Savings

The High‑Yield Savings Account Boom: Why HYSAs Are More Popular Than Ever

In the world of personal finance, the most important number on your savings account statement is often the one that isn't there. While most savers focus on the Annual Percentage Yield (APY) displayed in bold green letters on their bank's website, that number only tells half the story. To understand the true growth of your wealth, you must account for the silent predator of purchasing power: inflation.

As of April 2026, the financial landscape has shifted into what many economists are calling a "Goldilocks" period for savers. With the Federal Reserve maintaining a target interest rate range of 3.50% to 3.75% and the Consumer Price Index (CPI) cooling to a steady 2.4% for the 12 months ending February 2026, high-yield savings accounts (HYSAs) are finally delivering significant "Real APY". This guide will break down the top-performing accounts and show you how to calculate your true earnings in a fluctuating economy.

In 2026, the calculation of Real APY has become a daily necessity for serious savers. Bank rates shift constantly in response to "Fed Speak"—the public comments made by Federal Reserve officials—even when the official federal funds rate remains unchanged. At the same time, inflation data is released monthly, but its impact is felt every time you tap your credit card at the grocery store. To calculate your Real APY, we use the Fisher Equation:

Real APY = ((1 + Nominal APY) / (1 + Inflation Rate)) - 1

With the current US inflation rate sitting at 2.4% as of the latest February 2026 Bureau of Labor Statistics (BLS) report, any account yielding more than 2.4% is providing a positive real return [2]. Conversely, the national average savings account rate of approximately 0.46% is currently delivering a Real APY of -1.89%, meaning savers in traditional "big bank" accounts are actively losing purchasing power every single day.

Bread Financial and Vio Bank offer more consistent returns for larger balances. Bread Financial's 4.21% APY provides a 1.77% real return across the entire balance, making it a superior choice for emergency funds exceeding $10,000. Meanwhile, SoFi continues to be a favorite for its "all-in-one" approach, though its top 4.00% rate (1.56% Real APY) is strictly tied to direct deposit requirements.

This 2.4% figure is critical because it represents the "hurdle rate" for your money. If your savings are not growing by at least 2.4% per year, you are effectively becoming poorer in real terms. Economists distinguish between "Headline Inflation" (the 2.4% figure which includes food and energy) and "Core Inflation" (which excludes these volatile categories). In early 2026, both metrics have converged near the Fed's long-term target, creating a predictable environment for financial planning.

The next major update for savers is scheduled for April 10, 2026, when the Bureau of Labor Statistics will release the March CPI data [5]. If inflation continues to hold at 2.4% or dips further toward 2.0%, the Real APY of the accounts listed above will increase even if the banks do not raise their nominal rates.

When the Fed holds rates steady, online banks compete for deposits by offering APYs that track closely to the upper end of the Fed's range. This is why we see several banks offering 4.00% to 4.25% APY. However, if the Fed signals a "dovish" turn (indicating future rate cuts) in its upcoming meetings, banks will preemptively lower their HYSA rates. This makes "updated daily" tracking essential for savers who want to lock in high rates before they vanish.

However, the national average savings rate of 0.46% remains a trap for the uninformed. By settling for a traditional bank, you are essentially paying a "laziness tax" of nearly 2% of your purchasing power every year. As we move through April 2026, stay vigilant, calculate your Real APY, and don't be afraid to move your money to where it is treated best.

External References and Resources

As of April 2026, the financial landscape has shifted into what many economists are calling a "Goldilocks" period for savers. With the Federal Reserve maintaining a target interest rate range of 3.50% to 3.75% and the Consumer Price Index (CPI) cooling to a steady 2.4% for the 12 months ending February 2026, high-yield savings accounts (HYSAs) are finally delivering significant "Real APY". This guide will break down the top-performing accounts and show you how to calculate your true earnings in a fluctuating economy.

Table of Contents

- The "Real APY" Concept: A Savers' New Reality

- Top HYSAs with Real APY Calculations (April 2026)

- Inflation Analysis: Where the US Economy Stands in 2026

- How to Maximize Your Real Returns

- The Fed's Influence on Your Savings in 2026

- Conclusion

- Frequently Asked Questions (FAQ)

- External References and Resources

The "Real APY" Concept: A Savers' New Reality

The term "Real APY" refers to the interest earned on your savings after adjusting for the rate of inflation. While nominal APY represents the raw percentage increase in your bank balance, Real APY represents the actual increase in your purchasing power. If your bank pays you 5% interest but the cost of goods increases by 5% during that same period, your "Real" return is zero. You have more dollars, but those dollars buy the exact same amount of milk, gas, and rent as they did a year ago.In 2026, the calculation of Real APY has become a daily necessity for serious savers. Bank rates shift constantly in response to "Fed Speak"—the public comments made by Federal Reserve officials—even when the official federal funds rate remains unchanged. At the same time, inflation data is released monthly, but its impact is felt every time you tap your credit card at the grocery store. To calculate your Real APY, we use the Fisher Equation:

