Budgeting

6-Months Money Tracking Plan to Regain Financial Freedom

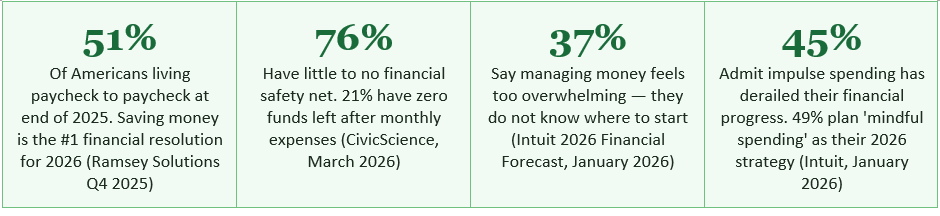

Fifty-one per cent of Americans were living paycheck to paycheck at the end of 2025, according to Ramsey Solutions' Q4 2025 State of Personal Finance. Seventy-six per cent have little to no financial safety net, according to CivicScience's March 2026 data. And thirty-seven per cent say managing money is so overwhelming they do not know where to begin, according to Intuit's January 2026 financial forecast. This guide is where they begin. A six-month money tracking plan, built around simple daily habits and weekly reviews, designed to take anyone from financial fog to genuine financial freedom.

Intuit's January 2026 financial forecast documents this clearly: 37% of Americans find managing money too overwhelming to know where to begin, and 45% admit impulse spending has derailed their financial progress. These are not people without income. They are people without a tracking system. Without tracking, every financial decision is made in the dark — against a mental model of your finances that research consistently shows is significantly less accurate than people believe.

The mechanism by which tracking produces financial improvement is straightforward. When you record every transaction, two things happen. First, you generate the data that makes reality visible — the actual spending patterns, the actual savings rate, the actual gap between where you are and where you want to be. Second, the act of recording creates a brief but genuine moment of conscious awareness before, during, or immediately after a spending decision. That awareness is the entry point for intentional behaviour change. Financial freedom-101.com's March 2026 guide on budget tracking confirms: 'families or small businesses who maintain detailed records and review them regularly make materially better financial decisions than those who manage from memory alone.'

Rather than sticking to a rigid, zero-tolerance budget, the majority of consumers are opting for consistent tracking that still leaves breathing room. 43% of people plan to adopt a balanced expense management mindset for 2026 — not perfection, but awareness.

— INTUIT — 2026 FINANCIAL FORECAST: STAYING MINDFUL AMID MONEY STRESS (JANUARY 2026)

The daily habit is the smallest possible unit of financial awareness — a five-minute record of what you spent today and whether it was planned or unplanned. This is not budgeting. It is not analysis. It is simply recording, consistently, so that you always know what happened to your money today. Done every day for six months, this habit alone transforms your relationship with money because it eliminates the financial fog — the state of not quite knowing where the money went — that keeps most people stuck.

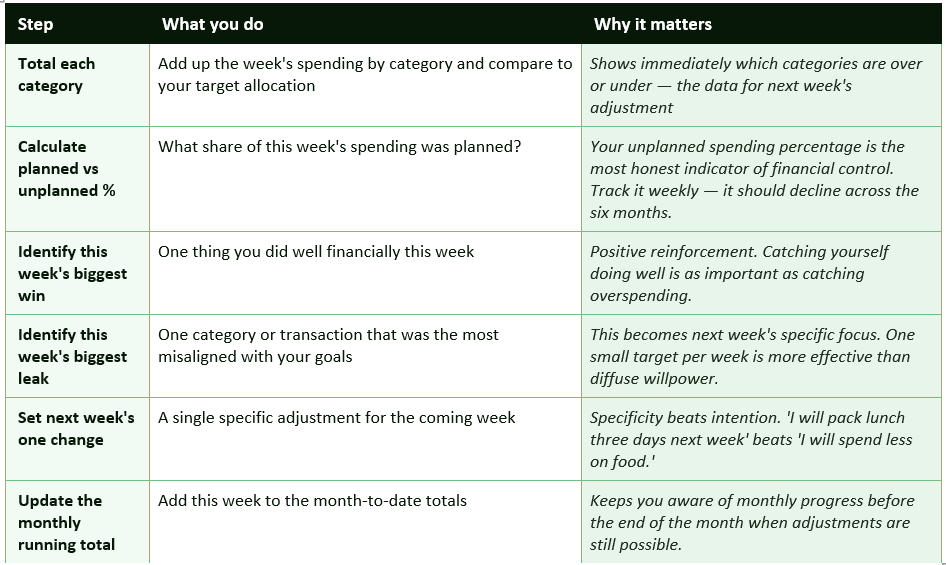

The weekly review is where the daily data becomes useful. Once a week, spend thirty minutes reviewing the week's spending against your allocations, identifying patterns, and making one specific adjustment for the following week. This is where decisions get made: which spending was genuinely aligned with your priorities, which was habitual or impulsive, and what one thing you will do differently next week. Over six months, fifty-two small weekly adjustments produce a financial life that looks radically different from the one you started with.

