Spending

Surcharges Are Everywhere: Why Americans Are Paying Up

Table of Contents

- The Bill at the Bottom of the Bill

- The Numbers: How Bad Has It Actually Gotten?

- The Surcharge Taxonomy: Every Fee You’re Now Paying

- The Psychology: Why the Lock-In Effect Makes You Pay Even When You’re Furious

- Why Businesses Prefer Surcharges to Price Increases

- The ‘Wellness Fee’ and Other Creative Names for the Same Thing

- The FTC Steps In — But Only Partially

- What the FTC Junk Fees Rule Actually Covers (and What It Doesn’t)

- The Backlash: When Surcharges Cost Businesses More Than They Earn

- What You Can Actually Do: The Practical Pushback Guide

- Conclusion: The Price You See Is Not the Price You Pay — Yet

- Frequently Asked Questions

- External References

The Bill at the Bottom of the Bill

You are at a restaurant. You have looked at the menu, made your decision, enjoyed the meal, and waited for the check. The check arrives. The food came to $68. The total at the bottom, the number you are actually expected to pay, is $77.52. Somewhere in the middle, quietly, between the food and the tip, there is a line that reads “Kitchen Appreciation Surcharge — 3%.” Nobody mentioned it. Nobody asked. And now, if you want to leave without paying it, you will have to make a scene.This is the experience of millions of Americans in 2026. Surcharges — additional charges layered on top of advertised prices for goods and services — have proliferated across industries to the point where they are no longer exceptions. They are the system. Credit card surcharges. Resort fees. Service fees. Fuel surcharges. Technology fees. Health and wellness funds. Low-income customer surcharges. Online checkout fees. They arrive, reliably, at the end of every transaction, after you have already decided to make the purchase.

The trend has a name — “fee fatigue” — and it has grown to the point where the federal government decided something needed to be done about at least part of it. The FTC issued its Rule on Unfair or Deceptive Fees, which took effect May 12, 2025. It was a start. But Americans are still paying surcharges at a rate that has only accelerated in the months since. This article examines where the surcharges come from, why businesses use them instead of simply raising prices, how the psychology works, what limited regulatory protection now exists, and what you can actually do about it.

The headline number: According to a JD Power study cited by The Wall Street Journal, 34 percent of small businesses now add credit card surcharges. Restaurant surcharges have jumped from 16 percent in 2022 to 20 percent in 2025, according to the National Restaurant Association. The WSJ described the trend as ‘fee fatigue’ spreading across the American economy.

The Numbers: How Bad Has It Actually Gotten?

The scope of the surcharge phenomenon is broad enough that tracking it comprehensively is genuinely difficult. Surcharges exist in dozens of forms across industries with different regulatory structures, different disclosure requirements, and different relationships to consumer expectations. What is measurable is directionally clear.Restaurant surcharges, once rare enough to generate local news coverage when a single restaurant added them, are now present at one in five restaurants nationally. The growth from 16 percent in 2022 to 20 percent in 2025 in just three years suggests the category is still expanding, not stabilising. Credit card surcharges have spread from a practice associated primarily with small, cash-preferred businesses to a standard feature at a third of small businesses nationally.

In the hotel sector, resort fees — mandatory additional charges for access to amenities like pools, gym facilities, and WiFi that a reasonable guest would expect to be included in the room rate — had, by some analyses, become so prevalent in Las Vegas and other resort-heavy markets that the effective cost of a room bore little resemblance to the advertised rate. The FTC estimated that in live-event ticketing and short-term lodging alone, consumers were wasting more than 50 million hours per year attempting to determine the true total price of purchases. That time was valued at more than $10 billion over a decade.

A Morning Consult survey found that 56 percent of Americans reported that junk fees had negatively affected their financial situation. Fifty-one percent reported a negative impact on their emotional well-being. In the financial sector, 62 percent of consumers expressed reduced trust in financial institutions specifically because of hidden fees. And remarkably, 74 percent of Americans said a candidate’s position on junk fees was an important factor in their voting decisions — a figure that places this consumer annoyance at the level of a political issue.