Real APY = ((1 + Nominal APY) / (1 + Inflation Rate)) - 1

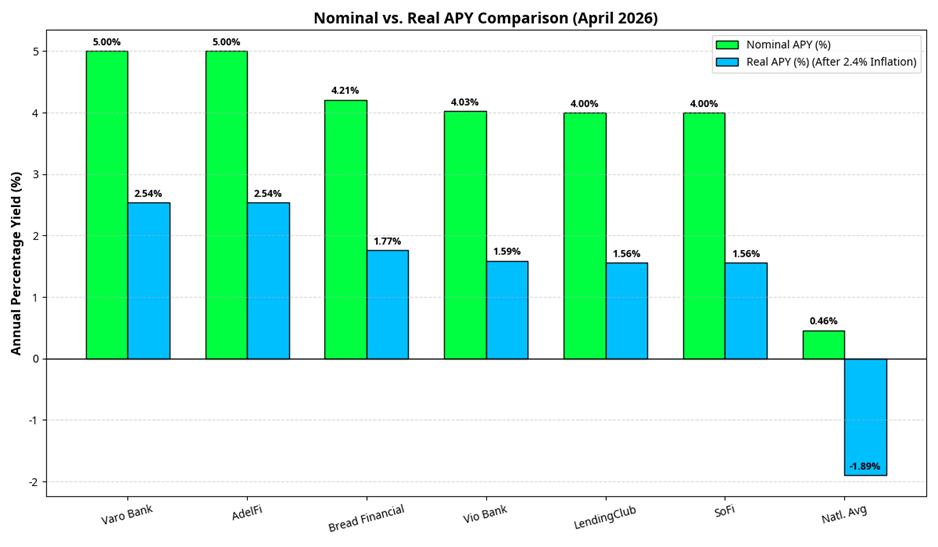

With the current US inflation rate sitting at 2.4% as of the latest February 2026 Bureau of Labor Statistics (BLS) report, any account yielding more than 2.4% is providing a positive real return [2]. Conversely, the national average savings account rate of approximately 0.46% is currently delivering a Real APY of -1.89%, meaning savers in traditional "big bank" accounts are actively losing purchasing power every single day.

Top HYSAs with Real APY Calculations (April 2026)

The following table compares the top-performing high-yield savings accounts available in April 2026. These rates are current as of the latest market data and are calculated against the current 2.4% inflation rate to reveal the true "Real APY" for each provider.| Financial Institution | Nominal APY | Real APY (After 2.4% Inflation) | Key Features |

| Varo Bank | 5.00% | 2.54% | 5% on first $5k; 2.5% thereafter |

| AdelFi | 5.00% | 2.54% | Competitive online-only rates |

| Bread Financial | 4.21% | 1.77% | No monthly fees; $100 min deposit |

| Vio Bank | 4.03% | 1.59% | Part of MidFirst Bank; $100 min |

| LendingClub | 4.00% | 1.56% | No minimum deposit; FDIC insured |

| SoFi | 4.00% | 1.56% | Requires direct deposit; combined accounts |

| National Average | 0.46% | -1.89% | Losing Purchasing Power |

Analysis of Top Performers

Varo Bank and AdelFi lead the market with a nominal 5.00% APY, which translates to a robust 2.54% real return. However, savers should be aware of the "tiered" nature of these accounts. Varo, for instance, typically limits the 5% rate to the first $5,000 of the balance, with any excess earning a significantly lower rate (currently around 2.50%). For a saver with $20,000, the "blended" nominal APY would be approximately 3.12%, resulting in a Real APY of just 0.70%.Bread Financial and Vio Bank offer more consistent returns for larger balances. Bread Financial's 4.21% APY provides a 1.77% real return across the entire balance, making it a superior choice for emergency funds exceeding $10,000. Meanwhile, SoFi continues to be a favorite for its "all-in-one" approach, though its top 4.00% rate (1.56% Real APY) is strictly tied to direct deposit requirements.

