Finance

Inflation, Energy Costs, and Saving by Switching Insurance

Table of Contents

- The Current Inflation and Cost-of-Living Picture

- How a Weaker Dollar Compounds the Squeeze

- Why Car Insurance Premiums Have Surged Faster Than General Inflation

- Why Switching Car Insurance Is an Unusually Effective Lever Right Now

- Where Households Are Finding Everyday Savings Right Now

- How to Switch Car Insurance Without Sacrificing Coverage Quality

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Household budgets across the United States are under renewed pressure in 2026. After a period of moderating price growth through late 2024 and 2025, inflation has reaccelerated, driven primarily by a sharp rise in energy costs and the lingering effects of a weaker dollar on imported goods. The result is a familiar but increasingly urgent feeling for millions of families: the same paycheque now covers noticeably less than it did even twelve months ago.

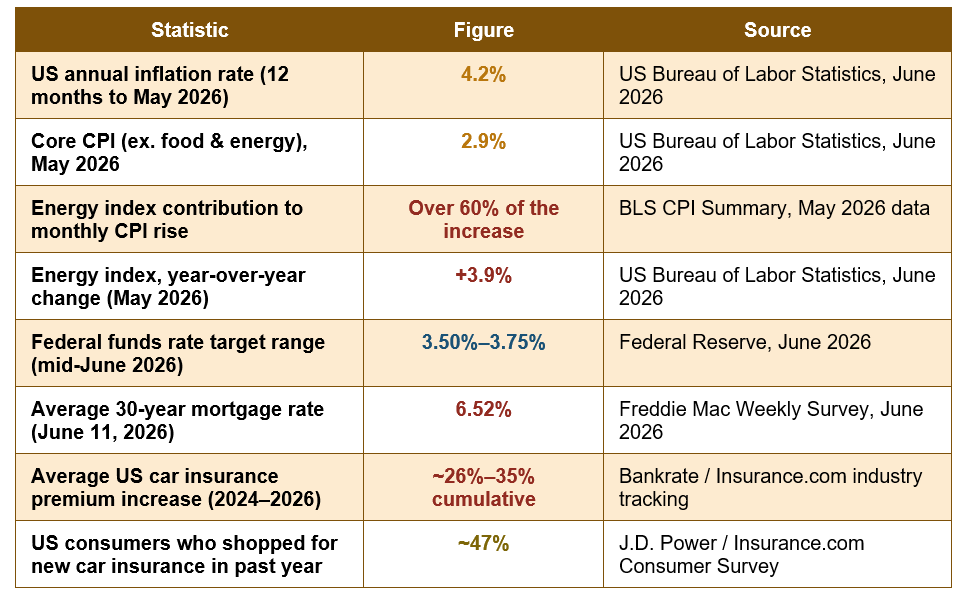

Unlike the inflation surge of 2021-2022, which was broadly distributed across goods and services, the current pressure is more concentrated — energy prices alone accounted for over 60% of the most recent monthly increase in the Consumer Price Index. This concentration matters because it shapes where households can realistically find relief. Broad-based inflation requires broad-based adjustment; energy-driven inflation, combined with currency weakness pushing up the cost of imported parts and materials, has made certain categories of spending — fuel, utilities, and the insurance products tied to vehicle ownership — disproportionately expensive relative to a year ago.

This is precisely why a growing number of households are turning their attention to one of the most overlooked, fastest-acting levers available to free up monthly cash flow: shopping around for car insurance. This guide explains the current inflation and cost-of-living picture in detail, the mechanics connecting a weaker dollar and elevated energy costs to household budgets, why car insurance specifically has become such a fertile area for savings, and a practical, step-by-step approach to switching providers without sacrificing coverage quality.

The Current Inflation and Cost-of-Living Picture

The data confirms what most households are already feeling at the till and the pump. The table below summarises the key figures shaping the current environment:

Annual inflation rate, 12 months to May 2026: 4.2% — up from 3.8% the prior month and the highest reading in roughly two years, with energy prices the dominant driver (US Bureau of Labor Statistics)

Why this inflation episode feels different: Core inflation (excluding food and energy) sits at a comparatively moderate 2.9%, while headline inflation has climbed to 4.2%. The roughly 1.3 percentage point gap between the two figures is unusually wide and reflects how concentrated the current price pressure is in energy specifically — a category households cannot easily substitute away from, since heating, fuel, and electricity are largely non-discretionary.