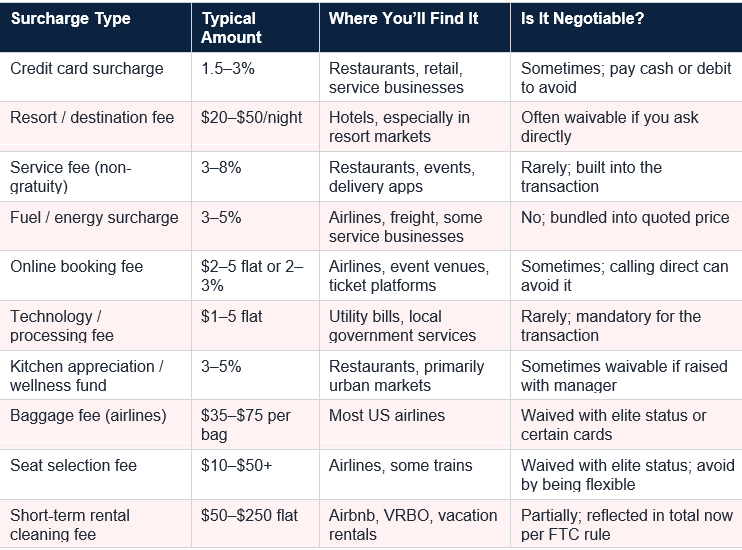

The Surcharge Taxonomy: Every Fee You’re Now Paying

The universe of surcharges and hidden fees has become complex enough that consumers benefit from understanding the different categories they are likely to encounter, their typical sizes, and what they are ostensibly for.

The naming creativity is notable. A “kitchen appreciation surcharge” sounds like a tip for the kitchen staff — but in most implementations, it is revenue that goes to the restaurant’s general operating fund, not directly to back-of-house employees. A “wellness fund” sounds like employer-provided healthcare for restaurant workers — and in some cases it is, but the labelling is inconsistent and rarely explained on the check.

The Psychology: Why the Lock-In Effect Makes You Pay Even When You’re Furious

The most revealing insight into the surcharge phenomenon comes not from the businesses deploying it but from the consumer psychologists who have studied it. Vicki Morwitz, a marketing professor at Columbia University, described the core dynamic to The Wall Street Journal with striking clarity: “Consumers tend to pay less attention to surcharges than to base prices.”This is the “lock-in effect,” and it is the foundational insight that makes surcharges a profitable strategy rather than a self-defeating one. By the time a surcharge appears on a restaurant bill, or a resort fee surfaces during online hotel checkout, or a service fee appears in a ticket purchase, the consumer has already mentally committed to the transaction. They have eaten the meal. They have spent 45 minutes selecting a hotel room and reading reviews. They have chosen their concert seats. The psychological cost of abandoning the transaction at that point — the sunk-cost reasoning, the inconvenience, the social awkwardness of refusing to pay at a restaurant — is higher than the cost of simply paying the surcharge.

Morwitz summarised the result precisely: “The next time I come back, I’m still drawn in by that initial low price. Even if I may have felt tricked the first time.” This is not irrational consumer behaviour. It is rational consumer behaviour in the face of intentionally designed information asymmetry. The low headline price attracts you. The locked-in surcharge extracts additional revenue from you. You are angry but compliant. And the business has calculated, correctly, that your anger will not translate into lost business at a rate that outweighs the surcharge revenue.

PYMNTS.com described it in April 2026: “By the time a surcharge shows up at the end of a transaction, consumers have already committed to the purchase and are much less likely to abandon it than if they had realized the full price from the start. That makes them angry, though it doesn’t lead them to alter their behavior.”

The academic term: Researchers describe the practice of advertising a low headline price and revealing mandatory fees only at the point of purchase as ‘drip pricing.’ The FTC’s analysis found it makes effective comparison shopping nearly impossible and causes consumers to systematically underestimate the true cost of purchases.

