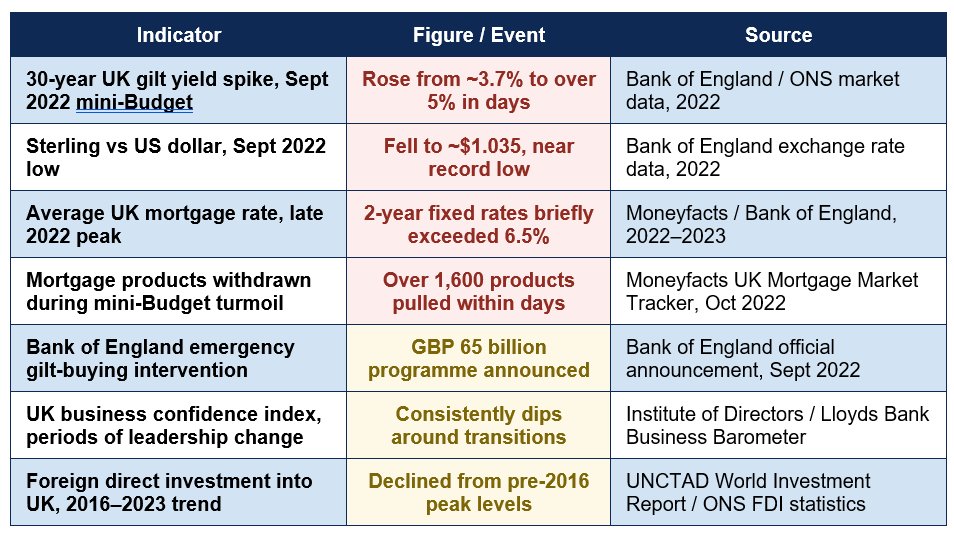

The clearest and most extensively documented example of political transition translating directly into personal financial harm came during Liz Truss's brief premiership. Her government's September 2022 'mini-Budget' announced large, largely unfunded tax cuts without an accompanying independent economic forecast from the Office for Budget Responsibility — a departure from established fiscal practice that financial markets interpreted as a significant increase in UK fiscal risk.The market reaction was rapid and severe. Yields on long-dated UK government bonds (gilts) spiked sharply within days, with 30-year gilt yields rising from around 3.7% to over 5%. Sterling fell to approximately $1.035 against the US dollar, close to its lowest level on record. The Bank of England was forced to intervene directly, announcing an emergency GBP 65 billion temporary gilt-purchase programme specifically to stabilise the market and prevent a more severe crisis.

The consequences for ordinary households were immediate and concrete, not abstract. Mortgage lenders, facing a sudden spike in the cost of the funding they rely on to price fixed-rate mortgages, withdrew over 1,600 mortgage products from the market within days as they scrambled to reprice in response to the gilt market turmoil. Average quoted rates on 2-year fixed mortgages briefly exceeded 6.5%, a dramatic jump from pre-crisis levels that meant millions of homeowners coming to the end of a fixed-rate deal in the following months faced significantly higher monthly payments than they had budgeted for, often adding hundreds of pounds to monthly repayments on a typical mortgage.

- The pension fund dimension: Less visible to most households, but arguably more systemically significant, was the impact on Liability-Driven Investment (LDI) strategies used by many UK defined-benefit pension funds. The speed and scale of the gilt yield spike triggered margin calls that some pension funds struggled to meet, requiring emergency asset sales and prompting the Bank of England's intervention specifically to prevent a disorderly collapse in this corner of the pension market — illustrating how political and fiscal instability can transmit risk into retirement savings well beyond the immediate mortgage market.

