Spending

12 Ways to Quit Emotionless Shopping for Good

Table of Contents

- The Scale of Emotionless Shopping: Key Statistics

- The Psychology Behind Emotionless Shopping

- 12 Ways to Quit Emotionless Shopping: Quick Reference

- The 12 Ways in Depth

- Way 1: Name Your Emotion Before You Buy

- Way 2: Use the 48-Hour Rule

- Way 3: Track Every Purchase for 30 Days

- Way 4: Delete Shopping Apps and Browser Shortcuts

- Way 5: Set a Monthly Discretionary Budget

- Way 6: Unsubscribe From All Retail Emails and Push Notifications

- Way 7: Shop With a Written List Only

- Way 8: Calculate the True Cost in Work Hours

- Way 9: Identify Your Emotional Triggers

- Way 10: Create a Values-Based Spending Filter

- Way 11: Find Non-Shopping Emotional Outlets

- Way 12: Automate Your Savings Before You Can Spend

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

You did not plan to buy it. You were not looking for it. You may not even remember adding it to the cart. Yet there it sits in your online order history — one more purchase made on autopilot, triggered by a flash sale notification, a moment of boredom, a particularly bad afternoon at work, or the irresistible gravitational pull of a beautifully designed product page at 11pm. Welcome to emotionless shopping: the habit of buying things not because you need or genuinely want them, but because the emotional moment made the purchase feel like the right response.

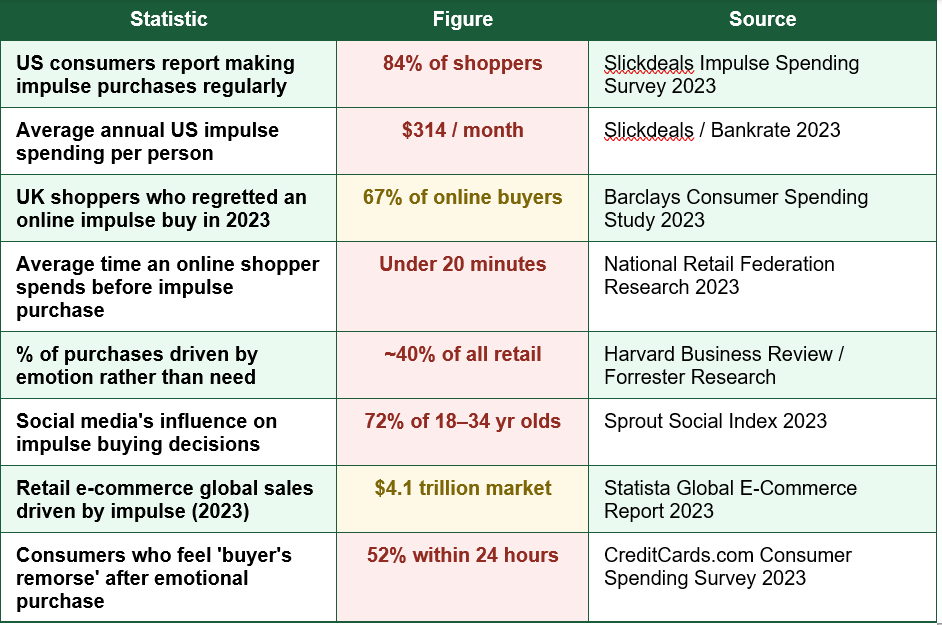

Emotionless shopping — also called impulse buying, emotional spending, or mindless consumption — is one of the most widespread and financially damaging habits in modern consumer life. According to a 2023 Slickdeals survey, 84% of American shoppers report making impulse purchases regularly, spending an average of $314 per month on unplanned items. Over a year, that is $3,768 — money that could have funded a meaningful emergency fund, a holiday, or a significant contribution to a retirement account.