Why Businesses Prefer Surcharges to Price Increases

The obvious question is why businesses do not simply raise their prices rather than adding surcharges. If a restaurant needs 3 percent more revenue to offset credit card processing costs, why not charge $0.75 more for the burger rather than adding a checkout line that reads “Credit Processing Fee — 3%”?The Wall Street Journal’s analysis, cited across numerous publications in April 2026, identified the core reason: surcharges shift blame. A higher price for a burger is the restaurant’s decision. The burger costs what the restaurant charges it. A “credit card processing surcharge” is something the credit card company is doing to the restaurant, which the restaurant is unfortunately being forced to pass along to you. The framing externalises the cost and implies that the restaurant itself is a neutral party in the transaction rather than its architect.

The secondary reason is competitive psychology. If every competitor in a market is advertising $12 burgers and you raise your price to $12.36, you look more expensive. If you also advertise $12 but add a 3 percent surcharge at the end, your headline price remains competitive and the surcharge is mentally processed separately — and less carefully.

The tertiary reason is selective applicability. A surcharge can be applied only to certain transactions (credit card payments, not debit or cash), certain customers (those who book online versus by phone), or certain services (the pool access fee only applies if you use the pool — though resort fees are charged regardless). This creates an impression of optionality even when none practically exists.

Economist insight: Economists say businesses are opting for surcharges instead of raising base prices to avoid scaring off customers with higher sticker prices. ‘Companies often opt for surcharges instead of straight price increases because they shift blame to circumstances beyond their control.’ — The Wall Street Journal, April 2026

The ‘Wellness Fee’ and Other Creative Names for the Same Thing

Restaurant surcharges deserve particular attention because they have become their own creative category. Unlike credit card surcharges, which at least describe what they are nominally for, restaurant surcharges have proliferated under names that obscure their true nature and create confusion about where the money goes.The most common variants include:

- Kitchen Appreciation Surcharge or Back-of-House Fee: typically 3 to 5 percent, ostensibly to help restaurants pay kitchen staff competitively. In many implementations, the money goes into general restaurant revenue rather than being specifically distributed to kitchen employees. When servers are asked whether the fee goes directly to cooks, the answer is frequently uncertain.

- Wellness Fund or Healthcare Surcharge: 3 to 5 percent, ostensibly to help the restaurant provide healthcare benefits to employees. Similar ambiguity about how the funds are specifically used and distributed.

- Service Fee (non-gratuity): 18 to 20 percent charged in addition to or instead of tips in some restaurants. Unlike a traditional tip, this fee goes to the restaurant rather than directly to servers in most states.

- Inflation Surcharge or Tariff Adjustment: a newer category, emerging in 2025 and 2026, explicitly attributing the fee to inflation or tariff costs. In April 2026, several restaurant chains announced tariff surcharges specifically citing the Iran conflict’s impact on food supply costs.

The FTC Steps In — But Only Partially

The FTC’s Rule on Unfair or Deceptive Fees took effect on May 12, 2025, and represented the most significant federal action on surcharges and hidden fees in decades. It was, by most accounts, a meaningful step — and an incomplete one.The rule emerged from the Biden administration’s “junk fees” initiative, which identified hidden and deceptive pricing as a significant source of consumer harm and a contributor to the distorted price signals that make comparison shopping difficult. The FTC estimated that eliminating deceptive fee disclosure practices would save consumers billions of dollars and eliminate tens of millions of hours of time spent trying to determine the true cost of purchases.

The rule had significant bipartisan support in its core consumer protection logic. The American Hotel & Lodging Association, which had long lobbied for consistent national standards to replace a patchwork of state-level regulations, actually welcomed the rule. “A transparent process means a better experience and greater satisfaction for all guests,” the association wrote in a statement on the day the rule took effect.

However, opposition came from other industry groups. The US Chamber of Commerce argued that the FTC was acting on “questionable legal theories” and recommended the rule’s complete withdrawal. The Hotel Fees Transparency Act of 2025, which would extend similar requirements nationwide through legislation rather than FTC rulemaking, passed the House but remained pending in the Senate as of mid-2026.