The monthly milestone review is the strategic layer — a sixty-minute review of where you stand against the month's specific goal, what the progress indicators show, and what the next month's focus should be. Each month in this plan has a specific theme and milestone, designed so that the six months build on each other in a sequence that takes you from financial fog to financial foundation.

Second, thirty days of actual transaction history. Pull your bank statements and card statements for the most recent full month before Day 1. This baseline gives you the starting data that Month 1's audit builds on — without it, you are building the plan on assumptions rather than facts.

Third, a specific definition of what financial freedom means for you. Not a philosophical statement — a specific, measurable one. 'Financial freedom means I have a three-month emergency fund, no credit card debt, and I am saving 15% of my income' is actionable. 'Financial freedom means I am not stressed about money' is not. Write your definition down. It will anchor the plan when motivation drops in Month 3.

Choose a consistent day and time for the weekly review — Sunday evening and Monday morning are the most common choices, both because they bracket the week naturally and because they align with paydays and bill due dates for most households. The financial-freedom-101.com March 2026 dashboard guide confirms: 'Some users prefer tactile or minimalist methods for daily tracking, reserving spreadsheets for periodic reconciliation. Daily Logging: a user records expenses in a notebook or a simple mobile app. Weekly Entry: Every Sunday, they transfer the data to a spreadsheet.' The weekly cadence is the standard that separates people who use their tracking data from those who generate data without acting on it.

The monthly review has five fixed components: total income and total outgoings for the month (net cash flow); comparison of actual spending to budget by category; progress toward the month's specific milestone (defined in the month-by-month sections below); one specific adjustment to the spending plan for next month; and an update of your financial dashboard — a simple running record of your net worth, emergency fund balance, and total debt that you update once a month.

The net worth tracking is particularly motivating over six months because it compounds progress in a way that monthly spending reviews alone do not. Even small improvements in net worth — a £200 increase in savings, a £300 reduction in credit card debt — are visible and meaningful on a net worth tracker. Ramsey Solutions' Q4 2025 data confirms that the people who make the most financial progress are those who track progress rather than just tracking spending: 79% of Americans in the survey reported optimism about their financial future specifically because they had a plan and were measuring against it.

The automation principle is well-established in personal finance: every financial decision that requires willpower in the moment is a decision that may not be made correctly when you are tired, stressed, or under financial pressure. Automating the decisions removes willpower from the equation. The three most important automations to set up in Month 3 are: automatic transfer to savings on payday (before the money can be spent), automatic minimum payment plus extra payment on all debts (so the paydown plan executes without active management), and automatic investment contribution if applicable.

Month 3 is also when the first balance transfer or debt consolidation actions should be explored if applicable. For anyone with credit card debt above £2,000 or $2,000 at high APR, a 0% balance transfer card (available for up to 21 months at 0%, as documented in previous guides in this series) eliminates all interest during the promotional period, allowing every payment to reduce the principal rather than being partially consumed by interest. The eligibility for a 0% balance transfer requires a credit score of 670 or above and is best applied for in Month 3 after two months of improved financial behaviour have been established.

By Month 4, your daily tracking habit is established, your subscriptions have been audited, your automations are running, and your emergency buffer is in place. The focus now shifts to the two parallel processes that build net worth: reducing liabilities (paying down debt) and increasing assets (growing savings and investments). These do not require new decisions — they require the consistent execution of the plan established in Month 3.

The weekly review in Month 4 adds one new tracking point: the weekly debt balance. Watching the credit card or loan balance fall week by week is one of the most powerful motivational tools in this plan. A £300 or $300 extra payment on a credit card at 22% APR reduces the balance by £300 immediately and eliminates approximately £66 in annual interest on that £300 — a visible, immediate, concrete result that most people find genuinely motivating. Track the debt balance every Sunday alongside your spending categories, and note the cumulative reduction since Month 1.

By Month 5, the foundational work is done — you know your numbers, you have a buffer, your spending is tracked and intentional, your debt is falling, and your savings are growing. The Month 5 focus is on two additional levers: income optimisation and first investment contributions.

Income optimisation in Month 5 means a deliberate review of three specific income opportunities: whether you are claiming all available tax reliefs and benefits (in the UK, this includes checking whether you are owed a pension tax relief claim through Self Assessment if you are a higher-rate taxpayer; in the US, reviewing your W-4 withholding to ensure you are not over-withholding); whether there is a realistic salary review or rate increase that is overdue; and whether one of the side income streams explored in previous guides (selling unused items, freelancing, one additional income source) is available and appropriate.

For investment contributions, the rule from our savings and investing guide applies: once the emergency fund is established at three months of expenses, any surplus above the emergency target belongs in appreciating assets rather than savings accounts. Month 5 is when the Stocks and Shares ISA (UK) or Roth IRA or 401(k) beyond the employer match (US) should receive its first deliberate monthly contribution from the surplus the previous four months have created.

In the final week of Month 6, spend ninety minutes on the most thorough financial review you have ever done. Compare your current net worth snapshot to the Month 1 baseline. Calculate the total change across six months in: emergency fund balance, total debt balance, monthly savings rate, unplanned spending percentage, and net worth. These numbers tell you the honest story of what six months of tracking has produced.