How Political Instability Transmits Into Different Parts of Your Finances

Mortgages and Borrowing Costs

Mortgage rates in the UK are priced substantially off the cost of funds in wholesale markets, which are themselves heavily influenced by gilt yields and Bank of England base rate expectations. When political instability raises perceived fiscal risk, lenders' funding costs rise, and those costs are passed through to new and remortgaging borrowers, often within days, as the 2022 episode demonstrated starkly.The Pound and Imported Inflation

A weaker pound, often triggered or amplified by political uncertainty, directly raises the cost of imported goods, fuel, and the many manufactured products the UK relies on global supply chains for. This contributes to the kind of imported inflation that erodes household purchasing power, separate from and in addition to domestic price pressures.Pension Funds and Retirement Savings

As the LDI episode demonstrated, the impact of acute political and fiscal instability is not confined to visible, day-to-day costs like mortgages — it can reach into the structural mechanics of pension funds, an area most savers assume operates independently of short-term political events until a crisis reveals otherwise.Business Investment and Employment

Surveys from bodies including the Institute of Directors and Lloyds Bank's Business Barometer consistently show measurable dips in UK business confidence around periods of leadership transition and policy uncertainty, since businesses delay major investment and hiring decisions when the policy environment they will operate in becomes harder to predict. Reduced business investment has knock-on effects for wage growth and job security that, while less immediately visible than a mortgage rate change, accumulate over time.Foreign Investment and Long-Term Growth

UNCTAD and ONS data on foreign direct investment into the UK show a declining trend since the period of heightened political turnover began around 2016, though this reflects multiple overlapping factors, including Brexit-related trade adjustments, rather than leadership turnover in isolation. Sustained foreign investment is a meaningful driver of long-term economic growth and job creation, making this a slower-moving but genuine channel through which political instability can affect the broader economic conditions household finances ultimately depend on.Practical Steps to Protect Your Finances From Political and Market Volatility

Individual households cannot control the pace of political change, but they can take concrete steps to reduce their exposure to the kind of sudden market shocks these transitions have repeatedly triggered:- Avoid relying on the lowest available fixed mortgage rate without a buffer: When choosing between mortgage products, factor in your ability to absorb a meaningfully higher rate at your next renewal, particularly if your current deal was secured during a period of unusually low rates. Building this buffer into your budget reduces the shock of a rate environment shift driven by a future fiscal or political event.

- Maintain a fully funded emergency fund independent of market conditions: A cash buffer of three to six months of essential expenses, held in an easily accessible savings account, provides genuine protection against the kind of sudden cost-of-living spikes that currency or rate shocks can trigger with little warning.

- Diversify investments geographically, not just by asset class: Holding investments concentrated entirely in UK equities, UK gilts, or sterling-denominated assets concentrates your exposure to UK-specific political and fiscal risk. A globally diversified portfolio, a standard recommendation from most regulated financial advisers, reduces the degree to which any single country's political turbulence can affect your overall wealth.

- Understand your pension fund's exposure to interest rate and gilt market risk: If you hold a defined benefit pension or a defined contribution pension invested partly in bond-heavy default funds, it is worth understanding, or asking a financial adviser to explain, how that fund is positioned relative to gilt market volatility, particularly in light of the 2022 LDI episode.

- Avoid making major financial decisions in the immediate aftermath of a political shock: The days immediately following a major political or fiscal announcement are typically the most volatile and the least informative period for making long-term decisions about mortgages, investments, or large purchases. Where possible, allow markets several weeks to digest and reprice before committing to major financial decisions during periods of acute uncertainty.

Conclusion

Six Prime Ministers in just over fourteen years is a genuinely unusual rate of political turnover for a major developed economy, and the data shows this has coincided with real, measurable financial consequences for UK households — most starkly during the September 2022 mini-Budget crisis, but more subtly through persistent effects on business confidence, currency stability, and foreign investment over the full period. These are not abstract economic statistics; they translate directly into mortgage costs, pension fund stability, and the price of everyday goods for millions of people.It is important to be precise about what this data does and does not show. Political instability has occurred under governments of different parties and different ideological directions, and the specific causes of each market episode discussed in this guide — fiscal policy choices, the pandemic, Brexit negotiations, global inflation — are distinct from leadership turnover itself, even where they are connected to it. The lesson is not about which party or individual is to blame, but about the structural reality that frequent, often abrupt changes in economic leadership increase the kind of policy uncertainty that financial markets price as risk, and that risk does not stay confined to Westminster — it reaches mortgage rates, pension funds, and weekly shopping bills.