Inflation Analysis: Where the US Economy Stands in 2026

To understand why 2026 is such a unique year for savers, we must look at the trajectory of the Consumer Price Index (CPI). After the volatile inflationary spikes of the early 2020s, the US economy has entered a period of relative stability. The "all items" index rose 2.4% for the 12 months ending February 2026, holding steady from the January report [2].This 2.4% figure is critical because it represents the "hurdle rate" for your money. If your savings are not growing by at least 2.4% per year, you are effectively becoming poorer in real terms. Economists distinguish between "Headline Inflation" (the 2.4% figure which includes food and energy) and "Core Inflation" (which excludes these volatile categories). In early 2026, both metrics have converged near the Fed's long-term target, creating a predictable environment for financial planning.

The next major update for savers is scheduled for April 10, 2026, when the Bureau of Labor Statistics will release the March CPI data [5]. If inflation continues to hold at 2.4% or dips further toward 2.0%, the Real APY of the accounts listed above will increase even if the banks do not raise their nominal rates.

How to Maximize Your Real Returns

Finding a high nominal rate is only the first step. To ensure you are capturing the full Real APY, you must navigate the fine print that often accompanies these high-yield offers.1. Navigating Tiered Interest Rates

As seen with Varo Bank, many "headline" rates of 5.00% or higher are capped at low balance amounts. To maximize your real return on a large sum of money, consider a "laddered" approach: keep the first $5,000 in a top-tier capped account and move the remainder to a provider like Bread Financial or LendingClub that offers a high rate on the entire balance.2. Avoiding "Real APY Killers": Fees and Requirements

A $25 monthly maintenance fee on a $10,000 account is equivalent to a 3.00% annual interest charge. If you are earning a 4.00% nominal APY but paying that fee, your "effective" nominal APY drops to 1.00%, which—after 2.4% inflation—leaves you with a Real APY of -1.37%. Always prioritize accounts with no monthly fees and no minimum balance requirements.3. The Tax Implication: The "Real" Real APY

It is a common mistake to forget that the IRS taxes your nominal interest, not your real interest. If you earn $400 in interest on a $10,000 balance (4.00% APY) and are in the 22% tax bracket, you will pay $88 in taxes. This leaves you with $312 in net interest, or a 3.12% post-tax nominal APY. After 2.4% inflation, your Post-Tax Real APY is only 0.70%. To fight this, consider holding a portion of your emergency fund in a Roth IRA (if eligible) or using tax-advantaged accounts for long-term savings.The Fed's Influence on Your Savings in 2026

The Federal Reserve remains the primary driver of HYSA rates. In its March 2026 meeting, the Fed held the federal funds rate steady in the 3.50% to 3.75% range [6]. This "higher for longer" stance is a direct reaction to the stabilized but persistent 2.4% inflation rate.When the Fed holds rates steady, online banks compete for deposits by offering APYs that track closely to the upper end of the Fed's range. This is why we see several banks offering 4.00% to 4.25% APY. However, if the Fed signals a "dovish" turn (indicating future rate cuts) in its upcoming meetings, banks will preemptively lower their HYSA rates. This makes "updated daily" tracking essential for savers who want to lock in high rates before they vanish.

Strategic Asset Allocation: The Role of HYSA in a 2026 Portfolio

To fully appreciate the scope of this guide, we must explore how a High-Yield Savings Account fits into a broader financial strategy in the current economic climate. While the 2.54% Real APY offered by top-tier banks is attractive, it should not be the only tool in your wealth-building arsenal. Instead, think of your HYSA as the "foundation" of your financial house—the stable base upon which all other investments are built.1. The Emergency Fund: Your First Line of Defense

In 2026, the standard advice of keeping 3 to 6 months of expenses in an emergency fund remains the gold standard. However, the location of that fund is more important than ever. By utilizing a 5.00% APY account, you are ensuring that your emergency fund isn't just sitting idle; it is actively fighting the 2.4% inflation rate and growing your purchasing power. This means that if you have $30,000 in an emergency fund, you are earning roughly $750 in "real" value every year.2. Opportunity Cost: HYSA vs. The Stock Market

The 2026 stock market has seen significant growth, but it also comes with increased volatility. For many conservative investors, a 4.00% or 5.00% guaranteed return is a powerful alternative to the risk of a market downturn. This is known as the "Equity Risk Premium"—the extra return you expect to get for taking on the risk of the stock market. When HYSAs offer 5.00% and the long-term stock market average is around 8-10%, the "premium" for taking on stock market risk is only 3-5%. For many near-retirees or those with short-term goals (like buying a house in 2027), the guaranteed real return of an HYSA is often the more rational choice.3. Psychology of Saving: The "Peace of Mind" Dividend