What the FTC Junk Fees Rule Actually Covers (and What It Doesn’t)

Understanding the actual scope of the FTC’s junk fees rule is essential for consumers who believe it provides broader protection than it does.What It Covers

- Short-term lodging: hotels, motels, vacation rentals, and platforms like Airbnb and Vrbo. All mandatory fees — including resort fees, destination fees, and internet fees — must now be included in the total price displayed upfront, before the booking checkout page.

- Live-event tickets: concert tickets, sporting event tickets, and other live events. All mandatory fees, including service fees and facility charges, must be included in the displayed total price. Ticketmaster announced it would display all-in pricing in response to the rule.

- Mandatory ancillary services: any fee for a service the consumer cannot reasonably avoid. If a hotel automatically charges a resort fee that is not genuinely optional, it must be in the total price.

What It Does NOT Cover

- Restaurant surcharges: not covered. Restaurants can still add credit card fees, kitchen appreciation charges, wellness funds, and other surcharges at checkout without upfront disclosure, except where state law requires otherwise.

- Airline fees: not directly covered by this rule (airlines are regulated separately by the Department of Transportation, which has its own fee transparency rules).

- Credit card surcharges at retail: not covered. A shop charging 3 percent for credit card use is not subject to this rule as long as another payment method is available.

- Bank fees, overdraft charges, and financial services fees: not covered by this rule, though other FTC and CFPB actions have targeted some of these.

- Optional fees: fees for genuinely optional services do not need to be included in the upfront total price. Binocular rental at a stadium, room service, and spa appointments are all optional and can be disclosed at point of selection rather than upfront.

The FTC’s own example: If a hotel automatically charges a resort fee for the use of its facilities, the fee must be included in the total price because a reasonable consumer would expect use of the hotel’s facilities to be included with the stay. This is the key principle: mandatory reasonable expectation equals required upfront disclosure. — FTC FAQ on the Rule on Unfair or Deceptive Fees

The Backlash: When Surcharges Cost Businesses More Than They Earn

Not every business that has experimented with surcharges has found them profitable. A growing number of case studies show restaurants and retailers discovering that the backlash from surcharges — negative online reviews, social media complaints, loss of repeat customers — exceeded the revenue the fee generated.The dynamics are predictable in retrospect. Surcharges are most damaging in high-competition, low-differentiation markets where consumers have ready alternatives. A restaurant in a competitive urban neighbourhood adding a 3 percent kitchen fee is one decision away from a Yelp review that mentions it ten times. A small coffee shop adding a credit card surcharge risks pushing regulars to the competitor across the street who accepts credit cards without a fee.

The lock-in effect that protects businesses in the short term — consumers pay even when angry — does not protect them from long-term defection. The Columbia University research that identified the lock-in effect also noted its limits: consumers remember the feeling of being tricked. They may return to that restaurant twice more, drawn by the low headline price, but the accumulation of annoyance eventually tips into genuine avoidance.

Some restaurant groups that had adopted surcharges during the post-pandemic cost crisis have quietly removed them as competitive conditions normalised. The calculus changed: when surcharges were industry-wide, no single restaurant suffered competitively from having one. As some competitors removed theirs, restaurants that kept the fee found it increasingly conspicuous.

What You Can Actually Do: The Practical Pushback Guide

The regulatory framework provides partial protection. The lock-in psychology works against you. But there are practical strategies that reduce your exposure to surcharges and, in many cases, allow you to avoid or recoup them.At Restaurants

- Ask before you commit. Before sitting down, ask whether the restaurant adds any service fees or surcharges to the check. In states without mandatory disclosure, this is the only pre-commitment warning you will get.

- Pay with cash or debit. Credit card surcharges specifically target credit card payments. Paying with cash or a debit card eliminates this fee entirely in establishments that charge it.

- Challenge non-tip service fees. A “service fee” that goes to the restaurant rather than your server is not a tip and does not go to the person serving you. Ask the manager where the money goes. In many cases, they will waive it for a customer who asks directly and politely.