How a Weaker Dollar Compounds the Squeeze

Currency strength might seem like an abstract macroeconomic concept disconnected from a household grocery bill, but the mechanism connecting the two is direct and significant. The United States imports substantial volumes of crude oil refining inputs, vehicle parts, electronics, and consumer goods priced in global markets. When the dollar weakens relative to other major currencies, the cost of every one of these imported inputs rises in dollar terms — even if the underlying global price of the commodity or good has not changed at all.This dynamic is particularly consequential for energy markets. Crude oil is priced globally in US dollars, but the equipment, refining capacity, and geopolitical risk premiums embedded in energy markets respond to global supply and demand conditions that a weaker dollar does not offset — it can amplify the domestic cost impact instead. Combined with the elevated energy costs already flowing through from global supply disruptions, a weaker dollar effectively means American households are paying a double penalty: higher global energy prices, converted at a less favourable exchange rate.

The practical consequence for car owners specifically is twofold. First, the direct cost of fuel rises, squeezing the household transportation budget immediately and visibly every time a driver fills up. Second, and less visibly, the cost of vehicle parts, electronics, and components used in vehicle manufacturing and repair — many of which are imported or contain imported sub-components — also rises. This second effect feeds directly into the cost of claims that insurers pay out, which in turn feeds into the premiums insurers charge. Understanding this chain is essential context for why car insurance specifically has become such a significant and rapidly rising household expense.

Why Car Insurance Premiums Have Surged Faster Than General Inflation

Car insurance premiums have risen significantly faster than overall inflation over the past two years, with cumulative increases of roughly 26% to 35% depending on the state and insurer. This sharp increase reflects a combination of factors that together have pushed insurers to raise premiums well beyond the general cost-of-living increase most households have experienced.- Rising repair costs: Modern vehicles contain significantly more electronics, sensors, and computer-controlled systems than vehicles a decade ago, and many of these components are imported. A weaker dollar directly raises the cost insurers pay to repair or replace these parts, a cost that is passed through to policyholders via higher premiums.

- Higher vehicle values: The average new and used vehicle price has risen substantially over the past several years, meaning insurers face higher payouts for total-loss claims on a comparable percentage-of-vehicle-value basis.

- More frequent and more severe claims: Industry data shows an increase in both the frequency and average severity of auto claims, driven by factors including increased distracted driving, more severe weather events affecting vehicles, and rising medical costs associated with injury claims.

- Reinsurance and catastrophe cost pass-through: Insurers themselves purchase reinsurance to manage risk, and the cost of that reinsurance has risen amid more frequent severe weather events — a cost that flows through to the premiums charged to individual policyholders.

The combined effect is that auto insurance has become one of the fastest-rising line items in many household budgets — rising faster than rent, faster than groceries, and significantly faster than wages for most income brackets. This is precisely why it has become such an attractive target for households looking to recover meaningful cash flow without changing their lifestyle or cutting discretionary spending.

Why Switching Car Insurance Is an Unusually Effective Lever Right Now

Unlike many cost-of-living pressures, which require structural life changes to meaningfully address — relocating to reduce housing costs, changing jobs to increase income, or significantly altering long-term spending habits — switching car insurance providers is one of the few household savings actions that combines a large potential dollar saving with very low effort and virtually no lifestyle trade-off.This effectiveness stems from a structural feature of the insurance market: pricing for the same driver, the same vehicle, and the same coverage can vary dramatically between insurers, often by hundreds or even over a thousand dollars annually. This variation exists because different insurers use different proprietary algorithms to weigh risk factors — driving history, credit-based insurance scores, geographic location, vehicle type, and claims history — meaning no single insurer is consistently the cheapest for every type of driver. An insurer that prices aggressively for safe drivers in suburban areas may price uncompetitively for urban drivers with a recent claim, and vice versa.

The market inefficiency that benefits switchers: Because pricing algorithms differ so significantly between insurers, the loyalty many drivers show to their existing provider is rarely rewarded financially. Research from J.D. Power and multiple insurance comparison platforms consistently shows that long-tenured policyholders frequently pay more than new customers for functionally identical coverage — a phenomenon sometimes called 'price walking,' which several state insurance regulators have begun actively investigating and restricting.