The good news is that emotionless shopping is not a character flaw or an immutable personality trait. It is a behaviour — and like all behaviours, it responds to awareness, strategy, and deliberate habit change. This guide presents 12 evidence-backed, practical strategies for breaking the emotional spending cycle, reclaiming conscious control over your purchasing decisions, and redirecting your money toward what genuinely matters to you.

The Scale of Emotionless Shopping: Key Statistics

Understanding how widespread and financially significant emotional spending has become provides crucial context for why tackling it matters so much. The data reveals a consumer landscape in which impulsive, emotion-driven buying has become the norm rather than the exception:

These statistics illuminate a striking paradox: people consistently experience regret after emotional purchases, yet the behaviour persists — often becoming entrenched over years or decades. This is because the driver of emotionless shopping is not rational assessment of need or value, but the neurochemical reward cycle of the brain's dopamine system. Understanding this mechanism is the first step toward breaking free from it.

The Psychology Behind Emotionless Shopping

Retailers, platform designers, and advertisers have invested decades and billions of dollars into understanding and exploiting the neurological triggers that drive impulsive buying. The result is a consumer environment that is deliberately engineered to bypass rational decision-making and activate the emotional, reward-seeking part of the brain.Dopamine, the neurotransmitter associated with reward and pleasure, plays a central role. Research from the California Institute of Technology found that the anticipation of a purchase — not the purchase itself — produces the strongest dopamine response. This explains why browsing, adding items to a cart, and clicking buy creates a temporary emotional lift that has nothing to do with the utility of the item purchased. The platform is the product, and the purchase is simply the symptom.

Three specific emotional states are consistently identified in consumer psychology research as the primary drivers of impulse buying: stress and anxiety (retail therapy as a coping mechanism), boredom (purchasing as stimulation), and social comparison (buying to match or surpass a perceived peer standard, amplified dramatically by social media). Each of these states creates a genuine emotional need — but purchasing is a temporary and financially costly way to meet it.

Key insight: Emotionless shopping is almost never about the product. It is about the emotion that preceded the purchase and the brief neurochemical relief that the act of buying provides. Sustainable change requires addressing the emotion, not just the transaction.

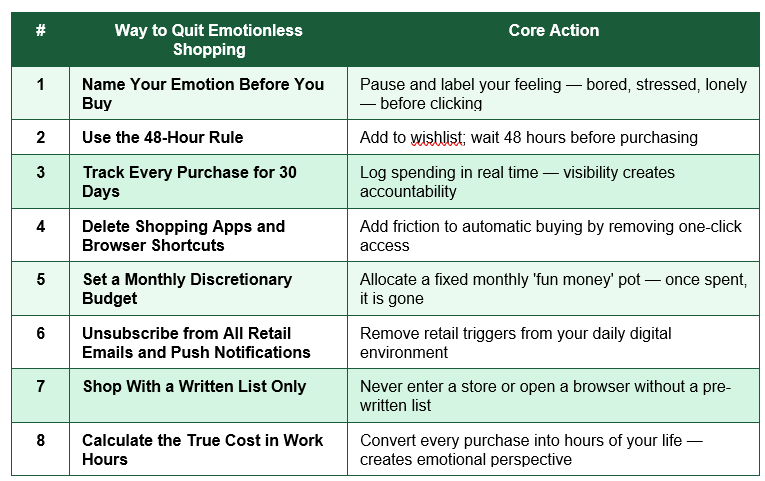

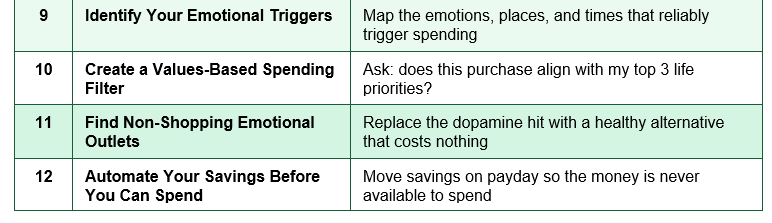

12 Ways to Quit Emotionless Shopping: Quick Reference

The table below provides a quick-reference overview of all 12 strategies before each is explored in depth:

The 12 Ways in Depth

Way 1: Name Your Emotion Before You Buy

The single most powerful intervention in breaking the emotional shopping cycle is deceptively simple: before making any unplanned purchase, stop and name the emotion you are currently feeling. Are you bored? Stressed? Lonely? Anxious? Celebratory? Naming the emotion engages the prefrontal cortex — the rational decision-making part of the brain — and creates a brief circuit-break in the automatic buying response. Research published in the journal Psychological Science found that labelling an emotion reduces its neurological intensity, giving you a window of rational choice that automatic behaviour bypasses.Way 2: Use the 48-Hour Rule

For any unplanned purchase above a personal threshold (e.g., $30 or £25), add the item to a wishlist or screenshot it and wait exactly 48 hours before deciding whether to buy. The anticipatory dopamine of the moment will have dissipated. In most cases, you will find either that you have forgotten about the item entirely, or that reviewing it with fresh eyes reveals it was less compelling than it appeared. Studies consistently show that the desire to purchase items added to a wishlist decreases significantly within 24-72 hours in the absence of active marketing triggers.Way 3: Track Every Purchase for 30 Days

Spend one full month logging every single purchase — no matter how small — in real time, either in a notebook, a notes app, or a dedicated budgeting tool. The act of writing it down immediately forces conscious awareness onto a behaviour that usually operates on autopilot. Many people who complete this exercise are genuinely shocked by the frequency and category of their unplanned purchases. Visibility alone has a measurable impact on spending behaviour — the Hawthorne effect in consumer psychology demonstrates that observed behaviour changes simply because it is being observed.Way 4: Delete Shopping Apps and Browser Shortcuts

Friction is the enemy of impulsive behaviour. One of the most effective structural interventions is to delete retail apps from your smartphone — Amazon, ASOS, eBay, Shein — and remove saved login credentials and one-click ordering from all retail websites. Adding even a small amount of friction to the purchase process — having to search for the site, log in manually, re-enter payment details — interrupts the automatic buying loop and creates moments for rational reconsideration. Research on behavioural economics consistently shows that small friction interventions produce disproportionately large reductions in impulsive behaviour.One-click purchase effect: 29% higher impulse rate — consumers who have one-click or saved payment settings active are 29% more likely to make an impulsive purchase than those who must manually enter payment details (Adobe Commerce Research 2022)

Way 5: Set a Monthly Discretionary Budget

Budgeting for discretionary spending does not mean eliminating enjoyment — it means making it conscious and bounded. Allocate a specific monthly amount as your personal discretionary fund: money you can spend on literally anything without guilt, because it has been intentionally planned. When this fund is spent, shopping stops for the month. This approach reframes discretionary spending from a source of financial anxiety into a controlled, guilt-free zone — reducing the emotional charge around spending that paradoxically drives many people toward more impulsive buying.Way 6: Unsubscribe From All Retail Emails and Push Notifications

Retail emails and push notifications are precision-engineered triggers. Flash sales, countdown timers, 'last one in stock' alerts, personalised recommendations, and abandoned cart reminders are all specifically designed to create urgency, scarcity, and emotional activation that drives unplanned purchases. A one-time investment of 30-60 minutes using a service like Unroll.me (US) or manually unsubscribing from retail email lists will permanently remove hundreds of weekly emotional triggers from your daily environment. Push notifications from shopping apps should be disabled before deletion. This single structural change removes the majority of external impulse-buying triggers for most people.Way 7: Shop With a Written List Only

The rule is simple and absolute: never enter a physical shop or open a retail website without a pre-written shopping list. Everything not on the list is off-limits on that shopping trip. This approach converts shopping from an open-ended browse — during which the emotional decision-making brain is in full control — into a specific, goal-directed task. Research from the Journal of Marketing Research found that shoppers using a written list spend significantly less per trip and report higher satisfaction with their purchases than unplanned browsers, because the purchases align with genuine pre-existing needs.Way 8: Calculate the True Cost in Work Hours

