The 4 Types Of Assets The Rich Own: A Guide to Wealth Building

You are about to get a clear, practical map of how many affluent households hold and grow wealth in the United States. This piece defines assets as the main classes used to store value, produce income, and compound gains over time. This is an informational, US-focused overview—not personal investment advice. Your ideal mix will depend on your goals, time horizon, and risk tolerance. I'll use a simple decision framework: cash flow, stability, and growth potential. That way you can compare options without getting lost in hype. In plain terms, I’ll walk through cash and equivalents, real estate, ownership in companies (stocks), and bonds — and explain why each appears in many affluent portfolios. You can also read a related summary in this brief overview.

Remember: where you keep money matters beyond returns. Liquidity, control, and the ability to act fast shape outcomes. An asset must be easy to document, access, and transfer when life happens.

Key Takeaways

- Assets here mean core holdings that store value and generate income.

- Focus on cash flow, stability, and growth when you compare options.

- Real estate, stocks, bonds, and cash equivalents are common in wealthy portfolios.

- Liquidity and control can be as important as raw returns.

- Your best mix depends on goals, timeline, and risk tolerance.

Why rich people diversify assets to build wealth in today’s market

Diversification is not a luxury for wealthy households — it's a practical strategy they use every day. You can evaluate holdings with one simple triad: cash flow, stability, and growth potential. This framework helps you compare any investment without a finance degree.

Cash flow, stability, and growth potential as your decision framework

Look at each holding and ask three plain questions: does it pay income, is its value predictable, and can it grow over time? That quick check shows you how an asset will help your portfolio in both calm and stressed conditions.

Why liquidity matters more than you think during downturns and life events

Liquidity lets you act when circumstances change. During recessions, job loss, or a medical emergency, liquid reserves stop you from selling long-term holdings at bad prices. Stability is useful, but stable does not always mean easy to sell.

What conservative portfolios look like for many high-net-worth investors

Conservative allocations often include meaningful cash, high-quality bonds, and broad equity exposure rather than speculative bets. Vanguard data shows many US millionaire households mix stocks, bonds, and cash rather than concentrating in one place — a pattern you can emulate.

- Diversify to reduce single-asset risk.

- Keep liquid reserves to avoid forced sales.

- Balance income and growth to smooth returns.

For more on how wealthy people allocate across holdings, read a practical summary of how wealthy Americans invest here. Next, you’ll get a clear breakdown of the four core classes and the role each plays in a resilient portfolio.

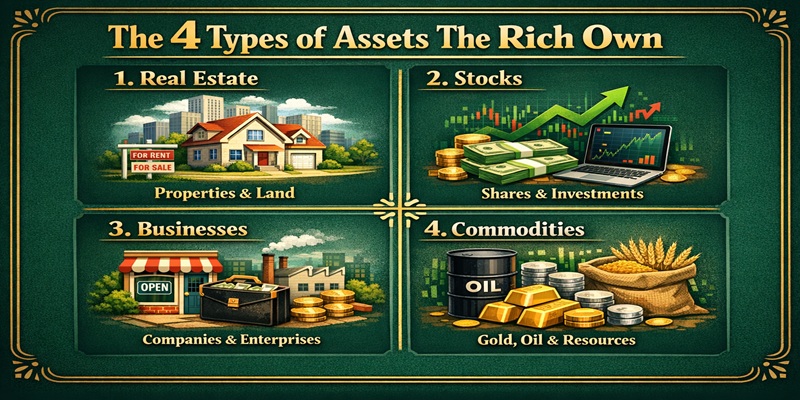

4 Types Of Assets The Rich Own

Smart portfolios assign roles. Each class performs a job: agility for quick moves, durable value for the long run, growth via ownership, and ballast when markets wobble.

Cash and cash equivalents for agility and opportunity

What it does: Keeps you ready for emergencies and buying opportunities when prices drop.

Real estate properties for long-term value and rental income

What it does: Delivers rental income and potential appreciation, but is less liquid than cash.

Stocks and ownership in companies for growth and dividends

What it does: Lets you compound value through company growth, dividend income, and broad funds for diversification.

Bonds for steadier income and portfolio ballast

What it does: Smooths volatility, supplies interest income, and acts as ballast when equities fall.

- Quick glance: cash for agility; real estate for durable value; stocks for growth; bonds for stability.