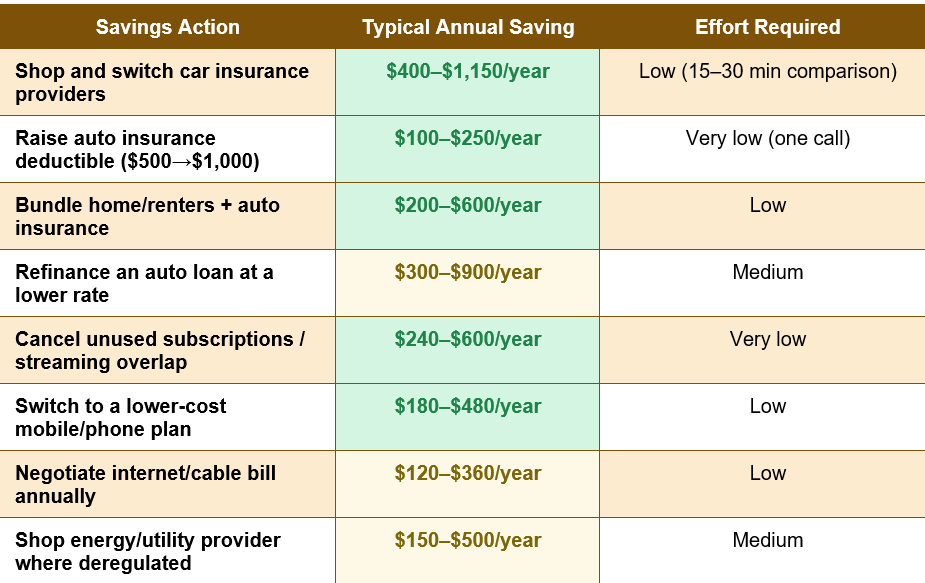

- Typical saving from switching car insurance providers: $400–$1,150 per year — based on national comparison data from insurance marketplaces tracking switching behaviour among drivers who actively shopped multiple quotes in the past 12 months (Bankrate / Insurance.com 2024–2026 data)

Where Households Are Finding Everyday Savings Right Now

Car insurance is the single largest and fastest-acting lever in most household budgets, but it is most effective when combined with a broader review of recurring monthly expenses. The table below ranks the most common cost-cutting actions households are taking in the current environment, by typical annual saving and effort required:

The clear pattern across this comparison is that the highest-saving actions also tend to require the least ongoing effort — they are one-time decisions (switching a provider, adjusting a deductible, cancelling an unused subscription) rather than ongoing behavioural changes (like reducing discretionary spending on dining or entertainment, which require sustained willpower and are far more likely to lapse after a few weeks). This is precisely why car insurance switching has become such a popular and frequently recommended starting point for households responding to the current inflation environment.

How to Switch Car Insurance Without Sacrificing Coverage Quality

Realising meaningful savings from switching insurance requires a structured approach — not simply choosing the cheapest quote on the first comparison page. The following steps maximise savings while protecting coverage quality:- Gather your current policy details first: Before requesting new quotes, write down your exact current coverage limits, deductibles, and any endorsements (roadside assistance, rental car coverage, gap insurance) so you can compare new quotes on a genuinely like-for-like basis rather than comparing a stripped-down quote against your current comprehensive policy.

- Get quotes from at least 4–5 providers: Use both online comparison platforms and direct quotes from major insurers, since not every insurer participates in every comparison site. Given how much pricing varies between insurers for the same risk profile, requesting fewer than four quotes substantially understates your potential savings.

- Check for the full range of available discounts: Bundling with home or renters insurance, multi-vehicle discounts, safe driver and telematics programs, good student discounts, low-mileage discounts, and professional or alumni association affiliations can all meaningfully reduce premiums and are sometimes not applied automatically — ask explicitly about every discount category.

- Confirm the new policy is active before cancelling the old one: Never allow a lapse in coverage between policies, even briefly, as a coverage gap can itself increase future premiums and, depending on your state, may violate legal insurance requirements.

- Review your policy annually going forward: Given current rate volatility, an annual review — even if you do not ultimately switch — ensures you catch any provider whose pricing has become uncompetitive before it costs you a full year of overpayment.