One of the most powerful reframing tools in mindful spending is converting the price of a purchase into the number of hours you must work to pay for it. If your take-home hourly rate is $20, a $120 impulse purchase costs you 6 hours of your working life — a morning's work. A $400 clothing haul costs a full two-day week. This reframe transforms abstract monetary figures into visceral time investments, reconnecting the purchase decision to the labour that earned the money. Many people find that purchases that seemed irresistible at face value become far less appealing when expressed in hours of life exchanged.Way 9: Identify Your Emotional Triggers

Keep a simple trigger journal for 30 days. Every time you feel an impulse to make an unplanned purchase, note the time, your location, what you were doing, and how you were feeling. After a month, review the patterns. Most people discover that their impulse buying concentrates around a small number of specific triggers: late evenings, after stressful work interactions, during social media scrolling, when commuting, or when feeling physically tired. Identifying your personal trigger profile allows you to create targeted interventions for exactly those moments — rather than attempting to maintain willpower across all situations simultaneously.Way 10: Create a Values-Based Spending Filter

Identify your three most important life values or goals — financial independence, family experiences, health, travel, career development — and create a simple decision rule: before any unplanned purchase above your threshold, ask whether it actively serves one of those three priorities. If the honest answer is no, it does not pass the filter and does not get bought. This approach does not restrict spending; it aligns spending with the things that genuinely matter, and systematically removes purchases that feel compelling in the moment but contribute nothing to your actual life priorities.Way 11: Find Non-Shopping Emotional Outlets

Because emotionless shopping is driven by emotional needs — stress relief, stimulation, connection, reward — the sustainable alternative is not suppression of those needs but substitution with healthier outlets. The key is to pre-identify specific activities that address the same emotional need and cost little or nothing. A 20-minute walk addresses stress and boredom simultaneously. Calling a friend addresses loneliness and the desire for connection. A challenging puzzle or creative activity addresses the stimulation need that boredom creates. Pre-committing to a specific alternative for each emotional trigger — written down and visible — dramatically increases the likelihood of using it when the emotional moment arrives.Replacement, not restriction: Willpower is a finite resource that depletes under emotional stress — precisely the condition that triggers emotional shopping. Successful habit change replaces the behaviour with an alternative that meets the underlying need, rather than simply attempting to suppress the impulse through discipline alone.

Way 12: Automate Your Savings Before You Can Spend

The most structurally powerful change you can make to your spending behaviour costs no willpower at all: automate a transfer of your savings target from your current account to a separate savings or investment account on the day you are paid — before you have the opportunity to spend it. This removes the money from the available-to-spend pool permanently, making it unavailable for impulse purchases without a deliberate effort to retrieve it. The psychological principle at work is loss aversion: once the money is in the savings account, you are far less likely to move it than you would be to simply not spend money that sits in your current account.Conclusion

Emotionless shopping is not a shopping problem. It is an emotional problem that manifests as a shopping behaviour — and understanding that distinction is the foundation of lasting change. The purchases are symptoms of stress, boredom, loneliness, or comparison. The 12 strategies in this guide work by addressing the emotion before the transaction, removing the structural triggers that make impulsive buying easy, and replacing the behaviour with alternatives that meet the same emotional needs at no financial cost.Not every strategy will resonate equally for everyone. The most effective approach is to start with two or three that address your most frequently identified triggers, apply them consistently for 30 days, and observe the impact on your spending patterns before adding more. Sustainable behaviour change is cumulative and compound — each layer of strategy strengthens the next, until conscious, intentional purchasing becomes the natural default rather than the effortful exception.