For most people who follow this plan consistently, the six-month results will include: a complete picture of their finances for the first time; an emergency buffer of at least one month of expenses; meaningfully reduced credit card debt; a regular savings and investment habit; and a monthly unplanned spending percentage significantly lower than at the start. Ramsey Solutions' Q4 2025 data shows that 79% of Americans are optimistic about their financial future when they have a plan they are measuring against. The six-month plan creates both the plan and the measurement.

Month 6 also produces the blueprint for the next six months — because financial freedom is not a state you arrive at and stop. It is a practice you maintain and deepen. Use the Month 6 review to set the next phase's goals: Is the emergency fund fully funded? Is the high-interest debt eliminated? Is the investment contribution at the level you want? What does the following six months build toward? The system you have spent six months building — daily tracking, weekly review, monthly milestone — is now a habit rather than an effort. The next six months will require less active work and produce better results.

The research on behaviour change is consistent: habits that survive Month 3 survive the full six months. The specific interventions that most effectively carry people through the Month 3 dip are: visible progress tracking (a physical or digital chart showing the emergency fund growing, or the debt falling, or the net worth improving — something you can see in thirty seconds that provides concrete evidence of progress); accountability (one person who knows your goal and asks about it once a month — not to judge, but to acknowledge progress); and lowering the bar when life gets hard (a missed tracking day is not a failed plan; return to the habit the next day, no penalty).

Intuit's January 2026 data on consumer financial psychology confirms that the 43% of consumers who plan to adopt a 'balanced expense management mindset' — consistent tracking with breathing room rather than zero-tolerance rigidity — are more likely to sustain their financial habits than those who set impossibly strict budgets. The six-month plan in this guide is designed to be balanced: it requires daily tracking and weekly review, but it does not require perfection. A bad week followed by a return to tracking is not a failure. It is exactly how habits are built.

By Month 6, the person who started this plan in Month 1 knows exactly where their money goes. They have a financial buffer. Their debt is lower. Their savings are automatic. Their net worth has moved in the right direction for six consecutive months. And they have something more valuable than any of those specific outcomes: a financial system that is now a habit rather than an effort — one that will continue working for them long after the six months are over. Financial freedom is not a destination. It is a practice. This plan is how the practice begins.

CivicScience — Living Paycheck to Paycheck in an Era of Financial Distress (March 2026) https://civicscience.com/living-paycheck-to-paycheck-in-an-era-of-financial-distress-and-survival-mode-mentality/

Ramsey Solutions — The State of Personal Finance in America Q4 2025 (February 2026) https://www.ramseysolutions.com/budgeting/state-of-personal-finance

Wealthvieu — Paycheck to Paycheck Statistics: How Many Americans Are Struggling? 2026 https://wealthvieu.com/personal-finance/income/paycheck-to-paycheck-statistics/

CNBC Select — 5 Best Free Budgeting Tools of 2026 (April 2026) https://www.cnbc.com/select/best-free-budgeting-tools/

Financial Freedom 101 — Budget Tracking in 2026: Why Modern Dashboards Outperform Spreadsheets (March 2026) https://financial-freedom-101.com/budget-tracking-in-2026-why-modern-dashboards-outperform-spreadsheets/

WalletHub — Personal Finance Statistics 2026 (April 2026) https://wallethub.com/edu/personal-finance-statistics/147459

TABLE OF CONTENTS

- Why Tracking Is the Gateway to Financial Freedom

- The Architecture of This Plan: Daily, Weekly, Monthly

- What You Need Before Day 1

- The Daily Money Tracking Habit: 5 Minutes a Day

- The Weekly Money Review: 30 Minutes That Changes Everything

- The Monthly Milestone Review: Your Financial Progress Report

- Month 1: Audit and Baseline — Know Your Numbers

- Month 2: Stabilise — Stop the Leaks and Build the Buffer

- Month 3: Systematise — Automate and Eliminate Drag

- Month 4: Build Momentum — Debt Attack and Savings Growth

- Month 5: Accelerate — Income, Investing, and Optimising

- Month 6: Freedom Foundation — Review, Sustain, Level Up

- The Best Free and Low-Cost Tools for Money Tracking in 2026

- The Psychology of Staying on Track: What Makes People Quit (and How Not To)

- Conclusion

- Frequently Asked Questions

- References

Why Tracking Is the Gateway to Financial Freedom

Financial freedom is not a destination that arrives when your income crosses a threshold. It is a state — the state in which your money is working according to a plan you have made rather than disappearing in ways you cannot account for. The vast majority of people who do not have financial freedom do not lack the income to achieve it. They lack visibility into where their money is going.Intuit's January 2026 financial forecast documents this clearly: 37% of Americans find managing money too overwhelming to know where to begin, and 45% admit impulse spending has derailed their financial progress. These are not people without income. They are people without a tracking system. Without tracking, every financial decision is made in the dark — against a mental model of your finances that research consistently shows is significantly less accurate than people believe.