Conclusion

The combination of reaccelerating inflation, a weaker dollar pushing up the cost of imported energy and vehicle components, and genuinely elevated global energy prices has created a distinctly uneven cost-of-living squeeze — one concentrated heavily in categories like fuel, utilities, and auto insurance rather than spread evenly across all household spending. Understanding this concentration is the key to responding effectively: broad lifestyle austerity is rarely necessary or sustainable, but targeted action on the specific expense categories driving the current pressure can meaningfully restore household cash flow.Car insurance has emerged as one of the most effective targets precisely because of how this inflation episode has unfolded. Rising repair costs tied to imported parts, higher vehicle values, and increased claims severity have pushed premiums up faster than general inflation, while the structural pricing differences between insurers mean that switching providers — a low-effort, one-time action — can recover several hundred to over a thousand dollars annually without any change to coverage quality or lifestyle.

For households feeling the squeeze of this inflation environment, the most effective response is not generalised worry about the macroeconomic picture, but a specific, structured review of the expense categories most directly affected — starting with the policies and bills that have not been actively shopped or reviewed in the past year. Car insurance, given the scale of recent increases and the genuine savings available through switching, represents one of the clearest and fastest wins available to almost any household right now.

Frequently Asked Questions (FAQ)

Why has car insurance gone up so much more than other expenses?

Car insurance premiums have risen faster than general inflation because the underlying cost drivers — vehicle repair costs, vehicle values, claims frequency and severity, and reinsurance costs — have each risen significantly in their own right, compounding on top of broader inflationary pressure. Rising repair costs are particularly affected by currency weakness, since many vehicle parts and electronic components are imported and priced in foreign currencies or globally traded commodities.How often should I shop around for car insurance?

Most insurance experts recommend comparing quotes at least once a year, ideally a month or two before your policy renewal date. Given the current pace of premium increases and the documented tendency of insurers to raise long-tenured customers' rates faster than new-customer rates (sometimes called 'price walking'), an annual review has become more financially significant than it was during periods of more stable, predictable premium pricing.Will switching insurance providers hurt my credit score?

No. Insurance quotes typically involve a soft credit check (used to calculate a credit-based insurance score in most states), which does not affect your credit score, unlike a hard credit inquiry used for loan or credit card applications. You can safely request multiple insurance quotes without any negative impact on your credit profile.Does a weaker US dollar actually affect prices for things made in America?

Yes, indirectly but significantly. Even goods manufactured domestically frequently rely on imported raw materials, components, or machinery, meaning a weaker dollar raises production costs throughout the supply chain. Additionally, globally traded commodities such as crude oil are priced in US dollars on international markets, and currency weakness can amplify the domestic price impact of global supply and demand shifts, even though the headline price is denominated in dollars.What other household bills should I review alongside car insurance?

Beyond car insurance, the highest-value, lowest-effort reviews typically include: homeowners or renters insurance (which can often be bundled with auto for additional savings), mobile phone and internet plans (where promotional rates frequently expire after 12-24 months without notice), streaming and subscription services (where overlapping or unused subscriptions commonly go unnoticed), and, in deregulated energy markets, your electricity or natural gas supplier, where switching to a different retail energy provider can produce meaningful savings without any change to your actual utility service or delivery.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. US Bureau of Labor Statistics — Consumer Price Index Summary, May 2026

https://www.bls.gov/news.release/cpi.nr0.htm

2. Federal Reserve — Federal Funds Rate and Monetary Policy Press Releases

https://www.federalreserve.gov/monetarypolicy/openmarket.htm

3. Freddie Mac — Primary Mortgage Market Survey

https://www.freddiemac.com/pmms

4. US Inflation Calculator — Current US Inflation Rates 2000–2026

https://www.usinflationcalculator.com/inflation/current-inflation-rates/

5. Bankrate — Average Car Insurance Rates and Trends

https://www.bankrate.com/insurance/car/average-cost-of-car-insurance/

6. J.D. Power — US Auto Insurance Shopping and Satisfaction Studies

https://www.jdpower.com/business/press-releases

7. National Association of Insurance Commissioners (NAIC) — Auto Insurance Pricing and Consumer Protections

https://content.naic.org/insurance-topics/auto-insurance

8. Insurance.com — Annual Car Insurance Rate Trends and Shopping Survey

https://www.insurance.com/auto-insurance/coverage/average-car-insurance-rates

0 Comments Comments