- The FTC rule now requires total price disclosure upfront. If you are still being surprised by a resort fee at checkout, the hotel may be in violation of the rule. File a complaint at reportfraud.ftc.gov.

- For existing reservations, call the front desk and ask to have the resort fee waived. This works more often than most people expect, particularly for guests with elite status, long stays, or a simple willingness to ask. Hotels prefer not to lose a booking over a fee.

- Use status or affiliated credit cards. Many hotel credit cards with annual fees waive resort charges for cardholders, which can represent significant savings if you travel frequently.

Online and Ticketing

- Look for all-in pricing. Since the FTC rule took effect, many platforms display all-in prices by default. If you are still seeing low base prices with fees added at checkout, the platform may not be compliant — or the fees are genuinely optional.

- Compare total prices, not base prices. When booking hotels or buying event tickets, always compare based on the final checkout total, not the advertised headline price. Price comparison engines increasingly surface all-in prices.

- Report persistent violations. If a hotel or ticket platform is still hiding mandatory fees until checkout, file a complaint with the FTC at reportfraud.ftc.gov. The rule has enforcement mechanisms and the FTC has brought actions against companies for similar deceptive pricing practices.

Conclusion

Surcharges are not a new phenomenon. Airlines have charged for checked bags since 2008. Hotels have charged resort fees for decades. What is new in 2026 is the speed of proliferation, the creative naming, and the cultural normalisation. “Fee fatigue” describes not just consumer frustration but a kind of resignation: people have grown accustomed to the gap between the price they see and the price they pay. That resignation is exactly what businesses have been counting on.The FTC’s rule is a genuine step toward transparency, but its scope is limited. It covers hotels and concert venues. It does not cover restaurants, airlines (separately regulated), credit card surcharges at retail, or the dozens of other contexts in which Americans encounter end-of-transaction surprises every week. A more comprehensive federal standard — one that requires all mandatory fees to be included in advertised prices across all industries — has bipartisan support in principle but faces a significant lobbying headwind from the industries most profitably engaged in the practice.

In the meantime, the most effective consumer protection is information. Knowing why businesses use surcharges rather than price increases. Knowing the lock-in psychology and why you pay even when you are furious. Knowing which fees are regulated, which can be waived by asking, and which are genuinely unavoidable. And knowing that an angry consumer who both pays and complains is precisely what the business model counted on — which means the only truly effective individual pushback is the one that actually affects the business’s bottom line.

The price you see is not the price you pay. It will not be the price you pay until the law requires otherwise — or until enough consumers decide that the annoyance translates into something more consequential than a grumble on the way out the door.

Frequently Asked Questions

Why are there so many surcharges now?

Multiple factors have converged simultaneously. Post-pandemic inflation raised business costs across labour, food, and energy. Credit card processing fees (typically 1.5 to 3.5 percent per transaction) have increased as card issuers raised interchange rates. Labour shortages drove wages up, particularly in food service. And the pandemic normalised the consumer acceptance of digital checkout screens that make adding line items straightforward. Businesses discovered that surcharges generate revenue with less competitive blowback than equivalent price increases.What is ‘fee fatigue’?

Fee fatigue is the term used by consumer researchers and economists to describe the accumulated frustration consumers experience from encountering numerous small additional charges across transactions. Studies show it reduces consumer trust in businesses and industries, negatively affects emotional well-being (51 percent of consumers in a Morning Consult survey), and contributes to a general sense that advertised prices are not honest representations of actual costs. Despite the frustration, it rarely leads to immediate behaviour change because of the lock-in effect.What is the FTC junk fees rule and what does it require?

The FTC’s Rule on Unfair or Deceptive Fees took effect on May 12, 2025. It requires businesses selling live-event tickets and short-term lodging (hotels, vacation rentals) to display the total price — including all mandatory fees — whenever a price is advertised. Businesses cannot reveal mandatory fees only at the end of the checkout process. The rule does not cover restaurants, airlines, retail credit card surcharges, or most other industries.Can a restaurant legally add surcharges without telling me upfront?