The mechanism by which tracking produces financial improvement is straightforward. When you record every transaction, two things happen. First, you generate the data that makes reality visible — the actual spending patterns, the actual savings rate, the actual gap between where you are and where you want to be. Second, the act of recording creates a brief but genuine moment of conscious awareness before, during, or immediately after a spending decision. That awareness is the entry point for intentional behaviour change. Financial freedom-101.com's March 2026 guide on budget tracking confirms: 'families or small businesses who maintain detailed records and review them regularly make materially better financial decisions than those who manage from memory alone.'

Rather than sticking to a rigid, zero-tolerance budget, the majority of consumers are opting for consistent tracking that still leaves breathing room. 43% of people plan to adopt a balanced expense management mindset for 2026 — not perfection, but awareness.

— INTUIT — 2026 FINANCIAL FORECAST: STAYING MINDFUL AMID MONEY STRESS (JANUARY 2026)

The Architecture of This Plan: Daily, Weekly, Monthly

This plan operates at three time horizons simultaneously, and the interaction between them is what produces lasting change rather than temporary improvement.The daily habit is the smallest possible unit of financial awareness — a five-minute record of what you spent today and whether it was planned or unplanned. This is not budgeting. It is not analysis. It is simply recording, consistently, so that you always know what happened to your money today. Done every day for six months, this habit alone transforms your relationship with money because it eliminates the financial fog — the state of not quite knowing where the money went — that keeps most people stuck.

The weekly review is where the daily data becomes useful. Once a week, spend thirty minutes reviewing the week's spending against your allocations, identifying patterns, and making one specific adjustment for the following week. This is where decisions get made: which spending was genuinely aligned with your priorities, which was habitual or impulsive, and what one thing you will do differently next week. Over six months, fifty-two small weekly adjustments produce a financial life that looks radically different from the one you started with.

The monthly milestone review is the strategic layer — a sixty-minute review of where you stand against the month's specific goal, what the progress indicators show, and what the next month's focus should be. Each month in this plan has a specific theme and milestone, designed so that the six months build on each other in a sequence that takes you from financial fog to financial foundation.

What You Need Before Day 1

The plan requires three practical things and one mindset commitment before it starts.The three practical requirements

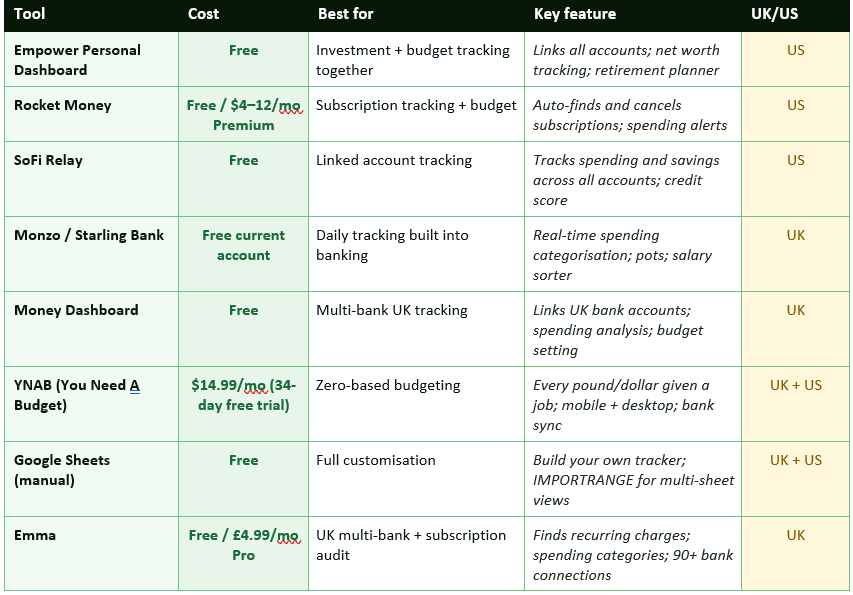

First, a tracking method that you will actually use. The best tracking system is the one you stick to — not the most sophisticated one. Options range from a simple notebook (the most tactile and most consistent for many people) to a spreadsheet (free and highly customisable) to an app (the most automated and most convenient). CNBC Select's April 2026 review of best free budgeting tools in 2026 identifies Empower Personal Dashboard, Rocket Money, and SoFi Relay as the strongest free options — each links to your bank and card accounts and categorises spending automatically. For those who prefer a paper-first approach, a simple daily expense log in a notebook works equally well. The method matters less than the consistency.Second, thirty days of actual transaction history. Pull your bank statements and card statements for the most recent full month before Day 1. This baseline gives you the starting data that Month 1's audit builds on — without it, you are building the plan on assumptions rather than facts.

Third, a specific definition of what financial freedom means for you. Not a philosophical statement — a specific, measurable one. 'Financial freedom means I have a three-month emergency fund, no credit card debt, and I am saving 15% of my income' is actionable. 'Financial freedom means I am not stressed about money' is not. Write your definition down. It will anchor the plan when motivation drops in Month 3.