For individual savers and households, the most productive response is not to attempt to predict the next political transition, but to build genuine resilience against the kind of volatility this period has repeatedly demonstrated: adequate cash reserves, mortgage decisions that can withstand a meaningfully higher rate environment, properly diversified investments, and a clear understanding of how your own pension and savings are positioned relative to UK-specific market risk. Political cycles will continue to turn at whatever pace they turn; a well-structured personal financial plan is what allows your own financial position to weather that turning, regardless of who occupies Downing Street next.

Frequently Asked Questions (FAQ)

How many Prime Ministers has the UK actually had since 2010?

Six full or substantially complete premierships: David Cameron (2010-2016), Theresa May (2016-2019), Boris Johnson (2019-2022), Liz Truss (2022, serving just 49 days, the shortest premiership in British history), Rishi Sunak (2022-2024), and Keir Starmer (2024-2026, who announced his resignation on 22 June 2026). A seventh Prime Minister was being selected at the time of writing, following the established process of the governing party choosing a new leader.Did the mini-Budget crisis really affect ordinary mortgage holders, or just financial markets?

It affected ordinary mortgage holders directly and immediately. Mortgage lenders withdrew more than 1,600 products from the market within days of the September 2022 mini-Budget as they repriced in response to the spike in gilt yields, and average quoted rates on 2-year fixed mortgages briefly exceeded 6.5%. Anyone who needed to remortgage or take out a new mortgage during this window faced materially higher costs than they would have a few weeks earlier, illustrating how quickly market-level instability can reach individual household budgets.Is this level of political instability unique to the UK, or does it happen elsewhere?

While leadership changes happen in every democracy, the pace of UK premiership turnover since 2016 in particular — five Prime Ministers in roughly eight years at one point — is unusual among major developed economies, most of which have seen considerably more stable executive leadership over the same period. This relative instability has been specifically cited by some international economic commentators and ratings agencies as a contributing factor in UK-specific risk premiums on government debt and currency volatility, alongside other factors like Brexit and global economic shocks.Should I avoid investing in UK assets because of this political instability?

This is a personal investment decision that depends on your individual circumstances, risk tolerance, and overall portfolio strategy, and this article does not constitute financial advice. What the data does support is the general principle, endorsed by most regulated financial advisers regardless of any specific country's political situation, that geographic diversification reduces concentration risk. Holding a globally diversified portfolio rather than one concentrated entirely in UK-domiciled assets is a standard risk-management approach that reduces your exposure to any single country's political or economic volatility, UK or otherwise.What is a Liability-Driven Investment (LDI) strategy, and why did it cause problems in 2022?

LDI strategies are investment approaches used by many UK defined-benefit pension funds to match their long-term liabilities (future pension payments) with appropriately matched assets, often using leveraged positions in gilts and derivatives to do so efficiently. When gilt yields spiked rapidly during the September 2022 mini-Budget crisis, many LDI strategies faced sudden, large margin calls — essentially requiring additional cash or collateral very quickly — that some pension funds struggled to meet without selling other assets at a loss. The Bank of England's emergency gilt-buying intervention was specifically designed to calm this market and prevent a broader pension fund stability crisis.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. House of Commons Library — Research Briefing: How Is a Prime Minister Appointed? (Updated June 2026)

https://researchbriefings.files.parliament.uk/documents/SN04256/SN04256.pdf

2. GOV.UK — Past Prime Ministers (Official List)

https://www.gov.uk/government/history/past-prime-ministers

3. Bank of England — Gilt Market Intervention Announcement, September 2022

https://www.bankofengland.co.uk/news/2022/september/bank-of-england-announces-gilt-market-operation

4. Office for National Statistics — UK Government Bond Yields and Exchange Rate Data

https://www.ons.gov.uk/economy/governmentpublicsectorandtaxes

5. Moneyfacts — UK Mortgage Market Tracker, October 2022

https://moneyfacts.co.uk/news/mortgages/

6. PBS News — 6 Leaders in 10 Years: A Look at the Quick Succession of British Prime Ministers

https://www.pbs.org/newshour/world/6-leaders-in-10-years-a-look-at-the-quick-succession-of-british-prime-ministers

7. UNCTAD — World Investment Report, Foreign Direct Investment Statistics

https://unctad.org/topic/investment/world-investment-report

8. Institute of Directors / Lloyds Bank — UK Business Confidence and Barometer Surveys

https://www.iod.com/news/

0 Comments Comments