In most US states, yes. There is no universal federal requirement for restaurants to disclose surcharges before you order. Some states have their own requirements: California required prominent menu disclosure of surcharges starting in July 2024. Other states have no specific rules. Best practice is to ask the server or check the menu’s fine print for any mention of service fees, credit card surcharges, or other additional charges before committing to a table.Can I refuse to pay a restaurant surcharge?

In theory, yes — if you were not informed of it before the service. In practice, refusing creates a confrontational situation. The more effective approach is to raise it calmly with a manager, ask what the surcharge is for, and request that it be waived. Many managers will accommodate a reasonable, polite request, particularly for a customer who is otherwise paying their bill and tipping appropriately. If the surcharge was not disclosed anywhere on the menu or at entry, you have a stronger position.What is ‘drip pricing’?

Drip pricing is the practice of advertising an attractively low base price and then incrementally revealing mandatory fees throughout the purchasing process — at checkout, on the confirmation page, or on the final bill. The FTC has described it as a deceptive practice that makes comparison shopping nearly impossible and causes consumers to systematically underestimate the true cost of purchases. It is now prohibited in hotel and live-event ticketing contexts under the 2025 FTC rule.Are credit card surcharges legal?

In most US states, yes — with restrictions. Merchants are generally permitted to charge a surcharge for credit card use, but the surcharge cannot exceed the merchant’s actual processing cost (typically 1.5 to 3.5 percent) and must be clearly disclosed before payment. Some states, including Massachusetts, have their own restrictions. Merchants are generally not permitted to surcharge debit card transactions. The FTC’s junk fees rule does not directly address retail credit card surcharges, though the rule’s general transparency requirements apply if the surcharge is mandatory and unavoidable.What is a resort fee and can I avoid it?

A resort fee is a mandatory additional charge at hotels for access to facilities like pools, gyms, WiFi, and parking. They range from $20 to $50 or more per night at resort properties. Since the FTC’s rule took effect in May 2025, hotels must now include resort fees in the total price displayed during booking rather than revealing them at checkout or check-in. You can still try to negotiate them off your bill at check-in, particularly if you are not using the facilities, have elite status, or are staying for multiple nights. Success rates vary.How do I report a business for violating the FTC junk fees rule?

You can file a complaint at reportfraud.ftc.gov. Provide the business name, website, and a description of how the fee was disclosed (or not disclosed). The FTC uses complaint data to identify patterns and prioritise enforcement. For individual disputes with hotels or ticket platforms, you can also dispute the charge with your credit card company if the fee was not disclosed before you made the purchase.Are junk fees actually a political issue?

More than most consumer protection topics, yes. A Morning Consult survey found that 74 percent of Americans said a candidate’s stance on junk fees was an important factor in their voting decisions — a remarkable figure for a policy topic. The Biden administration made junk fees a signature consumer protection issue, and the FTC rule was part of that initiative. The Trump administration has not reversed the rule but has taken a more permissive stance toward business practices generally. Bipartisan support for basic fee transparency legislation exists in Congress, though it has not advanced to final passage.External References

PYMNTS.com — Americans Grudgingly Accept Surcharges as Consumer Confidence Wanes (April 2026), Daily Voice — Hidden Costs Adding Up: Sudden Surcharge Surge Frustrating Consumers (April 2026), FTC — Rule on Unfair or Deceptive Fees: Frequently Asked Questions, FTC — Rule on Unfair or Deceptive Fees to Take Effect on May 12, 2025, GovFacts — Junk Fees: The Hidden Costs Americans Pay (December 2025), Britannica Money — FTC Junk Fees Rule: What It Means for Consumers, Hotel Dive — How the FTC’s Junk Fees Rule Sets a Standard for Hotel Pricing Nationwide (May 2025), Empower — FTC Junk Fees Rule: What It Means for Travel, Rentals and Event Tickets, Morgan Lewis — FTC Issues Final Junk Fees Rule to Crackdown on Aggressive Pricing Practices (January 2025), FTC — Report Fraud (Consumer Complaint Portal)

0 Comments Comments