The mindset commitment

Wealthvieu's 2026 paycheck-to-paycheck analysis captures the psychological barrier precisely: 'Escaping the paycheck-to-paycheck cycle is not about willpower or deprivation — it is about creating a small buffer that breaks the emergency-to-debt pattern. Once you have even $1,000 set aside, the psychology changes: you are no longer one expense away from crisis.' The mindset commitment this plan asks for is not perfection. It is consistency over six months. A bad week in Month 2 does not end the plan. A missed tracking day does not end the plan. The plan ends when you decide to stop — and the single most important commitment is to not decide that until Month 6 is complete.The Daily Money Tracking Habit: 5 Minutes a Day

The daily tracking habit is the non-negotiable foundation. Every other element of this plan depends on the data it generates. The habit itself has three components and takes five minutes.The daily 5-minute money tracking routine

- Step 1 — Record today's spending (2 minutes): Write down or log every transaction from today. Use your tracking method of choice — app, spreadsheet, or notebook. The format is simple: date, description, amount, category (Food, Transport, Housing, Entertainment, Health, Personal, Other). If you use an app that imports transactions automatically, review and correct any miscategorisations. The goal is a complete, accurate record of today's money movements.

- Step 2 — Tag each transaction: planned or unplanned (1 minute): Next to each transaction, mark whether it was planned (you expected to spend this money today) or unplanned (it was not in your mental plan for the day). This is the most revealing data point in the entire system — because the gap between what you planned to spend and what you actually spent is precisely the gap between your current financial reality and your financial goals.

- Step 3 — Note one observation (1 minute): Write one sentence about today's spending. It can be an observation (I spent £12 on coffee this week), a question (Why did I buy that?), a recognition (I stayed on plan today), or a decision (I will bring lunch tomorrow). This one-sentence practice creates the micro-habit of financial reflection that, over six months, becomes automatic financial mindfulness.

- Step 4 — Check the running weekly total (1 minute): Update your weekly running total for each category. This takes 60 seconds and keeps you aware of where you are in the week's budget before the week is over — so you can make adjustments on Thursday rather than noticing on Sunday that you overspent on Wednesday.

The Weekly Money Review: 30 Minutes That Changes Everything

The weekly review is where daily tracking data becomes financial intelligence. Without the weekly review, tracking is just record-keeping. With it, tracking becomes the engine of change.Choose a consistent day and time for the weekly review — Sunday evening and Monday morning are the most common choices, both because they bracket the week naturally and because they align with paydays and bill due dates for most households. The financial-freedom-101.com March 2026 dashboard guide confirms: 'Some users prefer tactile or minimalist methods for daily tracking, reserving spreadsheets for periodic reconciliation. Daily Logging: a user records expenses in a notebook or a simple mobile app. Weekly Entry: Every Sunday, they transfer the data to a spreadsheet.' The weekly cadence is the standard that separates people who use their tracking data from those who generate data without acting on it.

The Monthly Milestone Review: Your Financial Progress Report

At the end of each month, before the new month begins, spend sixty minutes on a structured financial progress review. This is not a punishment session for any overspending that occurred — it is a strategic review of where you are against where you planned to be, and what the following month's specific focus will be.The monthly review has five fixed components: total income and total outgoings for the month (net cash flow); comparison of actual spending to budget by category; progress toward the month's specific milestone (defined in the month-by-month sections below); one specific adjustment to the spending plan for next month; and an update of your financial dashboard — a simple running record of your net worth, emergency fund balance, and total debt that you update once a month.

The net worth tracking is particularly motivating over six months because it compounds progress in a way that monthly spending reviews alone do not. Even small improvements in net worth — a £200 increase in savings, a £300 reduction in credit card debt — are visible and meaningful on a net worth tracker. Ramsey Solutions' Q4 2025 data confirms that the people who make the most financial progress are those who track progress rather than just tracking spending: 79% of Americans in the survey reported optimism about their financial future specifically because they had a plan and were measuring against it.

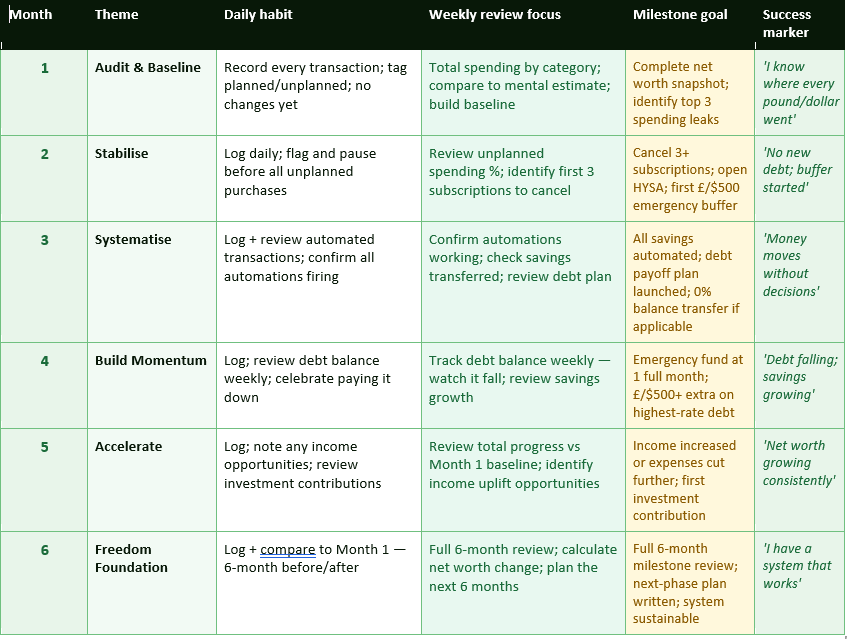

Month 1: Audit and Baseline — Know Your Numbers

Theme: No judgement. Only information. The goal of Month 1 is not to change anything. It is to discover reality.What Month 1 is for