Beyond the math, there is a psychological benefit to seeing your savings balance increase every single month. Unlike a brokerage account, which can fluctuate wildly based on global news, an HYSA provides a steady, predictable climb. In an era of rapid technological change and AI-driven market shifts, this predictability is a valuable form of "financial self-care."Technical Deep Dive: The Mechanics of Online Banking in 2026

How do online banks like Varo, Bread Financial, and SoFi manage to offer rates that are 10 times higher than the national average? The answer lies in their business model and the modern plumbing of the US banking system.1. The Low-Overhead Advantage

Traditional "brick-and-mortar" banks like Chase, Bank of America, and Wells Fargo have massive overhead costs. They must pay for thousands of physical branches, tellers, security guards, and local advertising. Online-only banks, on the other hand, operate out of a few central offices. They pass these massive savings on to you in the form of higher APYs. In 2026, the technology behind these apps has matured to the point where mobile check deposit and instant P2P transfers are as reliable as visiting a physical branch.2. The Battle for Liquidity

Banks don't just "hold" your money; they use it to fund loans to other customers (like mortgages and car loans). To make these loans, they need a steady supply of cash, known as liquidity. Smaller or newer banks use high APYs as a marketing tool to attract this liquidity quickly. This is why you often see the highest rates from banks you may not have heard of five years ago. They are essentially "buying" your deposits to fuel their growth.3. Neobanks vs. Traditional Online Banks

It is important to distinguish between "Neobanks" (like Varo) and "Traditional Online Banks" (like Ally or Marcus). Neobanks are often technology companies that partner with a traditional bank to provide FDIC insurance. In 2026, Varo has become one of the few neobanks to obtain its own national bank charter, giving it more control over its rates and products. Always check the fine print to see which bank is actually holding your funds and providing the insurance.Case Study: The Cost of Inaction

To illustrate the importance of moving to a high-yield account, let's look at a hypothetical scenario for a saver named Sarah. Sarah has $50,000 in a traditional savings account at a major national bank earning the average rate of 0.46%.- Scenario A (Traditional Bank): Sarah's $50,000 earns $230 in interest over one year. However, with 2.4% inflation, the goods that cost $50,000 today will cost $51,200 next year. Sarah is "short" by $970. She has lost nearly $1,000 in purchasing power simply by doing nothing.

- Scenario B (Top HYSA): Sarah moves her $50,000 to an account earning 4.21% (like Bread Financial). She earns $2,105 in interest. After the same 2.4% inflation ($1,200 cost increase), she still has a "real" gain of $905.

Conclusion

The 2025-2026 financial cycle has been a transformative one for American savers. For the first time in years, the gap between bank interest rates and inflation is wide enough to provide a genuine increase in wealth for those who choose the right accounts. With top HYSAs offering up to 5.00% nominal APY against a 2.4% inflation rate, the opportunity to earn a 2.54% Real APY is too significant to ignore.However, the national average savings rate of 0.46% remains a trap for the uninformed. By settling for a traditional bank, you are essentially paying a "laziness tax" of nearly 2% of your purchasing power every year. As we move through April 2026, stay vigilant, calculate your Real APY, and don't be afraid to move your money to where it is treated best.

Frequently Asked Questions (FAQ)

1. What is the difference between APY and interest rate?

Interest rate is the raw percentage of interest your bank pays you. APY (Annual Percentage Yield) includes the effect of compounding—interest earned on your interest. Because HYSAs compound daily or monthly, the APY is always slightly higher than the nominal interest rate.2. How often do HYSA rates change?

Unlike Certificates of Deposit (CDs), HYSA rates are variable. They can change at any time without notice. Banks typically adjust their rates within days of a Federal Reserve announcement or a significant shift in the 10-year Treasury yield.3. Is my money safe in these online-only banks?

Yes, provided the institution is FDIC-insured (for banks) or NCUA-insured (for credit unions). This insurance protects up to $250,000 per depositor, per institution. Always verify insurance status on the FDIC's "BankFind" tool before depositing.4. Does inflation affect my savings if I don't spend the money?

Yes. Inflation reduces the purchasing power of every dollar you own. Even if the money stays in the bank, it will buy fewer goods and services in the future than it does today. This is why "Real APY" is the only metric that truly matters for long-term wealth preservation.External References and Resources

- Bankrate: Best High-Yield Savings Accounts of April 2026

- Bureau of Labor Statistics: Consumer Price Index Summary - February 2026

- NerdWallet: Best High-Yield Online Savings Accounts for April 2026

- Forbes Advisor: 10 Best High-Yield Savings Accounts Of April 2026

- Bureau of Labor Statistics: CPI Release Schedule

- Federal Reserve: Recent Monetary Policy Decisions

0 Comments Comments