- Pende rick data shows wealthy holdings commonly split across bank and brokerage accounts, property, and company shares.

- Your optimal blend should match your horizon, cash needs, and tolerance for drawdowns.

| Asset | Role | Typical wealthy allocation |

| Cash | Liquidity & opportunities | 25%-34% |

| Real estate | Income & long-term value | 12%-15% |

| Stocks | Growth & dividends | ~20%-30% |

| Bonds | Stability & interest | 12%-15% |

For a clear practical summary of how these classes work together, see this four-asset framework. Each following section dives into allocation ranges, benefits, and hidden risks like inflation and documentation friction.

Cash and cash equivalents the wealthy keep for flexibility

You should view cash holdings as a tool for speed and safety in volatile markets.

Why it matters: Market reports show many affluent households hold about 25% to 34% in liquid reserves. That level lets you act fast and avoid selling long-term holdings at poor prices.

Where cash commonly sits

People keep money in bank accounts, brokerage cash sweeps, and safe deposit boxes. About 31% of wealthy portfolios use one or more of these locations. Access rules vary by provider and country.

Cash equivalents and when to use them

Cash equivalents include money market funds, T-bills, CDs, and commercial paper. Use short-term bills for safety and money markets for ready liquidity.

Risks you should know

Inflation slowly erodes buying power if your yield lags price growth. A key fact: 22.7% of deposit boxes are overdue at any time and 14.2% lack current owner records, creating access headaches.

| Holding | Role | Access note |

| Bank deposit | Immediate liquidity | Fast electronic access |

| Brokerage cash | Trading ready | Linked to accounts and custodial rules |

| Safe deposit box | Physical cash or documents | Requires ID and renewal; owners may be unknown |

Keep clear records and update access information so family members can find critical information in time. That small step protects value and preserves transferability of every asset.

Real estate investment strategies the rich use to grow net worth

Well-chosen property can deliver steady cash flow while preserving value across cycles.

Allocation context: Many high-net-worth portfolios hold about 12% to 15% in real estate. That level keeps property as a meaningful slice without crowding out other holdings.

How most investors scale holdings

You often start with a primary residence, then add one or more rental properties as experience grows. Later, some move into commercial holdings to expand cash flow and diversification.

Residential vs. commercial — quick comparison

| Asset class | Typical cash flow | Liquidity & management |

| Multifamily residential | Regular rental income | Moderate liquidity; active property management |

| Offices / hotels / warehouses | Higher income potential, variable | Lower liquidity; complex leases and business operations |

| Primary residence | Indirect value and stability | Least liquid for quick cash; tax timing advantages on sale |

Why rental income and records matter

Rental income acts as core passive income that complements dividends and interest during market swings. Remember tax timing: gains are generally taxed when you sell, not while you hold.

Practical note: About 16% of prestigious homes worldwide have unclear ownership. Clean title, updated entity records, and solid documentation protect transferability and preserve value when you pass holdings to heirs.

Stocks, dividend income, and ownership in companies

Equity ownership often serves as the engine of long-term growth in many high-net-worth portfolios. In the US, wealthy families typically allocate a meaningful slice to public and private equity to capture business earnings and compounding over time.

How wealthy households lean into stocks, funds, and retirement accounts

Penguin Analytics shows UHNW/HNW families dedicate about 17.2% to stocks, split between private company shares (9.1%) and public stock (8.1%).

Bank of America data adds perspective: many millionaires hold roughly 55% in stocks, mutual funds, and retirement accounts. That mix speeds growth while keeping retirement and tax wrappers in play.

Dividend stocks as a complement to rental income

Dividend-paying securities provide steady income that can pair with rental receipts. Some investors use dividends to cover expenses, reducing the need to

sell holdings in weak markets.

Public vs. private ownership and funds

Ownership can mean public shares, private company equity, or private equity exposure. Private equity offers higher returns but brings complexity and transfer limits.

Mutual funds and ETFs let you diversify fast across sectors and geographies. For example, spot Bitcoin ETFs approved in early 2024 let you track price moves without holding crypto directly.

- Equities compound through earnings growth and reinvestment.

- Dividend income adds stability to cash flow.

- Broker records matter: missing account IDs or signing-entity details can block access when time is critical.