Before you can build a plan, you need accurate data about your current financial position. Most people operate with a mental model of their finances that research consistently shows to be approximately 20% to 30% inaccurate — they underestimate recurring subscriptions, underestimate food and discretionary spending, and overestimate what they save. Month 1 replaces that mental model with facts.The Month 1 daily and weekly actions

Daily: Track every single transaction for thirty days without making any deliberate spending changes. The tracking itself will influence some spending (this is called the Hawthorne effect — being observed changes behaviour), but do not make active changes yet. The goal is a clean baseline. Weekly review: every Sunday, total the week's spending by category and note any patterns without judgement. By the end of four weeks, you will have a complete picture of your actual spending across all categories.The Month 1 milestone

Complete a full net worth snapshot: total all assets (bank accounts, savings, pension/retirement accounts, investments, property equity if applicable) and all liabilities (credit card balances, loans, mortgage outstanding, any other debt). The difference is your current net worth. This number may be negative. That is fine — it is your starting point, and it will move in the right direction across the six months.Month 2: Stabilise — Stop the Leaks and Build the Buffer

Theme: Stop the bleeding. Month 2 is about identifying and eliminating the spending that is not aligned with your values or goals, and creating the first financial buffer that breaks the paycheck-to-paycheck cycle.The subscription audit

One of the most consistent findings across personal finance research is that most households have more recurring subscriptions than they are aware of. Rocket Money's 2026 subscription tracking data confirms this — the app regularly finds forgotten recurring charges worth $100 to $300 per month for average households. In Month 2, use your Month 1 transaction data to list every recurring subscription and direct debit. For each one, ask: have I used this in the past 30 days? If the answer is no, cancel it. The annual saving from cancelling four unused £10/month subscriptions is £480 — a meaningful contribution to the emergency buffer.Building the first financial buffer

The most important financial milestone in Month 2 is opening a high-yield savings account and making the first deposit toward a £500 or $500 mini emergency fund. CivicScience's March 2026 data shows that 21% of Americans have zero funds remaining after monthly expenses — the mini emergency fund is the specific intervention that breaks this pattern. The money does not need to come from a big sacrifice. It can come from cancelled subscriptions, reduced unplanned spending identified in Month 1's audit, and any windfall. The target is £/$500 in the account by the end of Month 2.The unplanned spending discipline

Month 2 introduces one new daily practice: a deliberate pause before every unplanned purchase. Before completing any transaction that was not in your plan for the day, wait twenty-four hours. This is not a permanent restriction — it is a thirty-day experiment in interrupting the impulse-to-purchase pathway that Intuit's January 2026 data identifies as having derailed the financial progress of 45% of surveyed consumers. Many unplanned purchases that survive the twenty-four hour pause turn out to be genuine rather than impulse — those are fine. The ones that do not survive the pause would have been regretted.Month 3: Systematise — Automate and Eliminate Drag

Theme: Build the system so the money moves without decisions. Month 3 is about converting the deliberate practices of Months 1 and 2 into automatic systems that work even when motivation is low.The automation principle is well-established in personal finance: every financial decision that requires willpower in the moment is a decision that may not be made correctly when you are tired, stressed, or under financial pressure. Automating the decisions removes willpower from the equation. The three most important automations to set up in Month 3 are: automatic transfer to savings on payday (before the money can be spent), automatic minimum payment plus extra payment on all debts (so the paydown plan executes without active management), and automatic investment contribution if applicable.

Month 3 is also when the first balance transfer or debt consolidation actions should be explored if applicable. For anyone with credit card debt above £2,000 or $2,000 at high APR, a 0% balance transfer card (available for up to 21 months at 0%, as documented in previous guides in this series) eliminates all interest during the promotional period, allowing every payment to reduce the principal rather than being partially consumed by interest. The eligibility for a 0% balance transfer requires a credit score of 670 or above and is best applied for in Month 3 after two months of improved financial behaviour have been established.

Month 4: Build Momentum — Debt Attack and Savings Growth

Theme: Both debt falls and savings grow. Month 4 is where the work of the previous three months begins to produce compounding results that are visibly rewarding.By Month 4, your daily tracking habit is established, your subscriptions have been audited, your automations are running, and your emergency buffer is in place. The focus now shifts to the two parallel processes that build net worth: reducing liabilities (paying down debt) and increasing assets (growing savings and investments). These do not require new decisions — they require the consistent execution of the plan established in Month 3.