The financial rewards of breaking the emotionless shopping habit are significant: at the average $314 per month in saved impulse spending, a person who redirects this amount into an index fund investment account for ten years at a 10% average return accumulates over $64,000 — from purchases they would never have missed. But the deepest reward is not financial. It is the experience of spending your money with intention, in alignment with your values, and without the guilt and anxiety that accompany impulsive purchases. That clarity — that alignment between your money and your life — is worth more than any impulse buy.

Frequently Asked Questions (FAQ)

What exactly is emotionless shopping?

Emotionless shopping (also called emotional spending or impulse buying) refers to purchases made in response to an emotional state rather than a genuine need or deliberate intention. The 'emotionless' descriptor captures the paradox: the buyer appears to be acting automatically, without conscious emotional awareness, even though the purchase is entirely driven by an unacknowledged feeling such as stress, boredom, anxiety, or the desire for reward. The key characteristic is that the decision is made reactively rather than proactively.How do I know if I am an emotional spender?

Common indicators include: buying things you do not remember adding to your cart; experiencing buyer's remorse shortly after most purchases; accumulating items in your home that are unused or duplicated; spending more when you are stressed, tired, or bored; feeling a brief mood lift when browsing or buying that is quickly replaced by guilt or anxiety; and consistently spending beyond your budget despite good intentions. If three or more of these patterns are familiar, emotional spending is likely a significant factor in your financial behaviour.Is the 48-hour rule realistic for all purchases?

The 48-hour rule is most valuable for discretionary and non-urgent purchases — clothing, home accessories, electronics, subscriptions, entertainment. It is not necessary for genuine consumable necessities (groceries, toiletries) or time-sensitive opportunities with genuine deadlines. The practical approach is to set a personal price threshold — for example, any unplanned purchase above $30 — and apply the 48-hour rule automatically to anything above that amount. Over time, this threshold can be calibrated based on your spending patterns and financial goals.What are the best free apps for tracking impulse spending?

Several free and low-cost tools are well-regarded for spending awareness: YNAB (You Need a Budget) uses a zero-based budgeting approach that makes discretionary spending visible in real time; Mint (US) provides automatic transaction categorisation and spending reports; Emma (UK) connects to bank accounts and highlights recurring and discretionary spending patterns. For those who prefer manual tracking, a simple notes app or paper notebook is equally effective — the act of manual logging often has a stronger behaviour-change effect than automatic categorisation because it requires conscious engagement with each purchase.How long does it take to break an emotional shopping habit?

Research on habit formation — including the widely cited work by Dr Phillippa Lally at University College London — suggests that new behavioural habits take an average of 66 days to become automatic, with significant individual variation from 18 to 254 days depending on the complexity of the behaviour and the consistency of practice. For emotional spending, which is tied to deep-seated emotional patterns, sustainable change typically requires 60-90 days of consistent application of the strategies described in this guide. The most important indicator is not the absence of all impulse purchases but the gradual shift in your default response to emotional triggers — from automatic buying to conscious pause.External References

The following authoritative sources informed this article and are recommended for further reading:1. Slickdeals — Impulse Spending Survey Report 2023

https://slickdeals.net/editorial/study-american-impulse-spending/

2. Bankrate — Impulse Buying Statistics and Survey 2023

https://www.bankrate.com/personal-finance/impulse-buying-statistics/

3. Barclays — Consumer Spending Research Report 2023 (UK)

https://home.barclays/news/research/

4. National Retail Federation — Consumer Behaviour Insights 2023

https://nrf.com/research/consumer-research

5. Harvard Business Review — The Emotional Side of Consumer Decisions

https://hbr.org/2015/11/the-science-of-sensory-marketing

6. Sprout Social — Social Media Index and Buying Behaviour 2023

https://sproutsocial.com/insights/data/social-media-index/

7. Psychology Today — Why We Buy: The Science of Impulse Purchasing

https://www.psychologytoday.com/us/blog/inside-the-consumer-mind

8. YNAB (You Need A Budget) — Free Budgeting and Spending Tracker

https://www.ynab.com/

0 Comments Comments