Next, compare equity volatility with bonds and how fixed income adds portfolio ballast for risk management.

Bonds and fixed-income assets for stability and risk management

Bonds act as the quiet anchor in many wealthy portfolios, locking in steady income when markets wobble.

Why they matter: This asset class supplies steadier income, lower volatility than stocks, and useful diversification when equities fall.

Why wealthy investors commonly allocate roughly 12% to 15%

Many high-net-worth investors keep about 12%–15% in bonds to preserve capital without giving up growth. That range gives you balance: enough stability to

dampen swings, but enough equity to chase growth.

Treasury bonds vs. corporate bonds

Treasuries offer high safety and lower credit risk, while corporate bonds usually pay higher yields for added risk.

Simple rule: higher returns typically mean higher risk. Mix both to match your tolerance and timeline.

When active bond management matters

Rising inflation or political uncertainty can push bond prices and yields around. That is when active management—duration control, credit checks, and laddering—helps protect real returns and liquidity.

- Job: Provide cash flow through interest and lower portfolio volatility.

- Allocation guide: Use 12%–15% as a stabilizer, not an anchor that halts growth.

- Practical steps: ladder maturities, monitor credit quality, and factor tax treatment into decisions.

Alternative assets: why most high-net-worth investors keep this slice small

You will find that nontraditional holdings sit on the edge of most portfolios rather than at the center.

What counts as alternative investments

Alternative investments include art, collectibles, fine wine, classic cars, and digital items like crypto and tokenized goods. These items differ from stocks, bonds, cash, and real estate because they lack standard pricing and routine markets.

Portfolio reality check

Only about 3.29% of high-net-worth portfolios report exposure to alternatives. That shows most wealthy people treat these holdings as a small satellite allocation. Wealth planning favors predictable cash flow and transferability first, then small bets on novelty.

Volatility, liquidity, and the crypto contrast

Alternatives carry extra custody work, uncertain pricing, and higher liquidity risk. That makes them harder to use when you need cash fast.

Cryptocurrencies are more volatile: roughly 4.32% report crypto exposure versus 0.62% in asset-backed tokens. Tokens tied to physical goods may track commodity value more closely and swing less.

Bottom line: alternatives can add upside potential, but they also add complication and risk. Keep them small, document ownership, and prioritize core holdings first.

How to think like the wealthy about risk, returns, and keeping money transferable

Think of risk and transferability as twin parts of smart wealth planning: one manages market moves, the other manages family moves.

Liquidity vs. transferability: an item can trade fast in markets but still be hard for heirs to access. Missing account numbers, outdated beneficiary forms, or complex signing entities create delays at banks and broker desks.

KYC and documentation friction slow access. Modern source-of-wealth checks and identity rules make banks pause when information is incomplete. Brokers may refuse a request without contract numbers or signing-entity details.

"On average, families lose about $340,000 per $1,000,000 during transfers,"

Penguin Analytics found many transfers fail: roughly 7 out of 10. Losses can hit 72%–91% in some categories; overall clip is ~34%. Only 2% know up to 31% can vanish from data gaps.

Building an asset inventory

Treat each asset like a file. A single holding may need up to 22 attributes to move cleanly. That data keeps value usable and prevents delays that erode returns.

Practical portfolio strategies

- Reframe liquidity: plan access for heirs, not just market exits.

- Document thoroughly: account IDs, contracts, entity records, and beneficiary forms.

- Diversify across time as well as asset classes: ladder maturities, stage purchases, and use recurring contributions to lower timing risk.

Actionable positioning: thinking like wealthy investors means you prepare for volatility and continuity. Keep clear information, update estate records, and design a strategy so your money survives both market stress and family transitions.

Conclusion

Keep these core rules in mind as you balance holdings across cash, property, stocks, and bonds. Recap: wealthy allocations often emphasize cash (about 25%–34%), real estate and property (roughly 12%–15%), stocks (around 17% in some surveys), and bonds (about 12%–15%). Alternatives stay small, near 3.3% of many portfolios. Quick checklist you can use now: confirm your liquid reserves, audit your property and account documents, review stocks and fund diversification, and match bond exposure to your risk profile. Make decisions through the same lens used here—income, stability, and growth potential—and update beneficiary and signing details so value passes cleanly. For historical ownership trends and context, see this historical ownership trends.

0 Comments Comments