The weekly review in Month 4 adds one new tracking point: the weekly debt balance. Watching the credit card or loan balance fall week by week is one of the most powerful motivational tools in this plan. A £300 or $300 extra payment on a credit card at 22% APR reduces the balance by £300 immediately and eliminates approximately £66 in annual interest on that £300 — a visible, immediate, concrete result that most people find genuinely motivating. Track the debt balance every Sunday alongside your spending categories, and note the cumulative reduction since Month 1.

Month 5: Accelerate — Income, Investing, and Optimising

Theme: Stop managing the deficit and start building the surplus. Month 5 is where the plan shifts from defensive (stopping the leaks) to offensive (building wealth).By Month 5, the foundational work is done — you know your numbers, you have a buffer, your spending is tracked and intentional, your debt is falling, and your savings are growing. The Month 5 focus is on two additional levers: income optimisation and first investment contributions.

Income optimisation in Month 5 means a deliberate review of three specific income opportunities: whether you are claiming all available tax reliefs and benefits (in the UK, this includes checking whether you are owed a pension tax relief claim through Self Assessment if you are a higher-rate taxpayer; in the US, reviewing your W-4 withholding to ensure you are not over-withholding); whether there is a realistic salary review or rate increase that is overdue; and whether one of the side income streams explored in previous guides (selling unused items, freelancing, one additional income source) is available and appropriate.

For investment contributions, the rule from our savings and investing guide applies: once the emergency fund is established at three months of expenses, any surplus above the emergency target belongs in appreciating assets rather than savings accounts. Month 5 is when the Stocks and Shares ISA (UK) or Roth IRA or 401(k) beyond the employer match (US) should receive its first deliberate monthly contribution from the surplus the previous four months have created.

Month 6: Freedom Foundation — Review, Sustain, and Level Up

Theme: Measure everything. Build what comes next. Month 6 is the evaluation and the beginning, not the end.In the final week of Month 6, spend ninety minutes on the most thorough financial review you have ever done. Compare your current net worth snapshot to the Month 1 baseline. Calculate the total change across six months in: emergency fund balance, total debt balance, monthly savings rate, unplanned spending percentage, and net worth. These numbers tell you the honest story of what six months of tracking has produced.

For most people who follow this plan consistently, the six-month results will include: a complete picture of their finances for the first time; an emergency buffer of at least one month of expenses; meaningfully reduced credit card debt; a regular savings and investment habit; and a monthly unplanned spending percentage significantly lower than at the start. Ramsey Solutions' Q4 2025 data shows that 79% of Americans are optimistic about their financial future when they have a plan they are measuring against. The six-month plan creates both the plan and the measurement.

Month 6 also produces the blueprint for the next six months — because financial freedom is not a state you arrive at and stop. It is a practice you maintain and deepen. Use the Month 6 review to set the next phase's goals: Is the emergency fund fully funded? Is the high-interest debt eliminated? Is the investment contribution at the level you want? What does the following six months build toward? The system you have spent six months building — daily tracking, weekly review, monthly milestone — is now a habit rather than an effort. The next six months will require less active work and produce better results.

The Best Free and Low-Cost Tools for Money Tracking in 2026

The Psychology of Staying on Track: What Makes People Quit (and How Not To)

The most common failure point for any six-month financial plan is not Month 1, when motivation is high, or Month 6, when the end is in sight. It is Month 3 — the midpoint at which the novelty has worn off, the results are not yet fully visible, the sacrifices of the early weeks have created a form of decision fatigue, and a difficult week or unexpected expense can feel like evidence that the whole plan is not working.The research on behaviour change is consistent: habits that survive Month 3 survive the full six months. The specific interventions that most effectively carry people through the Month 3 dip are: visible progress tracking (a physical or digital chart showing the emergency fund growing, or the debt falling, or the net worth improving — something you can see in thirty seconds that provides concrete evidence of progress); accountability (one person who knows your goal and asks about it once a month — not to judge, but to acknowledge progress); and lowering the bar when life gets hard (a missed tracking day is not a failed plan; return to the habit the next day, no penalty).

Intuit's January 2026 data on consumer financial psychology confirms that the 43% of consumers who plan to adopt a 'balanced expense management mindset' — consistent tracking with breathing room rather than zero-tolerance rigidity — are more likely to sustain their financial habits than those who set impossibly strict budgets. The six-month plan in this guide is designed to be balanced: it requires daily tracking and weekly review, but it does not require perfection. A bad week followed by a return to tracking is not a failure. It is exactly how habits are built.

CONCLUSION

Fifty-one per cent of Americans ended 2025 living paycheck to paycheck. Seventy-six per cent have little to no financial safety net. Thirty-seven per cent say managing money is too overwhelming to begin. These are the people this plan was built for. Not people who lack income. People who lack a system — a simple, daily structure that makes the invisible visible and turns awareness into action. The six-month plan in this guide is that system: five minutes a day, thirty minutes a week, sixty minutes a month, across six months that each have a specific theme, a specific milestone, and a specific success marker.By Month 6, the person who started this plan in Month 1 knows exactly where their money goes. They have a financial buffer. Their debt is lower. Their savings are automatic. Their net worth has moved in the right direction for six consecutive months. And they have something more valuable than any of those specific outcomes: a financial system that is now a habit rather than an effort — one that will continue working for them long after the six months are over. Financial freedom is not a destination. It is a practice. This plan is how the practice begins.

Frequently Asked Questions

How long does daily money tracking take and what is the minimum I need to do?

The daily tracking routine in this plan takes five minutes — recording the day's transactions, tagging them as planned or unplanned, writing one observation, and checking the weekly running total. This is the minimum viable version of the habit. If five minutes feels too much on a difficult day, the absolute minimum is simply recording the total amount spent today in any format — a note on your phone, a single line in a notebook. The goal is an unbroken streak of recording rather than a perfect record. Missing one day is acceptable; the plan's effectiveness depends on near-daily consistency, not on perfection. Research on habit formation consistently shows that keeping the daily habit alive — even at reduced intensity during difficult weeks — produces better outcomes than maintaining strict standards that lead to abandonment when they are inevitably missed.What is the best free money tracking app in 2026?

CNBC Select's April 2026 review identifies three standout free tools: Empower Personal Dashboard (best for tracking both spending and investments/net worth together, with links to all financial accounts and a retirement planning tool), Rocket Money (best for subscription tracking — it finds recurring charges you have forgotten about and can cancel them on your behalf), and SoFi Relay (best for linked account tracking with credit score monitoring). For UK users, Monzo and Starling Bank provide the most seamless daily tracking experience as free current accounts with built-in real-time spending categorisation, budget pots, and salary sorting. Emma is the strongest UK-specific multi-bank tracking app, connecting to over 90 banks and identifying subscriptions. For maximum customisation without cost, a Google Sheets spreadsheet with IMPORTRANGE functionality allows you to build exactly the tracker the plan requires with no subscription cost.What is the most important month in the 6-month plan?

Month 1 is the most structurally important — without an accurate baseline from the audit phase, the rest of the plan is built on assumptions rather than facts. But Month 3 is the most psychologically important, because it is the most common failure point. The novelty of Month 1 has faded, the dramatic gains of Month 2 (cancelled subscriptions, first emergency buffer deposit) are not repeating at the same scale, and motivation is at its cyclical low. The plan anticipates this and provides Month 3's theme specifically to counter it: systematising and automating so that the plan runs on its own systems rather than on active willpower. The specific action that most reliably carries people through Month 3 is setting up the automatic savings transfer — once the money moves automatically, the plan continues even when motivation drops.How do I track money if my income is irregular?

Irregular income is common among the self-employed, gig workers, freelancers, and anyone with commission-based or seasonal pay. The tracking plan works for irregular income with one adaptation: rather than setting weekly or monthly spending targets based on expected income, set them based on your lowest recent monthly income. This creates a conservative floor — a plan that is achievable even in slow months. Any income above the floor in higher-earning months goes immediately to the emergency fund or debt payoff rather than being absorbed by spending. The daily tracking habit and weekly review are equally important for irregular income earners — arguably more so, because the discipline of tracking prevents the very common pattern where high-earning months are spent rather than buffered, leaving the next slow month without reserves.Can I start the plan at any time of year or month?

The plan can start on any day — not just the first of a month or the first of January. The six months are defined by the day you begin, not by the calendar. Some people prefer to start on the 1st of a month to align with pay cycles and billing dates; others find that starting immediately on the day they read this is more effective than waiting for a convenient start date that may never arrive. The single most important condition for starting is having your prior 30 days of transaction history available for the Month 1 audit. Pull your bank and card statements before Day 1. If you start today, you can pull the last 30 days from your online banking immediately. The most effective start date is always today.References

Intuit — 2026 Financial Forecast: Staying Mindful Amid Money Stress (January 2026) https://www.intuit.com/blog/innovative-thinking/2026-financial-forecast-mindful-stress/CivicScience — Living Paycheck to Paycheck in an Era of Financial Distress (March 2026) https://civicscience.com/living-paycheck-to-paycheck-in-an-era-of-financial-distress-and-survival-mode-mentality/

Ramsey Solutions — The State of Personal Finance in America Q4 2025 (February 2026) https://www.ramseysolutions.com/budgeting/state-of-personal-finance

Wealthvieu — Paycheck to Paycheck Statistics: How Many Americans Are Struggling? 2026 https://wealthvieu.com/personal-finance/income/paycheck-to-paycheck-statistics/

CNBC Select — 5 Best Free Budgeting Tools of 2026 (April 2026) https://www.cnbc.com/select/best-free-budgeting-tools/

Financial Freedom 101 — Budget Tracking in 2026: Why Modern Dashboards Outperform Spreadsheets (March 2026) https://financial-freedom-101.com/budget-tracking-in-2026-why-modern-dashboards-outperform-spreadsheets/

WalletHub — Personal Finance Statistics 2026 (April 2026) https://wallethub.com/edu/personal-finance-statistics/147459

0 Comments Comments